Guides · Property investment

Property Investment in Kenya: The Complete 2026 Guide for Foreigners

Property Investment in Kenya: The Complete 2026 Guide for Foreigners

Yes, foreigners can invest in Kenyan property — and plenty of Americans, diaspora Kenyans and other expats do. The catch is the kind of title you’re allowed to hold. As a non-citizen you can own property on a 99-year leasehold, not freehold, and you can’t buy agricultural land. In practice that makes a Nairobi apartment, a town house, or units in a listed property fund the cleanest ways in.

This is the honest overview — the hub for everything else we’ve written on the subject. It covers why people invest here, exactly what you can and can’t own, how the buying process runs, what it costs in fees and taxes, how financing works, what prices and rental yields actually look like in 2026, the hands-off REIT route, the diaspora angle, and the risks that catch people out. Each section links to a deeper guide if you want the detail.

One thing up front: this is general guidance, not legal or tax advice. Kenyan land law is specific and the penalties for getting it wrong are real. Before you sign or send money, use your own advocate — never the seller’s.

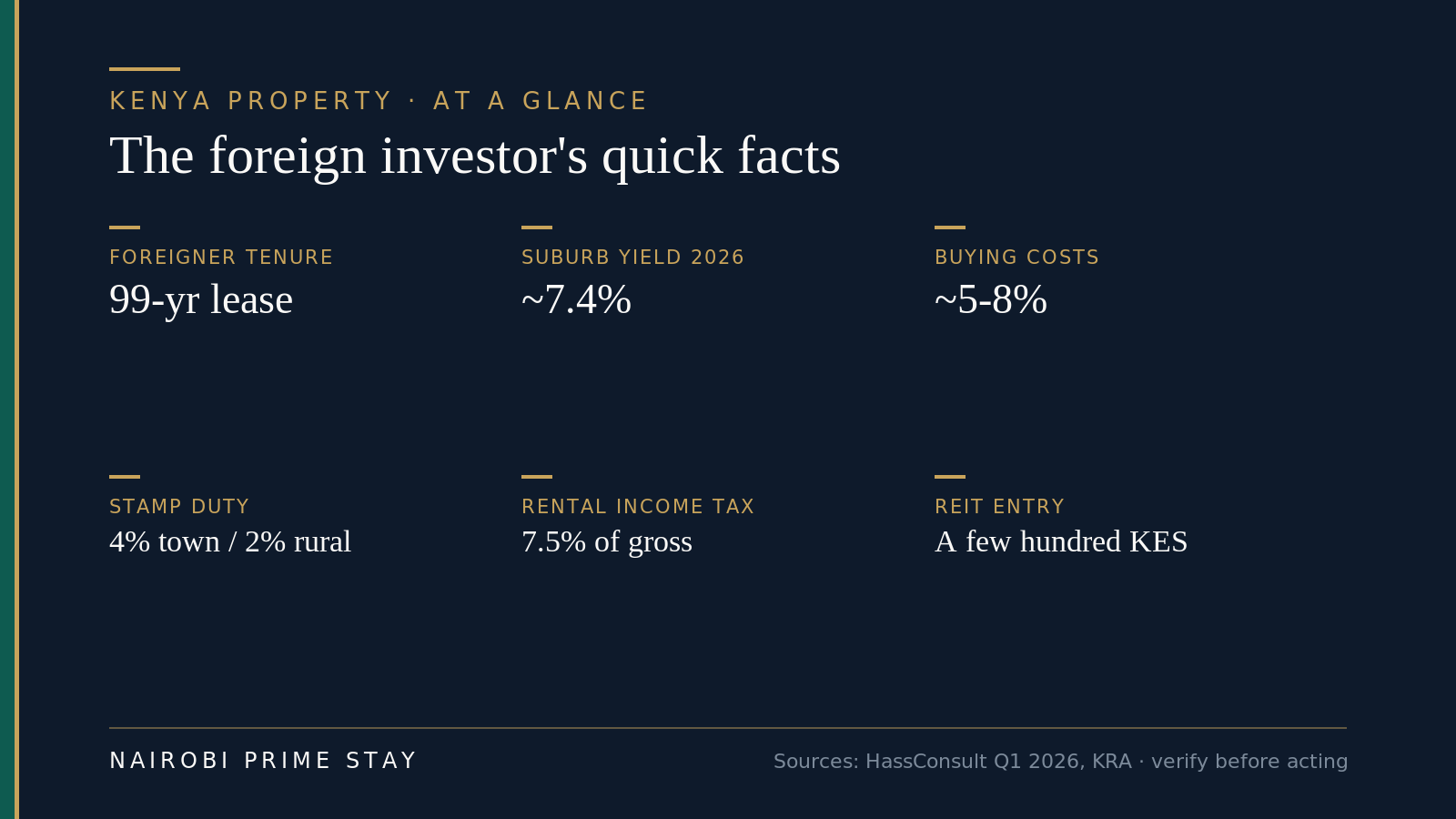

The short version (TL;DR). Foreigners can invest in Kenyan real estate, but only on leasehold of up to 99 years — no freehold, no agricultural land. The simplest routes are a Nairobi apartment on a sectional title, or REIT units on the Nairobi Securities Exchange from as little as a few hundred shillings. Buying costs run roughly 5–8% on top of the price (stamp duty 4% in towns, legal fees ~1.5–2%), and Nairobi-suburb rental yields held at about 7.4% in early 2026 — though prices in some oversupplied prime suburbs have fallen. Most foreign buyers pay cash; local mortgages are expensive. Do an official title search, hire your own advocate, and never wire money for a place you haven’t verified. It’s a real opportunity with real pitfalls — go in slowly.

The foreign investor’s quick facts for 2026. Sources: HassConsult Q1 2026 and the KRA, verify any figure before you act.

The foreign investor’s quick facts for 2026. Sources: HassConsult Q1 2026 and the KRA, verify any figure before you act.

Why invest in Kenyan property?

Nairobi is East Africa’s business and diplomatic hub, and that’s the whole investment case in one sentence. The UN’s only headquarters in the global south sits here. Embassies, multinationals, NGOs, regional banks and a large student population all need somewhere to live, and a lot of them rent. That’s steady, dollar-friendly tenant demand in the prime suburbs — exactly the housing we help people find.

The numbers back the income story. HassConsult’s Q1 2026 index put Nairobi-suburb residential rental yields at about 7.4% — the highest since 2007 — with satellite towns at about 5.3%, where the average rent has just crossed KES 64,765 a month. For an income investor used to 3–4% gross yields in a US city, that’s a meaningful step up.

Here’s the honest other side. Capital growth is patchy and, in places, negative. Years of apartment building have left parts of the prime market oversupplied. HassConsult’s Q1 2026 index still shows apartment prices sliding in the most over-built pockets, with Westlands down 2.8% and Upper Hill down 2.5% in that quarter alone, even as undersupplied suburbs like Lavington and Kilimani rose; over the longer run the worst-hit prime suburbs fell 7–11.5% as that supply landed. The Kenyan shilling has also lost value against the dollar over the long run, which eats into returns when you eventually convert back. So Kenya tends to reward the investor who buys for rental income and holds, not the one chasing a quick flip.

If you’re weighing this as part of a wider move, our complete guide to moving to Nairobi covers the life side — visas, neighborhoods, schools and healthcare — and the cost of living in Nairobi sets the day-to-day budget your rental income would sit against.

What foreigners can and can’t own

As a non-citizen, you can hold Kenyan property on leasehold tenure only, for a maximum of 99 years. That’s set by Article 65 of the Constitution. You can’t hold freehold, and you can’t buy agricultural land without consent from the State. Those are the rules that shape every foreigner’s strategy here.

What a non-citizen can and can’t own. Article 65 of the Constitution of Kenya 2010 caps foreign ownership at a 99-year leasehold — confirm your specific case with a Kenyan advocate.

What a non-citizen can and can’t own. Article 65 of the Constitution of Kenya 2010 caps foreign ownership at a 99-year leasehold — confirm your specific case with a Kenyan advocate.

A few practical points sit behind that picture:

- Apartments are the clean route. Most foreign buyers buy a flat on a sectional title (under the Sectional Properties Act 2020) or a long leasehold. The title is registered in your name, it’s straightforward to verify, and there’s no agricultural-land complication.

- “99 years” is the maximum, not what you get. If a lease was granted in 1980 for 99 years, a buyer in 2026 inherits the years that are left — roughly 53 — not a fresh 99. Always check the unexpired term and ask about renewal.

- The company workaround usually doesn’t work. A company counts as Kenyan only if it’s 100% owned by citizens. Put a single foreign shareholder in and it’s a non-citizen entity, still capped at leasehold. Courts have struck down shell structures designed to get a foreigner freehold land.

- Marriage and citizenship change the math. Kenyan citizens (including many in the diaspora) can hold freehold. A foreign spouse doesn’t automatically gain that right.

The plain-English version of the law lives in our guide to whether foreigners can buy property in Kenya, and the different title types — freehold, leasehold, sectional — are explained in title deeds in Kenya.

How the buying process works

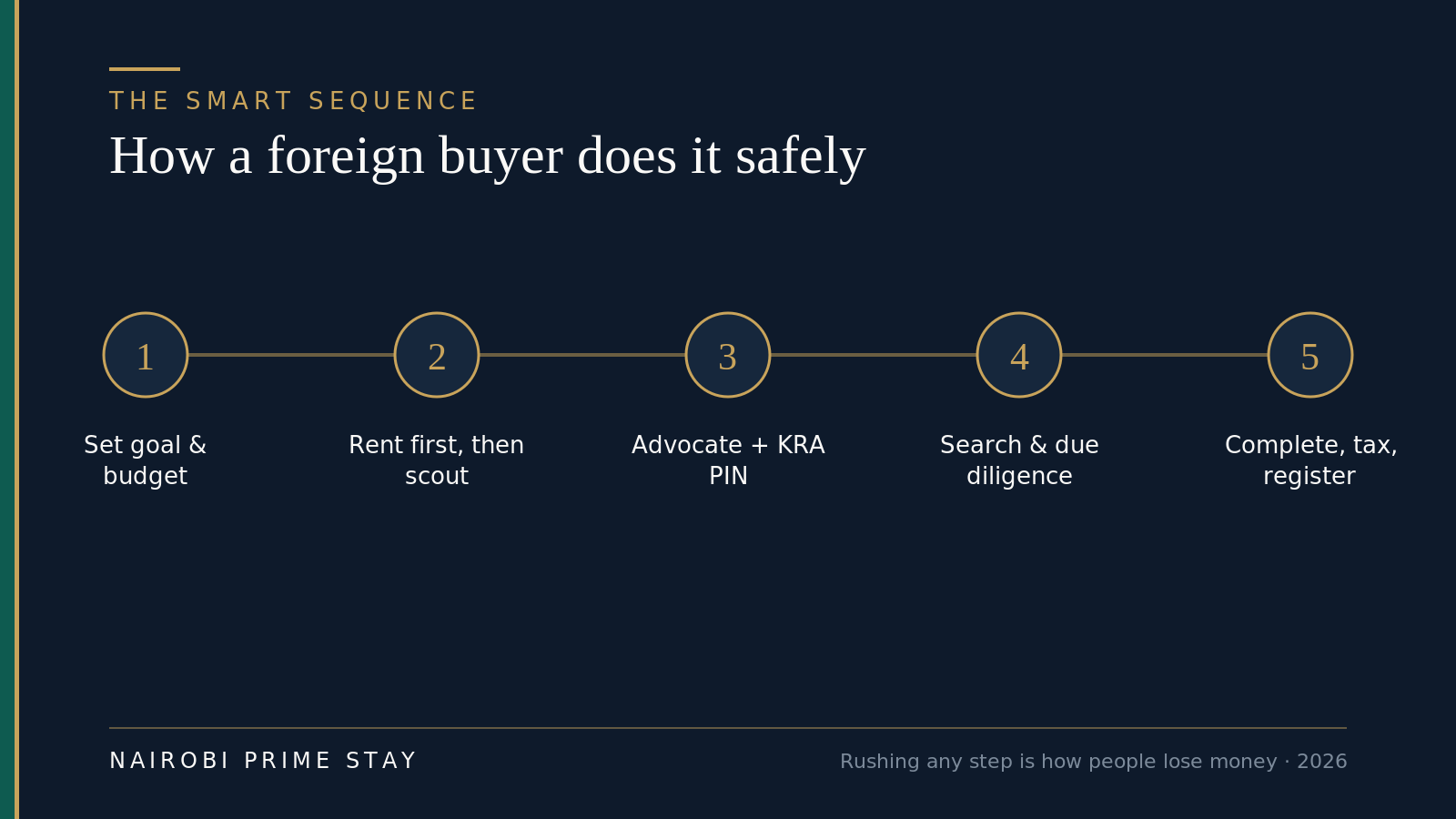

Buying a property in Kenya follows a clear sequence, and the order matters — most of the money is lost by people who skip a step. Here’s the shape of it.

The safe sequence for a foreign buyer. Rushing the search or due-diligence step is the single most common way people lose money.

The safe sequence for a foreign buyer. Rushing the search or due-diligence step is the single most common way people lose money.

In a bit more detail, you’ll usually: find a property and agree a price; engage your own advocate; get a KRA PIN (the tax ID you need to transact); run an official title search at the land registry or on the ardhisasa portal; sign a sale agreement and pay a deposit (often around 10%) into the advocate’s account, not the seller’s; complete due diligence; pay the balance on completion; pay stamp duty; and finally register the transfer into your name. For a clean apartment with good title, the whole thing often takes about six to twelve weeks.

Two people do the heavy lifting. Your advocate runs the legal side — the search, the agreement, the consents and the registration. A registered valuer confirms the price is sane and is needed for the stamp-duty assessment. For land or a stand-alone house you’ll often add a surveyor to confirm the boundaries.

We cover the full walk-through in how to buy property in Kenya step by step, the lawyer’s side in conveyancing in Kenya, and the extra care that land (as opposed to an apartment) demands in buying land in Kenya.

What it costs: fees and taxes

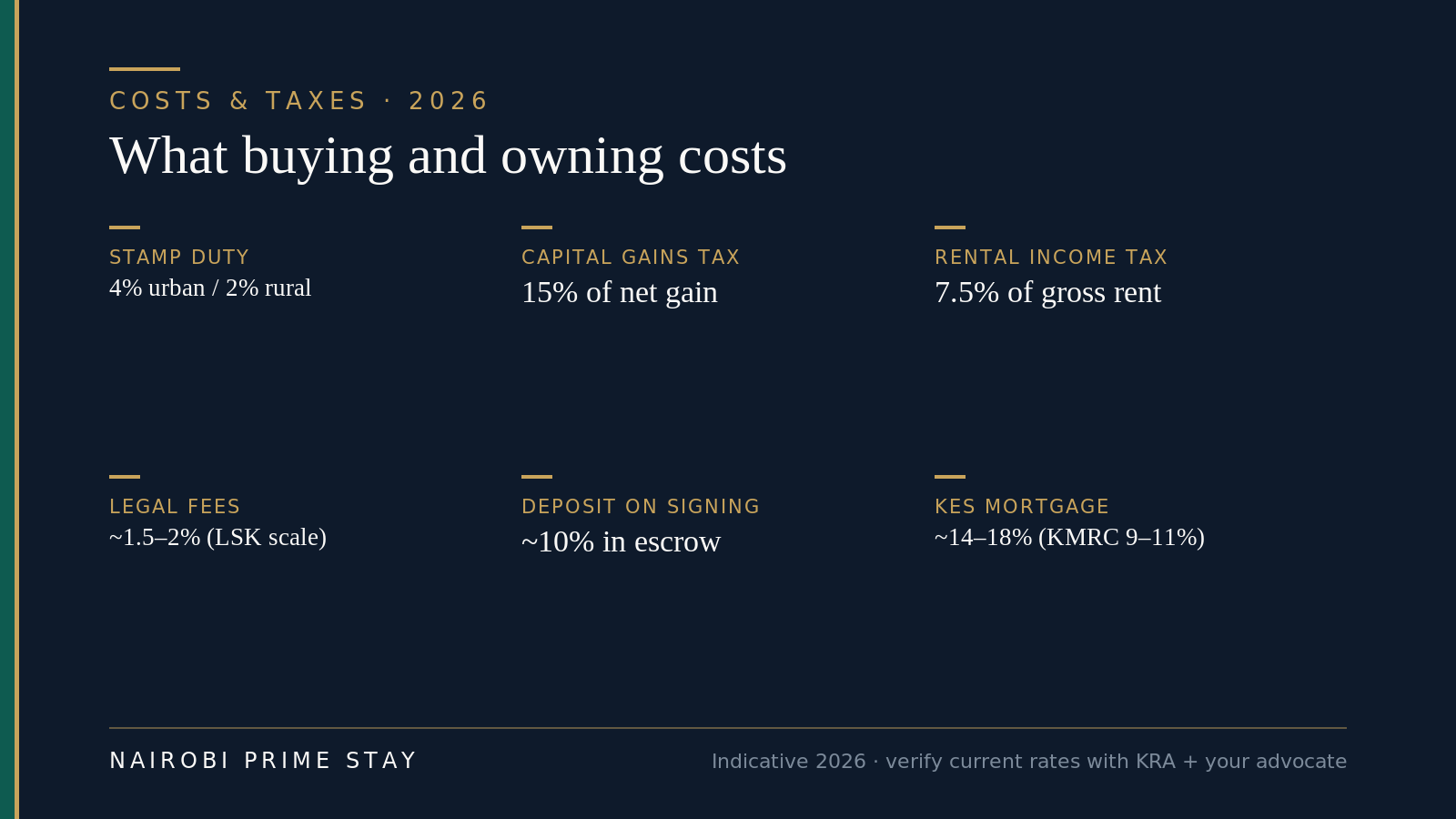

Budget roughly 5–8% of the purchase price for transaction costs on top of the price itself, then a few ongoing taxes once you own. None of it is exotic, but it adds up, so price it in before you offer.

Indicative 2026 costs and taxes. Verify the current rates with KRA and your advocate before you budget — tax rules change with each Finance Act.

Indicative 2026 costs and taxes. Verify the current rates with KRA and your advocate before you budget — tax rules change with each Finance Act.

The one-off costs at purchase:

| Cost | Indicative 2026 rate | Who pays |

|---|---|---|

| Stamp duty | 4% of value in a town/city, 2% rural | Buyer |

| Legal/advocate fees | ~1.5–2% (LSK remuneration scale) | Buyer |

| Valuation, search, registration | Smaller fixed fees | Buyer |

| Deposit on signing | ~10%, held by the advocate | Buyer (toward price) |

Two quick notes on stamp duty. Commercial property is charged at 6%, not 4%. And because a 2024 reclassification gazetted many former rural areas as urban, including parts of fast-growing Kiambu County, some plots that once paid 2% now attract the full 4%. It’s assessed on the government valuation or the price, whichever is higher.

The taxes you meet as an owner:

- Capital Gains Tax (CGT): 15% of the net gain when you sell, due within 30 days of the transfer. The seller pays, so it matters on your exit, not your entry.

- Residential rental income tax: 7.5% of gross rent for resident landlords earning between KES 288,000 and KES 15 million a year (the Monthly Rental Income regime, in force since January 2024). Earn more than KES 15 million and you move to normal income tax with deductions. A rise back toward 10% has been floated in the 2026 Finance Bill, so confirm the current rate with the KRA before you budget.

- Land rates and land rent: an annual county charge (land rates) and, on leasehold, an annual ground rent to the government. Small, but keep them current — arrears can block a future sale.

US citizens have a second layer: the IRS taxes you on worldwide income, so Kenyan rent and gains are reportable at home too, and foreign accounts may trigger FBAR/FATCA filings. There’s no US–Kenya double-tax treaty, so you lean on the Foreign Tax Credit instead. This is exactly where a cross-border tax professional earns their fee. Our Kenya visa guide for Americans touches on residency and the 183-day tax line; the full tax picture is in property taxes in Kenya.

Financing your purchase

Most foreign buyers in Kenya pay cash, and there’s a simple reason: local mortgages are expensive. Standard KES mortgage rates in 2026 run about 14–18% a year, and many are variable, so they climb when the Central Bank Rate does. Borrowing shillings at those rates to chase a 7% rental yield rarely makes sense.

There are cheaper doors if you qualify. Loans backed by the Kenya Mortgage Refinance Company (KMRC) can land around 9–11%, and in 2026 a few banks ran promotional fixed rates as low as 8.9–8.99% (a Stanbic/KCB campaign running to mid-September 2026). These mostly target the affordable-housing bracket and Kenyan borrowers, so check eligibility. Banks typically want 10–20% down (80% loan-to-value is standard).

Diaspora mortgages are a real option if you hold Kenyan citizenship. KCB, Stanbic and Co-op all run diaspora products you can apply for from abroad, with the loan in shillings. The currency mismatch is the thing to watch: if you earn dollars and borrow shillings, a falling shilling quietly works in your favor on repayments, but a rising one doesn’t — model it before you commit.

For a new build, developer payment plans are common — pay a deposit and stage payments through construction, with the balance on handover. That spreads the cost but adds completion risk, which we’ll come back to. The financing routes, including who can borrow and at what deposit, are compared in financing property in Kenya.

Prices, yields and the 2026 market

Prices vary enormously by area and type, so treat any single number with suspicion and always check the date. As a rough 2026 marker, mid-range Kilimani apartments were trading around KES 120,000–165,000 per square meter. With the shilling near 129–130 to the dollar in mid-2026 (about 129.5), that’s the order of magnitude — but verify current asking prices before you act, because the market is moving.

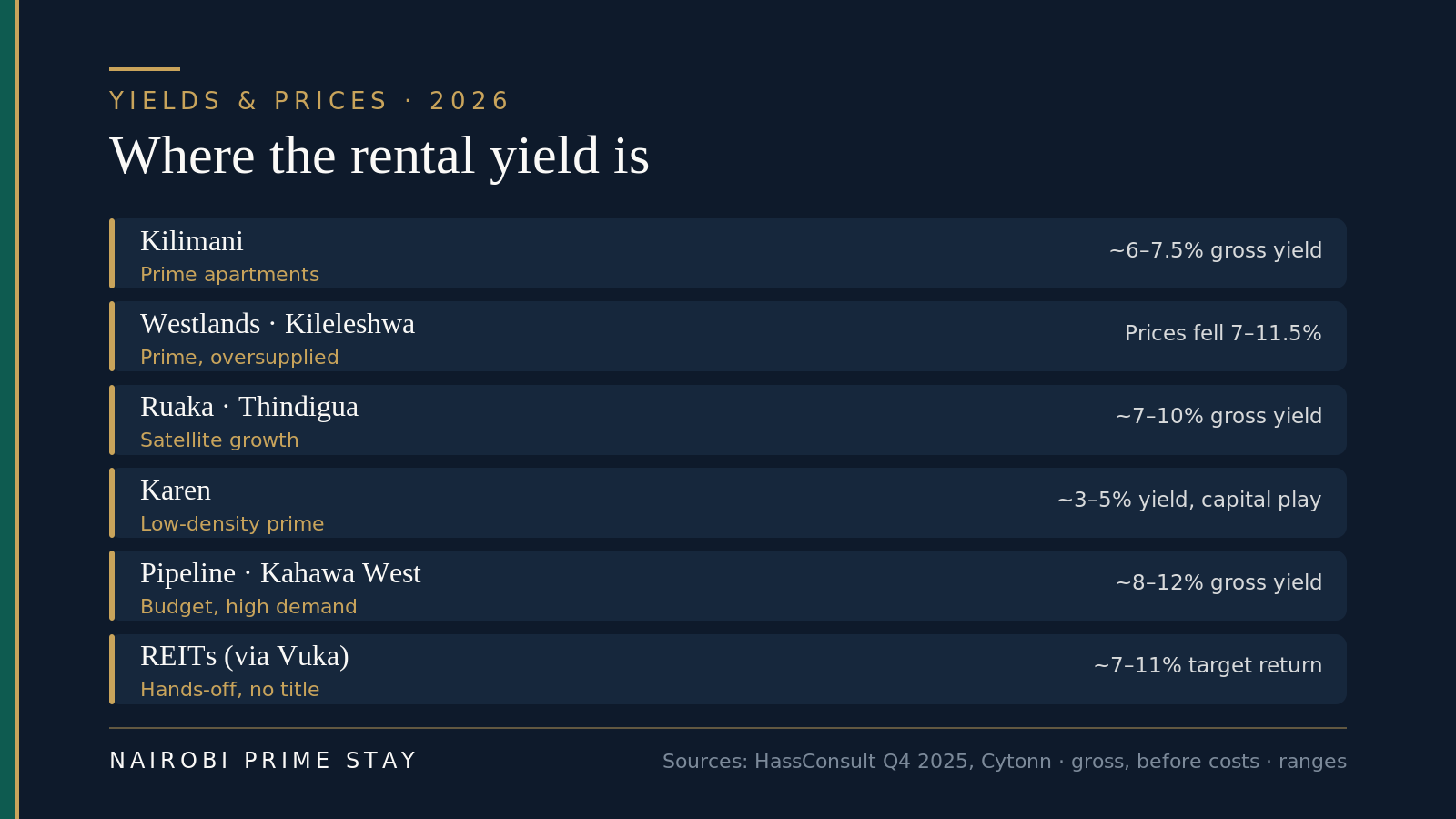

Where the rental yield is, as of 2026. Yields are gross and before costs; sources are HassConsult (Q1 2026) and Cytonn. Figures are ranges — confirm live data for any specific building.

Where the rental yield is, as of 2026. Yields are gross and before costs; sources are HassConsult (Q1 2026) and Cytonn. Figures are ranges — confirm live data for any specific building.

The pattern is consistent across the indices. The highest gross yields sit in budget, high-demand areas (Pipeline, Kahawa West and the like, often 8–12%) and in fast-growing satellite towns such as Ruaka, Syokimau and Ruiru (roughly 7–10%). Prime apartment suburbs like Kilimani and Westlands deliver more moderate yields (around 5–7.5%) but tend to attract more stable, longer-staying tenants — the embassy, UN and corporate crowd. Low-density prime areas like Karen yield the least (3–5%) because you’re really buying land and lifestyle, with capital appreciation as the play.

So the investor’s trade-off is clear: chase yield in the affordable and satellite markets, or chase tenant quality and resale liquidity in prime. Many expat-focused landlords pick prime precisely because the tenants are reliable and pay in hard currency. We go deeper in Nairobi property prices and market trends, rank the areas in best areas to invest in Nairobi real estate, and run the rental-landlord math in buy-to-let in Nairobi.

The hands-off route: Kenya REITs

If you want Kenyan property exposure without a title, an advocate or a tenant, a Real Estate Investment Trust (REIT) is the answer. A REIT is a fund that owns income-producing property and pays most of its rent out to unit-holders. You buy units on the Nairobi Securities Exchange, and as a foreigner you can hold them freely — none of the leasehold or agricultural-land rules apply.

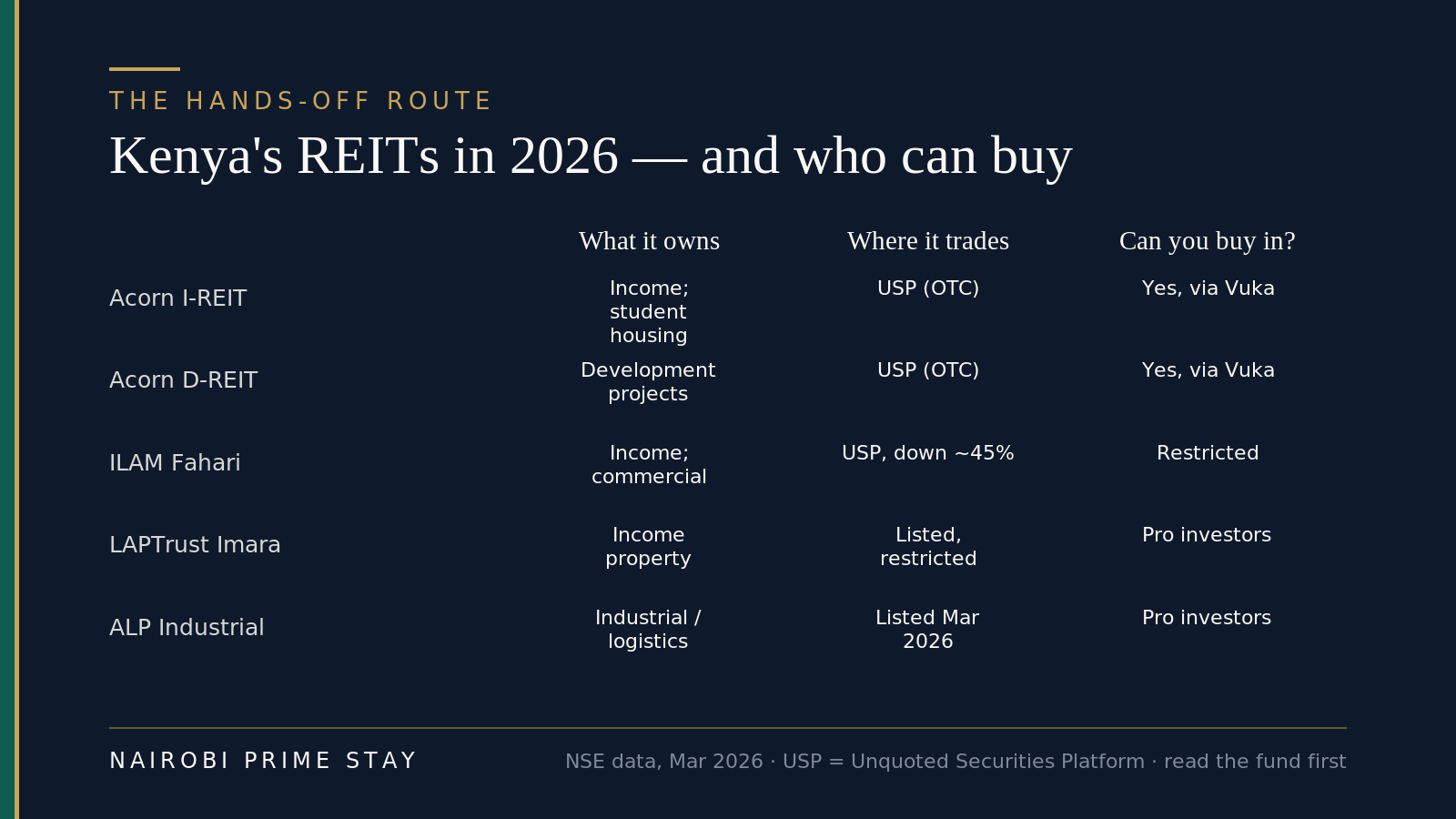

Kenya’s REITs in 2026, and who can actually buy in. USP is the NSE’s over-the-counter Unquoted Securities Platform. Read the fund before you buy.

Kenya’s REITs in 2026, and who can actually buy in. USP is the NSE’s over-the-counter Unquoted Securities Platform. Read the fund before you buy.

The entry price is the headline. Through Acorn’s Vuka platform you can start with as little as a few hundred shillings — the kind of money that doesn’t get you a parking space, let alone an apartment. But be clear about which funds a small investor can actually reach. As of 2026 the realistic retail route is Acorn: its income-focused I-REIT and development-focused D-REIT trade on the Nairobi Securities Exchange’s Unquoted Securities Platform (USP), an over-the-counter segment, and you buy in through the Vuka app. The other names are harder to get into: the LAPTrust Imara I-REIT and the new ALP Industrial REIT (which listed on 11 March 2026) sit on the NSE’s restricted segment, aimed at professional and institutional investors, and the ILAM Fahari I-REIT also trades on the USP. The whole listed REIT market is still small, on the order of KES 25 billion.

Returns have been mixed, which is the honest caveat. Acorn’s funds have grown: combined net operating income across Kenya’s REITs rose about 28% in the 2025 financial year, led by Acorn’s development REIT, and the Acorn I-REIT has targeted roughly 7–10% a year and traded up since launch; LAPTrust Imara has paid a dividend around 8%. But the ILAM Fahari I-REIT is the cautionary tale: by early 2026 it had fallen about 45% from its KES 20 launch price to around KES 11 — proof that “REIT” doesn’t mean “safe.” It’s a small, young, fairly illiquid market, so read the specific fund, weighing its assets, its track record and how easily you could sell, before you buy. We break the options down in our guide to Kenya REITs.

A REIT is the natural starting point if you want to test Kenyan property with money you can afford to leave alone, or to balance a direct apartment purchase with something liquid.

Getting your money back out

Think about the exit before you buy. It’s the part newcomers skip. A direct property is an illiquid asset: selling an apartment in a soft market can take months, and you pay the agent and advocate again on the way out. So Kenyan property suits money you won’t need in a hurry.

Three things shape what you actually walk away with:

- Capital Gains Tax. You pay 15% of the net gain when you sell, due within 30 days of the transfer. Keep your purchase records and the receipts for any improvements, because they reduce the taxable gain.

- Getting the proceeds home. Kenya has no exchange controls, so you can convert shillings to dollars and send the money out through a bank. The catch is the rate: if the shilling has weakened since you bought, your dollar return shrinks. Our USD to KES currency guide explains the spread, and our guide to sending money to and from Kenya covers the mechanics.

- Liquidity by route. REIT units are easier to exit than a building, since you can sell them on the platform, but the market is thin, so a large sell order can move the price. Land is the hardest thing to offload quickly.

None of this is a reason not to invest. It’s a reason to buy for income, hold for years, and treat the eventual sale as a slow, planned move rather than an emergency.

The diaspora and returning-American angle

Kenya actively courts diaspora investment, and the property market is one of the biggest places that money lands. If you hold Kenyan citizenship — including dual citizens and many in the wider diaspora — you’re treated as a citizen for land: you can own freehold, access diaspora mortgages, and buy agricultural land. That’s a materially stronger position than a non-citizen has.

For African Americans exploring a move “home,” the distinction is worth being precise about. Heritage and belonging are real, but they don’t by themselves confer Kenyan citizenship, so without it you invest under the non-citizen rules — leasehold apartments, REITs, the routes in this guide. That’s still a perfectly good position to invest from; just go in with the right expectations. The dedicated walk-through is diaspora property investment in Kenya.

Whichever bracket you’re in, the soft-landing advice is the same: spend time on the ground before you buy. A month in a serviced apartment while you scout areas, meet advocates and watch the traffic beats buying off a website from 8,000 miles away.

The risks — and the scams

Property fraud is the real risk in Kenya, and it’s worth more than a footnote. The classic schemes: a “seller” who doesn’t actually own the land, the same plot sold to several buyers, forged titles, and plots that turn out to sit on a road reserve or riparian (river) land that can’t be built on. Land is far more exposed to this than a registered apartment, which is one more reason most foreigners start with a flat on a clean sectional title.

The defenses are boring and they work:

- Run an official search at the land registry or on ardhisasa before any money moves, and again just before completion.

- Use your own advocate, never the seller’s, and never one the seller “recommends.”

- Hold the deposit in the advocate’s account, released against verified title — not paid to the seller directly.

- Never wire money for a property you (or your representative) haven’t physically verified. This single rule prevents most disasters.

Beyond fraud, price the market risks too: oversupply has pushed some prime apartment prices down, the shilling can weaken against the dollar, and off-plan buyers carry the risk that a developer stalls or never finishes. The full playbook is in property scams in Kenya and how to avoid them and the land-specific checks in buying land in Kenya.

How it plays out: a realistic example

Say you’re an American couple, both on remote salaries, who’ve decided to spend a few years in Nairobi. You want somewhere to live that also makes financial sense.

The cautious version goes like this. You arrive on an eTA, book a serviced apartment in Kilimani for the first month, and use it to scout. You meet two advocates, settle on one, and get your KRA PIN. You find a two-bed on a clean sectional title and offer. Your advocate runs the search, you sign and place 10% in their account, due diligence comes back clean, and you complete and register about ten weeks later. You pay 4% stamp duty and ~2% in fees. You live in it. If you leave, the expat rental demand in Kilimani means you can let it at a 6–7% gross yield, paying 7.5% rental tax on the rent, and you keep a foothold in the market.

The hands-off version is shorter. You decide you don’t want to be a landlord at all, so you put a slice of capital into a REIT through Vuka, keep renting your home, and stay liquid. Less upside, far less hassle, no title to manage.

Neither is “right.” The point is to match the route to how much time, money and risk you actually want to take on.

Ways to invest, compared

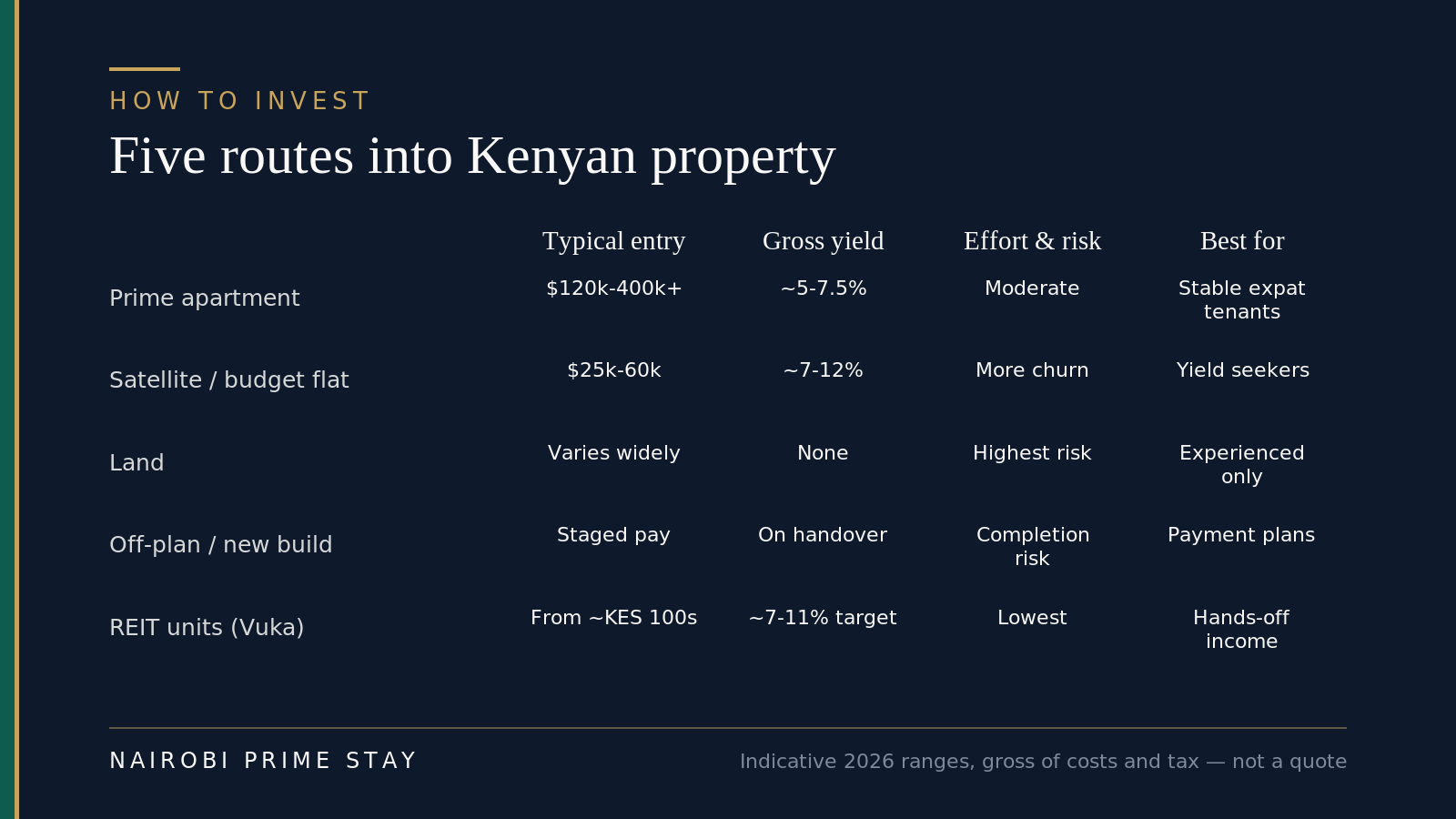

Five ways in, side by side. Indicative 2026 ranges, gross of costs and tax, not a quote.

Five ways in, side by side. Indicative 2026 ranges, gross of costs and tax, not a quote.

| Route | Typical entry | Indicative gross yield | Effort & risk | Best for |

|---|---|---|---|---|

| Prime apartment (buy-to-let) | $120k–400k+ | ~5–7.5% | Moderate; clean title, real tenants | Expat-focused landlords wanting stable, hard-currency tenants |

| Satellite/affordable apartment | $25k–60k | ~7–12% | Higher tenant churn; verify the developer | Yield-focused investors comfortable managing turnover |

| Land | Varies widely | None until developed | Highest — fraud risk, no income | Experienced buyers with local help and patience |

| Off-plan / new build | Staged payments | Depends on completion | Completion + developer risk | Buyers wanting payment plans and new stock |

| REIT units (NSE/Vuka) | From a few hundred KES | ~7–11% target | Lowest; liquid, no title | Anyone testing the market or wanting hands-off income |

Indicative 2026 ranges for orientation, not a quote. Yields are gross and before costs and tax.

The honest pros and cons

| The case for | The case against |

|---|---|

| Strong rental yields (~7% citywide) vs many Western cities | Capital growth is patchy; some prime prices have fallen |

| Deep, dollar-paying expat/diplomat tenant demand | Shilling can weaken against the dollar over time |

| Apartments on sectional title are clean and verifiable | Land carries real fraud risk; do heavy due diligence |

| REITs let you start tiny and stay liquid | REIT market is small, young and uneven |

| Foreigners are clearly allowed in (leasehold) | No freehold, no agricultural land as a non-citizen |

| Local mortgages exist | …but they’re expensive (~14–18%), so most pay cash |

The smart sequence — your checklist

- Decide your goal: rental income, capital growth, a home, or hands-off exposure.

- Set a budget that includes ~5–8% in transaction costs.

- Spend time on the ground first — a serviced apartment beats buying blind.

- Engage your own advocate (not the seller’s).

- Register a KRA PIN.

- Shortlist clean-title apartments — or pick a REIT for the hands-off route.

- Run an official title search before any money moves.

- Sign the sale agreement; place the deposit in the advocate’s account.

- Complete due diligence, pay the balance, pay stamp duty, register the transfer.

- Get cross-border tax advice if you’re a US person.

Frequently asked questions

Can foreigners buy property in Kenya?

Yes. Non-citizens can own Kenyan property on leasehold tenure for up to 99 years, under Article 65 of the Constitution. You can’t hold freehold, and you can’t buy agricultural land without State consent. In practice the cleanest route is a Nairobi apartment on a sectional title, or REIT units on the stock exchange.

Can an American buy an apartment in Nairobi?

Yes. Americans and other non-citizens routinely buy Nairobi apartments on a long leasehold or sectional title. You’ll need a KRA PIN (tax ID) and your own advocate to transact, and the title is registered in your name. You just can’t get freehold tenure as a non-citizen.

How much does it cost to buy property in Kenya?

Budget roughly 5–8% of the price in transaction costs on top of the price itself. The main items in 2026 are stamp duty (4% of value in towns and cities, 2% rural), legal fees of about 1.5–2%, and smaller valuation, search and registration fees. Confirm current figures with your advocate.

What taxes do you pay on property in Kenya?

At purchase you pay stamp duty (4% urban, 2% rural). When you sell, Capital Gains Tax is 15% of the net gain, due within 30 days. Rental income is taxed at 7.5% of gross rent for resident landlords earning KES 288,000–15 million a year. There are also annual land rates and, on leasehold, ground rent. US citizens must also report income and gains to the IRS.

What rental yield can you get in Nairobi?

Citywide residential rental yields were about 7.4% in late 2025, the highest since 2007. Prime apartment suburbs like Kilimani and Westlands run roughly 5–7.5%, satellite and budget areas often 7–12%, and low-density Karen around 3–5%. These are gross figures before costs and tax, and they change — verify current data for any specific building.

Can a foreigner get a mortgage in Kenya?

Yes, but local mortgages are expensive — standard KES rates run about 14–18% in 2026, so most foreign buyers pay cash. KMRC-backed loans can reach 9–11%, and diaspora mortgage products from banks like KCB, Stanbic and Co-op are open to Kenyan citizens abroad. Banks usually want 10–20% down.

How do I avoid property scams in Kenya?

Land fraud is the real risk — fake titles, plots sold twice, or sellers who don’t own the land. Protect yourself: run an official title search at the registry or on ardhisasa, use your own advocate rather than the seller’s, hold the deposit in the advocate’s account, and never wire money for a property you haven’t verified. A registered apartment is much lower-risk than raw land.

What is the best property investment in Kenya for a foreigner?

It depends on your goal. For stable, hard-currency tenants, a clean-title apartment in a prime expat suburb is the classic choice. For higher yield, satellite and affordable areas pay more but turn over faster. For a hands-off start, REIT units let you invest from as little as a few hundred shillings with no title to manage.

Can foreigners invest in Kenyan REITs?

Yes, freely. REIT units trade on the Nairobi Securities Exchange and none of the leasehold or agricultural-land rules apply. Through Acorn’s Vuka platform you can start with a few hundred shillings. Returns have been mixed across funds, so read the specific REIT before you buy — it’s a small and fairly illiquid market.

What is the minimum amount to start investing in Kenyan property?

Less than people think, if you go the REIT route. Acorn’s Vuka platform lets you buy REIT units from a few hundred shillings, so you can get property exposure for the price of a nice dinner. A physical buy-to-let is a bigger commitment: satellite-town apartments start around KES 3 to 6 million (roughly $25,000 to $45,000), and prime Nairobi apartments from about $120,000. There’s no special minimum for a foreigner beyond the price of the asset and the 5 to 8 percent in costs on top.

Is 2026 a good time to invest in Nairobi property?

It depends on what you want from it. For rental income, yes: Nairobi-suburb yields held around 7.4% in early 2026, the highest on record, and expat demand is steady. For quick capital gains, be cautious, because apartment prices in over-built prime pockets like Westlands and Upper Hill were still sliding in early 2026, even as undersupplied suburbs like Lavington and Kilimani rose. The honest play in this market is to buy a clean-title apartment for income and hold it, not to flip. Always verify the numbers for the specific building before you commit.

Final thoughts

Kenyan property can be a genuinely good investment — the rental yields beat most Western cities, and the expat and diplomatic demand in Nairobi’s prime suburbs is real and pays in hard currency. But it rewards patience over hustle. Buy for income and hold, stick to clean-title apartments or REITs unless you’ve got local expertise, and treat every step of the legal process as non-negotiable. The people who lose money here almost always skipped the search or trusted the wrong person.

If you’re not ready to buy, you don’t have to. Renting first — ideally from a secure, fully-equipped base while you learn the city — is the smartest move most newcomers can make.

This guide is general information for 2026, not legal, tax or investment advice. Land law and tax rates change, and your situation is specific. Confirm the details with a Kenyan advocate and, for US tax, a cross-border professional before you act.

Related reading

- Moving to Nairobi: the complete guide — the relocation hub this sits under

- Can foreigners buy property in Kenya? — the law in plain English

- How to buy property in Kenya, step by step

- Property taxes in Kenya — every levy, with rates

- Best areas to invest in Nairobi real estate

- Buy-to-let in Nairobi — the landlord math

- Airbnb and short-let investment in Nairobi — the honest returns and the new rules

- Buying off-plan property in Nairobi — the discounts, the real risks, and how to vet a developer

- New developments and satellite cities around Nairobi — Tatu City, Konza, Tilisi, Northlands and Two Rivers, and the honest risks

- Building a house in Kenya vs buying — costs per square metre, the process, and building from abroad

- Commercial property investment in Nairobi — office, retail, industrial and mixed-use, by segment

- Kenya REITs explained — the hands-off route

- Diaspora property investment in Kenya — buying from abroad safely

- Property management in Nairobi — agents, fees and what to expect

- Common property scams in Kenya — the scams to know and how to avoid each one

- Cost of living in Nairobi and serviced apartments in Nairobi

Before you buy, live there for a month

The best due diligence is time on the ground. A serviced apartment for your first month gives you a secure, fully-equipped base — Wi-Fi, cleaning, backup generator and security included — while you meet advocates, scout areas and watch how the market actually behaves. It’s all-inclusive, on flexible monthly terms, and a $50 deposit reserves your dates with the balance paid on arrival.

Browse our serviced apartments, or tell our AI relocation assistant your budget and plans and it’ll shortlist options in a couple of minutes — a calmer way to start than buying off a website from abroad.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.