Guides · Property investment

Common Property Scams in Kenya and How to Avoid Them (2026 Guide)

Common Property Scams in Kenya and How to Avoid Them (2026 Guide)

Property fraud in Kenya is real, common, and almost entirely avoidable. That last part is the good news. Scams here look frightening from the outside, but they run on a short list of tricks — and the same small set of checks stops nearly all of them. If you do the official search, hire your own advocate, and never pay an individual in cash, you’ve closed most of the doors a fraudster needs open.

This guide is for anyone buying property in Kenya from a distance or for the first time: Americans relocating, diaspora buyers sending money home, and newcomers who don’t yet know which questions to ask. We’ll name the scams plainly, show you how each one works, and give you the defense for each. Then we’ll cover what to do if it has already happened to you.

We’re not trying to scare you off. Tens of thousands of people buy land and homes in Kenya every year and complete the deal cleanly. The buyers who lose money almost always skipped a step that takes a day and costs a few hundred shillings. By the end of this, you’ll know every step worth taking.

Quick answer (TL;DR)

Most property scams in Kenya come down to a few moves: a fake or duplicate title deed, someone selling land they don’t own, the same plot sold to several buyers, a fake agent who collects deposits and disappears, or an off-plan project that never gets built. You stop almost all of them with five habits. Run an official title search on Ardhisasa or eCitizen (roughly KES 500–1,000) before any money moves. Hire your own advocate, not the seller’s. Check that the seller’s ID matches the name on the title. Visit the site and have a licensed surveyor confirm the beacons. And never pay cash to an individual — send money to a completion or escrow account against a signed agreement. One more: refuse to be rushed. Pressure to “pay today” is the single most reliable sign of a scam.

Why this matters

Land is Kenya’s most valuable — and most disputed — asset, and the paperwork behind it has been fraud-prone for decades. The Ministry of Lands has estimated that more than 10% of title deeds in circulation may be fraudulent, and in 2024 it reported over 10,000 land-fraud cases under investigation, with losses running into billions of shillings. Fake titles have even been used to draw real bank loans, which is why lenders and investors lose money on them too.

The scale of the problem in 2026 — and the reassuring part: a handful of checks defeat most of it. Verify figures with the Ministry of Lands and ardhisasa.lands.go.ke.

The scale of the problem in 2026 — and the reassuring part: a handful of checks defeat most of it. Verify figures with the Ministry of Lands and ardhisasa.lands.go.ke.

Two groups get targeted more than anyone: foreign buyers and the diaspora. Both tend to buy at a distance, move large sums, and lean on a “trusted” contact on the ground — exactly the conditions a con needs. Foreign nationals have turned up among the victims even in Nairobi’s upscale estates. None of this should stop you investing. It should make you invest like a professional: slowly, on paper, and with people whose job is to protect you rather than to close the sale.

The government is closing gaps. A multi-billion-shilling digitization drive is moving records onto the Ardhisasa platform, where an official search returns the registered owner, the size and description of the parcel, and any loans, caveats or restrictions — in a day or so rather than weeks. That single tool, used before you pay, prevents a large share of the scams below.

How property scams actually work

Almost every property scam relies on three things lining up. Take away any one and the con usually collapses.

One: you skip the official record. Fraud lives in the gap between what a document looks like and what the registry actually says. A forged title can look perfect. The official search can’t be forged — it’s the government’s own record of who owns the land. Scammers need you to trust the paper in their hand instead of the record in the system.

Two: you pay an individual directly. Cash, or a transfer to a personal M-Pesa or bank account, is almost impossible to claw back. Legitimate purchases run money through an advocate’s completion account or an escrow arrangement, released only when the title transfers. Scammers need the money to land somewhere they control and can empty.

Three: you’re in a hurry. Every con artist manufactures urgency — “another buyer is viewing tomorrow,” “the price goes up next week,” “I can only hold it 24 hours.” Speed is the enemy of due diligence, and they know it. A real seller of real property can wait a week for your search to come back.

Keep those three levers in mind as you read. The specific scams change costume, but underneath they’re all trying to get you to skip the record, pay a person, and do it fast.

The most common property scams in Kenya

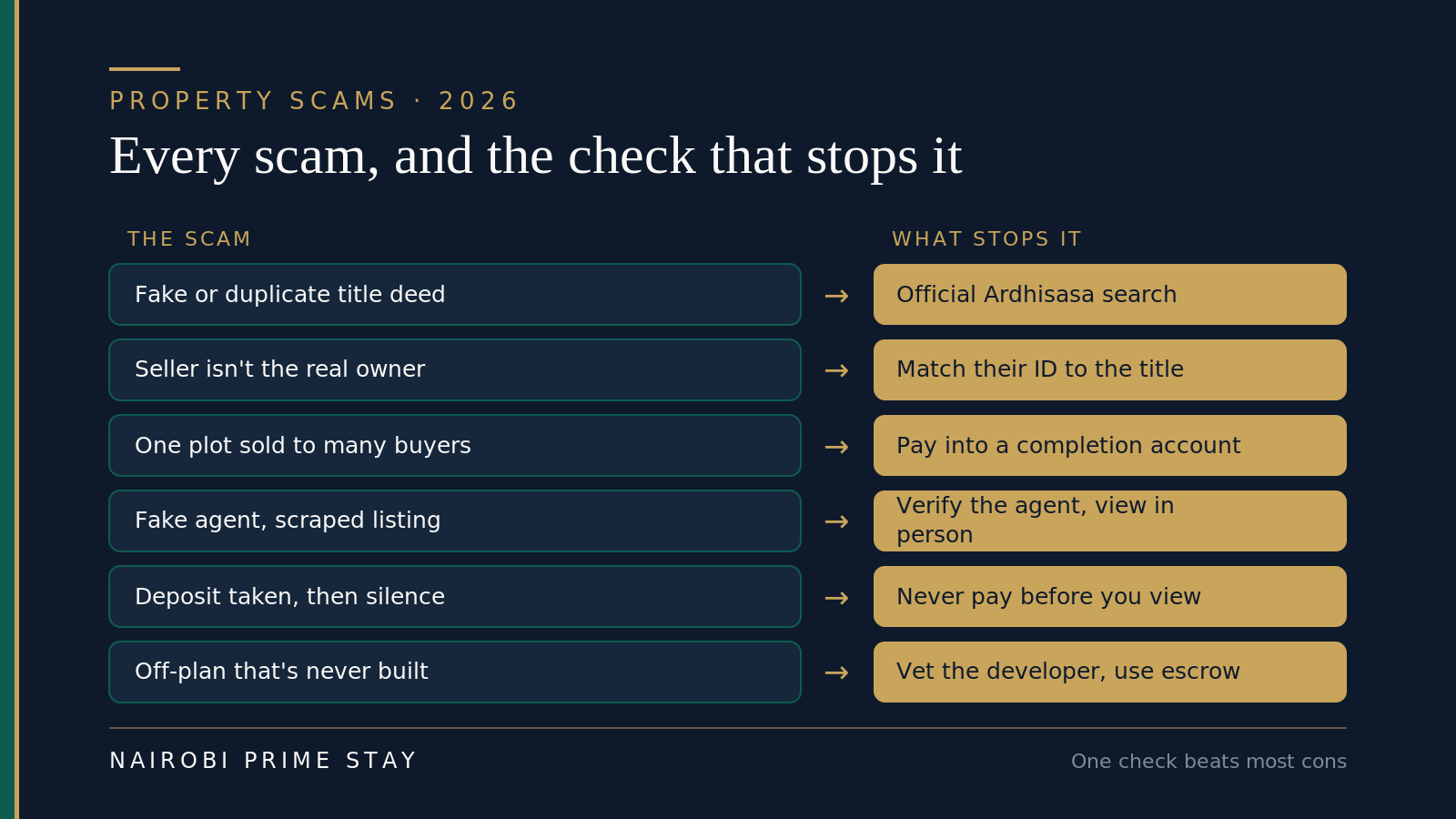

Here are the scams you’re most likely to meet, how each one works, and the check that beats it.

Each scam has a defense. Most are the same defense, applied early.

Each scam has a defense. Most are the same defense, applied early.

Fake or duplicate title deeds

The classic. A seller produces a title deed that’s either forged outright or a duplicate of a genuine one — same parcel number, different “owner.” The document can look flawless: right paper, right stamps, a convincing signature. Some duplicates are created with insider help at a registry, which is why they pass a casual eyeball test.

How it bites: you pay, “transfer,” and only later — sometimes years later — discover the real owner, or a second buyer holding the genuine title. Fake titles have even been used to take out bank loans against land the borrower never owned.

The defense: an official search. Pull the record yourself on Ardhisasa (or at the registry) and confirm the title number, the registered owner’s name, the parcel size, and that there are no surprise charges or caveats. Then have your advocate confirm the deed’s authenticity against the registry. A genuine Kenyan title carries security features — government seals and watermarks — but don’t rely on those alone; rely on the search.

Selling land the seller doesn’t own

Here the title is real, but the person selling it isn’t the owner. They might be a tenant, a caretaker, a relative, a broker who “has an arrangement,” or an outright impersonator using a stolen or forged ID. Grabbed public land and road reserves get sold this way too — land that was never anyone’s to sell.

How it bites: you buy from someone with no right to transfer, so you get nothing. The real owner appears later, and your “seller” is long gone.

The defense: match the human to the record. The name and ID of the person signing must match the registered owner on the search, full stop. If they’re acting for the owner, demand to see a registered, specific power of attorney — and verify it. Meet the actual owner where you can. Be doubly careful when someone says the title “is being transferred” or “is with my lawyer.”

Double-selling the same property

A dishonest seller or broker sells one plot or apartment to several buyers at once, collecting a deposit from each, then disappears. It happens fastest in hot markets where units move quickly — Kileleshwa and Kilimani are repeat settings.

How it bites: only one buyer, at most, can register the title. The rest are left chasing a vanished seller for a refund.

The defense: speed of registration and control of money. Run your search, then move to transfer promptly so the title is registered in your name before anyone else can. Crucially, hold your deposit and balance in a completion account controlled by your advocate, released only on registration — not handed over on a handshake.

Fake agents and brokers

Scammers scrape photos and details from a genuine listing, then pose as the agent on social media, classifieds or WhatsApp. The property may be real; the “agent” is not. A variant collects a “viewing fee” or “holding deposit” from several would-be renters or buyers for the same unit.

How it bites: you pay a deposit or fee to someone with no connection to the property, then they go quiet.

The defense: verify the agent and never pay before a real, in-person viewing. Registered estate agents can be checked against the Estate Agents Registration Board. Confirm the agent actually represents the owner. Treat any request to “pay to secure a viewing” as a red flag — that isn’t standard practice.

”Deposit and disappear”

The simplest con of all: you’re asked for a deposit to “hold” a property before you’ve seen it or done any checks. The money goes to a personal account, communication slows, then stops. It hits renters and buyers alike, and it’s especially common in the short-let and apartment market.

How it bites: your holding deposit is gone, and there was often no real property — or it was never theirs to let.

The defense: never pay to hold something sight-unseen. View in person (or send someone you trust), confirm ownership, and only pay against a signed lease or sale agreement, into a traceable account.

Off-plan projects that never finish

Buying off-plan — paying in installments while a development is built — can be a legitimate, discounted way in. But some projects stall for years or never break ground, and a few are pure fiction: a glossy brochure, a deposit request, no real site or approvals.

How it bites: you pay deposits and installments toward a building that never gets handed over, with weak legal protection because Kenya still has no dedicated off-plan law.

The defense: vet the developer hard and protect your money. Check their completed projects, their approvals (NCA, county and NEMA), and their financing bank. Insist your payments go into an escrow/stakeholder account released against construction milestones, with a firm completion date and penalties for delay. Our honest guide to buying off-plan in Nairobi walks through the contract clauses that matter.

Family-land and succession disputes

Not every loss is a stranger’s con. A lot of Kenyan land is family or ancestral land, and a single seller may not have the right to sell it alone — other heirs, a spouse, or the wider family may have a claim. Selling inherited land before succession is completed, or without everyone’s consent, is a recipe for a court case.

How it bites: you buy in good faith, then a relative of the seller emerges with a competing claim and the transaction unravels.

The defense: check how the seller acquired the land and whether succession is complete. For family or agricultural land, confirm spousal and family consents and any required Land Control Board consent. Your advocate’s search and questions will surface most of this before you commit.

The red flags that show up in almost every scam

Different scams, same tells. If you see one of these, slow down and verify before anything else — and if you see two, walk away.

Save this to your phone. The left column is where money disappears.

Save this to your phone. The left column is where money disappears.

- A price well below the market. A genuine bargain is rare; a too-good deal is usually bait. Ask why it’s cheap and verify the answer.

- Pressure and urgency. “Someone else is interested,” “the price rises next week,” “pay today.” Real deals survive a week of checks.

- Cash, or payment to a personal account. Any push toward untraceable money — cash, personal M-Pesa, a friend’s account — is a major warning.

- The seller won’t allow a search, or rushes the documents. Refusing an official search, or producing the title only at the last second, is disqualifying.

- The name doesn’t match. The seller’s ID must match the registered owner on the search. “I’m handling it for my uncle” needs a verified power of attorney.

- Frequent recent transfers. A title that changed hands two or three times in the past year can signal a chain of fraudulent transactions.

- No site visit, or a “different” plot. Photos only, vague directions, or beacons that don’t match the title diagram are reasons to stop.

- Off-market documents. An allotment letter instead of a title, a “share certificate” for land, or a deal run entirely on WhatsApp all need extra scrutiny.

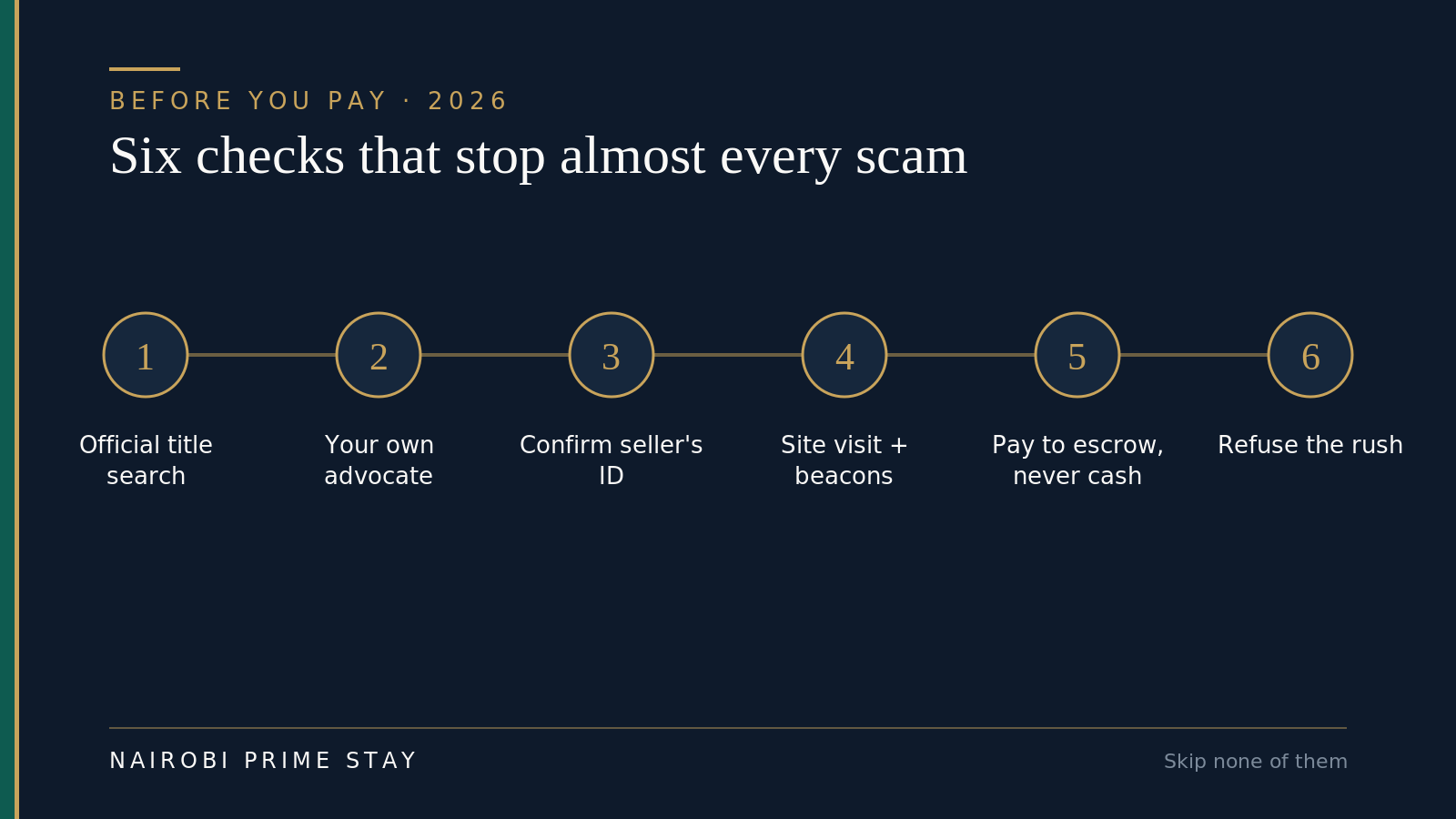

How to protect yourself: the checks that stop almost every scam

None of these is expensive or slow. Together they defeat the large majority of property fraud in Kenya. Do them in order, and don’t skip one because a deal “feels” right.

Six steps, in order. Each one closes a door a fraudster needs open.

Six steps, in order. Each one closes a door a fraudster needs open.

1. Run an official title search. Before any money, confirm ownership at the source. On Ardhisasa (ardhisasa.lands.go.ke), register with your ID and KRA PIN and pull a search for roughly KES 500–1,000 (about KES 1,000, plus a small fee, on eCitizen, which returns an official RL27 certificate valid six months). Ardhisasa is fully live for Nairobi and Murang’a; for other counties use the eCitizen land search or the county registry. The report shows the registered owner, parcel size and description, and any charges, caveats or restrictions, and it comes back within about one to three business days. This one step beats most title scams. See our guide to title deeds in Kenya for how to read what comes back.

2. Hire your own advocate. Not the seller’s, not the agent’s — yours. A registered advocate runs the legal due diligence, drafts the sale agreement, holds your money in a completion account, and registers the transfer. Conveyancing fees are modest next to the price of the property and tiny next to the cost of a scam. Our conveyancing guide explains exactly what they do.

3. Confirm the seller is the owner. Match the ID of the person signing to the name on the search. If they act through a power of attorney, see it, confirm it’s registered, and check it actually authorises this sale. Meet the real owner whenever you can.

4. Visit the site and confirm the beacons. Walk the actual plot. Hire a licensed surveyor to confirm the boundaries and beacons match the registry’s parcel diagram — this catches “wrong plot” and road-reserve scams. For a finished home, confirm the unit exists and matches the documents.

5. Pay into escrow or a completion account — never cash. Money should move only through traceable, regulated channels: a bank transfer or Wise into your advocate’s completion account or an escrow/stakeholder account, released when the title transfers. Never pay cash, and never send to a personal M-Pesa or an individual’s account.

6. Refuse to be rushed. Give yourself time for the search to return and the advocate to do their work. If a seller can’t wait a week, that tells you what you need to know.

Two more habits help, especially if you’re buying from abroad. Get independent eyes on the ground — a surveyor and a trusted person with no stake in the deal. And put nothing in the hands of an informal “fixer.” If you’re investing from overseas, our diaspora property guide covers buying safely at a distance, and our guide to whether foreigners can buy property in Kenya explains what you’re actually allowed to own.

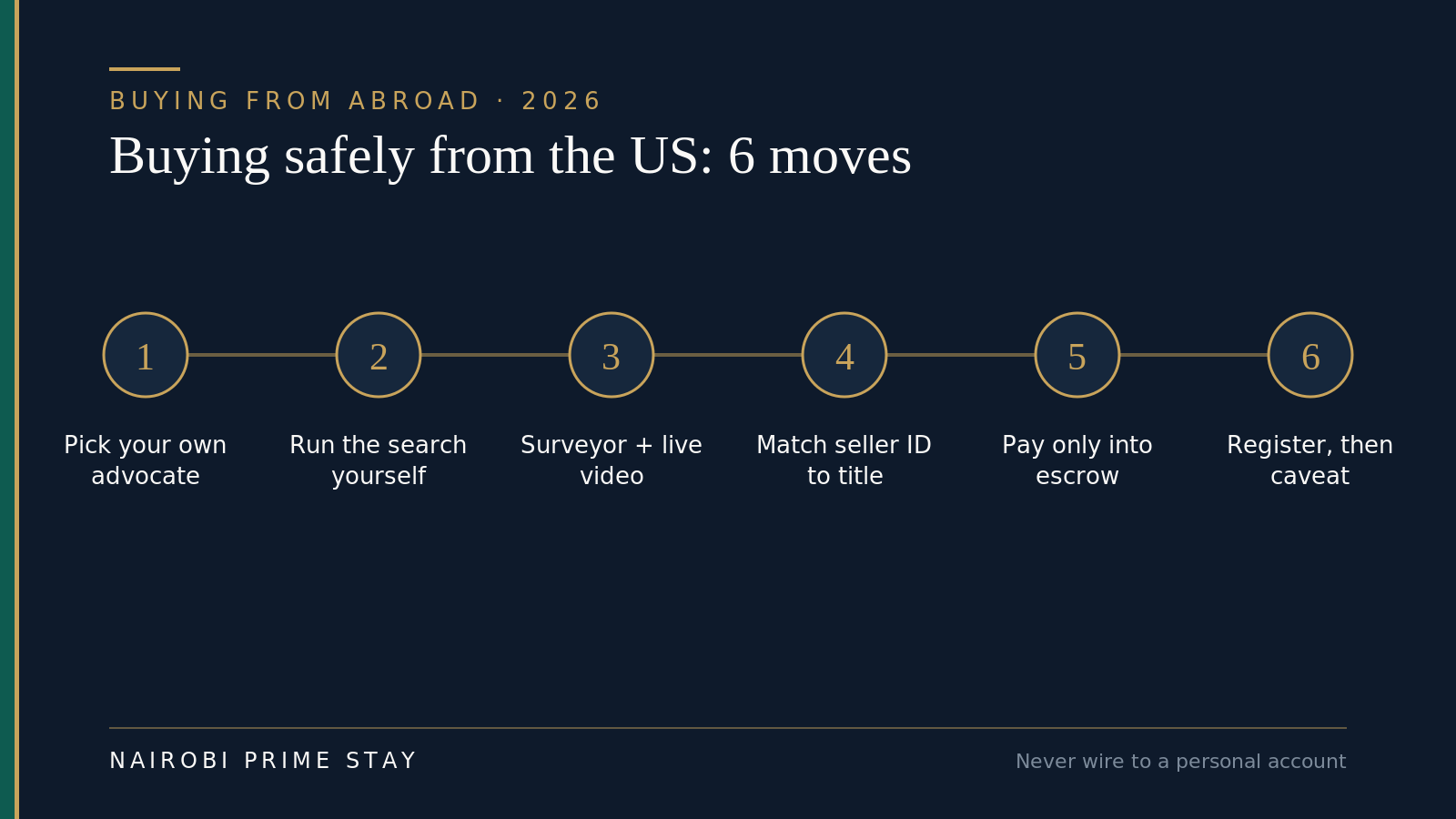

Buying from 8,000 miles away: the diaspora scam playbook

Distance is the fraudster’s favorite advantage. Kenya’s Ethics and Anti-Corruption Commission ranks property fraud among the top five scams reported to it, and it names the diaspora as the most-targeted victims — property fraud is the single most costly con hitting Kenyans abroad. Americans buying remotely walk into the same trap for the same reason: you can’t pace the plot, sit across from the seller, or read the room. Everything you’d normally sense in person has to be replaced by paperwork and by people you actually trust.

At a distance the cons wear slightly different costumes. Three are worth naming.

The absent-owner sale. Fraudsters hunt for land whose owner lives overseas, forge a title and a matching ID, and sell it to someone else — often another diaspora buyer. So if you already own land in Kenya and live in the US, you’re a target too, not just a buyer. Pull your own official search once or twice a year, and ask your advocate about lodging a restriction or caveat that blocks any transfer without your say-so.

The rogue off-plan developer. Some developers treat diaspora money as easy money: glossy renderings, a diaspora roadshow, a deposit request, then a building that stalls or never breaks ground. Distance means you never see the empty site. Vet the developer’s finished projects, approvals and financing bank as hard as you would at home, and never let payments leave escrow ahead of real construction milestones. Our honest guide to buying off-plan in Nairobi covers the clauses that protect you.

The trusted cousin who becomes the weak link. Nearly every diaspora buyer leans on one person on the ground. That’s sensible — but never let the same person choose the property, hold your money, and confirm the paperwork. Concentrating all of it in one pair of hands is exactly what gets abused, sometimes even by family who started out honest.

Six moves that stand in for being in the room. Each closes a gap a remote buyer can’t see across.

Six moves that stand in for being in the room. Each closes a gap a remote buyer can’t see across.

Here’s the remote-buyer version of the defense, tightened for the fact that you’re not there:

Hire your own advocate, and find them yourself. Don’t use the advocate the seller or agent “recommends.” Choose a registered advocate independently — the Law Society of Kenya keeps a directory — so their only job is protecting you. Our conveyancing guide explains what they should be doing.

Run the search yourself. You don’t need to be in Kenya. Register on Ardhisasa or eCitizen and pull the official search before any money moves, or have your advocate pull it and send you the report. Read it against the seller’s documents line by line.

Get independent eyes and a live video walkthrough. Send a licensed surveyor to confirm the beacons and a trusted person with no stake in the deal to stand on the land. Ask for a live video call from the plot with street signs and neighbors visible — not a pre-recorded clip, which is easy to fake or lift.

Move money the boring way. Wire only to your advocate’s client account or a regulated escrow, never to a personal M-Pesa or an individual’s bank account. Kenya has no exchange controls, so funds move in and, later, a sale’s proceeds move out freely; you just declare physical cash over about USD 10,000. Expect the shilling to drift — the US dollar bought about 129.4 shillings in mid-2026 — so build in a currency buffer and consider pricing large payments in dollars. Our guides to sending money to Kenya and the US dollar to shilling rate go deeper.

Register fast, then lock it. Once the transfer completes, register it in your name promptly and keep the digital records. If you’ll rent it out from abroad, use a licensed property manager rather than an informal contact — and, again, don’t let one person hold both the keys and the cash. Diaspora and returning African American buyers will find more of this playbook in our diaspora property investment guide and our African American relocation guide.

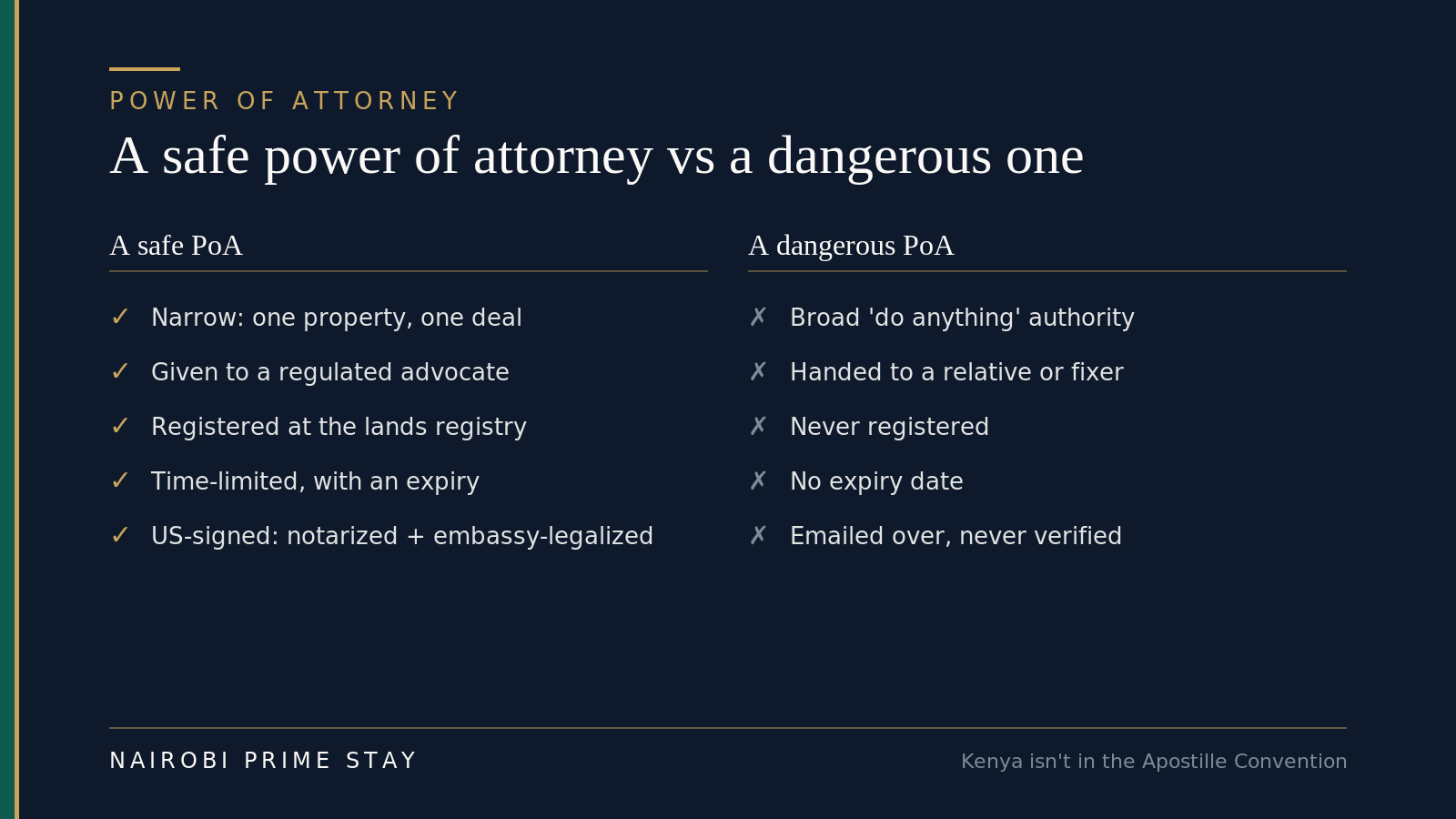

The power-of-attorney trap

A power of attorney lets someone act for you when you can’t be there — and it’s one of the most abused documents in Kenyan property fraud. It fails in two directions, and diaspora buyers meet both.

On the seller’s side, a con artist produces a power of attorney claiming to act “for the owner.” Forged PoAs turn up constantly, and they’re how a stranger sells land that was never theirs. On your side, you grant a PoA to a relative or a fixer so they can sign while you’re overseas — and they sell the property to themselves, quietly overpay a colluding seller for a kickback, or move the land into their own name.

The fix isn’t to avoid a power of attorney; sometimes you genuinely need one. The fix is to keep yours tight and to prove theirs.

A power of attorney is a tool, not a risk — as long as it’s narrow, registered, and in an advocate’s hands.

A power of attorney is a tool, not a risk — as long as it’s narrow, registered, and in an advocate’s hands.

Keep any PoA you grant narrow and specific: one named property, one transaction, with an expiry date, so it can’t be reused for anything else. Give it to a regulated advocate rather than an informal contact, so there’s professional accountability behind it. Register it at the lands registry so it’s on the record. And mind the cross-border step: a PoA you sign in the United States must be notarized and then legalized at a Kenyan embassy or consulate, because Kenya isn’t part of the Apostille Convention — a plain apostille stamp isn’t enough on its own.

For any PoA the other side relies on, treat it as a document to be proven, not trusted. Have your advocate confirm it’s registered and authentic against the registry, check that it actually authorizes this specific sale, and meet or video-call the real owner wherever you can. If someone resists letting you verify their authority to sell, that’s your answer.

A real-world example: the deal that almost worked

Say you’re a buyer in Atlanta, and a cousin in Nairobi sends you a listing: a two-bedroom apartment in Kileleshwa, KES 9 million, “well below market because the owner is relocating fast.” The agent is friendly, sends a clean-looking title, and asks for a KES 500,000 “holding deposit” to your cousin’s M-Pesa to “lock it before a viewing this weekend.”

Three of the levers are already pulled: a below-market price, a personal-account deposit, and a rush. So you stop. You hire your own advocate in Nairobi and pay KES 500 for an Ardhisasa search. The search shows the registered owner — and the name doesn’t match the “owner” the agent named. It also shows a recent transfer and an active caveat. Your advocate calls the agent, who suddenly can’t arrange a viewing and stops replying.

You’re out KES 500 and a few days. Without the search, you’d have wired the deposit to a stranger and chased it forever. That’s the whole game: a small, boring check, done before the money moves, in place of a fast, exciting deal that quietly skips the record.

Legitimate sale vs scam: spot the difference

| What you see | A legitimate sale | A likely scam |

|---|---|---|

| The title | Verifiable on an official search, in the owner’s name | Refused, “being processed,” or a name that doesn’t match |

| The seller | ID matches the registered owner; meets you | A relative, “agent,” or fixer who won’t produce the owner |

| The price | In line with the area | Far below market, with a hurried excuse |

| The money | Into an advocate’s completion or escrow account | Cash, personal M-Pesa, or an individual’s bank account |

| The pace | Patient; waits for searches and contracts | Urgent: “pay today,” “another buyer is coming” |

| The site | Open visit; surveyor confirms beacons | Photos only, vague location, no beacon check |

| The advocate | You have your own; both sides registered | ”Let’s share one to save money,” or none at all |

If a deal sits mostly in the right-hand column, it doesn’t matter how good it feels. Walk away.

The clear do / don’t list

Do

- Run an official Ardhisasa or registry search before any money moves.

- Hire your own registered advocate, every time.

- Confirm the seller’s ID matches the title, and meet the real owner.

- Visit the site and confirm beacons with a licensed surveyor.

- Pay only into a completion or escrow account, against a signed agreement.

- Keep a paper trail of every document and payment.

- Take your time, and treat urgency as a warning.

Don’t

- Don’t pay cash, or send to a personal M-Pesa or an individual’s account.

- Don’t pay a “holding deposit” before viewing and verifying ownership.

- Don’t rely on the title in the seller’s hand instead of the official record.

- Don’t buy from a “relative of the owner” or “agent” without verified authority.

- Don’t share one advocate with the seller to save a fee.

- Don’t let anyone rush you past a check.

- Don’t buy family or agricultural land without consents and completed succession.

The paperwork to collect and verify

Ask for — and independently verify — each of these before you pay:

- An official search from Ardhisasa or the registry, in the seller’s name

- The title deed, with its authenticity checked against the registry

- The seller’s national ID or passport, matching the title

- KRA PIN certificates for both sides (needed to transfer)

- A registered survey / mutation map and beacon confirmation

- Land rates and land rent clearance certificates (no arrears)

- For apartments: the sectional title or share/lease documents and service-charge status

- For family or agricultural land: spousal and family consents and Land Control Board consent

- A written sale agreement drafted or reviewed by your advocate

- Proof that payments go to a completion / escrow account

Our step-by-step guide to buying property in Kenya and our buying-land playbook cover where each of these fits in the process.

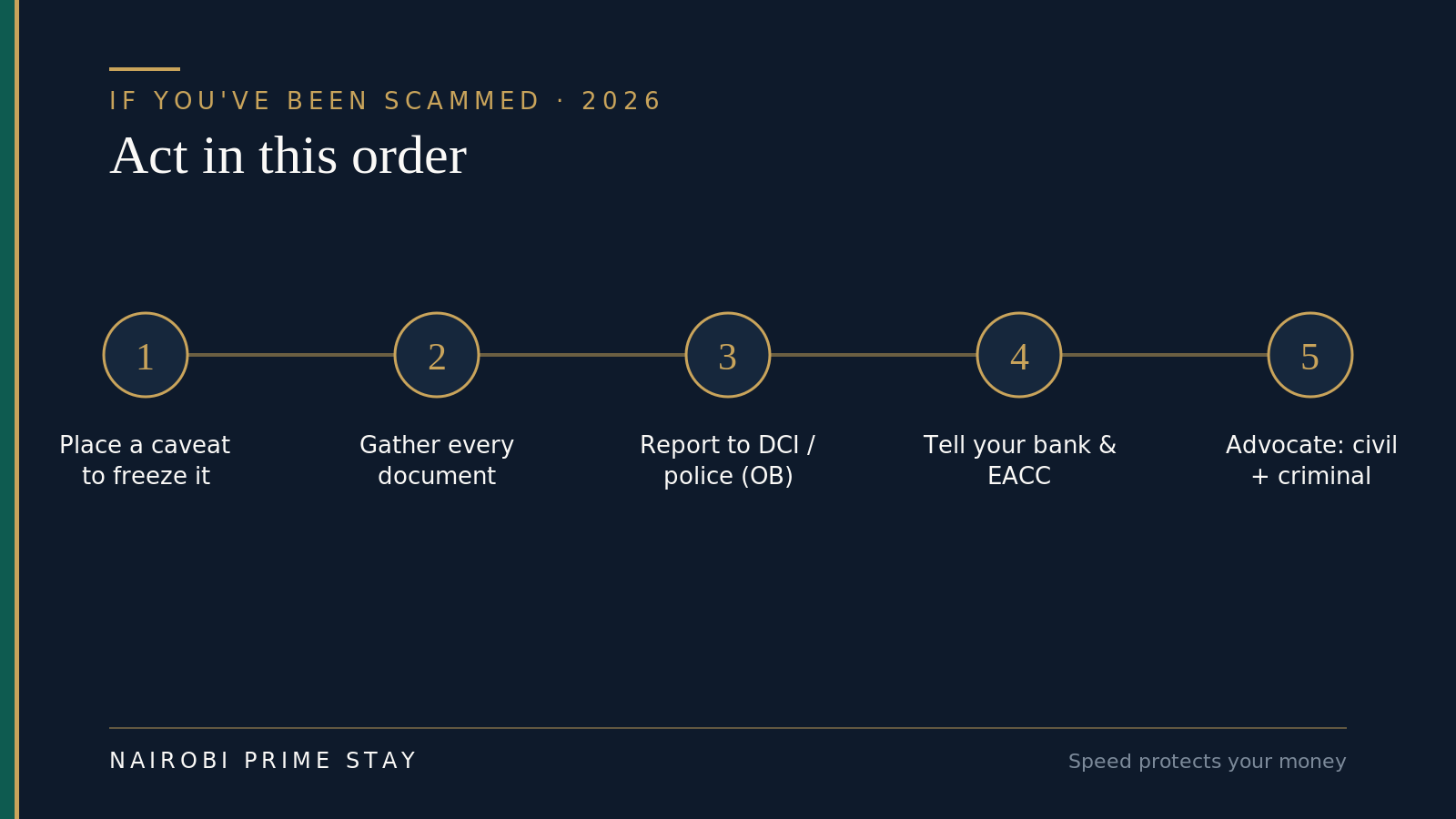

What to do if you’ve already been scammed

Act quickly — speed protects whatever money or claim you still have. The order matters.

If it has happened, move fast and in this order — a frozen title and a clear paper trail are your strongest cards.

If it has happened, move fast and in this order — a frozen title and a clear paper trail are your strongest cards.

- Freeze the land. Have your advocate lodge a caveat or restriction on the title to block any further transfer while you act. This is often the single most important early move.

- Gather your evidence. Collect every document, message, receipt and transfer record. Save phone numbers, account details and the original listing. A clean paper trail drives both the criminal case and any refund claim.

- Report it. File with the DCI Land Fraud Unit or your nearest police station and get an OB (Occurrence Book) number. Lodge a complaint at the Ministry of Lands or the relevant county registry as well.

- Escalate where it fits. Tell your bank immediately if money just moved — a fast call can sometimes stop a transfer. Where government officials or grabbed public land are involved, report to the EACC; for public-land and allocation disputes, the National Land Commission (NLC) is relevant too.

- Get legal remedies moving. Your advocate can pursue both criminal (fraud) and civil (recovery, compensation) routes. The sooner a caveat is on and a case is filed, the better your odds.

No outcome is guaranteed once money has left, which is exactly why the checks earlier in this guide matter so much. Prevention is cheap; recovery is slow and uncertain.

Before you buy: rental and booking scams that hit new arrivals

Most newcomers meet a scam long before they buy anything — while booking a place to live for their first few weeks. The setup is familiar: a beautiful apartment on Facebook, Airbnb or a classifieds site, priced a little below the market, with a “landlord” or “agent” who needs a deposit wired before you can view it. The photos are real; they’ve just been scraped from a genuine listing. You pay a holding deposit to a personal M-Pesa or bank account, and then the replies slow down and stop.

It works because you’re far away, you don’t yet know the market, and a good deal feels urgent. The tell is always the same: money before viewing, to a personal account, under time pressure.

The highlighted column is worth saving to your phone before you start apartment-hunting from overseas.

The highlighted column is worth saving to your phone before you start apartment-hunting from overseas.

The defenses are simple. Never wire a deposit for a place you — or someone you trust — haven’t actually seen. Ask for a live video walkthrough, not a set of photos. Confirm the listing exists and that the person you’re dealing with controls it, and be especially wary of any “I’m traveling abroad, just pay my agent to hold it” story. Pay on arrival, or through a platform with real buyer protection, rather than by irreversible transfer to an individual. And check the market first, so a suspiciously cheap price actually reads as suspicious. Our guide to renting an apartment in Nairobi covers viewing safely and the deposit norms, and our best-neighborhoods guide helps you sanity-check prices by area.

This is exactly where a vetted serviced apartment earns its keep. Instead of wiring a stranger from another continent, you book a verified place with a company you can call, settle in for a few weeks, and use that secure base to view long-term homes and run your searches in person. A small deposit reserves your dates and the balance is paid on arrival — no large, irreversible transfer before you’ve seen a thing.

Frequently asked questions

How common are property scams in Kenya?

Common enough to take seriously. The Ministry of Lands has estimated that more than 10% of titles in circulation may be fraudulent, and it reported over 10,000 land-fraud cases under investigation in 2024, with losses in the billions of shillings. Kenya’s anti-corruption commission also names property fraud as the single most costly scam hitting the diaspora. Most victims, though, skipped a basic check — an official search and your own advocate stop the large majority of scams.

How do I check if a title deed is genuine in Kenya?

Run an official search. On Ardhisasa (ardhisasa.lands.go.ke) or eCitizen, register with your ID and KRA PIN and pull a search for roughly KES 500–1,000; the report shows the registered owner, the parcel size, and any charges or caveats. Then have your advocate confirm the deed against the registry. Genuine titles carry seals and watermarks, but the search, not the look of the paper, is what proves ownership.

What is the most common property scam in Kenya?

Fake or duplicate title deeds and selling land the seller doesn’t own are the most common, alongside ‘deposit and disappear,’ where you’re asked to pay before viewing. They all rely on you trusting a document instead of the registry and paying an individual directly. An official search plus payment into a completion account defeats most of them.

Is it safe to buy property in Kenya as a foreigner or from the diaspora?

Yes, if you use the safeguards. Foreigners and the diaspora are targeted more because they buy at a distance and move large sums, so the checks matter more, not less. Use your own advocate, an official search, an escrow or completion account, an independent site inspection, and never an informal fixer. Non-citizens can hold property on a 99-year leasehold rather than freehold.

How much does an official land search cost in Kenya?

Roughly KES 500–1,000. An official Ardhisasa or eCitizen search is about KES 1,000 (plus a small fee), paid by M-Pesa or card; some counter searches are nearer KES 500. Ardhisasa is fully live for Nairobi and Murang’a, so for other counties use the eCitizen land search or the county registry. Results come back within about one to three business days. It is the cheapest and most powerful anti-fraud step you can take, so never skip it to save time.

Should I ever pay a deposit before viewing a property?

No. A request to pay a ‘holding deposit’ or ‘viewing fee’ before you have seen the property and verified ownership is a classic scam. View in person or send someone you trust, confirm the title, and pay only against a signed agreement into a traceable account, never cash or a personal M-Pesa.

What should I do if I’ve been scammed in a property deal in Kenya?

Move fast. Have your advocate lodge a caveat to freeze the title, gather all documents and payment records, and report to the DCI Land Fraud Unit or police for an OB number. Alert your bank if money just moved, and the EACC where officials are involved. Then pursue civil and criminal remedies through your advocate.

Can an advocate or escrow account really protect my money?

Largely, yes. A registered advocate runs the legal checks and holds your funds in a completion account, releasing them only when the title transfers into your name, so a seller can’t take the money and vanish. It is the structural protection that turns a risky handshake into a safe transaction, and the fee is small next to the cost of a loss.

How do I buy property in Kenya from the US without being scammed?

Treat distance as the risk to manage. Hire your own advocate — found independently, not recommended by the seller or agent — and have them run an official Ardhisasa or eCitizen search before any money moves. Get independent eyes on the ground: a licensed surveyor to confirm the beacons and a trusted person with no stake in the deal, plus a live video walkthrough. Wire funds only to the advocate’s client account, never to a personal M-Pesa or an individual. If you must appoint someone to sign for you, use a narrow, registered power of attorney to a regulated advocate, not an informal fixer.

Is it safe to give someone power of attorney to buy property for me in Kenya?

It can be, if you keep it tight. A power of attorney is heavily abused in Kenyan land fraud, both by sellers who forge one and by ‘trusted’ relatives or fixers who sell to themselves. Keep any PoA you grant narrow and specific — one named property, one transaction, with an expiry — give it to a regulated advocate rather than an informal contact, and register it. A PoA you sign in the US must be notarized and then legalized at a Kenyan embassy or consulate, because Kenya isn’t in the Apostille Convention. Have your advocate authenticate any PoA the other side relies on.

How do I avoid rental and apartment scams when moving to Nairobi?

Never wire a deposit for a place you or someone you trust hasn’t seen. Most newcomer scams are fake listings with scraped photos, a below-market price, and a ‘landlord’ who’s traveling and needs a holding deposit to a personal account first. Verify the listing exists and that the person controls it, ask for a live video walkthrough, and pay on arrival or through a platform with buyer protection. A vetted serviced apartment — where a small deposit reserves and the balance is paid on arrival — is a safe first base while you view long-term homes in person.

Final thoughts

Property fraud in Kenya is real, but it isn’t mysterious. It runs on three things — skipping the official record, paying an individual, and moving fast — and every check in this guide takes one of those away. Do the search. Hire your own advocate. Match the seller to the title. See the land. Pay into escrow. Refuse the rush. That’s the whole defense.

The buyers who lose money almost never lose it to a genius con. They lose it to a skipped step that would have cost a few hundred shillings and a week of patience. Treat every purchase as a transaction, not a favour or a stroke of luck, and you’ll be in the large, quiet majority who buy in Kenya and never have a story to tell. This is general guidance, not legal advice — confirm the specifics with a registered Kenyan advocate, and verify current figures and processes with the Ministry of Lands and ardhisasa.lands.go.ke.

Related reading

- Property investing in Kenya: the complete guide — the cluster pillar, start here

- Buying land in Kenya — the full due-diligence playbook

- Title deeds in Kenya explained — how to read an official search

- Conveyancing in Kenya — what your advocate actually does

- How to buy property in Kenya — the step-by-step process

- Buying off-plan property in Nairobi — vetting developers and contracts

- Diaspora property investment in Kenya — buying safely from abroad

- Can foreigners buy property in Kenya? — what you’re allowed to own

- Moving to Nairobi: the complete guide — the relocation hub

A safer way to land

If you’re buying from abroad or scouting before you commit, give yourself a secure base instead of rushing a deal from a hotel lobby. A serviced apartment lets you settle in Nairobi for a few weeks — Wi-Fi, cleaning, a backup generator and 24/7 security included — while you view properties, meet advocates, and run your searches without pressure. Browse available apartments; a $50 deposit reserves your dates and the balance is paid on arrival.

Not sure where to start, or which checks apply to your situation? Our AI relocation assistant can point you to the right guides and shortlist a place to stay while you do this properly, day or night.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.