Guides · Property investment

Buying Land in Kenya: A Safe 2026 Due-Diligence Guide

Buying Land in Kenya: A Safe 2026 Due-Diligence Guide

Buying land in Kenya can be a sound investment. It can also go very wrong. Land is the single most fraud-prone purchase in the country — the same plot gets sold twice, “owners” turn out to own nothing, and beautiful roadside plots sit on land the government can take back. The good news: almost every loss is preventable. The checks that protect you are cheap, public, and well-established.

This guide is the safe way to do it. We cover the official land search, how to confirm the seller really owns the land, why you walk the boundaries with a surveyor, the public-land traps to avoid, the consent agricultural land needs, and the scams that catch newcomers. It’s written for Americans and other foreigners, but Kenyans buying land use the same playbook.

Two honest cautions before we start. First, this is general information, not legal advice — Kenyan land law is detailed and the money at stake is real, so hire your own advocate before you sign or pay anything. Second, if you’re a foreigner, bare land is the hardest thing to own here: you can’t hold freehold or buy agricultural land, and the due diligence is heavy. For most foreign buyers a city apartment on a sectional title is far simpler and safer. We’ll show you why, and link you to can foreigners buy property in Kenya for the full rules.

The short version (TL;DR). Never buy land in Kenya on trust. Run an official land search (about KES 500–1,000 on ardhisasa or eCitizen) to confirm the owner, the size and any charges. Confirm the seller’s ID matches the title, and for estates or companies confirm who’s legally allowed to sell. Walk the plot with a licensed surveyor to verify the beacons. Check it isn’t on a road reserve, a riparian (river) strip or public land. If it’s agricultural, you’ll need Land Control Board consent — and as a foreigner you generally can’t buy farmland at all. Use your own advocate, keep the deposit in their trust account, and never send money for a plot nobody independent has verified. Budget roughly 60–90 days.

The safe sequence on one screen. Your advocate runs most of it with you; skipping a step is exactly where buyers lose money.

The safe sequence on one screen. Your advocate runs most of it with you; skipping a step is exactly where buyers lose money.

Why land is riskier than an apartment

Land carries more ways to lose money than any other property purchase in Kenya. An apartment comes with one clean question — is the sectional title genuine and unencumbered? A plot of land comes with a dozen: Does the seller actually own it? Are the boundaries where they say? Is it really private, or is part of it a road reserve? Is it agricultural, and does that block you? Has it already been sold to someone else? Each of those is a place a deal can fail.

The numbers back this up. The Ministry of Lands has estimated that a meaningful share of title deeds in circulation — by some official accounts more than one in ten — are fraudulent or irregular. That doesn’t mean most land is fake; it means you cannot assume, and a single afternoon of checks separates a safe buy from a costly one.

For a foreigner the gap is even wider. You can own an apartment on a 99-year sectional title in your own name with light due diligence. Bare land brings ownership limits (no freehold, no farmland), boundary checks, possible Land Control Board consent, and the full fraud risk on top. That’s why our honest advice to most overseas buyers is to start with an apartment and treat land as a later, eyes-open project. If you want the wider picture first, our Kenya property investment guide maps every route.

What you can actually buy as a foreigner

Start here, because it shapes everything else. Under Kenya’s Constitution, a non-citizen can only hold land on a leasehold of up to 99 years — never freehold. And under the Land Control Act, a foreigner generally cannot buy agricultural land at all. A sale or lease of agricultural land to a non-citizen is void unless the Cabinet Secretary for Lands gives express consent, which is rare. In practice, foreigners who want rural land take a long lease rather than owning it outright.

So what counts as “agricultural”? Broadly, land outside a town or municipality that’s classified for farming. Much of the cheap roadside land sold to first-time buyers in counties around Nairobi — Kiambu, Kajiado, Machakos — is agricultural on paper, even if it looks like a building plot. That classification is exactly what trips up foreign buyers. Urban and commercial plots inside gazetted municipalities are usually fine to lease; farmland usually isn’t.

There’s also the company workaround you’ll hear about — “just buy it through a Kenyan company.” It doesn’t do what people think. A company counts as a citizen only if it’s 100% owned by Kenyan citizens. The moment a foreigner holds shares, the company is a non-citizen for land purposes and inherits the same limits. Nominee arrangements (putting the land in a Kenyan friend’s name) are worse: you hold no legal title and little recourse if it goes sideways. For the full breakdown, see can foreigners buy property in Kenya, and for the different title types you might encounter, title deeds in Kenya explained.

The honest bottom line: if you’re a foreigner set on land, focus on urban leasehold plots, lean hard on your advocate, and accept that the cleanest path to property ownership here is still a sectional-title apartment.

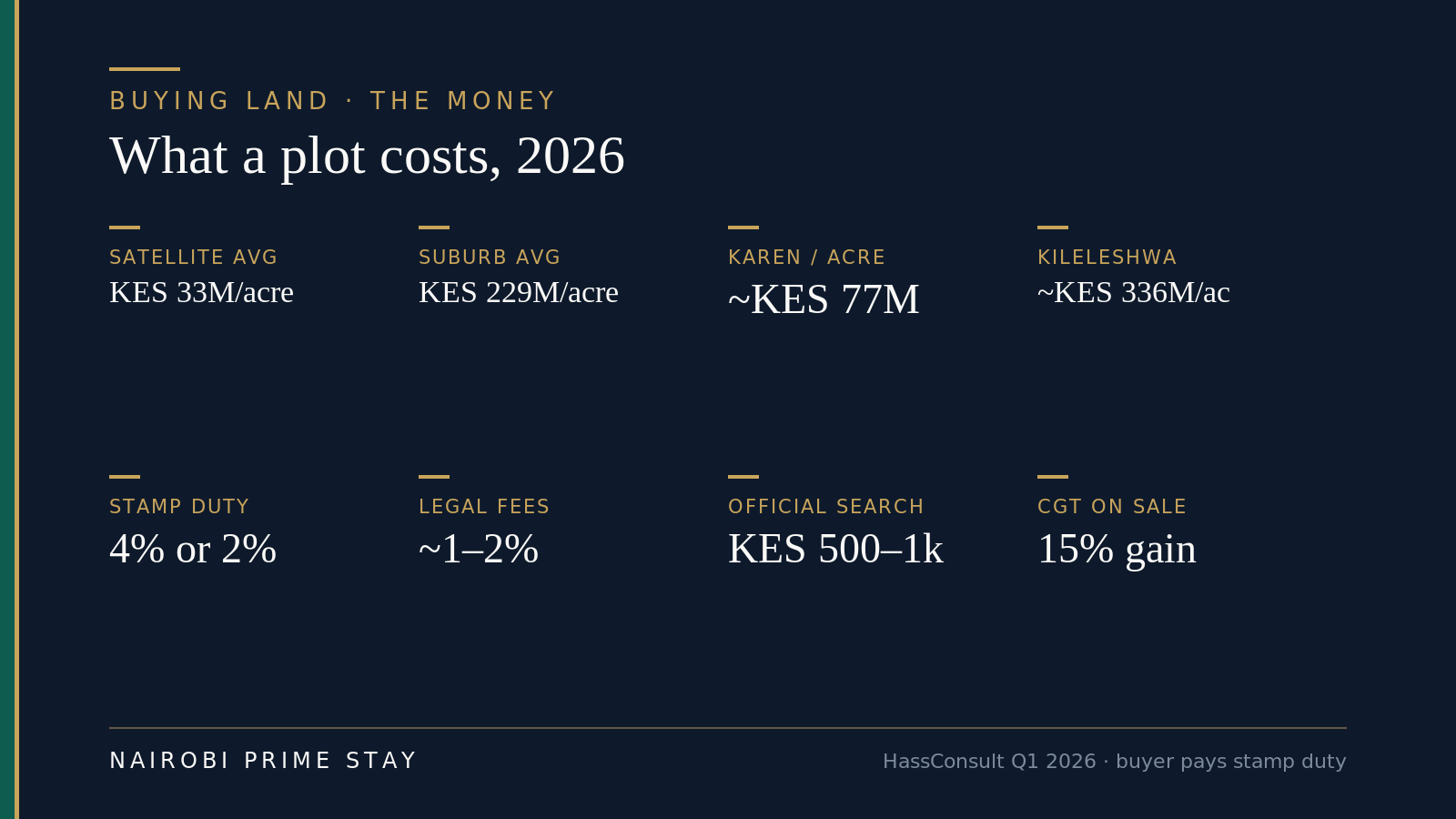

What a plot actually costs around Nairobi in 2026

Land around Nairobi isn’t cheap, and the plot price is only part of what you pay. Prices swing enormously by location, so treat any single figure as a starting point and confirm current numbers on the ground with an agent and a valuer.

The money on one screen. Prices are HassConsult Q1 2026 averages; your plot will differ.

The money on one screen. Prices are HassConsult Q1 2026 averages; your plot will differ.

Here’s the lay of the land. In early 2026, HassConsult put the average price of an acre in Nairobi’s suburbs at about KES 228.8 million, and the average satellite-town acre at roughly KES 33 million — with annual growth around 5% in the suburbs and 4.3% in the satellite towns, the slowest in five years. Within the suburbs the spread is huge: an acre in high-density Kileleshwa ran to about KES 336 million, while lower-density Karen sat near KES 77 million. Out in the satellite towns — Kitengela, Juja, Ruiru, Ongata Rongai, Thika — Q1 2026 growth was flat to modestly positive as tighter household budgets cooled the market. For the wider market read, see our Nairobi property prices guide.

Most retail plots aren’t sold by the acre, though. They’re sold as an eighth of an acre (the classic 50-by-100-foot plot) or a quarter, so divide accordingly — and remember that a cheap roadside eighth and a serviced plot in a gated scheme with a clean title, tarmac access, water and power are very different things at very different prices. Location, access, services and the quality of the title drive the number far more than the raw size does.

Then there’s the transaction cost stack on top of the price. Budget for these before you commit:

| Cost | Typical amount (2026) | Notes |

|---|---|---|

| Stamp duty | 4% of value (town/municipality) or 2% (rural) | Buyer pays, on the higher of price or government valuation |

| Legal fees | ~1–2% of the price | Your advocate’s scale fee; get the quote in writing |

| Official search | KES 500–1,000 | The cheapest, most important check — do it first |

| Licensed surveyor | A few thousand KES up | Confirms the beacons and the size on the ground |

| Valuation | Modest | Often needed for the stamp-duty assessment and any loan |

| Registration | Modest statutory fees | Lodges the transfer and issues the new title |

Stamp duty is the big one. As of 2026 it’s 4% of the value for land inside a town or municipality — which now takes in Nairobi and most gazetted towns in Kiambu, after a 2024 directive folded areas like Ruiru, Kikuyu and Thika into the urban rate — and 2% for genuinely rural land. The buyer pays it, and it’s charged on the higher of your price or the government’s own valuation, so a low number on paper won’t shrink the bill. Confirm the current rate and your plot’s classification with your advocate; our property taxes in Kenya guide has the wider picture.

The official land search: your first and most important check

The official land search is the single most important thing you do, and you do it before you pay a shilling. It’s a government record check that tells you who legally owns the parcel, its exact size, and whether anything is registered against it — a mortgage (charge), a court order, or a caveat (a flag someone has lodged claiming an interest). If the search doesn’t match what the seller is telling you, that’s the end of the conversation.

An official search is a search of the land registry. For Nairobi and other digitized registries it’s done online through ardhisasa, the government’s digital land platform at ardhisasa.lands.go.ke. For registries that aren’t yet on ardhisasa, the search is done through eCitizen or the local lands office. Either way the cost is small — roughly KES 500–1,000 (a few US dollars) — and results usually come back in about 1–3 working days.

Cheap, fast and decisive. Confirm the live details at ardhisasa.lands.go.ke.

Cheap, fast and decisive. Confirm the live details at ardhisasa.lands.go.ke.

A few things to know. To search on ardhisasa you register with your ID and KRA PIN, then apply against the title number. On the digital system the registered owner is notified and, in many cases, has to approve the search before the certificate is released — a privacy feature that can add a day or two, and a useful honesty test of whoever you’re dealing with. Read the certificate with your advocate: confirm the registered proprietor’s name, the parcel size, the tenure (freehold or leasehold and how many years remain), and that the encumbrances section is clean — or that you understand anything listed there. Run the search once early, then run it again right before completion, because someone can register a charge or caveat in the gap.

One rule that saves people: the search is done in the registry, not on a piece of paper the seller hands you. A genuine-looking title deed proves nothing on its own — forgeries are common and convincing. Trust the registry record your advocate pulls, not the document in the seller’s hand.

Full due diligence: the documents to check

Beyond the search, a safe land purchase rests on a short stack of documents. Your advocate gathers and reads these; your job is to know what they are and refuse to move until each one checks out. Here’s the core set and what each proves.

| Document | What it is | Why it matters |

|---|---|---|

| Official search certificate | Registry record of owner, size and encumbrances | Confirms the seller owns it and it’s unencumbered |

| Original title deed / certificate of lease | The seller’s proof of ownership | Compared against the search; copies alone prove nothing |

| Land rates clearance certificate | County receipt that rates are paid up | Unpaid rates can block the transfer |

| Land rent clearance certificate | Proof ground rent is paid (leasehold land) | Required for leasehold transfers |

| Mutation form / deed plan / RIM | Survey records showing the parcel’s shape and size | Confirms what’s on the ground matches the title |

| Seller’s ID and KRA PIN | Identity of the registered owner | Must match the name on the title exactly |

| Land Control Board consent | LCB approval for agricultural land | Without it, an agricultural transfer is void |

| Sale agreement | The written contract, drawn by advocates | Sets price, deposit, completion terms and protections |

Don’t skip the boring ones. The rates and rent clearances feel like paperwork, but an unpaid balance can stall your transfer for months — and quietly become your problem. For the registration mechanics that turn these documents into a title in your name, see conveyancing in Kenya.

Confirm the seller is really the seller

Match the name. The person selling must be the exact registered owner named on the title and the search — same spelling, same ID number. It sounds obvious, but impersonation is one of the most common land frauds: a stranger poses as the owner (sometimes with a stolen or forged ID) and sells land they don’t own. Your advocate verifies identity carefully, and a face-to-face meeting with the registered owner is worth insisting on.

Estates and joint owners need extra care. If the registered owner has died, the seller must have a confirmed grant of probate or letters of administration — without it, no one can legally pass title, and “the family agreed” is not enough. If the land is jointly owned, every owner must consent and sign. For married sellers, spousal consent protects against a later challenge under matrimonial property law. These are exactly the situations where a deal looks fine and unravels a year later.

Buying from a company? Pull a CR12 (the official record of a company’s directors and shareholders) to confirm who controls it and who’s authorized to sell, alongside the company’s certificate of incorporation and KRA PIN. Your advocate will know what to ask for — the point is that “the director said so” isn’t proof.

Walk the land with a licensed surveyor

Never buy land you haven’t stood on, and never stand on it without a surveyor. A licensed surveyor — registered with the Institution of Surveyors of Kenya (ISK) — pulls the parcel’s survey map (the mutation map or registry index map) from Survey of Kenya, then visits the site with GPS to find and confirm the beacons. Beacons are the physical markers, usually concrete or metal, that fix each corner of the boundary. They are the difference between the land you think you’re buying and the land you actually get.

This step catches a surprising number of problems. The plot on the ground is smaller than the title says. The boundaries overlap a neighbor’s. The beacons are missing, moved, or never existed. The “plot” being walked is a different parcel entirely from the one on the title — a classic bait-and-switch. A surveyor confirms the size, shape and exact position, and re-establishes beacons if needed, giving you a report you can trust.

While you’re there, look around with clear eyes. Is there a road cutting through or beside it? A river or stream nearby? Power lines overhead? Existing structures or people farming it? Each of those is a question to answer before you pay, not after.

Public-land traps: road reserves, riparian and “greenlands”

Some plots can’t legally be owned or built on, no matter how good the paperwork looks — because they sit on public land. These are the traps that catch buyers who fall for a great location and a low price.

A road reserve is the strip of land set aside along a road for future widening, drainage and services. It belongs to the public. Plots carved into a road reserve get demolished when the authority comes through, and no compensation follows. Riparian land is the protected buffer along rivers, streams and lakes — commonly measured from the highest watermark — meant to stay undeveloped. Build on it and you risk demolition; Nairobi has seen exactly that. “Greenlands” and other reserves set aside for parks, utilities or public use are the same story: not for sale, whatever a broker claims.

How do you avoid them? The same checks already in this guide do most of the work. The survey map and a surveyor’s site visit show where the parcel sits relative to roads and water. The official search shows the tenure and whether it’s genuinely private. And an advocate who knows the area will recognize a road-reserve or riparian plot on sight. If a deal depends on you not asking where the road or the river is, that’s your answer.

Land Control Board consent (for agricultural land)

If the land is agricultural, the sale needs Land Control Board (LCB) consent to be valid — and this is where many foreign purchases simply stop. The LCB is a local board that must approve transactions in agricultural land. You apply for consent (your advocate handles the form), the board sits and considers it, and it issues a consent letter that’s typically valid for six months. The approval usually takes a few weeks, so build it into your timeline.

Two hard rules matter here. First, timing: you must get LCB consent before completing the transfer. A transfer of agricultural land done without consent is void — not “delayed,” void — and that has cost buyers their money. Second, and decisive for overseas buyers: an LCB cannot approve a sale of agricultural land to a non-citizen, or to a company that isn’t wholly owned by citizens. So if the plot is agricultural and you’re a foreigner, the board can’t say yes. That’s the legal wall behind our advice to focus on urban leasehold or, better, an apartment.

Common land scams and the red flags

Most land fraud in Kenya falls into a handful of patterns. Learn them and you’ll spot trouble early. The recurring scams are the fake title deed (a convincing forgery for land the seller doesn’t own), the double sale (the same plot sold to several buyers, sometimes with a corrupt insider), the impersonation (a fraudster posing as the real owner), the ghost plot (a parcel that doesn’t exist, sold with staged photos or a visit to unrelated land), and the public-land sale (road reserve, riparian or forest land that can never be privately owned).

If the right-hand column isn’t all true, you’re not ready to pay.

If the right-hand column isn’t all true, you’re not ready to pay.

The red flags are consistent across all of them. A price far below the market, paired with pressure to “decide today” and pay cash, is the oldest one. So is a seller who resists an official search, offers only photocopies, or doesn’t want your advocate involved. A name on the title that doesn’t match the person selling. A plot you’re shown quickly but never allowed to survey. Money requested to a personal account before anything is verified. None of these is automatically fraud — but each is a reason to slow down, not speed up. Real sellers expect you to check; only fraudsters are in a hurry. For the deeper field guide, see property scams in Kenya.

A real scenario

Say you’ve found a one-acre plot in Kitengela, an hour from Nairobi, advertised well below the going rate because the “owner is relocating urgently.” You like it. Here’s the safe version of what happens next.

Your advocate runs an official search on the title number. It comes back showing a different registered owner than the person you’ve been emailing — and a caveat lodged by a bank. That’s two deal-killers in one certificate, found for under KES 1,000 before any money moved. You walk away, a few thousand shillings lighter and a fortune safer. Now run the same plot the unsafe way: you wire a deposit to a personal account to “secure it,” and discover later that the seller never owned it and three other buyers paid too. The only difference between those two stories is a search, a surveyor and an advocate — a few weeks and a modest fee. That’s the whole lesson of buying land in Kenya.

Land vs an apartment: the safer foreign buy

For most foreign buyers, an apartment on a sectional title is the cleaner choice — and it’s worth being honest about why. Land asks more of you on every axis that matters: ownership rights, fraud risk, the depth of due diligence, and the consents involved.

Both can be good buys. For an overseas buyer, an apartment removes most of the risk.

Both can be good buys. For an overseas buyer, an apartment removes most of the risk.

| Factor | Bare land | Apartment (sectional title) |

|---|---|---|

| Open to foreigners | Limited — urban leasehold only, no farmland | Yes — 99-year leasehold in your own name |

| Fraud risk | High — the most fraud-prone purchase | Low — one clean title to verify |

| Due-diligence load | Heavy — search, seller, survey, consents | Lighter — search and the sectional title |

| Boundary / beacon checks | Required on site | Not applicable |

| Land Control Board consent | May be required (agricultural land) | Not required |

| Registered in your name | Leasehold, urban plots only | Yes, directly |

If land is still the goal, that’s fine — just go in with the right team and timeline. If a simpler, lower-risk entry into Kenyan property appeals, the how to buy property in Kenya guide walks the apartment route end to end.

The taxes on land: buying, holding and selling

Land carries a tax at each stage — when you buy, while you hold it, and when you sell. None of it is complicated, but the last one is easy to forget, and for an American owner there’s a sting in the tail if you ever build and rent.

Three stages, three taxes. The one people forget is the 15% on the way out.

Three stages, three taxes. The one people forget is the 15% on the way out.

When you buy, you pay stamp duty — 4% of the value in a town or municipality, 2% for rural land, on the higher of price or valuation, as covered above. While you hold the land, you owe annual county land rates, and on leasehold plots a separate land rent to the national government. Vacant land earns you nothing, but those charges keep running — and unpaid rates or rent will block your next transfer, so keep them current.

When you sell, capital gains tax (CGT) is 15% of the net gain — your sale price minus what you paid and your allowable costs (stamp duty, legal fees and any improvements). It was raised from 5% to 15% back in 2023, it’s a final tax, and the seller pays it. The exemption for a private home you’ve owned and lived in for three continuous years doesn’t apply to bare investment land, so plan for the full 15% on any appreciation. Kenya has no annual tax on a property’s value the way US states do; the recurring bill is county rates, and the big one-off is CGT on the way out.

One more thing for US owners. If you build on the land and rent it out, you become a non-resident landlord, and Kenya taxes that rent at a flat 30% of the gross — withheld and remitted by your tenant or agent, with no deductions. There’s no US–Kenya tax treaty, so you can’t offset it against Kenyan tax; you claim a US foreign tax credit instead. That’s a separate calculation from holding raw land, but worth knowing before you picture rental income. Our taxes for expats in Kenya guide covers the cross-border side — and none of this is tax advice, so get your own before you act.

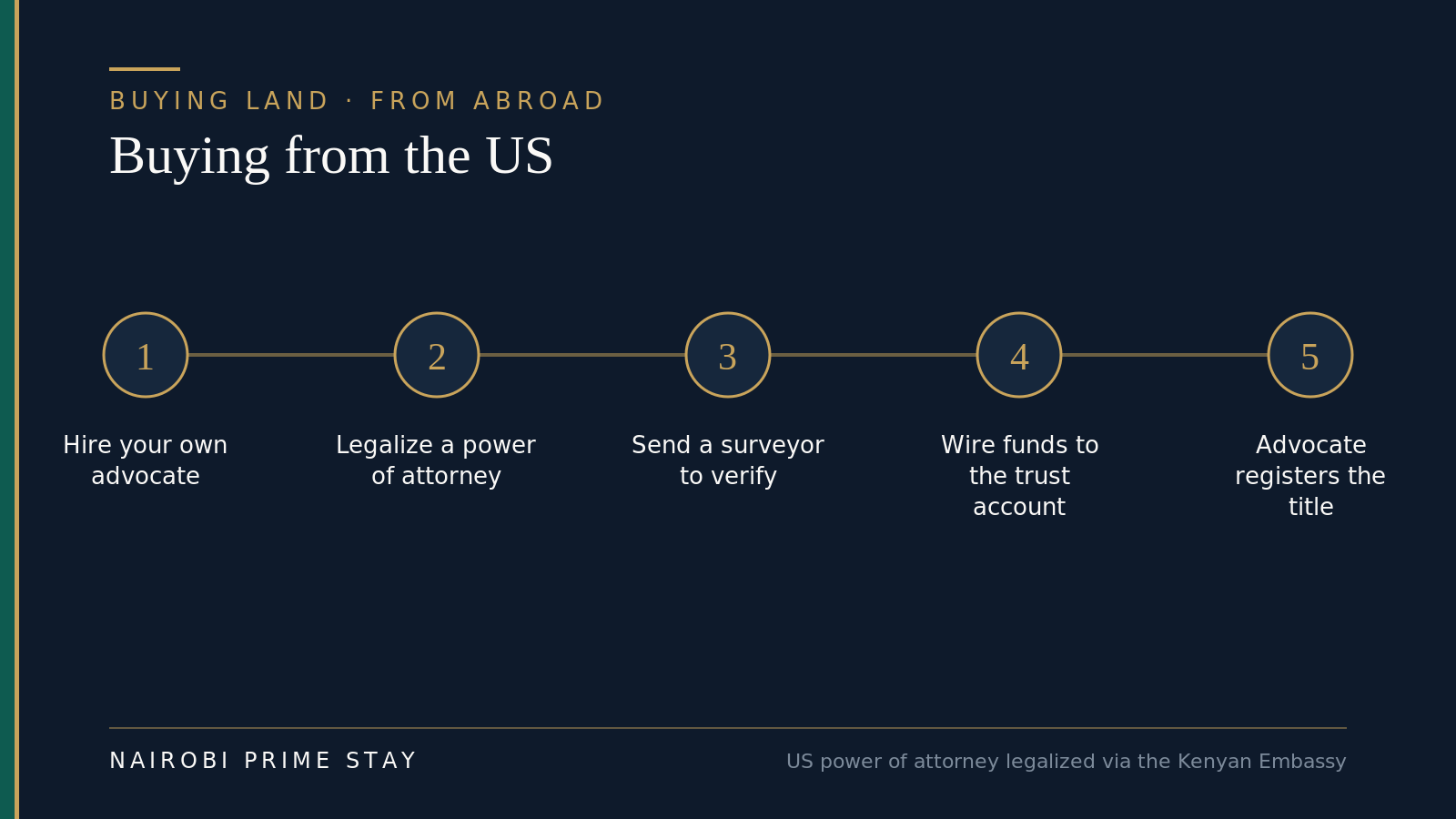

Buying and paying from the US

You can buy Kenyan land from the US, but land is the single worst thing to buy sight-unseen — so do it with a team on the ground and, ideally, at least one trip. Here’s how the money and the mechanics actually work.

The remote-purchase sequence. Never skip the surveyor, and never wire to a personal account.

The remote-purchase sequence. Never skip the surveyor, and never wire to a personal account.

Moving the money. Kenya has no exchange controls, so you can send dollars in and, later, repatriate your sale proceeds freely. Move funds by bank transfer or a service like Wise into your advocate’s trust account or your own Kenyan account — never carry or wire cash to a personal account to “secure” a plot. If you do bring cash into Kenya, amounts over USD 10,000 must be declared. Watch the exchange rate too: the shilling traded around KES 129–130 to the dollar in mid-2026 (about 129.4 on 1 July), and over a long purchase that drift shifts your real cost, so price the plot in both currencies. See our sending money to Kenya and USD/KES currency guides for the detail.

Buying without being there. If you can’t fly out to sign, you appoint your advocate under a power of attorney to act for you. A power of attorney signed in the US has to be notarized and then legalized through the Kenyan Embassy before it’s valid in Kenya — Kenya isn’t part of the Apostille Convention, so an apostille alone won’t do — and your advocate will confirm the exact wording and process. Even buying remotely, don’t cut the checks that protect you: run the official search, send an independent licensed surveyor to walk the plot and confirm the beacons, and keep the deposit in the advocate’s trust account until everything verifies. This is exactly the ground our diaspora property investment in Kenya guide covers in depth.

The honest version: many diaspora buyers who’ve lost money were buying land they never stood on, from a “seller” they never met, wiring to an account nobody vetted. The fix isn’t complicated — an advocate, a surveyor, a search, and money that only ever moves through a trust account. A scouting trip, with a serviced apartment as your base, is the cheapest insurance of all.

Your land due-diligence checklist

Run this in order. Don’t pay until every box is genuinely ticked.

- Get an official search on the title number (ardhisasa or eCitizen) and confirm the owner, size, tenure and a clean encumbrances section.

- Match the seller’s ID and KRA PIN to the exact name on the title; meet the registered owner in person.

- For an estate, confirm a grant of probate / letters of administration; for joint owners, get every owner’s consent; for a company, pull a CR12.

- Hire a licensed (ISK) surveyor to confirm the beacons and that the plot on the ground matches the title.

- Check it isn’t on a road reserve, riparian strip or public land.

- Confirm the land use — if it’s agricultural, remember foreigners generally can’t buy, and consent is required either way.

- Obtain land rates and land rent clearance certificates.

- If agricultural, secure Land Control Board consent before completion.

- Sign a written sale agreement drawn by advocates; pay the deposit into your advocate’s trust account, never a personal one.

- Re-run the search just before completion, then lodge the transfer and get the new title in your name.

Final thoughts

Buying land in Kenya rewards patience and punishes shortcuts. The protections are public, cheap and reliable — an official search, a surveyor, the right clearances, and your own advocate. Use them every time and the horror stories simply don’t happen to you. The buyers who lose money are almost always the ones who moved fast, paid first, and checked later.

If you’re moving to Nairobi and weighing whether to buy at all, give yourself room to learn the ground before you commit. Rent first, see the areas, talk to people who’ve done it. A plot will still be there in six months; your savings should be too. When you’re ready, do it slowly and do it right.

This is general information for 2026, not legal advice. Land law and fees change — confirm current details on ardhisasa.lands.go.ke and through your own advocate before acting.

Related reading

- Property investing in Kenya — the pillar guide to every route, returns and rules.

- Can foreigners buy property in Kenya? — the ownership rules in plain English.

- How to buy property in Kenya — the step-by-step buying process.

- Building a house in Kenya vs buying — what it costs, the approvals, and the diaspora pitfalls

- Title deeds in Kenya explained — freehold, leasehold and sectional title.

- Conveyancing in Kenya — how the legal transfer and registration work.

- Property scams in Kenya — the frauds to know and how to avoid them.

- Moving to Nairobi: the complete guide — the relocation hub for everything else.

Before you buy land, get your bearings

The smartest land buyers start by living here a while first. A serviced apartment for your first month or two gives you a secure, all-inclusive base — Wi-Fi, cleaning, generator and security included — while you scout areas, meet advocates and learn the market before committing a cent to a plot. Browse our serviced apartments in Nairobi, or let our AI relocation assistant shortlist options to match your plans in a couple of minutes. A $50 deposit reserves your place and the balance is paid on arrival — nothing more before you travel.

Frequently asked questions

Can foreigners buy land in Kenya?

Only on a limited basis. A non-citizen can hold land only on a leasehold of up to 99 years, never freehold, and generally cannot buy agricultural land at all — a sale of farmland to a foreigner is void unless the Cabinet Secretary for Lands gives rare express consent. In practice foreigners focus on urban leasehold plots or, more cleanly, buy a sectional-title apartment in their own name. Buying through a Kenyan company doesn’t help unless the company is 100% citizen-owned.

How do I do an official land search in Kenya?

Run an official search of the land registry against the parcel’s title number. For Nairobi and other digitized registries this is done online through ardhisasa (ardhisasa.lands.go.ke), where you register with your ID and KRA PIN; for registries not yet on ardhisasa, use eCitizen or the local lands office. The search certificate shows the registered owner, the size, the tenure, and any charges or caveats. Results usually come back in about 1–3 working days, and on ardhisasa the owner may need to approve the request first.

How much does a land search cost in Kenya?

An official land search costs roughly KES 500–1,000 — a few US dollars — as of 2026. It’s the cheapest and most important check you’ll make, so confirm the current fee on ardhisasa or eCitizen and run the search before you pay any deposit, then again right before completion.

How do I avoid land-buying scams in Kenya?

Verify everything independently and never pay on trust. Run an official search to confirm the seller really owns the land, match the seller’s ID exactly to the name on the title, hire a licensed surveyor to confirm the beacons on the ground, and check the plot isn’t on a road reserve, riparian strip or public land. Use your own advocate, pay the deposit into their trust account rather than a personal one, and treat any below-market ‘urgent’ cash sale as a red flag, not a bargain.

What is Land Control Board consent and when do I need it?

Land Control Board (LCB) consent is approval from a local board that’s required for any transaction in agricultural land. You apply (your advocate handles it), the board considers it, and it issues a consent letter typically valid for six months. You must get consent before completing the transfer — an agricultural transfer done without it is void. Importantly, an LCB cannot approve a sale of agricultural land to a non-citizen, which is why foreigners generally cannot buy farmland.

Do I need a lawyer to buy land in Kenya?

Yes — hire your own advocate, and do it before you sign or pay anything. An advocate runs the official search, verifies the seller and documents, drafts and reviews the sale agreement, holds your deposit in their trust account, and handles the transfer and registration so the title ends up in your name. The cost is modest against the money at stake, and skipping this step is how most buyers get defrauded.

What are road reserves and riparian land?

They are public land you can’t legally own or build on. A road reserve is the strip set aside along a road for future widening and services; riparian land is the protected buffer along rivers, streams and lakes, measured from the highest watermark. Plots sold on either can be demolished without compensation, so a survey site visit and an advocate who knows the area are essential to spot them.

Is it safer to buy an apartment than land in Kenya?

For most foreign buyers, yes. An apartment on a sectional title is registered in your own name on a 99-year lease, carries far lighter due diligence, and avoids farmland limits, boundary checks and Land Control Board consent. Bare land is the most fraud-prone purchase in Kenya and brings the heaviest checks, so many overseas buyers start with an apartment and treat land as a later, eyes-open project.

How much does it cost to buy land in Kenya?

Beyond the plot price, budget for the transaction costs. Stamp duty is the biggest — 4% of the value for land in a town or municipality (including Nairobi and most gazetted Kiambu towns) and 2% for rural land, paid by the buyer on the higher of the price or the government valuation. Add legal fees of roughly 1–2%, a licensed surveyor, a valuation, the official search (KES 500–1,000) and registration fees. As a rough anchor, HassConsult put the average Nairobi suburban acre near KES 229 million and the satellite-town acre near KES 33 million in early 2026, but retail plots are sold as eighths of an acre and prices swing widely with location, access and services — confirm current numbers locally.

Do foreigners pay tax when they sell land in Kenya?

Yes. When you sell, capital gains tax is 15% of the net gain — the sale price minus what you paid and allowable costs like stamp duty, legal fees and improvements. It’s a final tax paid by the seller, and the three-year private-residence exemption doesn’t cover pure investment land, so plan for the full 15% on any appreciation. While you hold the land you owe annual county land rates and, on leasehold, land rent. And if you build and rent it out as a US-based non-resident, that rent is taxed at 30% of the gross, with a US foreign tax credit rather than a treaty offset.

Can I buy land in Kenya from the US without visiting?

Technically yes, but land is the worst thing to buy sight-unseen. You can appoint your advocate under a power of attorney to sign and register for you — a US power of attorney must be notarized and then legalized through the Kenyan Embassy, since Kenya isn’t in the Apostille Convention, so confirm the exact process with your advocate. Even then, send an independent licensed surveyor to walk the plot and verify the beacons, run the official search, and wire the deposit into the advocate’s trust account, never a personal one. Many diaspora buyers pair a scouting trip with a serviced apartment before committing a cent.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.