Guides · Money

USD to KES in 2026: A Practical Currency Guide for Americans Moving to Nairobi

USD to KES in 2026: A Practical Currency Guide for Americans Moving to Nairobi

One US dollar buys about 129.5 Kenyan shillings as of late June 2026. That number is the quiet backbone of your whole budget here — rent, groceries, school fees, the taxi home. Get a feel for it and Nairobi stops feeling like a foreign-currency puzzle.

The good news for anyone moving on a US income: the shilling has been remarkably steady for about two years, and your dollars go a long way. The honest part: rates move, old habits from home don’t all transfer, and a few small mistakes (changing money at the airport, carrying worn bills) quietly cost you. This guide fixes that.

It’s written for Americans who’ve never handled shillings before. By the end you’ll know today’s rate and where to check it, where to change money for the best deal, whether to hold dollars or shillings, and how to budget so a wobble in the rate never catches you out.

TL;DR: In June 2026, USD/KES ≈ 129–130 (about 129.5 on 30 June; check the Central Bank of Kenya or Wise for the live number). The shilling is market-set and has been stable near 129–130 since it recovered sharply in 2024, so budgeting is easier than it’s been in years. Change money at a city forex bureau (best cash rates) or a bank ATM, not the airport. Bring newer $50 and $100 bills printed after 2006. Hold some dollars for big-ticket and savings; convert to shillings as you go for daily life, which you’ll pay for with M-Pesa. Plan your budget at roughly 130 with a 5–10% buffer and you’re covered.

The numbers that matter, at a glance. The rate is market-set — confirm the live figure before you change a large sum.

The numbers that matter, at a glance. The rate is market-set — confirm the live figure before you change a large sum.

What’s the dollar-to-shilling rate right now?

About 129.5 shillings to the dollar (30 June 2026). Through June the rate sat in a tight band — roughly 129.25 to 129.65, averaging about 129.4. So when you see a price of KES 13,000, that’s almost exactly $100. A quick mental shortcut: divide shillings by 130 to get dollars, and you’ll be within a rounding error.

A few things to know about that number. The Central Bank of Kenya (CBK) publishes a daily indicative rate, but it doesn’t set the rate — the shilling is market-determined, moving with supply and demand for foreign currency. The rate you actually get when you change cash or spend on a card will be a little worse than the headline “mid-market” figure, because that gap is how banks and bureaus make their money. More on that below.

For the live number, two sources are enough: the Central Bank of Kenya rates page for the official daily figure, and Wise for the real mid-market rate you can benchmark everyone else against. Bookmark one. Glance at it the morning you plan to change a meaningful amount.

A quick conversion cheat sheet

Until the divide-by-130 shortcut becomes second nature, keep a few common amounts in your head. At about 129.5 to the dollar, a KES 13,000 dinner bill is almost exactly $100, and a KES 234,000 month — a fair all-in budget for a remote worker — runs around $1,800.

Common shilling amounts in dollars, at June 2026’s ~129.5. Divide any shilling price by 130 for a close-enough dollar figure.

Common shilling amounts in dollars, at June 2026’s ~129.5. Divide any shilling price by 130 for a close-enough dollar figure.

Why the exchange rate matters when you’re moving

Because almost everything you’ll pay for is priced in shillings, while your money probably arrives as dollars. The rate is the bridge, and it shapes three things.

First, your purchasing power. At ~130, a comfortable professional life in Nairobi costs a fraction of a big US city — see our honest cost-of-living breakdown for the real monthly numbers, or the head-to-head in Nairobi vs the US. When the shilling is weaker (a higher number, say 150), your dollars stretch even further. When it strengthens (a lower number), Nairobi gets a little pricier in dollar terms.

Second, your timing on big transfers. The exact day you move a deposit or a school-fee payment can swing the shilling total by a percent or two. That’s not worth losing sleep over for everyday sums, but on a $30,000 transfer it’s real money. Our guide to sending money to Kenya covers how to move large amounts without losing a slice to hidden margins.

Third, your peace of mind. People who understand the rate stop second-guessing every price. They set a planning rate, keep a buffer, and get on with life. That’s the goal here.

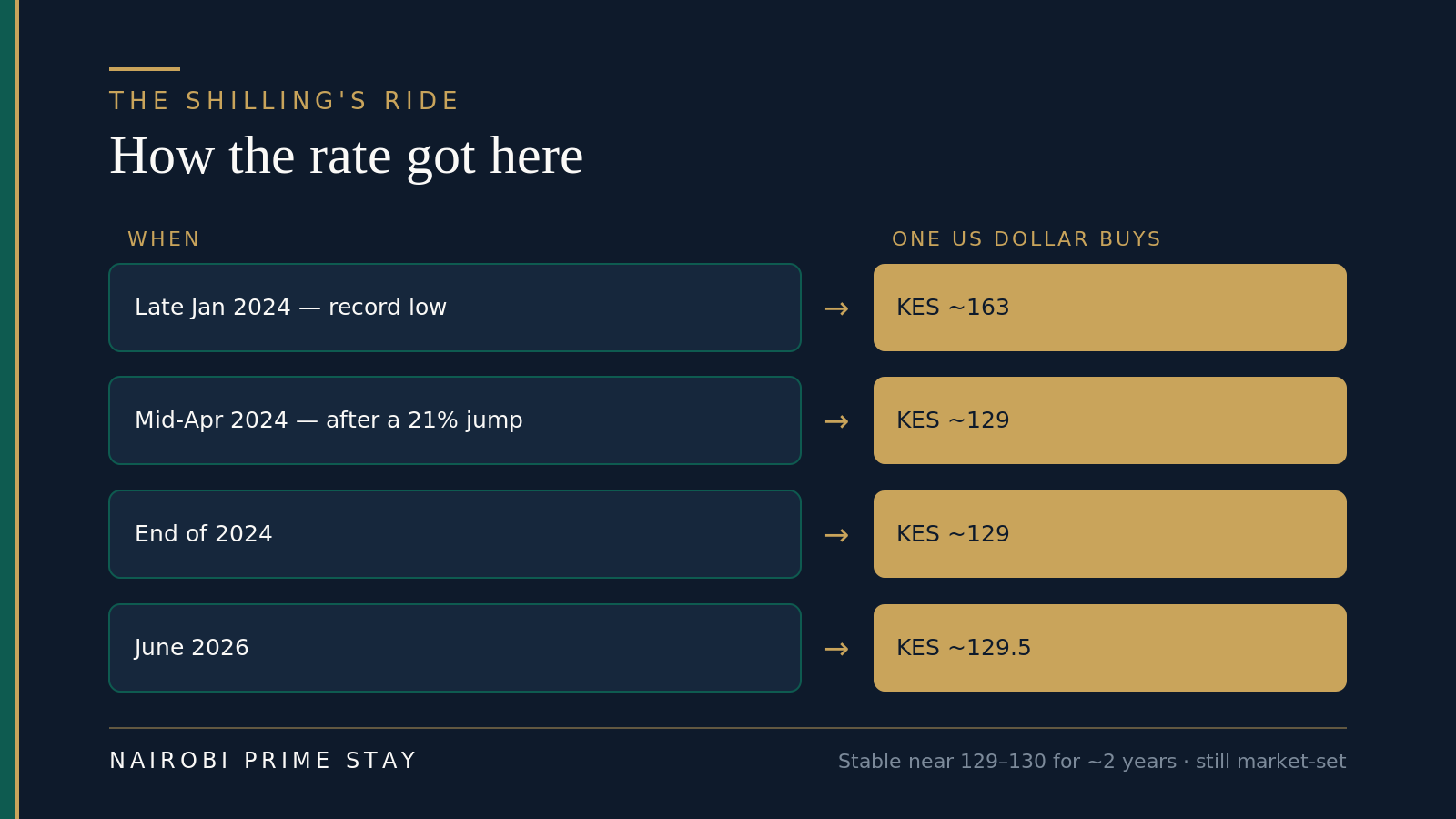

The honest volatility note: how the shilling got to 129

Here’s the real picture, good and bad, because the recent history tells you how much to trust the calm.

The shilling had a rough few years to 2023. It slid steadily and then fell off a cliff, hitting a record low of about 163 to the dollar in late January 2024. Anyone who moved over in that stretch watched their dollar budget get better month after month — small comfort against the wider economic stress that caused it.

Then it snapped back hard. In early 2024 the Central Bank raised its benchmark interest rate to a 12-year high, and the government refinanced a looming Eurobond debt with a heavily oversubscribed new issue. Confidence returned fast. The shilling strengthened about 21% in a single quarter, to roughly 129 by mid-April 2024 — its best run since the early 1990s. It closed 2024 near 129, versus about 157 a year earlier.

Since then it has been unusually stable, hovering around 129–130 for roughly two years and into mid-2026. For someone budgeting a move, that stability is a gift — it’s far easier to plan against a steady rate than a sliding one.

From a record low to two years of calm. The rate is still market-set, so treat today’s stability as the current weather, not a permanent climate.

From a record low to two years of calm. The rate is still market-set, so treat today’s stability as the current weather, not a permanent climate.

What does that mean for you? Don’t assume the calm is permanent — it’s market-set, and forecasters expect it to drift gently rather than stay frozen. Most 2026 outlooks put the average for the year near 130, in a 129–131 range, with a slow tilt toward a weaker shilling into 2027 (some models pencil in roughly 132 by then). So plan at 130, keep a buffer, and you’re covered whether it firms up or eases off. Don’t try to time the market; you won’t beat it, and you don’t need to.

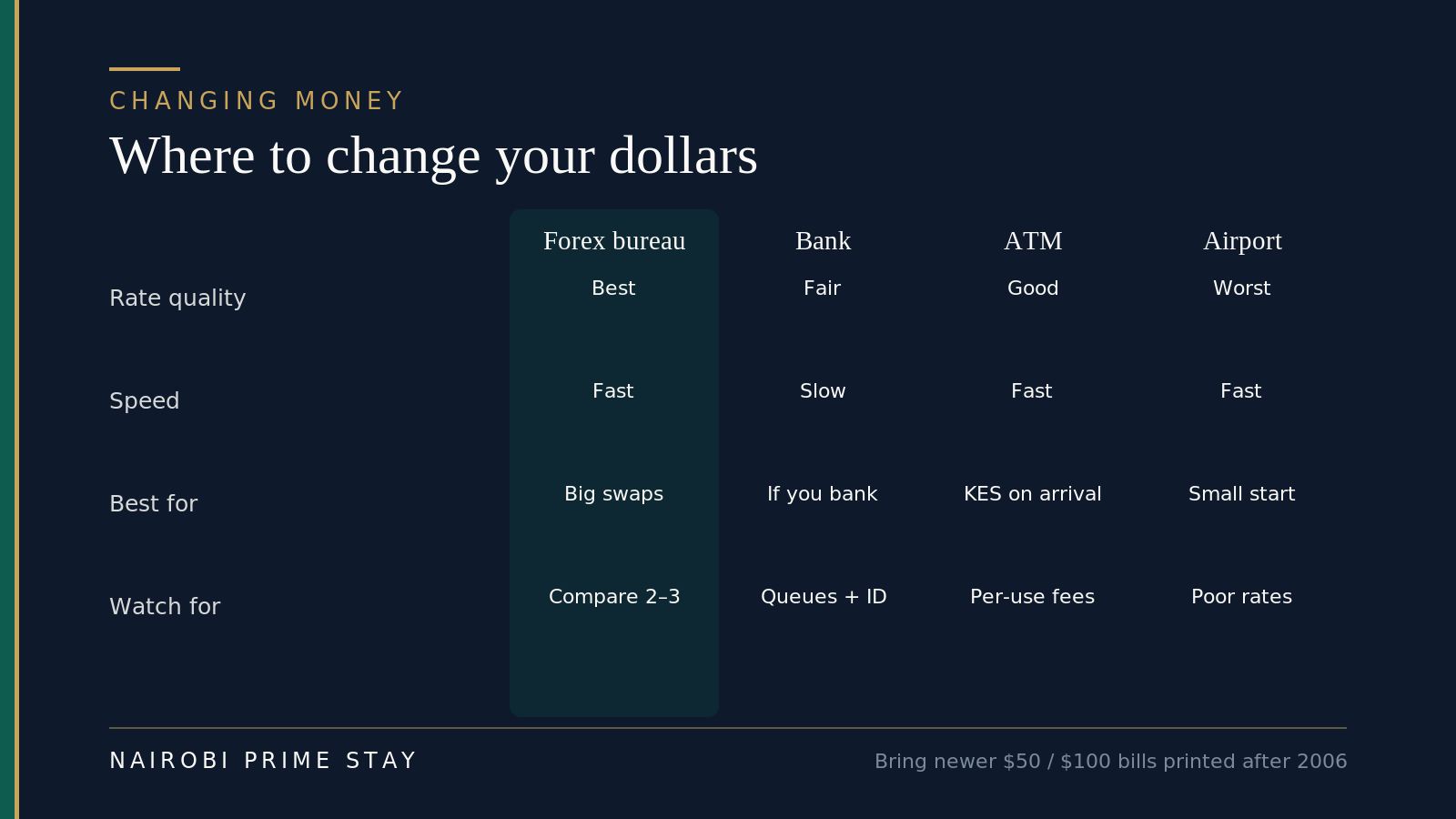

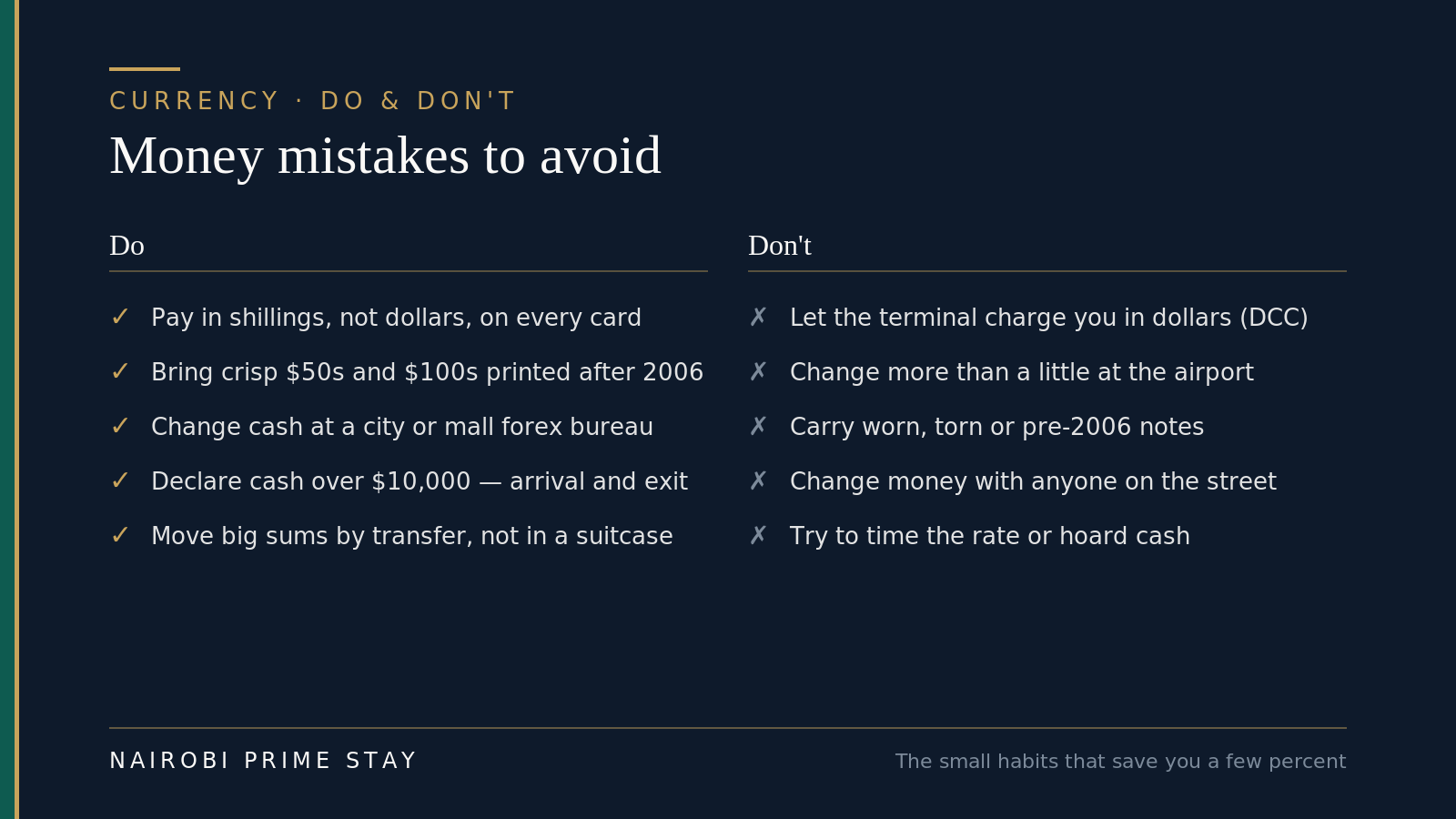

Where to change money safely (and where not to)

Short version: change cash at a licensed forex bureau in town, or pull shillings from a bank ATM. Skip the airport counters for anything more than a small starter amount, and never change money with someone on the street.

Here’s how the options actually compare.

Forex bureaus win on cash rates; ATMs win on convenience. The airport is for emergencies only.

Forex bureaus win on cash rates; ATMs win on convenience. The airport is for emergencies only.

Forex bureaus (best rates for cash). Licensed bureaus in the city and in malls give the best rates on dollar cash, usually beating banks. There are plenty, so compare two or three before you commit a large sum — rates vary street to street. Bureaus are regulated by the Central Bank; stick to established, signposted ones in malls or busy commercial areas rather than a hole in the wall. Mid-morning or mid-afternoon means shorter queues.

Bank ATMs (best for convenience). Withdrawing shillings directly from an ATM with your US debit or credit card gives you a rate close to the network mid-market — often very competitive. The catch is fees: your US bank may charge a foreign-transaction fee, and the Kenyan ATM may add its own withdrawal charge. Use a card that refunds or waives these and the ATM route is excellent. Withdraw inside a mall or bank branch, not a quiet standalone machine.

Banks (fine if you’re a customer). Over-the-counter exchange at a bank is secure and fully documented, which matters for large or official sums. Rates are fair but usually a touch worse than a good bureau, and it’s slower — expect to show ID and, for big amounts, answer source-of-funds questions. Most useful once you’ve opened a Kenyan account.

Airport counters (small starter amount only). The bureaus at JKIA are licensed and safe, but airport rates are poor — by some measures well over 10% worse than the going rate. Change just enough to get into town and through your first day (a taxi, a SIM, a meal) — our JKIA airport guide covers arrivals and getting around Nairobi covers the ride in. Then do the rest at a city bureau or ATM. Better still, your phone solves most of day one — see M-Pesa below.

The street (never). If someone offers to change money on the street or “at a better rate” outside an official bureau, walk away. It’s the classic short-change and counterfeit trap. There’s no upside.

Bring the right bills

A specific, money-saving detail Americans rarely hear: the physical condition and series of your dollar notes matters. Bureaus and banks pay the best rates for newer, large-denomination bills — $50s and $100s, crisp, and printed after 2006. Older series, worn notes, or small denominations ($1–$20) get a noticeably worse rate or get refused outright. So before you fly, ask your US bank for newer big bills in good condition. It’s a free few percent.

Bringing your money in: cash, transfers, and the $10,000 rule

Most of your money should travel as a transfer, not as cash in your bag. Carrying a little dollar cash for the first few days is smart; flying in with your savings in an envelope is not — it’s a theft risk, and it runs into a rule worth knowing.

The $10,000 declaration rule. If you arrive carrying more than USD 10,000 — or the equivalent in any currency, counting cash and monetary instruments like traveler’s checks — you must declare it to customs, both on the way in and on the way out. This isn’t a tax and you’re not charged for declaring; it’s an anti-money-laundering formality. But failing to declare can mean the cash is seized and you’re fined, so if you’re over the line, fill in the form. Under $10,000, no declaration is needed. The rule is set by the Central Bank of Kenya and enforced by customs at JKIA — confirm the current threshold before you fly.

Move the bulk by transfer. For anything beyond starter cash, send it electronically once your Kenyan bank account is open — it’s cheaper, safer, and leaves a clean paper trail for tax and source-of-funds checks. The main routes, compared:

Four ways to get dollars to Kenya. For most movers a transfer app wins; very big sums may justify a wire. Our sending money to Kenya guide compares providers in detail.

Four ways to get dollars to Kenya. For most movers a transfer app wins; very big sums may justify a wire. Our sending money to Kenya guide compares providers in detail.

A bank SWIFT wire works for very large amounts and is fully documented, but it usually carries a flat fee plus a hidden FX margin — compare it against a specialist transfer before sending. If you’re funding a property or a deposit from abroad, our diaspora property investment guide covers moving larger sums in safely. Whatever the route, big transfers can trigger routine source-of-funds questions on both ends; that’s normal, not a red flag.

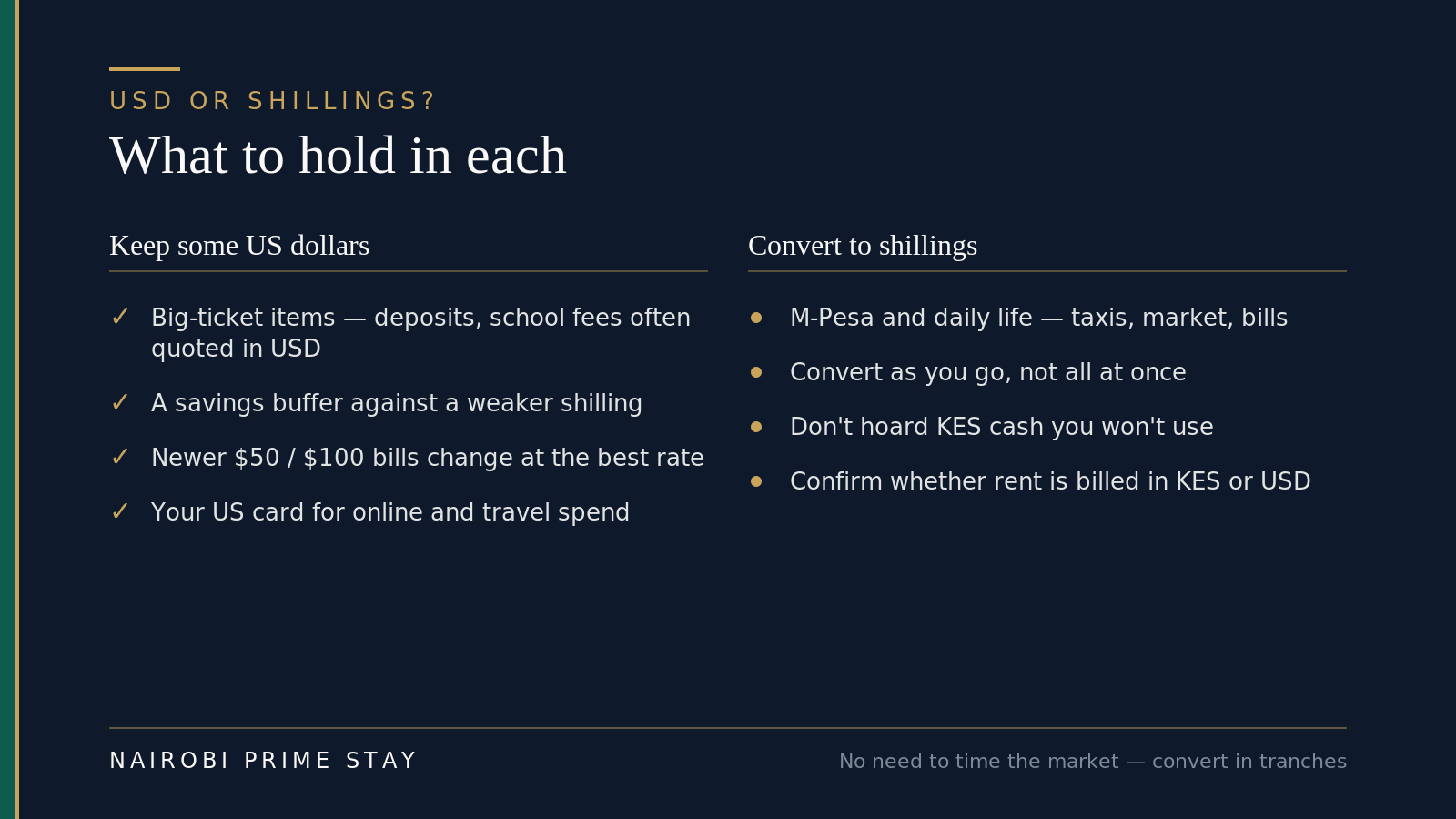

Should you hold dollars or shillings?

Both — for different jobs. Keep a dollar reserve for big-ticket and savings; convert to shillings for the daily spend you’ll actually make. You don’t need to pick a side or guess the rate.

Hold dollars for the big and the long-term; hold shillings for the everyday. Convert in tranches, not in one nervous lump.

Hold dollars for the big and the long-term; hold shillings for the everyday. Convert in tranches, not in one nervous lump.

Keep some US dollars for:

- Big-ticket items. Rent deposits in prime areas, international school fees, and serviced-apartment bookings are often quoted in USD. Holding dollars means no double conversion.

- Savings and your emergency buffer. If you’re keeping a cushion, dollars protect you if the shilling weakens.

- Online and travel spending. Your US card works for international subscriptions, flights, and trips out of the country.

Convert to shillings for:

- Everyday life. Taxis, the market, your phone bill, a coffee — all shillings, almost all paid via M-Pesa.

- Rent, if it’s billed in KES. Many leases are. Confirm the currency in writing before you sign, and check who absorbs the FX risk if it’s a USD lease paid in shillings.

The simple rule: convert in tranches, as you need shillings — not all at once. Spreading your conversions over weeks averages out the rate and means you’re never sitting on a big pile of cash. Trying to “buy at the bottom” is a game even professionals lose.

How you’ll actually pay for things: M-Pesa and cards

Day to day, you won’t be handling much cash at all. M-Pesa — Safaricom’s mobile-money wallet — is how Nairobi pays for everything, from a matatu ride to rent to the vegetable seller. You load shillings onto your phone number and send or pay with a few taps. Set up a SIM and M-Pesa at the airport on arrival with your passport; it takes minutes. Our M-Pesa starter guide walks through it.

So the realistic flow is: dollars → shillings → M-Pesa → daily life. You change a chunk of dollars to shillings, push them to M-Pesa, and spend from your phone. Cards work too — Visa and Mastercard are widely accepted in malls, hotels, and supermarkets — and keeping a US card for international spend is smart. But for local life, the phone wins. Once you’ve opened a Kenyan bank account, your bank and M-Pesa link together and moving money between them is instant.

The card trap: always choose to pay in shillings

One habit saves you a quiet few percent on every swipe. When a card machine or ATM asks whether to charge you in US dollars or Kenyan shillings, always choose shillings. Picking dollars triggers “dynamic currency conversion” — the merchant’s machine does the math at a marked-up rate, typically 3–7% worse than your card network’s. It’s dressed up as a convenience (“pay in your home currency!”), but it’s really a tax on not knowing. Choose KES and let Visa or Mastercard convert at the near-mid-market rate. Same at the ATM: if it offers to “lock in” a dollar amount, decline and take the shilling figure.

Ways to get shillings, compared

| Channel | Rate quality | Speed | Fees to watch | Best for |

|---|---|---|---|---|

| City forex bureau | Best for cash | Fast | None typical; compare 2–3 | Changing larger cash sums |

| Bank ATM | Very good | Fast | US foreign-transaction + ATM fee | Topping up shillings on the go |

| Bank counter | Fair | Slow | ID, source-of-funds on big sums | Large or documented exchanges |

| Airport bureau | Poor | Fast | Wide spread | A small starter amount only |

| Wise / transfer to account | Near mid-market | 0–2 days | Small, transparent | Moving money in from the US |

| M-Pesa (after conversion) | n/a (you spend KES) | Instant | Small send/withdraw tariff | Daily payments |

Indicative, as of 2026. For moving money from the US into Kenya specifically, compare providers in our sending money to Kenya guide.

How to budget around the exchange rate

You don’t need a finance degree — just a planning rate and a buffer.

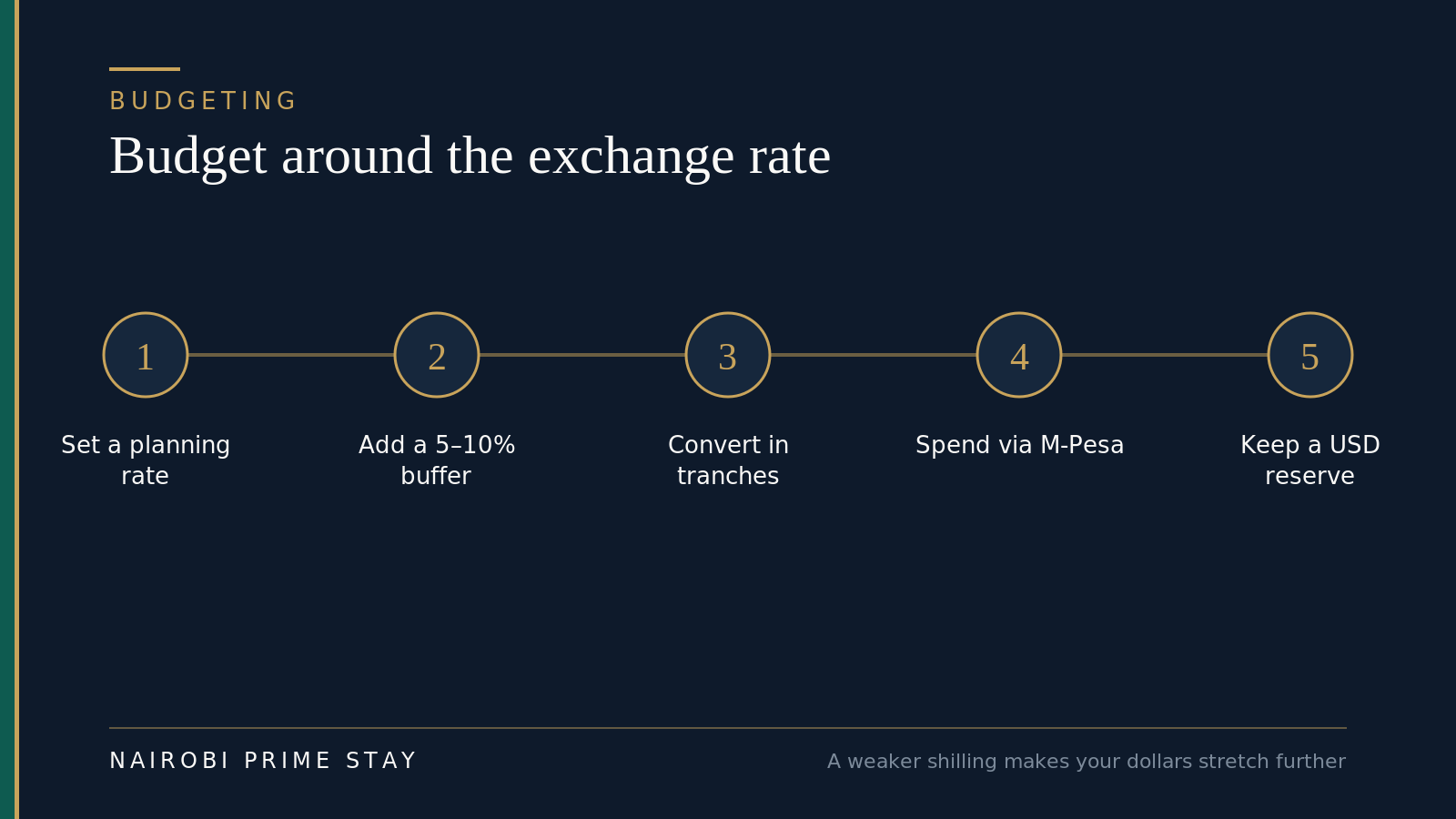

Five habits that make currency a non-issue. The buffer is the part people skip — and regret.

Five habits that make currency a non-issue. The buffer is the part people skip — and regret.

- Set a planning rate. Use a round, slightly conservative number — 130 works in 2026. Build your whole monthly budget at that rate. If the real rate is 129.5, you’ve quietly given yourself a small margin.

- Add a 5–10% buffer. Currencies move. A buffer means a rate wobble trims your cushion, not your rent. It also covers the spread you lose when changing money.

- Convert in tranches. Change money as you need shillings, across the month, rather than dumping a year’s budget at one rate. You’ll average out the ups and downs.

- Spend via M-Pesa. Keep day-to-day money on your phone and your records clean — handy at tax time, too.

- Keep a USD reserve. Hold a dollar emergency fund. If the shilling slips, your reserve buys more shillings, not fewer.

A weaker shilling is not a disaster for you — it’s the opposite. Because you earn or hold dollars, a higher USD/KES number means your money buys more here. The people who feel currency pain are those earning shillings and buying imports, not movers spending dollars.

A realistic example

Say you’re a remote worker on a US salary, renting a furnished one-bedroom in Kilimani for the equivalent of $900 a month, with another $900 for everything else — groceries, transport, dining, data. That’s about $1,800/month, or roughly KES 234,000 at a planning rate of 130.

You don’t change $1,800 in one go. On arrival you pull KES 20,000 from an ATM and set up M-Pesa for the first few days. Over the month you change dollars at a city bureau in two or three rounds, pushing shillings to M-Pesa as you spend. Rent you pay in shillings via M-Pesa or a bank transfer once your account is open. You keep a $5,000 dollar reserve untouched.

If the rate drifts from 130 to 135, your dollar budget actually gets a little easier — the same $1,800 now covers KES 243,000. If it firms to 127, you dip a little into your buffer. Either way, nothing breaks. That’s the whole point of planning at a conservative rate with a cushion.

Getting your money back out

Good news if you’re an investor or a retiree: Kenya has no exchange controls. You can convert shillings back to dollars and send them abroad through a bank or a transfer service whenever you like — there’s no government cap on taking your own money out. What you pay is the spread on the conversion and any transfer fee, plus the same FX risk in reverse: if the shilling has weakened since you brought money in, your shillings buy fewer dollars going home.

That matters most for two groups. If you’re investing in property here, think about currency on the way out, not just the way in — rental income and a future sale are in shillings, while your yardstick is dollars. And if you’re retiring in Kenya on a US pension, you’ll mostly be converting dollars to shillings each month, which a weaker shilling makes easier. Either way, keep big conversions sensible: split them, watch the rate, and use a low-margin provider.

Your currency checklist

Before you fly and in your first week:

- Check today’s rate on the CBK or Wise — know your number.

- Ask your US bank for newer $50/$100 bills, crisp and printed after 2006.

- Bring a no-foreign-fee debit/credit card for ATM withdrawals and card spend.

- Tell your bank you’re travelling so cards don’t get frozen on first use.

- Change only a small amount at the airport — enough for a taxi, SIM, and first meal.

- Set up a SIM + M-Pesa on arrival at JKIA with your passport.

- Find a couple of reputable city/mall forex bureaus and compare rates before a big swap.

- Set a planning rate (130) and a 5–10% buffer for your monthly budget.

- Confirm your rent’s currency (KES or USD) in writing before signing.

- Declare cash over $10,000 at customs — on arrival and departure — if you carry that much.

- On cards, always choose to pay in shillings, never dollars (skip DCC).

- Keep a USD reserve as your emergency cushion.

The handful of habits that keep your money yours. The dollar-on-a-card mistake is the one most people make first.

The handful of habits that keep your money yours. The dollar-on-a-card mistake is the one most people make first.

The honest balance

| In your favor | Worth watching |

|---|---|

| The shilling has been stable near 129–130 for ~2 years — easy to budget against. | It’s market-set; today’s calm isn’t guaranteed, and forecasts lean to slow weakening. |

| Earning or holding dollars means a weaker shilling helps you. | If you ever earn in shillings, the opposite is true. |

| M-Pesa and cards make daily payments frictionless once you’re set up. | Day one needs a little cash; airport rates are poor, so change just a little there. |

| Forex bureaus and ATMs give competitive rates if you choose well. | Worn or pre-2006 bills, and airport/street changers, quietly cost you. |

| You can move money in cheaply with the right provider. | Bank SWIFT wires for big sums carry fees and a hidden FX margin — compare first. |

None of the “watch” items is a dealbreaker. They’re just the small things that separate a smooth money setup from an avoidable few percent lost.

Final thoughts

Currency is one of those things that feels intimidating before you move and turns out to be simple once you’re here. The rate sits near 130, your dollars go far, and M-Pesa carries the daily load. Learn the divide-by-130 shortcut, change money at a real bureau or an ATM, keep some dollars in reserve, and budget with a buffer. Do that and you’ll never think about the exchange rate again — except to notice, pleasantly, how far your money goes.

Everything here reflects mid-2026 and the rate moves daily, so confirm the live figure with the Central Bank of Kenya or Wise before you change a large amount. This is general guidance, not financial advice.

Related reading

- Moving to Nairobi: the complete guide — the full relocation roadmap, start to finish.

- Cost of living in Nairobi — what a comfortable month actually costs, in real numbers.

- Sending money to Kenya — the cheapest, safest ways to move dollars across.

- Banking in Nairobi — how expats bank here, and which bank suits you.

- M-Pesa: a starter guide — set up the wallet that runs daily life.

- Opening a Kenyan bank account as a foreigner — what you need and the two routes in.

- Taxes for American expats in Kenya — the cross-border picture, in plain English.

- Serviced apartments in Nairobi — the all-inclusive soft-landing option, and why bookings are often priced in USD.

- Cost of living: Nairobi vs the US — how far your dollars really go, line by line.

- Diaspora property investment in Kenya — moving larger sums in to buy from abroad.

- Retiring in Kenya — living here on a US pension, currency side included.

Get a soft landing while you sort out the money

You don’t want to be hunting for a forex bureau and a long-term lease in the same jet-lagged week. A serviced apartment for your first month gives you a secure, all-inclusive base — Wi-Fi, cleaning, generator, security — while you open a bank account, set up M-Pesa, and learn the rate before signing anything. Browse our serviced apartments, or let our AI relocation assistant shortlist a few that fit your budget and commute in a couple of minutes.

Frequently asked questions

What is the dollar-to-shilling rate today?

As of 30 June 2026, one US dollar buys about 129.5 Kenyan shillings, and through June it held in a tight 129.25–129.65 band. A quick shortcut: divide a shilling price by 130 to get the dollar figure. The rate is market-set and moves daily, so confirm the live number on the Central Bank of Kenya rates page or Wise before changing a large sum.

Is the Kenyan shilling stable, or could it crash?

It’s been unusually stable, holding near 129–130 for about two years through mid-2026. That follows a sharp recovery in 2024, when it strengthened around 21% from a record low near 163 to about 129. The shilling is market-determined, so today’s calm isn’t guaranteed — most 2026 forecasts see a 129–131 range with a slow tilt toward a weaker shilling. Budget at 130 with a buffer and you’re covered either way.

Where can I change dollars to shillings in Nairobi?

Licensed forex bureaus in the city and malls give the best rates on dollar cash — compare two or three before a big swap. Bank ATMs are very convenient and offer competitive rates if your card doesn’t pile on fees. Bank counters are fine for large, documented amounts. Skip the airport for anything beyond a small starter amount, because its rates are poor, and never change money on the street.

Should I bring US dollars in cash?

Bring some — newer $50 and $100 bills, crisp and printed after 2006. Bureaus and banks pay the best rates for large, recent, good-condition notes, while worn or pre-2006 bills and small denominations get a worse rate or are refused. Change a little at the airport for day one, then do larger amounts at a city bureau or via an ATM.

Should I hold dollars or shillings?

Both, for different jobs. Keep dollars for big-ticket items often quoted in USD (rent deposits, school fees, apartment bookings), for savings, and for online and travel spend. Convert to shillings for daily life, which you’ll mostly pay for via M-Pesa. Convert in tranches as you need shillings rather than all at once — it averages out the rate and you don’t sit on a big cash pile.

Can I spend US dollars directly in Kenya?

Some hotels, tour operators and high-end services will quote or accept USD, but for everyday spending you’ll use shillings, and paying dollars informally usually means a poor built-in rate. The practical path is to convert to shillings and load them onto M-Pesa, your phone-based wallet, which is how Nairobi pays for nearly everything.

Are US credit and debit cards accepted in Nairobi?

Yes — Visa and Mastercard are widely accepted in malls, hotels, supermarkets and restaurants, and ATMs let you withdraw shillings on a US card. Keep a US card for international spending, but use a low- or no-foreign-fee card to avoid surcharges. For local, day-to-day payments, M-Pesa is faster and more universal than cards.

How should I budget if the shilling weakens?

A weaker shilling actually helps you if you earn or hold dollars, because each dollar then buys more shillings. Build your budget at a conservative planning rate (130 works in 2026), add a 5–10% buffer, convert in tranches, and keep a USD reserve. The people hurt by a weak shilling are those earning shillings and buying imports — not movers spending dollars.

How much US dollar cash can I bring into Kenya?

As much as you like, but if it’s more than USD 10,000 — or the equivalent in any currency, counting cash and monetary instruments like traveler’s checks — you must declare it to customs both entering and leaving Kenya. Declaring is free and isn’t a tax; not declaring can mean seizure and a fine. Most movers bring a few hundred to a couple thousand dollars for the first days and send the rest by bank transfer or Wise, which is safer and cheaper than carrying cash.

When a card machine asks, should I pay in dollars or shillings?

Always choose shillings. Paying in dollars triggers “dynamic currency conversion,” where the terminal converts at a marked-up rate typically 3–7% worse than your card network’s. Picking Kenyan shillings lets Visa or Mastercard convert at the near-mid-market rate instead. The same applies at ATMs that offer to “lock in” a dollar amount — decline and take the shilling figure.

Can I take my money back out of Kenya?

Yes. Kenya has no exchange controls, so you can convert shillings back to dollars and transfer them abroad through a bank or a money-transfer service without a government cap. You’ll pay the conversion spread and any fee, and you carry the exchange-rate risk in reverse — a weaker shilling means your shillings buy fewer dollars on the way home. For property income or a future sale, factor that currency round-trip into your numbers.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.