Guides · Money

Opening a Bank Account in Kenya as a Foreigner: The 2026 Step-by-Step

Opening a Bank Account in Kenya as a Foreigner: The 2026 Step-by-Step

Yes, a foreigner can open a Kenyan bank account. The real question is which of two routes fits you. If you’re already in Kenya on a residence permit, you open a normal resident account at a branch. If you’re still abroad — diaspora, or planning your move — you open a non-resident account remotely with a Kenyan bank’s diaspora desk. Both work. The documents and the timeline differ.

The thing that trips people up isn’t the banking. It’s the order. As a foreigner you can’t just walk in on a tourist stamp and open an account. Kenyan banks have to verify who you are and your legal standing in the country, and that means a permit (or a local signatory) plus a Kenyan tax PIN before they’ll open the door. Get the sequence right and the account itself takes one branch visit.

This guide is the step-by-step — built for Americans. We’ll cover who can open what, the exact documents for each route, how to get a KRA PIN as a foreigner, the FATCA paperwork US citizens have to sign, which banks are easiest for foreigners, and how long each step really takes. For the wider picture — choosing a bank, fees, dollar accounts, linking to M-Pesa — see our banking in Nairobi guide; this piece is just about getting the account open.

Every figure here is a 2026 range with the official source to confirm against, because deposits, fees and rules move.

The quick version (TL;DR)

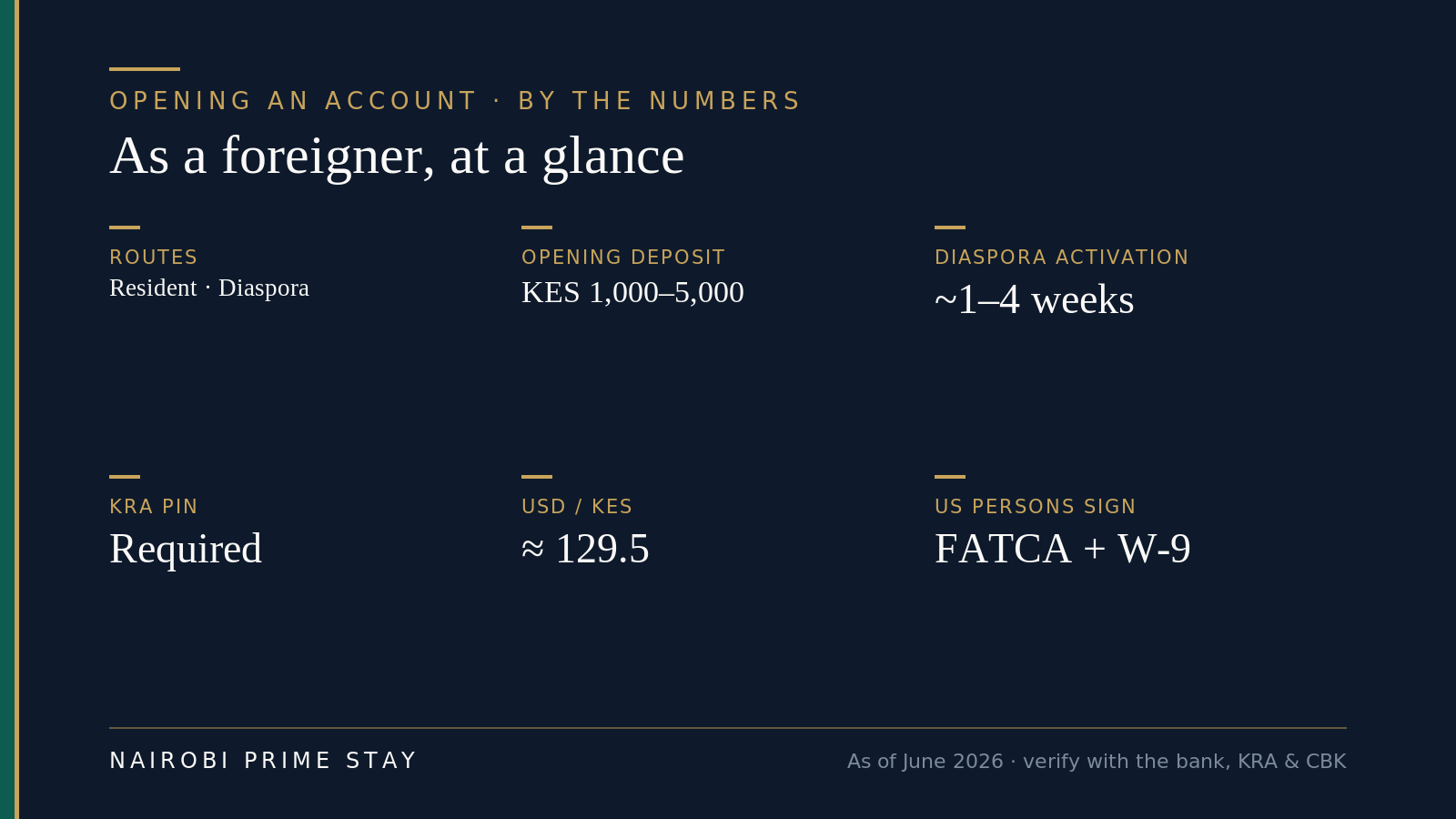

A foreigner opens a Kenyan bank account one of two ways. Resident route: once you hold a residence permit (or at least a special pass) and a KRA PIN, you walk into a branch with your passport, permit, PIN, proof of address, photos and a small deposit (about KES 1,000–5,000), and open a normal account — often the same day, sometimes after a few days of compliance checks. Non-resident / diaspora route: if you’re still abroad, banks like KCB, Equity, NCBA and I&M let you open a diaspora account remotely with your passport, a KRA PIN, proof of your overseas address, source-of-funds proof, and — because you’re a US person — FATCA and W-9 forms; activation takes about one to four weeks. Tourists on an eTA generally can’t open a full account. The golden sequence on the ground is permit → KRA PIN → bank account → lease. Get the PIN early; almost everything needs it.

Indicative 2026 figures for orientation — confirm current rules with the bank, KRA and the Central Bank of Kenya.

Indicative 2026 figures for orientation — confirm current rules with the bank, KRA and the Central Bank of Kenya.

Why the order matters when you’re new

The paperwork runs in a chain, and skipping a link stalls you. You can’t get a KRA PIN without legal standing, you can’t open most accounts without the PIN, and you can’t sign a year-long lease without an account and PIN. New arrivals discover this the hard way: they land, find an apartment they love, and then realize they can’t pay the deposit cleanly or sign the lease because the account underneath it all isn’t open yet.

The fix is to know the sequence and start early. M-Pesa, Kenya’s mobile money, is fast to set up with just your passport and covers your spending for the weeks it takes the bank account to come together. Meanwhile you work the chain in order. If you’re organized, you can even get the KRA PIN and a non-resident account started before you fly, so the bank piece is half-done by the time you arrive.

The two routes: resident vs non-resident

Which route you take depends on one thing: where you are when you apply.

A resident account is the normal one. You open it inside Kenya, at a branch, once you have legal standing — a work permit, dependant’s pass, investor permit or at least a special pass — plus a KRA PIN. This is what you’ll end up with for everyday life: salary in, rent out, debit card, M-Pesa linked. Most Americans who’ve actually moved use this route.

A non-resident or diaspora account is for people still living abroad. Kenyan banks run dedicated “diaspora” desks precisely because so many Kenyans and foreign investors abroad want an account back home. You apply remotely — online, by email, or through a correspondent bank — using your overseas address rather than a Kenyan one. It’s the route to use if you want money set up before you land, if you’re investing in Kenyan property from the US, or if you simply aren’t a resident yet.

Here’s the honest distinction: a non-resident account is genuinely useful for receiving funds, holding shillings or dollars, and getting started early — but it isn’t a substitute for the on-the-ground resident account you’ll want once you’re living in Nairobi. Many people open a diaspora account first, then convert it or open a resident account after they arrive and their permit is sorted.

Match your situation to the route — 2026 orientation; banks set their own diaspora rules, so confirm with the bank.

Match your situation to the route — 2026 orientation; banks set their own diaspora rules, so confirm with the bank.

| Resident account | Non-resident / diaspora account | |

|---|---|---|

| Who it’s for | Foreigners living in Kenya | Foreigners/diaspora still abroad |

| Where you apply | At a branch, in person | Remotely (online / email / correspondent bank) |

| Legal standing needed | Residence permit / pass | None — but a KRA PIN is still required |

| Address proof | Kenyan address | Your overseas address |

| US-specific forms | FATCA self-cert | FATCA + W-9 |

| Typical timeline | Same day to a few days | About 1–4 weeks |

| Best for | Daily life, salary, lease | Receiving funds early, property, pre-move setup |

Can a tourist open an account on an eTA?

Generally, no. An eTA (Kenya’s electronic travel authorization) marks you as a visitor, and the Central Bank’s know-your-customer rules require a bank to confirm your identity and your status in the country before opening a full account. A visitor stamp usually doesn’t clear that bar.

There’s a narrow exception worth knowing: Central Bank KYC guidance lets banks open an account for a non-Kenyan who has either valid immigration status or a local Kenyan mandated signatory on the account. So a foreigner setting up a business with a Kenyan partner, for example, may open a business account through that route. For an ordinary personal account, though, plan on sorting your immigration status first — or use the diaspora route from abroad, which is built for people without Kenyan residency.

If you only need to spend money while you scout neighbourhoods on a 90-day eTA, you don’t need a bank account at all. Register M-Pesa with your passport, and pay for everything from your phone while you decide where to live.

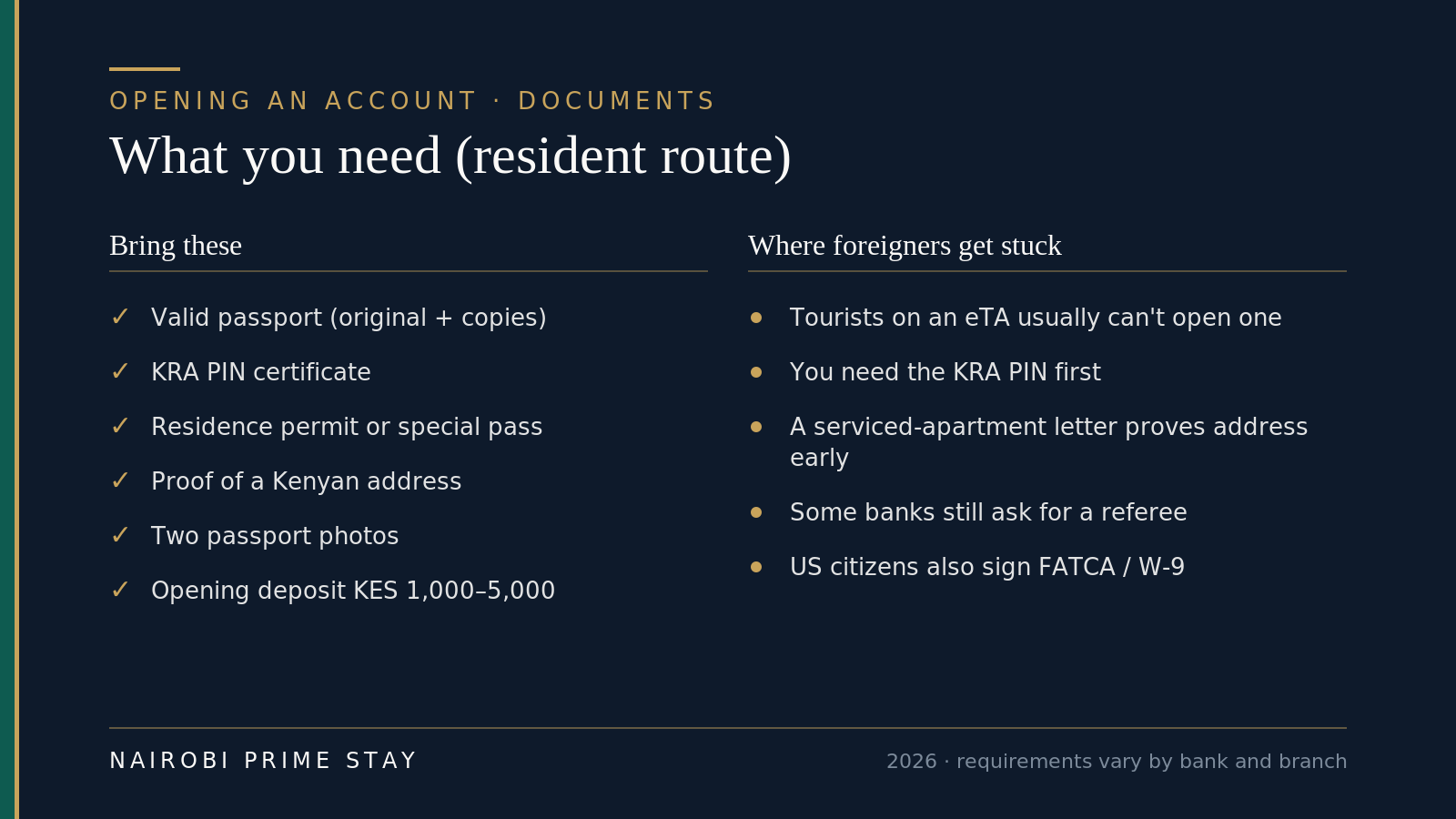

Documents you need — the resident route

For a resident account, banks want to see who you are, that you’re legally in Kenya, where you live, and that you’re in the tax system. The list is consistent across banks, with small variations branch to branch.

What to bring and where people get stuck — requirements vary by bank and branch, so call ahead.

What to bring and where people get stuck — requirements vary by bank and branch, so call ahead.

The typical document list:

- Your passport — the original, plus a photocopy of the photo page and of your permit or visa page.

- A KRA PIN certificate — your Kenyan tax ID, from the iTax portal. Almost every bank requires it. More on getting one as a foreigner below.

- Proof of immigration status — your residence permit, dependant’s pass, investor permit or special pass. The threshold varies: some banks open a basic account on a special pass, others want a full permit.

- Proof of address — a utility bill, a lease, or a letter. Just arrived and don’t have a long-term place? A serviced-apartment address letter or an employer letter usually works to get started.

- Passport photos — usually two.

- An opening deposit — typically KES 1,000–5,000, depending on the account.

- Sometimes a referee or introduction letter — an existing account holder, or a letter from your employer, depending on the bank.

- A FATCA self-certification — as a US citizen you’ll confirm your US tax status; see the FATCA section below.

A practical tip: take more than you think you need. Originals and copies of everything, two photos rather than one, and your employer or landlord letter even if the bank’s website doesn’t list it. The extra five minutes of photocopying saves a second trip across town.

The non-resident / diaspora route — opening from abroad

If you’re still in the US, you open through a bank’s diaspora desk, and the document mix shifts toward proving who you are and where your money comes from. Kenya’s big banks all court diaspora customers: KCB, Equity (through its online diaspora platform), NCBA, I&M, Co-operative, Absa and others run diaspora accounts you can start without setting foot in Kenya.

A representative example is KCB’s diaspora current account. To open it you provide proof of your address abroad (a utility bill, bank statement, pay stub or driver’s license), a Kenyan KRA PIN, and — for a foreign-currency account — proof of the source of your foreign currency, such as a pay stub, bank statement or employment contract. You complete the bank’s account-opening and indemnity forms, and because you’re in the US you also sign FATCA and W-9 forms. The opening balance is modest (KES 2,000 in KCB’s case), often with no minimum operating balance and no ledger fees on the diaspora product.

What to expect on this route:

- It’s remote, but slower. Activation typically takes about one to four weeks, depending on the bank and how complete your paperwork is.

- Documents may need notarizing. Some banks ask for notarized copies, or verify your identity through an international correspondent bank.

- You still need a KRA PIN. This is the one piece you can’t skip even from abroad — handle it first (below).

- Source-of-funds matters. For foreign-currency and investment accounts especially, be ready to show where the money comes from. It’s standard anti-money-laundering practice, not suspicion of you.

The diaspora route shines if you’re buying property in Kenya from the US, want a place to receive funds before you move, or just like having the account ready. When you arrive and your permit is sorted, you can add or convert to a full resident account.

Getting a KRA PIN as a foreigner

A KRA PIN is non-negotiable, and for foreigners it has its own small process. The PIN is your Kenya Revenue Authority tax ID. You need it to open a bank account, sign a lease, buy a car, set up utilities and buy property — so treat it as the first domino, not an afterthought.

You apply free on the iTax portal. The catch for foreigners: KRA wants a local point of contact. In practice, a foreigner’s PIN application needs a letter of introduction from a KRA-registered tax agent, who acts as your formal intermediary. That’s a real, normal step — many immigration lawyers and accountants who help expats include it — but it means your PIN’s speed depends partly on your agent.

Two things to get right:

- Resident vs non-resident PIN. On iTax you choose your taxpayer type. If you hold a Kenyan permit you register as a resident individual; if you’re applying from abroad without residency, you select the non-resident individual option. Non-resident applicants receive an acknowledgement to present, with supporting documents, to complete registration.

- Timeline. Registration itself can be quick, but official processing for foreigners can take up to around 21–30 business days in some cases, so don’t leave it to the last week. The PIN itself costs nothing — be wary of anyone charging a large “KRA fee.”

Because the PIN sits at the front of the whole chain, getting it early is the single best thing you can do to speed up your move. For how it ties into your wider tax position — residency, what you owe, the US side — see our taxes for expats in Kenya guide. None of this is tax advice; confirm your situation with a cross-border professional.

FATCA and the W-9 — the US-citizen part

If you’re American, expect to sign FATCA paperwork — and don’t be alarmed by it. FATCA (the Foreign Account Tax Compliance Act) is a US law that requires foreign banks to report accounts held by US persons to the IRS. Kenyan banks comply, so when a US citizen opens an account here, the bank asks you to certify your US status, usually on a W-9 form (which provides your US taxpayer ID), plus the bank’s own FATCA self-certification.

What this means for you in practice:

- It’s routine. Every US person opening an account abroad signs it. The bank can’t open the account without it.

- It doesn’t create new US tax. It’s a reporting mechanism. You already owe US tax on worldwide income as a citizen — FATCA just means the account may be reported.

- You may have your own US filing. Holding foreign accounts can trigger a US FBAR (FinCEN Form 114) filing if your combined foreign balances cross US$10,000 at any point in the year, and possibly Form 8938. That’s a US obligation, separate from Kenya — flag it with your US tax preparer.

Keep your US bank account and a US card open through all of this. They’re your bridge to US income and a backup when a Kenyan card gets declined on an overseas site. To move money between the two countries cheaply, compare a low-spread service against your bank — see sending money to and from Kenya.

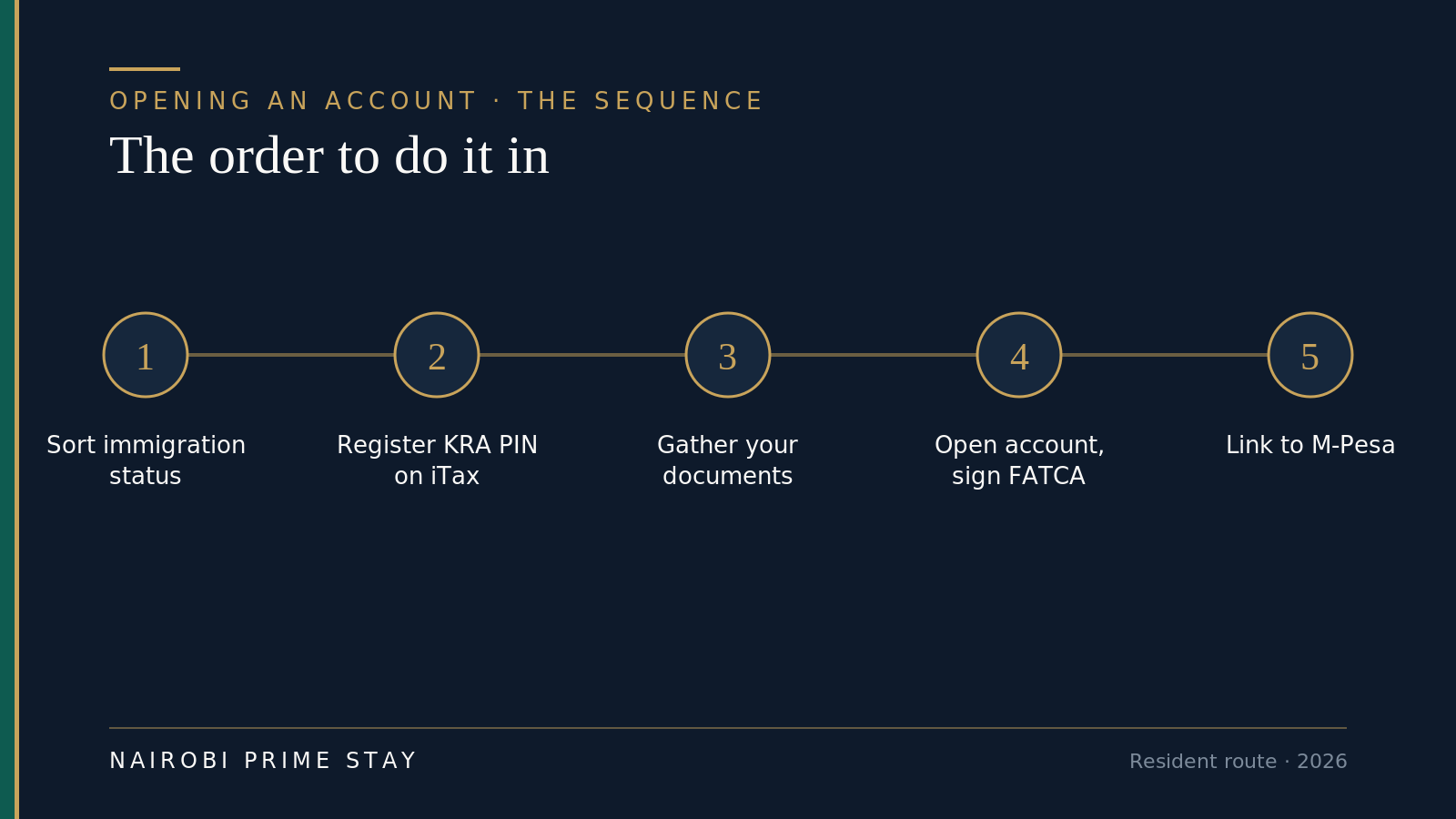

The sequence, step by step

For the resident route, do it in this order. Each step clears the way for the next.

The resident-route order of operations — 2026.

The resident-route order of operations — 2026.

- Sort your immigration status. A work permit, investor permit, dependant’s pass or special pass is the gate. Until you have one (or a Kenyan mandated signatory), most banks can’t open a personal account. An immigration lawyer files the right class for your situation.

- Register your KRA PIN. On iTax, with a tax agent’s introduction letter. Do this as early as your status allows — it’s the bottleneck.

- Gather your documents. Passport (plus copies), PIN certificate, permit/pass, proof of address, two photos, the opening deposit, and any referee or employer letter the bank wants.

- Open the account in person. Visit the branch (or finish a pre-started online application there). You’ll sign the account forms and your FATCA/W-9. Approval can be same-day, or take a few days while compliance reviews your file.

- Link it to M-Pesa and switch on alerts. Connect the account to your M-Pesa wallet in the bank’s app, turn on transaction SMS, and you’re running. See the M-Pesa guide for the how-to.

If you start the KRA PIN and a non-resident account from abroad, you compress this: you land with the PIN in hand and a diaspora account live, and you only need to add a resident account once your permit is through.

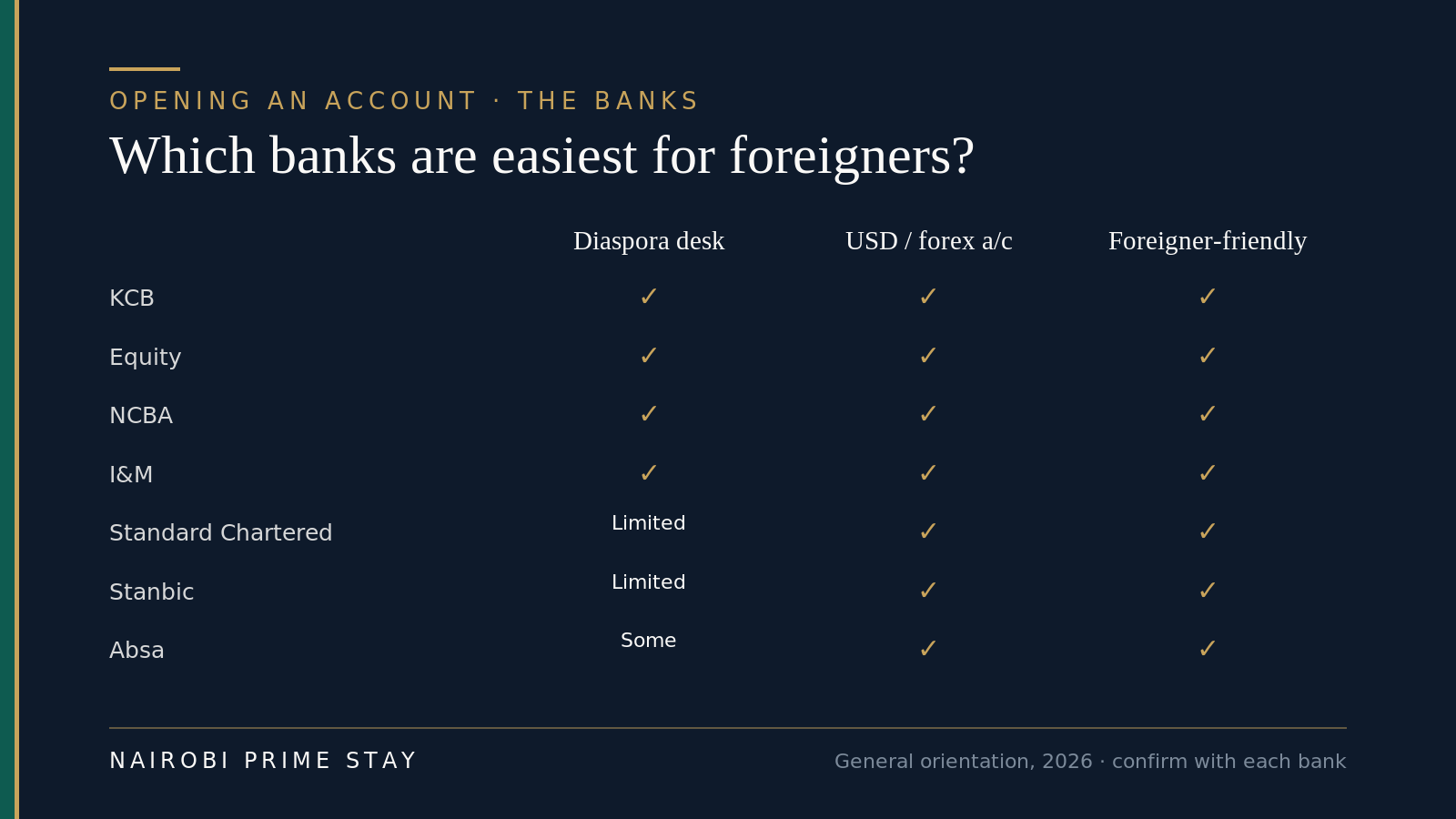

Which banks are easiest for foreigners?

No bank is objectively “best” for opening as a foreigner, but a few are known for smoother onboarding. The split mirrors the wider banking picture: the big retail banks give you reach, while the international-feeling banks give you a familiar, expat-friendly process and dollar accounts.

General orientation for 2026 — confirm current diaspora products and requirements with each bank.

General orientation for 2026 — confirm current diaspora products and requirements with each bank.

| Bank | Diaspora desk (remote open) | USD / forex account | Notes for foreigners |

|---|---|---|---|

| KCB | Yes — strong | Yes | Big network; diaspora current account, low opening balance |

| Equity | Yes — online platform | Yes | Largest reach; diaspora savings/investment products |

| NCBA | Yes | Yes | Good apps; added fully digital onboarding |

| I&M | Yes | Yes | Service-led, multi-currency, well-regarded |

| Standard Chartered | Limited | Yes | International feel, premium tiers, multi-currency |

| Stanbic | Limited | Yes | Multi-currency, premium, African footprint |

| Absa | Some | Yes | Familiar, tailored expat solutions |

A simple way to choose: if you want to open from abroad before you move, start with a strong diaspora desk — KCB, Equity, NCBA or I&M. If you’re already here and paid in dollars, the international banks (Standard Chartered, Stanbic, Absa, plus NCBA and I&M) make a multi-currency account easy. Many foreigners end up with two: a big-network account for daily Kenyan life and a multi-currency one for their dollars. Treat the table as a starting point — banks reshuffle products and requirements often, so confirm the current offer before you commit.

How long does it really take?

Honestly, it depends on the route and your paperwork — but here’s a realistic picture.

- The KRA PIN is the variable. Registration can be done in a sitting, but foreigner processing can run up to around 21–30 business days in some cases. Start it first.

- A resident account, once you have the PIN and permit, is often opened same-day, with the card and full activation following within a few days while compliance clears you.

- A diaspora account opened from abroad usually takes about one to four weeks to activate, longer if documents need notarizing or correspondent-bank verification.

- The whole chain — permit, then PIN, then account — is best measured in weeks, not days, mostly because of the permit and PIN. The banking itself is the fast part.

The practical takeaway: front-load the slow steps. Get your immigration filing and KRA PIN moving as early as you can, ideally before or right when you arrive, and the account falls into place quickly after.

A realistic example

Say you’re moving from Texas to Nairobi for a two-year NGO contract, with a spouse and one child. Two months before you fly, you engage a tax agent and register your KRA PIN from the US through the non-resident option — done and in hand before departure. You also open a KCB diaspora account online, signing the FATCA and W-9 forms, so you have somewhere to receive funds. You land, get a Safaricom SIM and register M-Pesa at the airport, and settle into a serviced apartment while you find a home.

Your employer files your work permit and your family’s dependant’s passes. Once the permit’s through, you walk into a branch with your passport, permit, the KRA PIN you already have, a letter from your serviced-apartment host as proof of address, two photos and the opening deposit, and open a resident shilling current account plus a US-dollar account for your overseas pay. You link both to M-Pesa. Total elapsed time was governed entirely by the permit — the banking took an afternoon. Because you’d front-loaded the PIN and diaspora account, the on-the-ground setup barely slowed you down.

The honest balance

Opening as a foreigner has real friction and real workarounds. Here’s the fair picture.

| The good | The less good |

|---|---|

| A foreigner genuinely can open an account — two routes cover most situations | You can’t open a full account on a tourist eTA |

| You can start from abroad before you even move (diaspora desks) | The KRA PIN needs a tax agent’s letter and can take weeks |

| Once your PIN and permit are sorted, opening is fast — often same-day | The permit/PIN chain, not the bank, is the slow part |

| Big banks actively want diaspora customers; low opening balances | Diaspora documents may need notarizing or correspondent-bank checks |

| US-dollar and multi-currency accounts are widely available | FATCA/W-9 and possible US FBAR filing add US-side paperwork |

| M-Pesa bridges the gap so you’re never stuck while you wait | Requirements vary by bank and branch — always call ahead |

None of the negatives is a dealbreaker. They’re one-time hurdles you plan around, then forget.

Your account-opening checklist

A simple order of operations:

- Decide your route: resident (you’ll be living in Kenya) or non-resident/diaspora (opening from abroad).

- Start your immigration filing early if you’re moving — the permit is the gate for a resident account.

- Register your KRA PIN on iTax via a KRA-registered tax agent — do this first; it’s the bottleneck.

- On arrival, get a Safaricom SIM and M-Pesa with your passport so you can spend from day one.

- Choose a bank: a diaspora desk (KCB, Equity, NCBA, I&M) to open from abroad, or an international bank if you want dollar accounts on the ground.

- Gather documents: passport + copies, KRA PIN, permit/pass, proof of address, two photos, opening deposit, plus any employer/referee letter.

- As a US citizen, be ready to sign FATCA and a W-9.

- Open the account in person (resident) or remotely (diaspora); expect same-day to a few days, or 1–4 weeks respectively.

- Link the account to M-Pesa and turn on transaction alerts.

- Keep your US account and card open, and flag foreign-account FBAR filing with your US tax preparer.

Frequently asked questions

Can a foreigner open a bank account in Kenya?

Yes. A foreigner can open a Kenyan bank account by one of two routes. If you live in Kenya on a residence permit or pass, you open a normal resident account at a branch with your passport, permit, KRA PIN, proof of address and a small deposit. If you’re still abroad, you open a non-resident or diaspora account remotely through a Kenyan bank’s diaspora desk. What you can’t do is open a full account as a tourist on an eTA.

Can I open a Kenyan bank account from abroad as a non-resident?

Yes. Banks like KCB, Equity, NCBA and I&M run diaspora desks that let you open an account remotely from the US — online, by email, or through a correspondent bank. You’ll provide your passport, a Kenyan KRA PIN, proof of your overseas address, source-of-funds proof, and FATCA and W-9 forms as a US person. Activation usually takes about one to four weeks, and some banks ask for notarized copies of your documents.

What documents do I need to open a bank account in Kenya as a foreigner?

For a resident account you typically need your passport (original plus copies), a KRA PIN certificate, your residence permit or pass, proof of a Kenyan address, two passport photos, and an opening deposit of about KES 1,000-5,000. Some banks also ask for a referee or an employer letter, and US citizens sign a FATCA self-certification. Requirements vary by bank and branch, so call ahead and bring more copies than you think you need.

Do I need a KRA PIN to open a bank account, and can a foreigner get one?

Yes, almost every Kenyan bank requires a KRA PIN, and foreigners can get one free on the iTax portal. The catch is that a foreigner’s application generally needs a letter of introduction from a KRA-registered tax agent, who acts as your local point of contact. You choose a resident or non-resident taxpayer type depending on your status. Apply early - official processing can take up to around 21-30 business days, and the PIN sits at the front of the whole chain.

Can I open a bank account on a tourist visa or eTA?

Generally no. An eTA marks you as a visitor, and the Central Bank’s know-your-customer rules require a bank to verify your legal status before opening a full account, which a visitor stamp usually doesn’t satisfy. The exception is that a bank may open an account for a non-Kenyan who has either valid immigration status or a local Kenyan mandated signatory, which can suit a business account. For ordinary personal banking, sort your permit first or use the diaspora route from abroad.

Which bank is easiest for a foreigner to open an account with?

It depends on your route. To open from abroad, start with a strong diaspora desk - KCB, Equity, NCBA or I&M all let you apply remotely. If you’re already in Kenya and paid in dollars, the international-feeling banks (Standard Chartered, Stanbic, Absa, plus NCBA and I&M) make a multi-currency account straightforward. Many foreigners keep two accounts: a big-network one for daily life and a multi-currency one for their dollars.

Do US citizens have to sign FATCA forms to open a Kenyan account?

Yes. FATCA is a US law requiring foreign banks to report accounts held by US persons to the IRS, and Kenyan banks comply, so you’ll sign a FATCA self-certification and usually a W-9. It’s routine and doesn’t create new US tax by itself - you already owe US tax on worldwide income as a citizen. Separately, holding foreign accounts can trigger a US FBAR filing if your combined foreign balances top US$10,000 in a year, so flag it with your US tax preparer.

How long does it take to open a bank account in Kenya as a foreigner?

The banking is fast; the paperwork around it is the slow part. A resident account is often opened the same day once you already hold a KRA PIN and permit, with the card following in a few days. A diaspora account opened from abroad usually takes about one to four weeks to activate. The real variable is the KRA PIN, which can take up to roughly 21-30 business days for foreigners, so start it first.

Final thoughts

Opening a bank account in Kenya as a foreigner is far simpler than it looks from afar — once you accept that the account is the last step, not the first. The bank isn’t the hard part. The permit and the KRA PIN are, and both are routine if you start them early and use a good immigration lawyer and tax agent. Get those moving, keep M-Pesa running in the meantime, and the account opens in an afternoon.

Our honest advice: pick your route deliberately. If you’re still in the US, open a diaspora account and register your KRA PIN before you fly, so money is half-sorted when you land. Once you’re here and your permit is through, add a resident shilling account — plus a US-dollar account if you’re paid in dollars — and link both to M-Pesa. That covers nearly all of expat life. None of this is legal or tax advice; for anything tied to your tax position, confirm with a cross-border professional and the official source.

Related reading

- Moving to Nairobi: the complete guide — the hub that ties together every part of your move.

- Banking in Nairobi for expats — choosing a bank, fees, dollar accounts and the wider picture.

- M-Pesa explained for newcomers — register a line, load and spend, pay bills, stay safe.

- Sending money to and from Kenya — the cheapest ways to move dollars and shillings.

- Taxes for expats in Kenya — tax residency, your KRA PIN and what you owe.

- The USD/KES currency guide — the rate, where to change money, and budgeting around it.

- Visas for Americans moving to Kenya — the eTA, permits and the status you need to bank.

- Cost of living in Nairobi — where your money goes each month.

Get set up the easy way

You don’t need a Kenyan bank account to land softly. Book a serviced apartment for your first month — Wi-Fi, cleaning, generator and security included — and use M-Pesa from day one while your permit, KRA PIN and bank account come together at their own pace. A $50 deposit reserves your place, and the balance is paid on arrival.

Not sure which area or building fits your commute and budget? Our AI relocation assistant can shortlist apartments and answer your move-to-Nairobi questions in a couple of minutes, any time of day.

Keep reading

Related guides

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.