Guides · Money

Banking in Nairobi for Expats: An Honest 2026 Guide

Banking in Nairobi for Expats: An Honest 2026 Guide

Here’s the part most guides bury: in Nairobi, your phone matters more than your bank card. M-Pesa, Kenya’s mobile money, handles most of daily life — rent, the market, taxis, your electricity. Your bank account sits behind it, holding your salary and savings, paying the big bills, and feeding cash onto your phone when you need it. Get both set up and the two work as one smooth system.

The banking itself is modern and easy once you’re in. Apps are slick, transfers are instant, cards work everywhere that takes cards. The friction is the front door: as a foreigner you can’t just walk in and open an account on a tourist stamp. You need a residence permit and a tax PIN first, and the order you do things in matters.

This guide is for Americans setting up money in Kenya — which banks to consider, what local versus US-dollar accounts are for, what it costs, what you actually need to open an account, and how to wire your bank to M-Pesa so daily life just flows. We’ll keep every figure to a 2026 range and point you at the official source to confirm against, because fees and rates move.

The quick version (TL;DR)

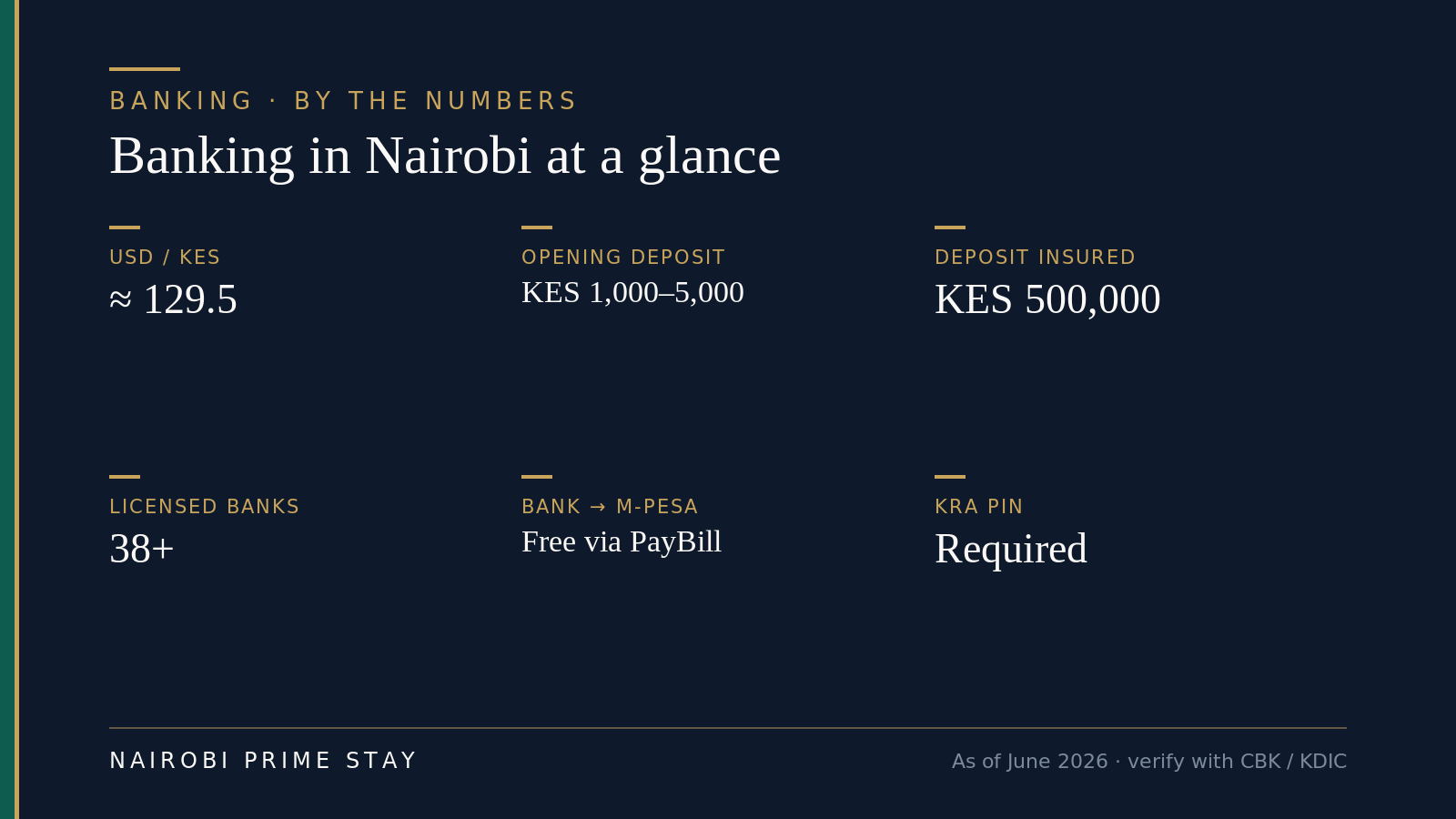

You can’t open a full Kenyan bank account as a tourist — you need a valid residence permit (or at least a special pass) plus a KRA tax PIN, your passport, and proof of address. Once you have those, opening an account takes a branch visit and a small deposit, usually KES 1,000–5,000. Equity and KCB have the biggest branch and ATM networks; Standard Chartered, Stanbic, Absa, NCBA and I&M lean more toward premium and expat-style banking, including US-dollar and multi-currency accounts if you’re paid in dollars. Day to day, you’ll lean on M-Pesa and link it to your bank, which is free and instant in both directions. Deposits are insured up to KES 500,000 per bank by the Kenya Deposit Insurance Corporation, so spread large balances or keep some money in the US. Keep your American account and card open too — and use a service like Wise to move money between countries.

Indicative 2026 figures for orientation — rates, fees and rules change, so confirm with the Central Bank of Kenya, KDIC and your bank.

Indicative 2026 figures for orientation — rates, fees and rules change, so confirm with the Central Bank of Kenya, KDIC and your bank.

Why this matters when you’re new

Money is one of the first walls new arrivals hit. You land, you want to pay a deposit on an apartment, buy a SIM, stock the fridge — and you discover that the smooth account-opening you imagined needs documents you don’t have yet. The paperwork runs in a chain: permit, then PIN, then bank account, then lease. Skip a link and you stall.

The good news is that the gap is bridgeable. M-Pesa is fast to set up and covers you for weeks while the bank account comes together. Knowing the sequence — and which bank fits how you’ll actually live — saves you the classic newcomer mistake of opening the wrong account at the wrong bank and paying for it in fees every month.

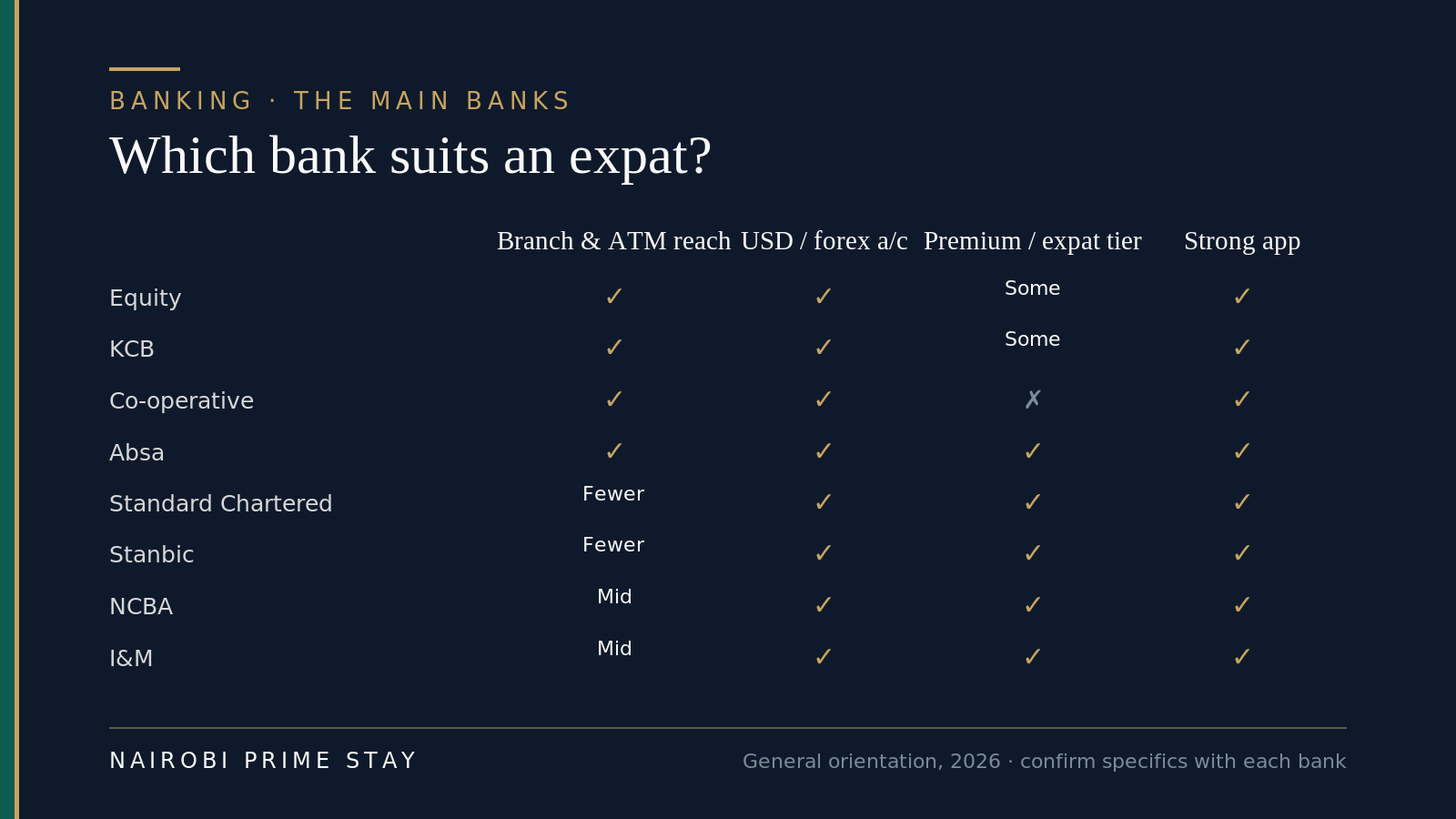

The main banks — and who each one suits

Kenya has around 38 licensed commercial banks, but expats cluster around a handful. They split loosely into two camps: the big retail banks with branches and ATMs on every other corner, and the more premium or international banks that feel familiar if you’ve banked in London or New York. None is objectively “best” — the right one depends on whether you value reach, a polished app, dollar accounts, or a relationship manager who’s used to foreigners.

Equity Bank is the giant. It has the widest reach in the country, a huge agent and ATM network, and almost all its banking happens on the phone rather than in a branch. If you want to be able to bank anywhere, including upcountry, Equity is hard to beat. Its Equity Mobile app is the everyday workhorse, and Equity Premier is its tier for higher balances.

KCB (Kenya Commercial Bank) is the other big beast — vast branch network, strong app rebuilt in 2025, full forex services. Like Equity, it’s a sensible default if branch and ATM access matter more to you than a boutique feel.

Co-operative Bank is the third of the big retail trio. Wide network, solid app (MCo-op Cash), popular with salaried Kenyans and businesses. Less of an “expat premium” feel, but reliable and everywhere.

Standard Chartered is the one most international movers gravitate to. It’s built for cross-border life: multi-currency and US-dollar accounts, a clean app (SC Mobile), priority banking tiers, and the comfort of a global name. Fewer branches than Equity or KCB, but you’ll barely need them.

Stanbic Bank (part of Africa’s Standard Bank group) is similar in spirit — multi-currency accounts, a strong premium offering, and a good fit if you want international banking with an African footprint.

Absa Kenya (formerly Barclays) keeps much of its old international polish, offers tailored expat solutions and a good app, and has decent branch coverage. A frequent expat pick.

NCBA and I&M are mid-sized banks that punch above their weight for professionals. NCBA’s apps (NCBA NOW and its lifestyle offshoot LOOP) are genuinely good, it added fully digital account opening in 2025, and it’s strong on cards and forex. I&M is well regarded for service and multi-currency banking. DTB (Diamond Trust) and Family Bank round out the list of names you’ll hear.

A simple way to choose: if you want maximum reach and agent access, start with Equity or KCB. If you’re paid in dollars and want a familiar, international experience, look at Standard Chartered, Stanbic, Absa, NCBA or I&M. Many expats end up with two: a big-network account for everyday Kenyan life and a multi-currency account for their dollars.

General orientation for 2026 — confirm current accounts, tiers and fees with each bank before you choose.

General orientation for 2026 — confirm current accounts, tiers and fees with each bank before you choose.

| Bank | Best for | Branch & ATM reach | USD / forex account | App |

|---|---|---|---|---|

| Equity | Maximum reach, agents everywhere | Largest | Yes | Equity Mobile |

| KCB | Big network + full forex | Very large | Yes | KCB Mobile |

| Co-operative | Everyday retail banking | Large | Yes | MCo-op Cash |

| Standard Chartered | Premium, international, multi-currency | Smaller, urban | Yes | SC Mobile |

| Stanbic | Multi-currency + premium | Smaller, urban | Yes | Stanbic app |

| Absa | Familiar, tailored expat banking | Good | Yes | Absa app |

| NCBA | Cards, forex, great apps | Mid-size | Yes | NCBA NOW / LOOP |

| I&M | Service-led, multi-currency | Mid-size | Yes | I&M On The Go |

Treat the table as a starting point, not gospel — banks reshuffle accounts and fees often, so check the current offer.

Shilling accounts vs US-dollar accounts

Most expats need a Kenyan shilling account, and many add a US-dollar one. Here’s how to think about it.

A shilling (KES) account is your day-to-day account. Your local salary lands here, your rent and bills go out from here, and it feeds your M-Pesa. You’ll want one regardless. It comes as a current account (for spending, with a debit card and checkbook) or a savings account (for holding money, sometimes with small interest).

A US-dollar or multi-currency account is worth it if you’re paid in dollars, get transfers from the US, or want to hold money in dollars rather than convert everything to shillings. Standard Chartered, Stanbic, Absa, NCBA, I&M, Equity and KCB all offer foreign-currency accounts. The catch is that you’ll still convert to shillings to spend locally, and every conversion has a spread — the gap between the buy and sell rate the bank gives you. For big or regular conversions, compare your bank’s rate against a service like Wise before assuming the bank is cheapest.

One honest note on the exchange rate: as of early July 2026 the US dollar buys about 129.4 shillings, and the shilling has been fairly stable through the year. But it has swung hard in the past, so don’t bank on any particular rate. If you earn dollars and spend shillings, a stable or strengthening dollar helps you; if that flips, your local spending power drops. Our USD/KES currency guide goes deeper, and the Central Bank of Kenya publishes the official daily rate.

Cards, ATMs and online banking

Day-to-day, Kenyan banking feels familiar. You get a Visa or Mastercard debit card that works at shops, restaurants, supermarkets and online, and at ATMs across the country. Contactless is common in Nairobi. Credit cards exist but are harder for newcomers to get early on — banks want to see history first.

The apps are the real workhorses. Equity Mobile, KCB Mobile, SC Mobile, NCBA NOW, the Absa, Stanbic, Co-op and I&M apps all let you do almost everything from your phone: check balances, pay bills, move money, buy airtime, and — crucially — push money to and from M-Pesa. Kenya is genuinely ahead of the US here; 94–99% of bank transactions happen outside a branch.

For moving money between banks, Kenya has PesaLink, an instant account-to-account transfer system that most banks support. You send straight to someone’s phone number or account at another bank and it arrives in seconds, usually cheaper than an old-style transfer. It’s the bank world’s answer to M-Pesa, and you’ll use it for things like paying a landlord or a contractor who wants a bank transfer rather than mobile money.

A few practical habits worth forming early. Turn on transaction SMS or app alerts so you see every debit. Withdraw cash from ATMs inside malls or bank branches rather than quiet street machines. And keep one US card active for international subscriptions and travel — Kenyan cards sometimes get declined on overseas sites, and you don’t want to be stuck.

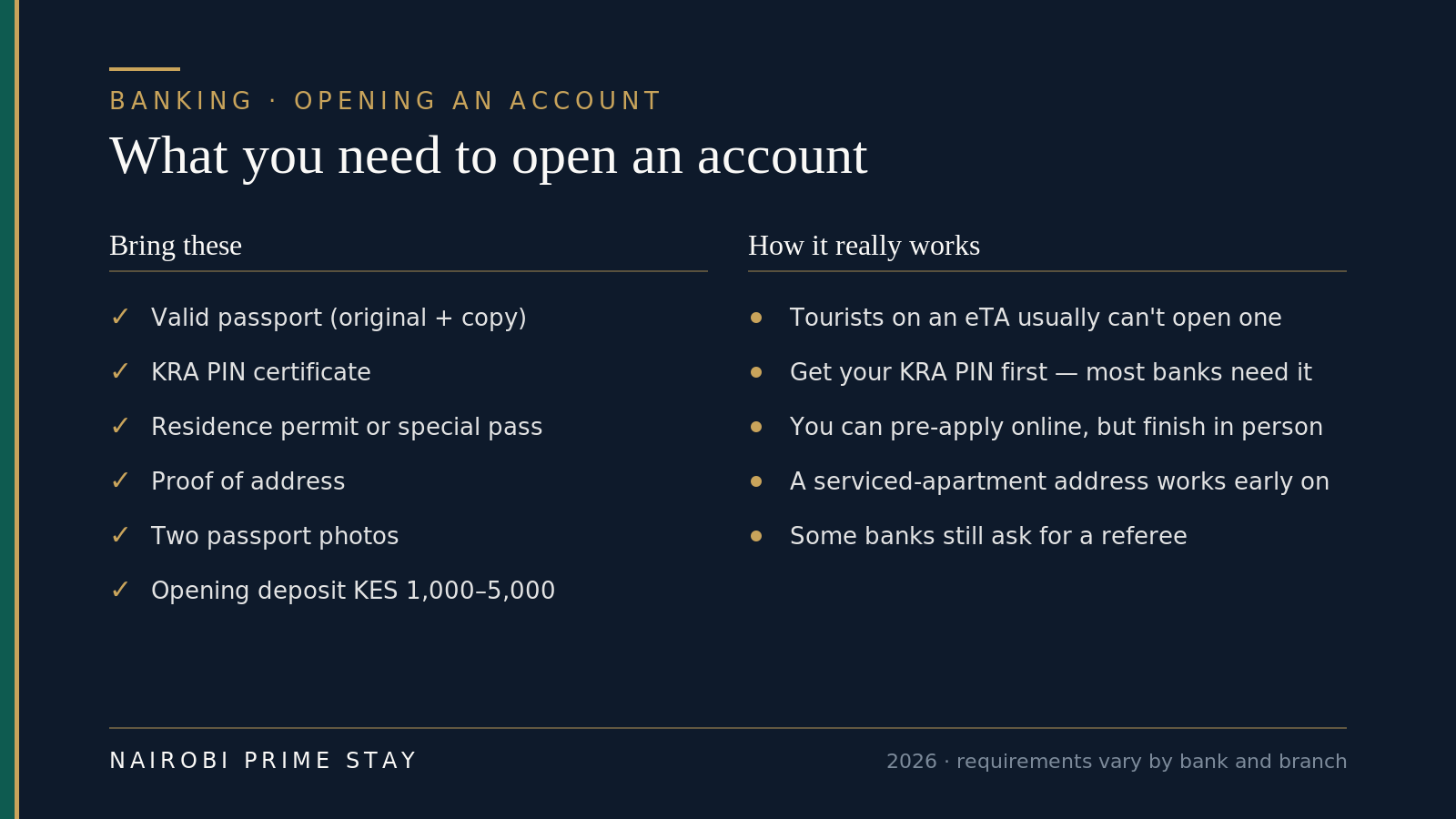

What you need to open an account

The single thing that trips up newcomers: you generally can’t open a Kenyan bank account as a tourist. Banks must verify your identity and your legal status in the country, so a visit stamp or eTA usually isn’t enough. You need to be here on a real footing — a residence permit, a dependant’s pass, or at least a special pass — and you need a tax PIN.

What to bring and how it actually plays out — requirements vary by bank and branch, so call ahead.

What to bring and how it actually plays out — requirements vary by bank and branch, so call ahead.

Here’s the typical document list:

- Your passport — the original plus a photocopy of the photo page and your permit/visa page.

- A KRA PIN certificate — your Kenyan tax ID, from the iTax portal. Most banks require it, and you can usually register for it once you hold a permit. It’s also needed to sign a lease, buy a car, and set up utilities, so make it an early priority.

- Proof of immigration status — your residence permit, dependant’s pass, or special pass. The exact threshold varies by bank and even by branch; some will open a basic account on a special pass, others want a full permit.

- Proof of address — a utility bill, a lease, or a letter. If you’ve just arrived and don’t have a long-term place yet, a serviced-apartment address or a letter from your employer often works.

- Passport photos — usually two.

- An opening deposit — typically KES 1,000–5,000.

- Sometimes a referee — an existing account holder or an employer letter, depending on the bank.

The smart sequence is permit → KRA PIN → bank account → lease. Each one clears the way for the next. You can often pre-register or start an application online — NCBA and others now offer digital onboarding — but Kenyan rules require an in-person identity check for foreigners, so plan to finish at a branch with your originals. Account approval can be same-day or take a few days while compliance reviews your file.

Because this sequence is where most people get stuck, we’ve written a dedicated walkthrough: see opening a bank account in Kenya as a foreigner for the step-by-step, bank by bank.

Fees — what to watch, and how to keep them low

Be honest with yourself here: Kenyan banks charge for more things than you may be used to. None of it is huge, but it adds up if you pick the wrong account. Ask any bank for its tariff guide (the published fee schedule) before you sign, and read it.

Common charges to look for:

- Monthly or ledger fees — a flat account-maintenance charge. Some accounts waive it if you keep a minimum balance.

- Minimum balance — fall below it and you may earn nothing or pay a fee.

- ATM withdrawal fees — usually free at your own bank’s ATMs, charged at other banks’ machines.

- Card fees — an annual debit-card charge, and a fee to replace a lost card.

- Transfer fees — PesaLink, RTGS and SWIFT (international) transfers each have their own charge; international wires are the priciest.

- SMS-alert fees — a small monthly charge for transaction texts.

- Forex spread — on dollar conversions, the real cost is the rate, not just any stated fee.

On top of the bank’s own charges, Kenyan bank fees also carry government excise duty, so the sticker fee isn’t the whole cost — ask for the all-in figure. Rates and levies change with each year’s Finance Act, so confirm the current position rather than trusting an old number.

How to keep fees down: match the account to how you’ll use it (don’t take a premium account you won’t fund), keep enough in to clear any minimum-balance fee, use your own bank’s ATMs, do most of your moving-around on the app and M-Pesa where it’s cheapest, and route international money through a low-spread service. For a sense of how banking fits your wider budget, see our cost of living in Nairobi guide.

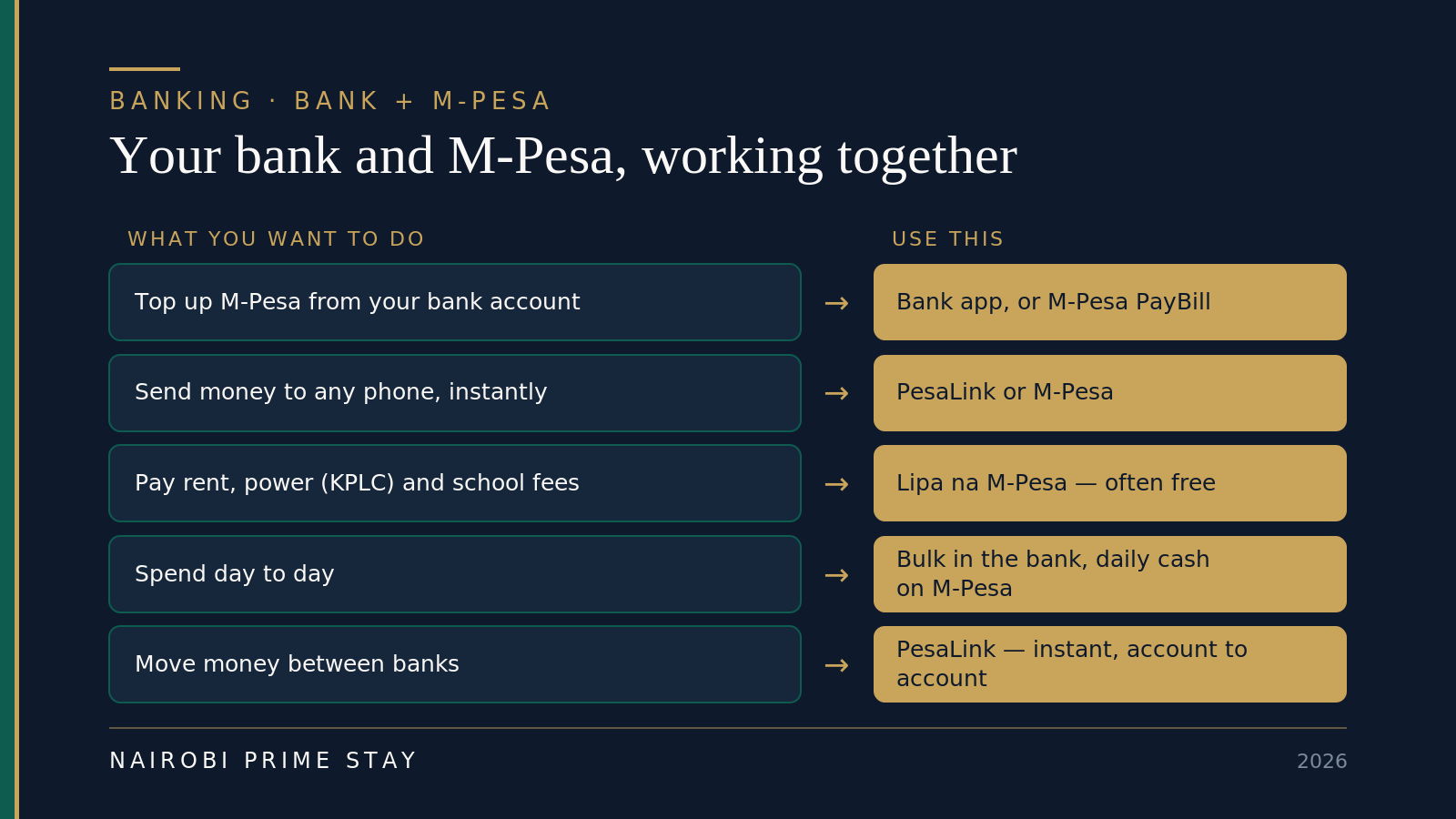

Linking your bank to M-Pesa — the part that makes it all flow

This is the trick that turns two separate systems into one. In Kenya, your bank account and your M-Pesa wallet talk to each other, instantly and usually for free, and once you set it up daily life gets very smooth.

Your bank holds the money; M-Pesa spends it. Linked, they cover almost everything.

Your bank holds the money; M-Pesa spends it. Linked, they cover almost everything.

The everyday pattern looks like this. Your salary or transfer lands in your bank account. When you need spending money, you push some to M-Pesa — either from inside your bank’s app (most have a “to M-Pesa” option) or by paying your bank’s PayBill from the M-Pesa menu. Then you use M-Pesa for the small stuff: the market, taxis, the duka (corner shop), splitting a bill. For bigger payments — rent, a contractor — you pay by bank transfer or PesaLink, or by M-Pesa if the landlord prefers it.

Two things newcomers love once they get it. First, paying bills via Lipa na M-Pesa PayBill is usually free to you — topping up your own bank account, paying KPLC for electricity (PayBill 888880), or paying school fees often costs nothing in M-Pesa fees. Second, you don’t carry much cash; the phone is the wallet. Keep larger sums in the bank where they’re safer and insured, and only what you’ll spend on M-Pesa.

To set the link up, you usually register your phone number in your bank’s app, or simply use the bank’s PayBill number whenever you want to move money. Our M-Pesa guide for newcomers walks through registering a line, loading and withdrawing cash, paying bills, and staying safe from the common scams.

Is your money safe? Deposit insurance and sensible habits

Yes, with the same common sense you’d use anywhere. Kenya’s banking sector is regulated by the Central Bank of Kenya, and deposits are protected by the Kenya Deposit Insurance Corporation (KDIC) up to KES 500,000 per depositor, per bank — roughly $3,800–4,000 at mid-2026 rates. The cover is automatic; you don’t register for it. There’s a 2026 proposal to double the limit to KES 1 million — the public-consultation window closed at the end of May 2026 — but as of July 2026 it hasn’t taken effect, so plan around KES 500,000.

What that means in practice: if you’ll hold more than the insured limit, it’s sensible to spread it across more than one bank, or keep a chunk in the US. Stick to established, well-capitalized banks — the big names in this guide are all long-standing. And use ordinary security habits: a strong unique PIN, app alerts on, never share an OTP or PIN (no real bank will ask for it), and be alert to “your account is blocked, confirm your details” texts and calls, which are scams.

A realistic example

Say you’re a remote worker arriving on a digital-nomad permit. Week one, you get a Safaricom SIM and register M-Pesa at the airport, so you can pay for taxis and groceries straight away while you settle into a serviced apartment. With your permit sorted, you register a KRA PIN online, then open a shilling current account at a big-network bank (Equity or KCB) and a US-dollar account where your overseas pay lands. You link the bank to M-Pesa. Now your dollars arrive in the USD account, you convert what you need to shillings (comparing your bank’s rate with Wise), push spending money to M-Pesa, and pay rent by transfer. Total setup time once the permit’s in hand: a few days. After that, money is the easy part of your week.

Can you open a Kenyan bank account from the US before you move?

For most Americans, no — not a full one. The “diaspora banking” programmes you’ll find on KCB, Equity and Co-operative Bank websites are built for Kenyan citizens living abroad, and they lean on a Kenyan national ID that you don’t have. As a US citizen with no Kenyan paperwork, banks will want you in the country, in a branch, with a residence permit (or at least a special pass) and a KRA PIN before they’ll open anything. A few premium banks will start the conversation by email and pre-fill forms for you, which saves a visit, but the account still switches on after you’ve landed and your status is verified.

What you can do from the US is set the table. Open a Wise or similar multi-currency account before you fly, so you can hold dollars and convert to shillings at a fair rate from day one. Keep your US checking account and at least two US cards open. Gather the documents your bank will want — passport, permit or pass, KRA PIN certificate, proof of address (your lease or a letter from your serviced apartment works), passport photos. And get your visa and permit strategy straight first, because immigration status is the gate everything else swings on.

The bridge for your first weeks is simpler than people expect: your US cards for supermarkets and restaurants, M-Pesa (registered with just your passport) for everything else. Plenty of newcomers run this two-rail setup for a month or two — including paying rent — while the permit, PIN and account come together. There’s no penalty for arriving un-banked; there’s only cost in rushing it.

Will your Kenyan bank tell the IRS about your account? FATCA, W-9s and FBAR

Yes — plan on it. When you open an account as a US citizen, the bank will hand you a Form W-9 along with a FATCA consent form; this is standard at Kenyan banks, not a red flag. Kenya hasn’t signed a FATCA intergovernmental agreement with the US as of July 2026, but the major Kenyan banks registered directly with the IRS as participating foreign financial institutions years ago, so they identify and report US-person accounts anyway. If a bank later sends you a “FATCA letter” asking you to confirm your US status, answer it by the deadline — ignoring it can get your account restricted.

The reporting duties that actually bite are your own. If the combined value of your non-US financial accounts — bank accounts, and yes, arguably your M-Pesa balance — exceeds $10,000 at any point in the year, you must file an FBAR (FinCEN Form 114) with the US Treasury. Separately, Form 8938 kicks in at higher thresholds — for Americans living abroad, $200,000 in foreign financial assets on the last day of the year, or $300,000 at any point ($400,000/$600,000 filing jointly). Neither form usually means extra tax; both carry ugly penalties for silence. Keep a simple year-end note of each account’s highest balance, and read our taxes for expats in Kenya guide for the fuller picture. None of this is tax advice — a cross-border CPA is worth the fee for your first year’s filing.

The honest balance

Banking in Kenya has real upsides and a few genuine annoyances. Here’s the fair picture.

| The good | The less good |

|---|---|

| Excellent apps; almost everything done from your phone | More small fees than US banking (ledger, SMS, card), plus excise duty |

| M-Pesa integration makes daily payments effortless | You can’t open an account until your permit and PIN are sorted |

| Instant bank-to-bank transfers via PesaLink | Deposit insurance caps at KES 500,000 per bank |

| US-dollar and multi-currency accounts widely available | Forex spreads can be worse than a dedicated transfer service |

| Established, well-regulated banks with a global feel (StanChart, Stanbic, Absa) | Credit (cards, loans) is hard to get until you’ve built local history |

| Contactless and online card payments are normal in Nairobi | Kenyan cards occasionally get declined on overseas websites |

None of the negatives is a dealbreaker. They’re the kind of thing you plan around once, then forget.

Your first-month banking checklist

A simple order of operations for your first weeks:

- On arrival, get a Safaricom SIM and register M-Pesa with your passport — minutes at the airport or any shop.

- Use M-Pesa for everything while the bank account comes together.

- Get your immigration status sorted (permit, pass, or dependant’s pass) — the bank gate.

- Register your KRA PIN on iTax once you hold a permit.

- Decide what you need: a shilling account for sure, plus a USD/multi-currency account if you’re paid in dollars.

- Compare two or three banks on reach, app, fees and forex — ask each for its tariff guide.

- Open the account in person with your passport, PIN, proof of status and address, photos and the opening deposit.

- Link the account to M-Pesa and turn on transaction alerts.

- Keep your US account and a US card open for international spending and as a backup.

- For moving money home or in, set up a low-spread transfer service and compare it to your bank.

Frequently asked questions

Can I open a bank account in Kenya as a tourist?

Usually not. Kenyan banks must verify your identity and legal status, so a visitor stamp or eTA generally isn’t enough. You typically need a residence permit, dependant’s pass or at least a special pass, plus a KRA tax PIN, your passport and proof of address. Sort your immigration status first, then open the account.

Which is the best bank in Kenya for an expat?

There’s no single best — it depends on what you value. For the widest branch, ATM and agent network, Equity and KCB lead. For a premium, international feel with US-dollar and multi-currency accounts, look at Standard Chartered, Stanbic, Absa, NCBA or I&M. Many expats keep two accounts: a big-network one for daily life and a multi-currency one for their dollars.

Can I open a US-dollar account in Kenya?

Yes. Most major banks offer US-dollar and other foreign-currency accounts, which are handy if you’re paid in dollars or receive transfers from abroad. You’ll still convert to shillings to spend locally, and each conversion carries a spread, so compare your bank’s rate with a service like Wise before moving large sums.

Do I need a KRA PIN to open a bank account?

Almost always, yes. A KRA PIN is your Kenyan tax ID, and most banks require it to open an account. You can register for it free on the iTax portal once you hold a permit. The same PIN is needed to sign a lease, buy a car and set up utilities, so get it early.

How do I link my bank account to M-Pesa?

You link them in your bank’s app, or simply use your bank’s Lipa na M-Pesa PayBill number to move money. Transfers between your bank and M-Pesa are instant and, for depositing to your own account, usually free. Once linked, you keep the bulk of your money in the bank and push spending cash to M-Pesa as you need it.

Are bank deposits insured in Kenya?

Yes. The Kenya Deposit Insurance Corporation (KDIC) protects deposits up to KES 500,000 per depositor, per bank, automatically. If you’ll hold more than that, spread it across banks or keep some abroad. A 2026 proposal would double the limit to KES 1 million and went through public consultation in May 2026, but as of July 2026 it isn’t in force, so plan around KES 500,000.

What does it cost to open and run a bank account in Kenya?

Opening usually needs a small deposit of about KES 1,000 to 5,000. Running the account brings small charges — monthly or ledger fees, ATM fees at other banks, card and SMS-alert fees — plus government excise duty on bank charges. Ask each bank for its tariff guide and pick the account that matches how you’ll actually use it.

Should I keep my US bank account after moving to Kenya?

Yes, keep it open. It’s your link to US income and subscriptions and a backup card, and Kenyan cards are sometimes declined on overseas sites. Use a low-spread service such as Wise to move money between your US and Kenyan accounts, and compare it against your bank’s rate.

What is the US dollar to Kenyan shilling exchange rate in 2026?

As of early July 2026, one US dollar buys about 129.4 Kenyan shillings, and the shilling has been fairly stable through the year. Rates move, though, so check the Central Bank of Kenya or Wise for the live figure before you convert or budget.

Can I open a Kenyan bank account from the US before I move?

Generally no. The diaspora accounts advertised by KCB, Equity and Co-op Bank are designed for Kenyan citizens abroad and rely on a Kenyan national ID. As an American you’ll need to be in Kenya with a residence permit or special pass and a KRA PIN, then open the account in a branch. From the US, set up a multi-currency service like Wise, keep your US cards, and plan to run M-Pesa plus US cards for your first weeks.

Do Kenyan banks report American account holders to the IRS?

Expect it, yes. Kenya has no FATCA intergovernmental agreement with the US as of July 2026, but major Kenyan banks registered directly with the IRS as participating institutions, so they ask US citizens for a Form W-9 at account opening and report US-person accounts. Your own duties matter more: file an FBAR if your non-US accounts together exceed $10,000 at any point in the year, and Form 8938 at higher thresholds. Talk to a cross-border tax professional.

Can I just use my US debit and credit cards in Nairobi?

For your first weeks, largely yes. Visa and Mastercard work in supermarkets, malls, restaurants and hotels, and ATMs dispense shillings on foreign cards. But foreign-transaction and ATM fees stack up, plenty of daily life runs on M-Pesa rather than cards, and card-only living gets awkward outside the malls. Treat US cards as the bridge, register M-Pesa on arrival, and open a local account once your permit and KRA PIN are in hand.

Final thoughts

Banking in Nairobi is one of those things that feels daunting from afar and turns out to be simple once you’re on the ground. The apps are excellent, the M-Pesa link makes daily payments effortless, and the banks themselves are solid and well-regulated. The only real hurdle is the front door — and that’s a paperwork problem, not a banking one. Get your permit and KRA PIN in order, walk into a branch with your documents, and you’re set.

Our honest advice: keep it simple at first. A shilling account at a big-network bank, a US-dollar account if you’re paid in dollars, M-Pesa linked to both, and your US account left open behind you. That covers ninety per cent of expat life. You can always add a premium tier or a second bank later, once you see how you actually spend. None of this is legal or tax advice — for anything tied to your tax position, talk to a cross-border professional and confirm current rules with the official source.

Related reading

- Moving to Nairobi: the complete guide — the hub that ties together every part of your move.

- Opening a bank account in Kenya as a foreigner — the step-by-step, document by document.

- M-Pesa explained for newcomers — register a line, load and spend, pay bills, stay safe.

- Sending money to and from Kenya — the cheapest ways to move dollars and shillings.

- Taxes for expats in Kenya — tax residency, your KRA PIN and what you owe.

- The USD/KES currency guide — the rate, where to change money, and budgeting around it.

- Cost of living in Nairobi — where your money goes each month.

Get set up the easy way

You don’t need a bank account to land softly. Book a serviced apartment for your first month — Wi-Fi, cleaning, generator and security included — and use M-Pesa from day one while your permit, PIN and bank account come together at their own pace. A $50 deposit reserves your place and the balance is paid on arrival.

Not sure which area or building fits your commute and budget? Our AI relocation assistant can shortlist apartments and answer your move-to-Nairobi questions in a couple of minutes, any time of day.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.