Guides · Money

Sending Money To and From Kenya: The 2026 Guide for Americans

Sending Money To and From Kenya: The 2026 Guide for Americans

You’ll move money across this border more often than you expect. Funding your first months, paying a deposit, topping up your phone wallet, sending support to family, wiring for a home. Each time, the channel you pick decides how much actually arrives.

This guide is for Americans moving to or already living in Nairobi who want the cheapest, safest way to send money between the US and Kenya in 2026. We’ll compare the real options, show where the hidden costs hide, and tell you which tool fits which job. No affiliate spin - just what works.

The quick version (TL;DR)

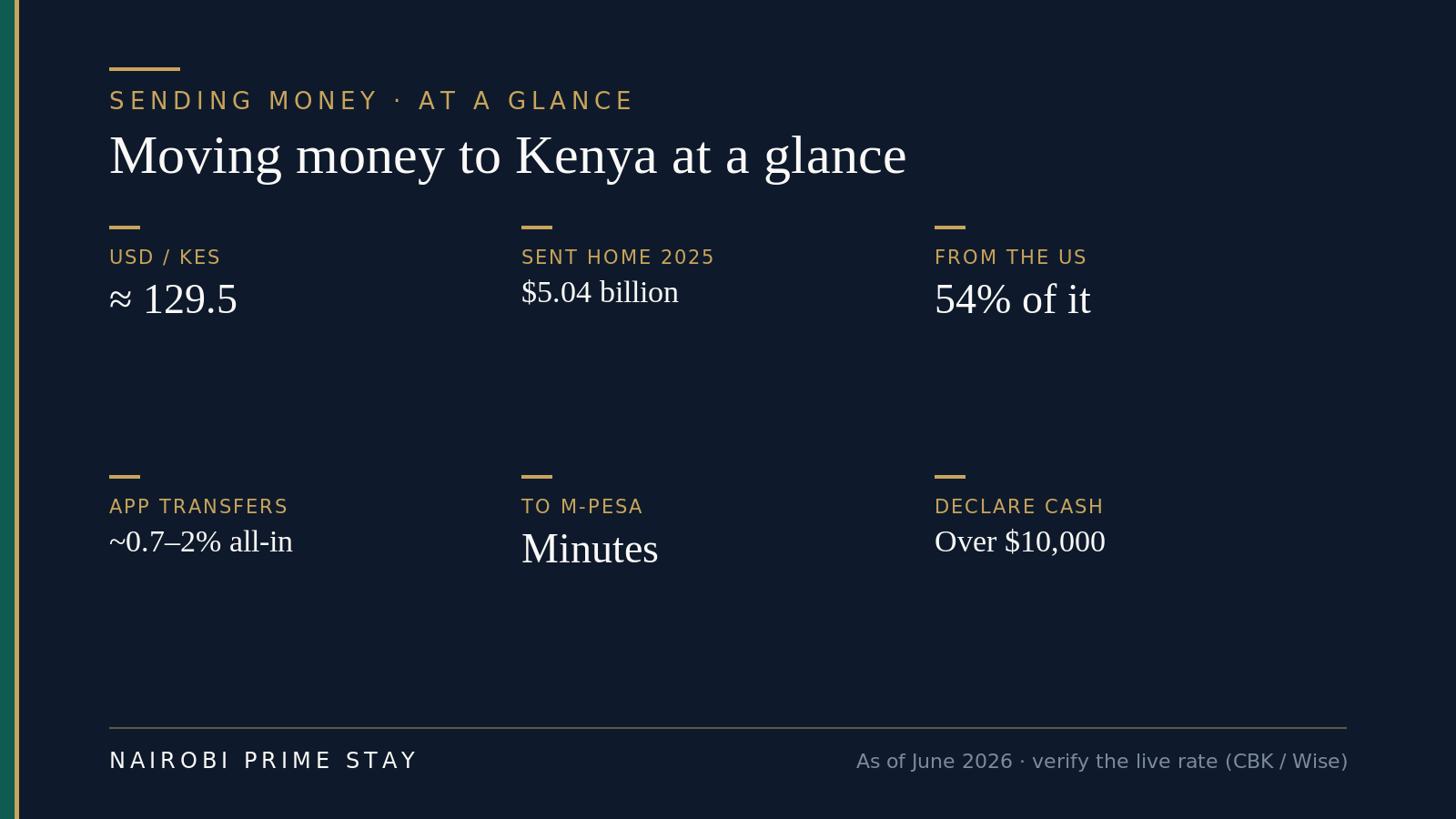

For most everyday transfers from the US to Kenya, a specialist app - Wise, Remitly, Sendwave or WorldRemit - beats a bank on both the fee and the exchange rate, and delivers to M-Pesa or a Kenyan bank account in minutes. Expect to pay roughly 0.7 to 2 percent all-in once you count the rate margin; on $1,000 that’s about $7 to $20. Banks and old-school wires cost more and move slower, but a bank-to-bank SWIFT wire is still the right tool for very large sums like a property purchase, where a clean paper trail matters more than saving a few dollars. As of 2 July 2026 the rate is about 129.4 shillings to the dollar. And note one new rule: since January 2026 the US charges a 1 percent excise tax on transfers funded with physical cash or money orders - fund your transfer from a bank account or card and it does not apply. Don’t carry cash to move money - anything over US$10,000 must be declared at customs.

The numbers that shape how you should move money, mid-2026. Always check the live rate before you send.

The numbers that shape how you should move money, mid-2026. Always check the live rate before you send.

The one idea that saves you the most: the real cost has two parts

Before any provider, understand this. The cost of a transfer is not just the fee they show you. It’s two things added together:

- The upfront fee - the visible charge, like $3.99.

- The exchange-rate margin - the gap between the mid-market rate (the real one you see on Google or Reuters) and the slightly worse rate they actually give you. This markup is invisible, and it’s often bigger than the fee.

The mid-market rate is the midpoint between what buyers and sellers pay for a currency at any moment - the fairest possible rate, with no markup. Wise and a few others use it and charge a clear fee. Most banks and cash services don’t; they quote you a weaker rate and bury their profit inside it. That’s how a transfer can say “no fees” and still cost you 4 percent.

So the only number that matters is how many shillings actually land for a given dollar amount. Get a live quote from two or three providers, compare the shillings received, and you’ll see the true cost instantly. A “free” transfer that gives you 124 shillings to the dollar is far worse than a $5 transfer at 129.

This single habit - compare the landed shillings, not the fee - will save you more than any provider loyalty ever will.

The main ways to send money to Kenya

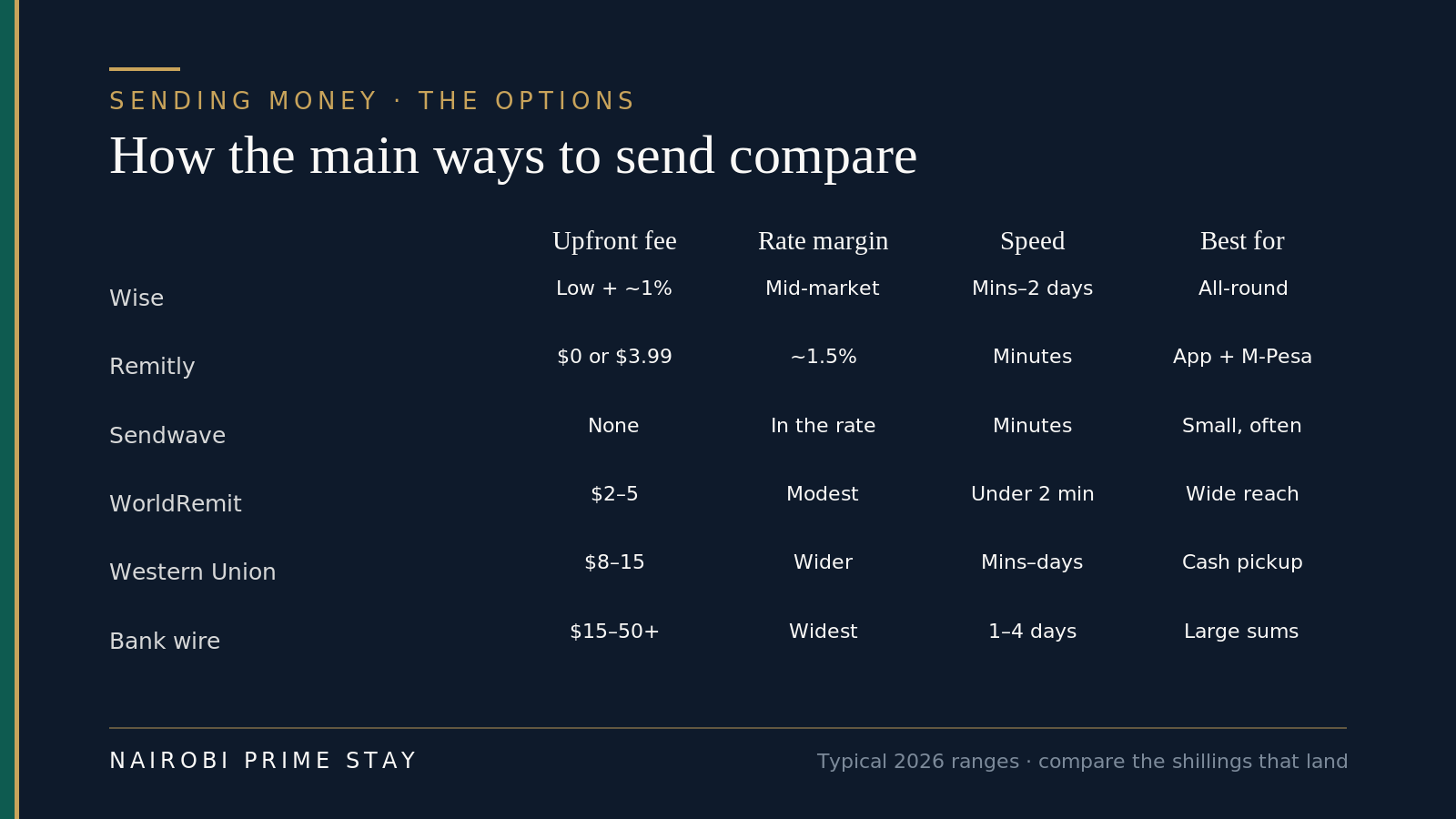

There are six channels worth knowing. Here’s how they stack up, then the detail on each.

Typical 2026 ranges. Exact costs change with the amount and how you pay - always pull a live quote.

Typical 2026 ranges. Exact costs change with the amount and how you pay - always pull a live quote.

| Channel | Typical upfront fee | Rate margin | Speed | Best for |

|---|---|---|---|---|

| Wise | Small fixed + ~1% | Mid-market (none) | Minutes–2 days | All-round value; holding USD/KES |

| Remitly | $0 (Economy) / from $3.99 (Express) | ~1.5% on Economy | Minutes | App users sending to M-Pesa |

| Sendwave | None | Built into the rate | Minutes | Frequent smaller sends |

| WorldRemit | ~$2–5 | Modest | Under 2 min to M-Pesa | Wide reach, mobile money |

| Western Union / MoneyGram | ~$8–15 | Wider | Minutes–days | Cash pickup in towns |

| Bank SWIFT wire | $15–50+ each side | Widest | 1–4 business days | Large sums, property |

Wise - the all-rounder

Wise (formerly TransferWise) is the default for most expats, and for good reason. It uses the mid-market rate and charges one clear fee - usually a small fixed amount plus roughly 1 percent, dropping a little on bigger transfers. Sending $30,000 from a Wise balance, for example, costs around $297, just under 1 percent. It pays out to M-Pesa or a Kenyan bank account, and transfers land anywhere from instantly to about two working days.

Its other trick is the multi-currency account. You can hold US dollars and Kenyan shillings side by side and convert when the rate looks good, rather than being forced to convert the moment you send. For anyone living between two currencies, that’s genuinely useful. The one limit: sending out of Kenya is more restricted than sending in.

Remitly - strong app, good for M-Pesa

Remitly gives you two speeds. Its Economy option is fee-free and a bit slower, with the cost sitting in an exchange margin of around 1.5 percent. Express delivery costs from about $3.99 and arrives within minutes. New customers usually get an unusually good rate on their first transfer, which is worth using once. It pays straight to M-Pesa or a bank, the app is easy, and it’s a solid pick for regular sends home.

Sendwave - no fees, built for frequent small sends

Sendwave is app-only and charges no upfront fee; its cost is baked into the exchange rate. Money reaches M-Pesa in minutes. Because there’s no flat fee, it shines for people sending smaller amounts often - say, weekly support to family - where a fixed fee would sting. It’s now part of WorldRemit but still runs as its own app.

WorldRemit - wide reach, fast to mobile money

WorldRemit charges a small fixed fee (about $2 to $5) plus a modest rate margin. Its strength is reach and speed to mobile wallets - transfers to M-Pesa often arrive in under two minutes. It also offers bank deposit and cash pickup, so it’s a flexible middle option between the cheap apps and the cash giants.

Western Union and MoneyGram - when someone needs cash

The old guard are usually the priciest on the rate, with fees around $8 to $15 and a wider margin. But they have the one thing the apps don’t: a vast physical network. If your recipient is upcountry without M-Pesa or a bank, and needs to collect cash in person at a local agent, this is the reliable choice. They also pay to M-Pesa now, but you’re paying for the cash-pickup network whether you use it or not.

Bank SWIFT wire - for the big, serious transfers

A traditional bank-to-bank wire is the most expensive and slowest way to send everyday money: flat fees of $15 to $50 or more on each end, often invisible correspondent-bank charges in the middle, a wider exchange spread, and one to four business days. For a $500 transfer it’s a bad deal. For a $250,000 property payment, it’s exactly right - more on that below.

How the money arrives: M-Pesa vs a bank account

Where your money lands matters as much as how you send it. You have two main destinations in Kenya.

M-Pesa is the fast, everyday choice. Most apps pay straight into your M-Pesa wallet, where it arrives in minutes and is instantly spendable - rent, shops, taxis, bills, all of it runs on M-Pesa. The catch is limits. Within Kenya you can hold up to about KES 500,000 and move up to about KES 250,000 per transaction. International transfers into M-Pesa are frequently capped lower per transfer, often somewhere between KES 150,000 and 300,000. That’s fine for a few hundred or a couple of thousand dollars; it’s not how you receive a house deposit. (Limits move - confirm with Safaricom and your provider.) If you’re new to all this, our M-Pesa guide for newcomers explains how to set it up with your passport.

A bank account is the choice for anything large or recurring: a salary, rent you collect as a landlord, or money you’ll convert in bulk. A Kenyan account also lets you receive and hold US dollars if you open a foreign-currency account, so you can sit on dollars and convert when the rate suits. The cost is that you need to open one first, which takes a permit and a KRA PIN - see opening a bank account in Kenya as a foreigner and our overview of banking in Nairobi.

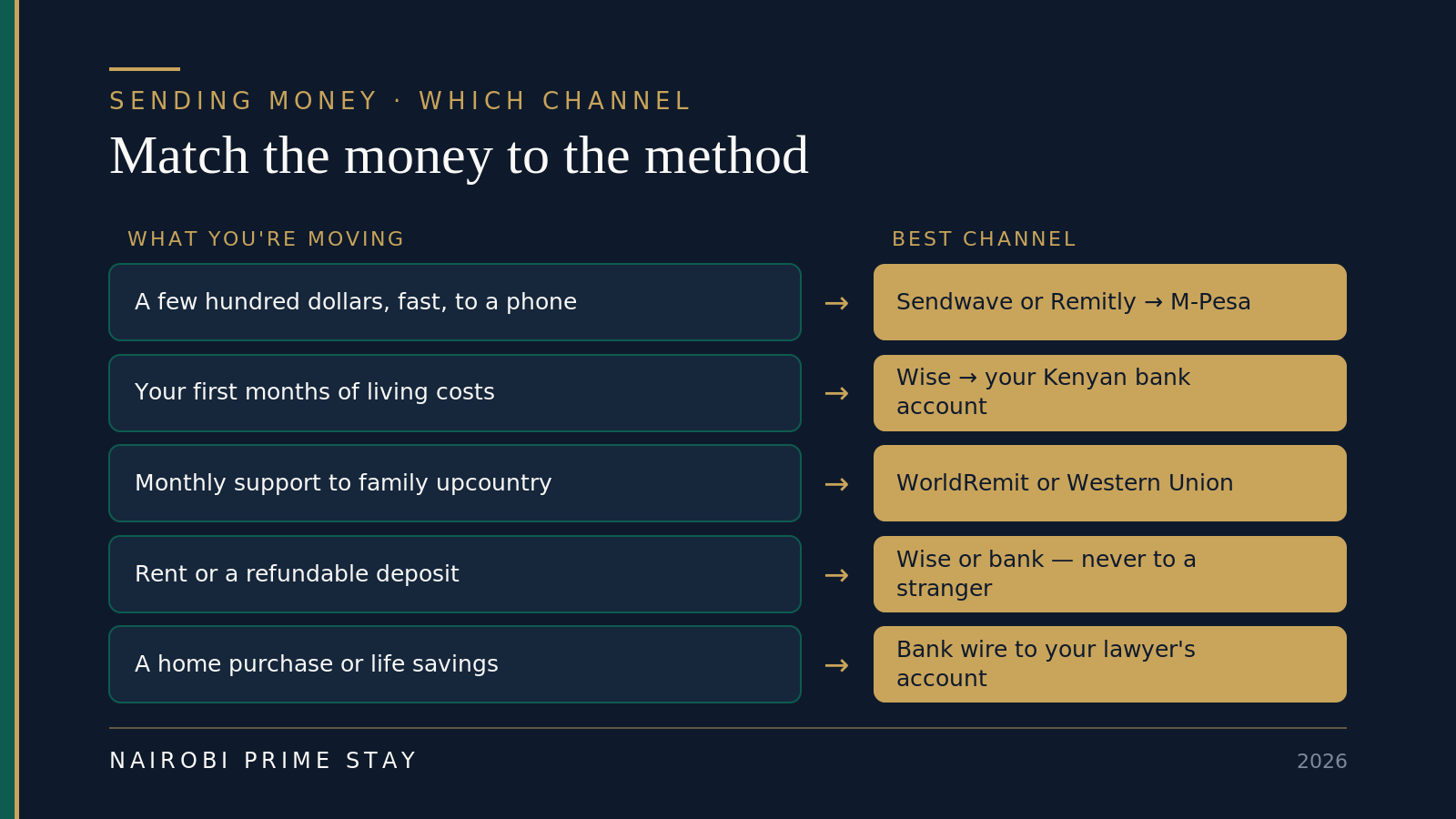

Most people end up using both: M-Pesa for daily life, a bank account for the big stuff. Here’s a rough guide to matching the money to the method.

Match the channel to the job. Speed for small and frequent; traceability for large.

Match the channel to the job. Speed for small and frequent; traceability for large.

Sending money out of Kenya, back to the US

This direction is harder and usually pricier, so plan for it. Kenya allows residents to move money abroad, but banks apply more scrutiny and a wider margin going out. Your main routes:

- An outward SWIFT wire from your Kenyan bank. The standard method for larger sums. You’ll need to show the source of the funds, especially for anything sizable, so keep records of how the money got into your account in the first place.

- M-Pesa Global. Safaricom’s service lets you send from your M-Pesa wallet to bank accounts and wallets abroad, and to partners like Western Union and PayPal. Handy for smaller amounts once you live there.

- Wise, where supported. Funding a transfer from a Kenyan account or card can work for some routes, though it’s more limited than the inbound direction.

The practical takeaway: set up your “way out” when you open your account, not when you suddenly need it. If you’ll repatriate income regularly - a remote salary, rental income, a pension - ask your bank exactly how outward transfers work, what they cost, and what documentation they want.

Send a transfer the smart way

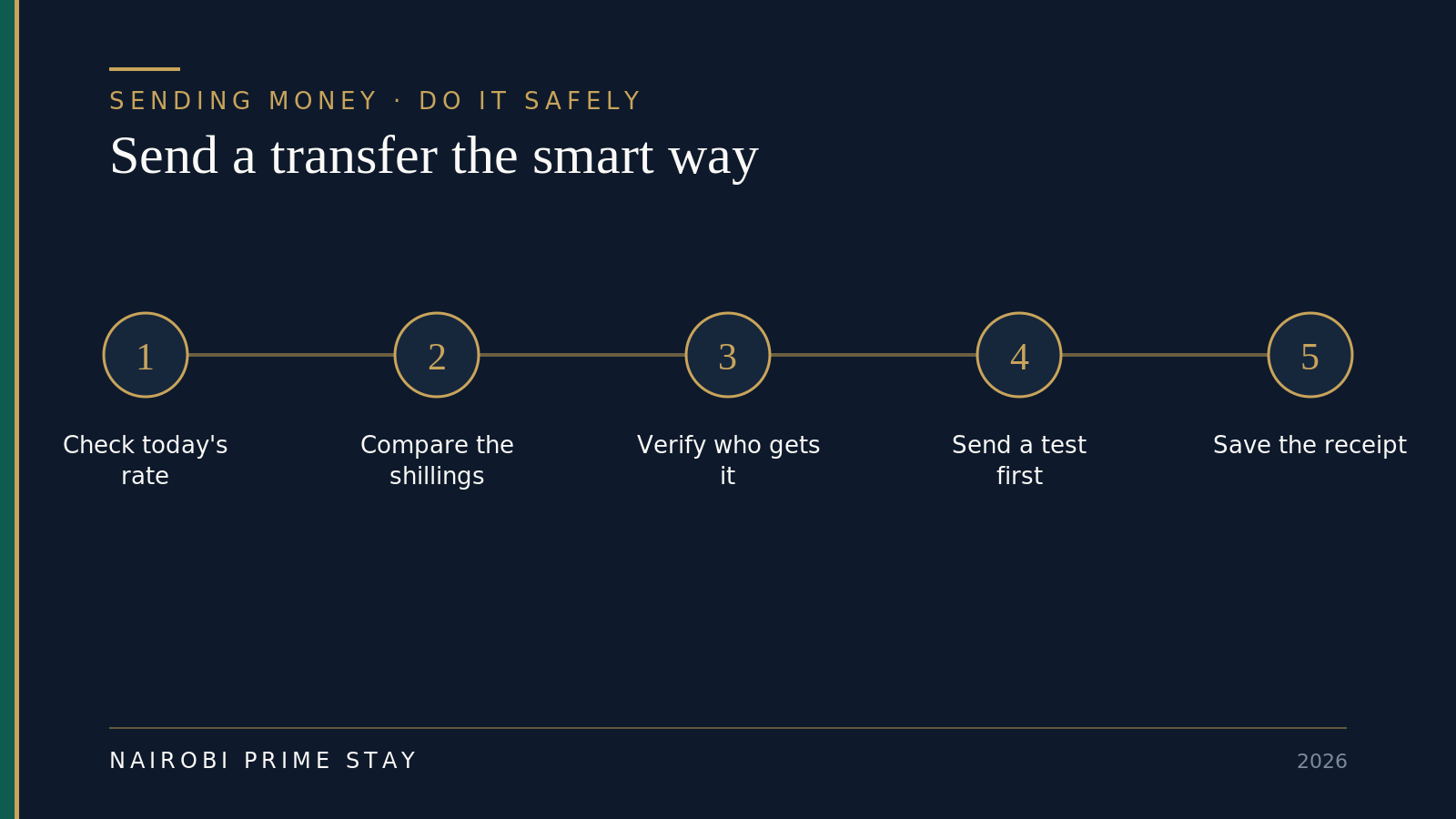

The mechanics are simple once you’ve done one. The discipline is in the habits around it.

Five habits that protect your money on every transfer, big or small.

Five habits that protect your money on every transfer, big or small.

- Check today’s rate. Glance at the mid-market USD/KES rate so you have a yardstick. Our USD/KES currency guide tracks it and explains the swings.

- Compare the shillings. Pull a live quote from two or three providers and compare what actually lands, not the advertised fee.

- Verify who gets it. Triple-check the M-Pesa number or account details. Transfers are hard to reverse once sent.

- Send a test first. For a new recipient or a big move, send a small amount first and confirm it arrived before sending the rest.

- Save the receipt. Keep every confirmation. You’ll want the paper trail for taxes, for source-of-funds questions, and for peace of mind.

Big transfers: buying property or moving your life savings

When the number gets large - a home deposit, a full purchase, your savings - the rules change. (For what a rental deposit itself should look like, see tenancy, leases and deposits in Kenya.) Three things matter more than which app is trendy.

Use a bank wire, into the right account. Send a property payment by bank-to-bank SWIFT wire, straight into your own Kenyan account or directly to your conveyancing lawyer’s client account. Never carry cash for this, and never use a consumer remittance app. The wire creates the clean record that a property transaction, and the law, expect. If you’re buying, read how diaspora investors buy property in Kenya and your financing options first.

Negotiate the rate - the spread dwarfs the fee. On a $300,000 transfer, a $40 wire fee is a rounding error. A 1 percent exchange-rate margin is $3,000. So on big sums, the rate is the whole game. Ask your bank’s treasury or forex desk for a negotiated rate rather than the screen rate, and compare it against a large-transfer specialist like Wise or OFX. Again, judge by the shillings that land.

Keep a clean source-of-funds trail. Banks on both sides run anti-money-laundering checks and will ask where large sums came from. As a US person you’ll sign FATCA and W-9 forms with a Kenyan bank, and holding over US$10,000 across foreign accounts means filing a US FBAR report. None of this is a problem if you keep records - statements, sale documents, transfer confirmations. It becomes a headache only if you can’t show the paper trail later, including when you want to move money back out.

And the cash rule, because it catches people: any currency or monetary instruments over US$10,000 (or the equivalent) must be declared at Kenyan customs, both arriving and leaving. Failing to declare can mean seizure and penalties. Carrying cash is the worst way to move relocation money anyway - it’s the slowest to use, the easiest to lose, and the hardest to prove. Wire it.

A quick word on crypto

Some people move money via stablecoins or crypto, and Kenya has caught up with rules. The Virtual Asset Service Providers Act became law in 2025, and licensed exchanges are arriving through 2026. Crypto gains are now taxable - around 10 percent for individuals - plus a 10 percent excise duty on the fees crypto platforms charge. So it’s no longer a grey area.

But for ordinary relocation money, it’s still the wrong tool. Prices are volatile, the spreads on cashing in and out can quietly erase any saving, and you carry counterparty risk if you trade peer-to-peer. Unless you already live in crypto and know exactly what you’re doing, stick to regulated transfer apps and banks.

Does the new US remittance tax affect you?

Probably not, but you should know it exists. On 1 January 2026 a new US federal excise tax on remittance transfers took effect: 1 percent of the amount sent abroad, collected automatically by the transfer provider at checkout and passed to the IRS.

Here’s the part that matters: the tax only applies when you fund the transfer with physical cash, a money order or a cashier’s check. Transfers funded from a US bank account, a debit or credit card, or a digital wallet are exempt. In other words, almost every transfer described in this guide - Wise from your checking account, Remitly on a debit card, Sendwave from your bank - carries no remittance tax at all.

The one habit to change: don’t walk cash into a Western Union or MoneyGram counter if you can avoid it. Sending $1,000 in cash now costs an extra $10 in tax on top of the usual worse pricing of cash transfers. Fund electronically and the tax never touches you. As with all tax rules, the fine print can shift - as of July 2026 this is how it works, and your provider will show any tax as a line item before you confirm.

The diaspora context - why the rates are good

Here’s the encouraging part. Sending money to Kenya is a mature, fiercely competitive business, and that competition works in your favor. Kenyans abroad sent home a record US$5.04 billion in 2025 - about KES 650 billion - and the Central Bank expects even more in 2026. The United States alone accounts for 54 percent of that flow. Money from the diaspora is now one of Kenya’s largest sources of foreign exchange, bigger than tea or tourism.

What that means for you: the rails are reliable, regulated, and cheap by global standards. Providers fight hard for this corridor, so a little comparison shopping reliably finds you a good rate. You’re not a pioneer here - millions of people move money along this exact route every month.

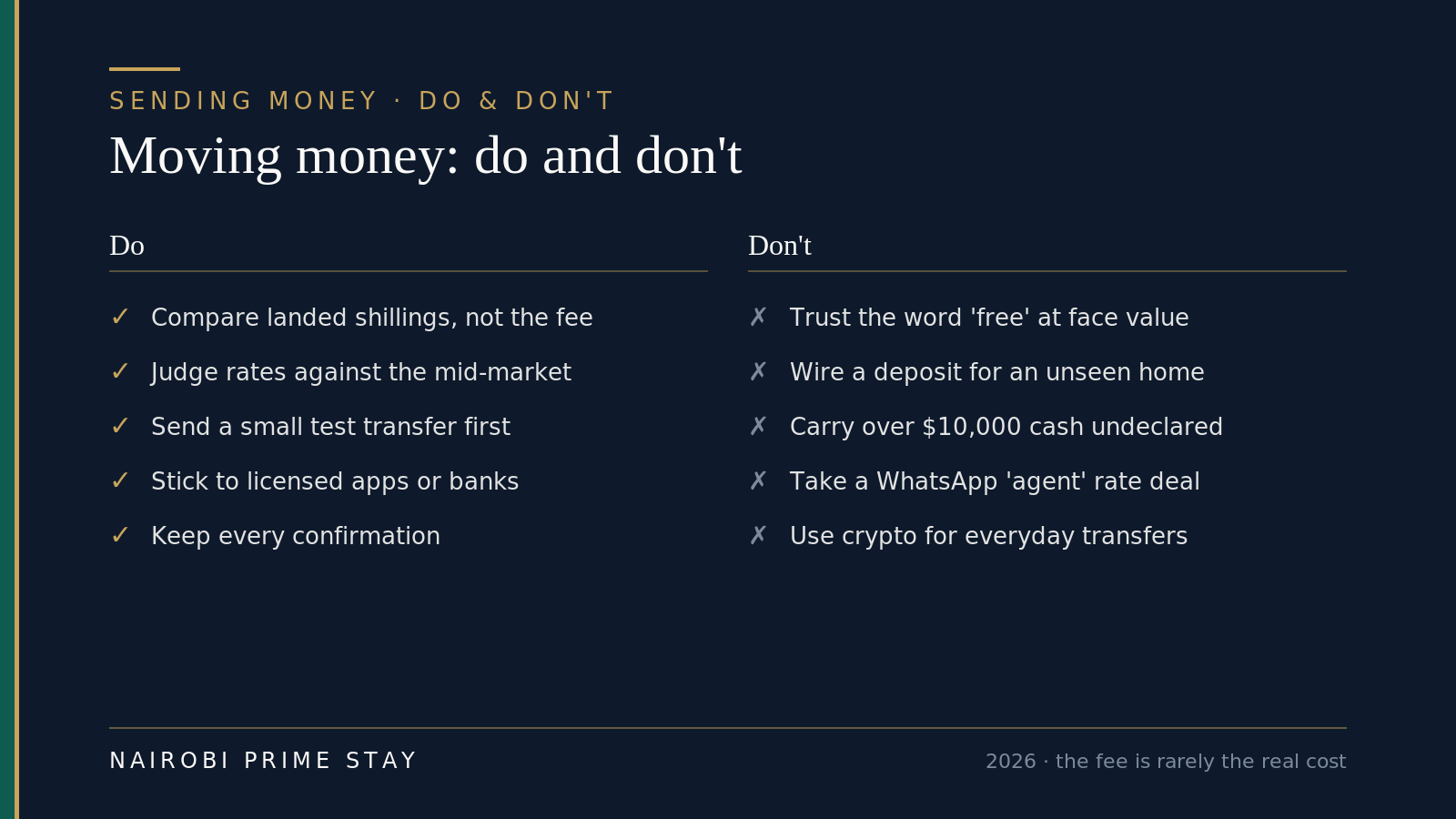

Do this, not that

The fee is rarely the real cost. These habits protect both your money and your safety.

The fee is rarely the real cost. These habits protect both your money and your safety.

One safety note worth its own line: never wire a deposit for an apartment or house you haven’t verified. Fake-listing scams target newcomers who pay before they’ve seen a place or confirmed the landlord - our guide to renting an apartment in Nairobi walks through the safe sequence. Pay only after viewing and verifying, use traceable channels, and be wary of anyone pushing a too-good “agent” exchange rate over WhatsApp. A serviced apartment for your first weeks gives you a safe base to view homes in person before any money moves.

How this plays out: three real examples

The remote worker. Maya moved to Kilimani and gets paid in dollars to her US bank. Each month she sends about $1,800 to cover rent and life. She uses Wise, paying into her Kenyan bank account, and converts a bit extra to shillings when the rate dips. All-in she loses around 1 percent - roughly $18 - and the money is usable the same day. For the cash she needs on her phone, she moves a slice to M-Pesa instantly from the bank app. See what a month actually costs in our cost of living in Nairobi guide.

The family sending support. James, in Texas, sends $250 to his mother near Nakuru every couple of weeks. She doesn’t use a bank, so he uses Sendwave straight to her M-Pesa - no fee, money in minutes, and she withdraws cash at the local agent. Because there’s no flat fee, sending small and often doesn’t punish him. When she once needed to collect cash in a town without an M-Pesa float, Western Union’s pickup network covered it.

The home buyer. The Olamis are buying a $240,000 townhouse in Lavington. They don’t touch an app. Their lawyer gives wiring instructions for the client account, and they send a bank-to-bank SWIFT wire after negotiating a rate with their bank’s forex desk - shaving about $2,400 versus the screen rate. They keep every document: the sale agreement, the wire confirmation, proof of where the funds came from. It’s slower and it’s deliberate, and that’s the point.

The honest balance

No single channel wins everything. Here’s the real trade-off.

Where the apps win: they’re cheap, fast, and easy, with the mid-market or near-mid-market rate and delivery to M-Pesa in minutes. For anything from $50 to a few thousand dollars, they beat a bank every time. Wise’s multi-currency account adds genuine flexibility for people living between dollars and shillings.

Where the apps fall short: per-transfer and wallet limits cap how much you can move at once, sending out of Kenya is more limited, and for a property-scale transfer you want a bank’s formal record, not an app receipt.

Where banks win: large, traceable transfers; receiving a salary; holding dollars; the documentation that big transactions and the law require. A negotiated forex rate on a large wire can be competitive.

Where banks fall short: everyday transfers, where their fees and wider spreads make them the expensive, slow option.

The smart setup isn’t loyalty to one - it’s using the cheap apps for daily money and a bank for the big, serious moves.

Your money-transfer checklist

Work through this and you’ll rarely overpay or get caught out.

- Open the destinations first. Get an M-Pesa line on arrival and a bank account once you have a permit and KRA PIN.

- Know today’s mid-market rate before you send (about 129.4 as of 2 July 2026 - verify live).

- Compare landed shillings across two or three providers, not the headline fee.

- Pick the channel for the job: app to M-Pesa for small and fast; Wise to your bank for living costs; bank wire for property.

- Send a small test to any new recipient or before a large transfer.

- Verify the recipient details - numbers and account names - twice.

- Never prepay for unseen housing; pay only after viewing and verifying.

- Keep every confirmation for tax and source-of-funds records.

- Declare cash over US$10,000 at customs, both directions.

- Get cross-border tax advice early if you’ll hold money or earn in both countries - start with taxes for expats in Kenya.

Frequently asked questions

What’s the cheapest way to send money to Kenya?

For most transfers from the US, a specialist app beats a bank. Wise gives you the real mid-market rate plus a small fee, usually around 0.7 to 1.2 percent all-in. Sendwave and Remitly’s Economy option advertise no fee and build their cost into the exchange rate instead, which can be just as cheap for smaller amounts. The trick is to ignore the word ‘free’ and compare the number of shillings that actually land. As of 2 July 2026 the rate is about 129.4 shillings to the dollar, so verify the live figure before you send.

Does the new US remittance tax apply to money I send to Kenya?

Usually not. Since 1 January 2026 the US charges a 1 percent federal excise tax on international transfers, but only when you fund them with physical cash, a money order or a cashier’s check. Transfers funded from a US bank account, a debit or credit card, or a digital wallet are exempt. So if you use Wise, Remitly, Sendwave or WorldRemit and pay electronically, as almost everyone in this guide would, you pay nothing extra. Walk cash into an agent location, though, and the provider adds the 1 percent at checkout.

Is it better to receive money in Kenya through M-Pesa or a bank account?

It depends on the size. For everyday amounts up to a few hundred dollars, having it land straight in M-Pesa is fastest - it arrives in minutes and you can spend it immediately. For a salary, rent you are paying a landlord, or anything large, a bank account is better, because M-Pesa caps how much you can hold and move in one go. Many newcomers use both: M-Pesa for daily life and a bank account for big sums.

Is Wise available in Kenya?

Yes. Wise sends money into Kenya to both M-Pesa and bank accounts, using the mid-market rate with a clear upfront fee. You can also hold US dollars and Kenyan shillings in a Wise multi-currency account and convert when the rate suits you. Sending out of Kenya is more limited, so most people use Wise for the US-to-Kenya direction and a bank for the way back.

How long does a money transfer to Kenya take?

To M-Pesa, usually minutes - WorldRemit and Sendwave often land in under two minutes, and Remitly Express within minutes. A Wise transfer can be near-instant or take up to about two working days, depending on how you pay and on verification checks. A bank SWIFT wire is the slowest, typically one to four business days. Your very first transfer with any provider can take longer while they verify your identity.

How much money can I send to M-Pesa from abroad?

M-Pesa has limits. Within Kenya you can hold up to about KES 500,000 and move up to about KES 250,000 in a single transaction. International transfers into M-Pesa are often capped lower per transfer - commonly somewhere between KES 150,000 and 300,000 - so anything bigger should go to a bank account instead. Limits change, so confirm the current figures with Safaricom and your transfer provider before a large send.

Can I use PayPal, Venmo or Zelle to send money to Kenya?

Mostly no, and where you can, it’s rarely the cheap option. Zelle and Venmo only work between US accounts, so they can’t deliver shillings to Kenya. PayPal does operate in Kenya and links to M-Pesa through a Safaricom withdrawal service, but the combined fees and exchange margin are usually worse than Wise, Sendwave or Remitly. Treat PayPal as a fallback for people who already hold a balance there, not as your main rail.

How do I send a large amount, like a deposit for a house?

Use a bank-to-bank SWIFT wire, ideally straight into your own Kenyan bank account or your conveyancing lawyer’s client account - never cash and never an everyday remittance app. On large sums the exchange-rate margin matters far more than the fee: one percent on $300,000 is $3,000, so ask your bank’s treasury desk for a negotiated rate and compare it against a large-transfer specialist. Keep clear source-of-funds records, and remember any cash over US$10,000 must be declared at Kenyan customs.

Do I pay tax on money I send to myself in Kenya?

Moving your own money to yourself is not taxable income - it is just a transfer. The only new wrinkle is the 2026 US remittance excise tax, and that applies only to transfers funded with physical cash, a money order or a cashier’s check; fund from a bank account or card and it doesn’t touch you. Separately, US citizens owe US tax on worldwide income wherever they live, and holding more than US$10,000 across foreign accounts triggers a US FBAR report. Kenya can also tax you once you have been resident long enough. Set this up with a cross-border tax professional early.

How do I avoid scams when sending money to Kenya?

Stick to licensed transfer apps and banks, verify the recipient’s exact M-Pesa number or account name before sending, and send a small test transfer to any new recipient. Never wire a deposit for an apartment or house you haven’t seen and verified - fake-listing scams specifically target newcomers who pay from abroad - and ignore anyone offering a special exchange rate over WhatsApp. Keep every confirmation so you have a paper trail if something goes wrong.

Can I send money from Kenya back to the US?

Yes, but it is harder and usually pricier than the other direction. The main routes are an outward SWIFT wire from your Kenyan bank (you will need to show where the money came from), M-Pesa Global, or a service like Wise where it is supported. Banks apply their own exchange margin and may ask what the money is for. If you expect to move money out regularly, set this up with your bank when you open the account.

What is the US dollar to Kenyan shilling exchange rate in 2026?

As of 2 July 2026, one US dollar buys about 129.4 Kenyan shillings, and the rate has been fairly stable through the first half of the year. Rates move, though, so check the Central Bank of Kenya, Wise or your provider’s live quote before you send or budget. On any transfer, judge providers by the shillings that actually land, not the advertised rate.

Final thoughts

Moving money between the US and Kenya is easier and cheaper than most newcomers fear. The whole game comes down to one habit: compare the shillings that actually land, ignore the word “free,” and match the channel to the job. Cheap apps for daily money, a bank for the big moves, M-Pesa for life on the ground. Do that and you’ll keep far more of your money than the average mover - month after month.

Set up your destinations early, keep your receipts, and get tax advice before the numbers get large. The rails are mature and the competition is on your side.

Related reading

- Moving to Nairobi: the complete guide - the hub for your whole relocation.

- Banking in Nairobi for expats - choosing a bank and what it’s for.

- Opening a bank account in Kenya as a foreigner - the documents and the two routes.

- M-Pesa explained for newcomers - the wallet that runs daily life.

- The USD/KES exchange rate guide - the rate, where to change money, and the swings.

- Cost of living in Nairobi - what your money actually buys.

- Diaspora property investment in Kenya - if you’re sending money to buy.

- Taxes for expats in Kenya - residency, KRA PIN, and what you owe.

Get set up the easy way

Your money is easiest to manage once you have a secure base. A serviced apartment for your first weeks is all-inclusive - Wi-Fi, cleaning, generator, security - so you can open your bank account, set up M-Pesa, and view homes in person before any large money moves. A $50 deposit reserves your place; the balance is paid on arrival.

Not sure which area or budget fits? Our AI relocation assistant can shortlist apartments and answer your move-in questions in a couple of minutes, day or night.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.