Guides · Property investment

Diaspora Property Investment in Kenya: The Honest 2026 Guide to Buying From Abroad

Diaspora Property Investment in Kenya: The Honest 2026 Guide to Buying From Abroad

Buying property in Kenya while you live in Maryland, Manchester or Doha is completely normal. Tens of thousands of people in the diaspora do it every year, and a good number do it well. The hard part isn’t the law or the money. It’s that you can’t stand on the plot, look the seller in the eye, or walk into the lands office yourself. Distance is where deals go wrong.

This guide is for two kinds of reader. The first is a Kenyan living abroad who wants to buy a home or an investment back home — to retire to, to rent out, or to anchor a future return. The second is anyone else overseas, including African Americans exploring a move “home,” who wants a stake in Kenya’s market. The rules differ for each, and we’ll be clear about who can own what.

We’ll walk through the safe way to buy from a distance: your own advocate, an escrow account, a narrow power of attorney, and independent eyes on the ground. We’ll cover diaspora mortgages and what they really cost, how to move money without losing a slice to fees or fraud, and the lower-hassle alternatives if you’d rather not deal with tenants and title at all. We’ll be honest about the scams, because the diaspora is targeted more than anyone.

Quick answer (TL;DR)

Yes — you can buy property in Kenya from abroad, and many people complete the whole thing without flying in. The safeguards matter more when you’re remote, not less. Use your own independent advocate (not the seller’s, not the agent’s), run an official title search on Ardhisasa before any money moves, hold deposits in an escrow/stakeholder account rather than sending cash to an individual, and grant a narrow, written power of attorney so someone you trust can sign for you. Get independent eyes on the property — a licensed surveyor plus a person with no stake in the sale. Kenyan citizens (including dual citizens) can own freehold and agricultural land; non-citizens are capped at 99-year leasehold and can’t own farmland. If you’d rather skip the landlording entirely, a REIT bought through the regulated Vuka app gives you property exposure from about KES 2,500. The single biggest cause of diaspora loss isn’t a clever scam — it’s an informal “just send the money to my cousin” arrangement with no paperwork. Treat every purchase as a transaction, not a favor.

Why this matters

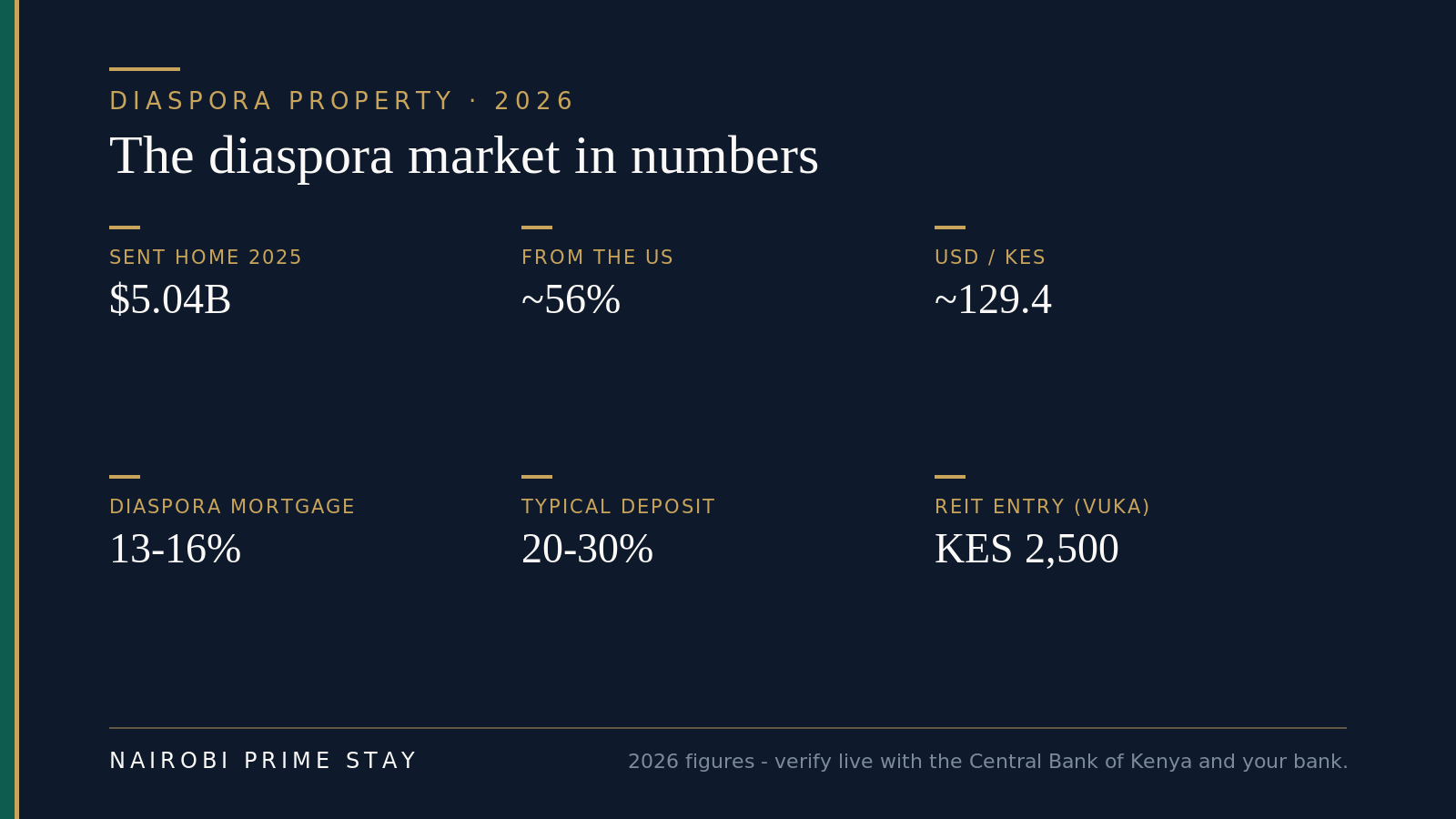

The diaspora is now one of the biggest forces in Kenya’s economy. Kenyans abroad sent home about $5.04 billion in 2025 — roughly KES 650 billion — according to Central Bank of Kenya data, more than the country earns from tea or tourism. That was a record — the first time flows topped $5 billion, up from about $4.95 billion in 2024. The United States alone is the largest single source, sending roughly 56% of that money. A large share of that money goes into land and houses.

That’s the good news. The hard news is that property is also where diaspora money disappears. Land fraud is common, “agents” vanish with deposits, and relatives sometimes build a smaller house than the money paid for — or a different one, on a different plot. None of this means you shouldn’t invest. It means you should invest like a professional: slowly, with paperwork, and with people whose job is to protect you rather than to close a sale.

The diaspora property market in numbers — 2026. Verify live figures with the Central Bank of Kenya and your bank.

The diaspora property market in numbers — 2026. Verify live figures with the Central Bank of Kenya and your bank.

Get it right and Kenyan property can be a real anchor: a home for visits or retirement, rental income in a currency that has steadied, and a foothold for an eventual return. Get it wrong from 8,000 miles away and it’s slow and expensive to unwind. This guide is built to keep you in the first group.

First: are you a citizen or a foreigner? It changes everything

Before anything else, work out which set of rules applies to you, because Kenyan law treats citizens and non-citizens very differently.

If you’re a Kenyan citizen living abroad — including a dual citizen, which Kenya has allowed since 2010 — you have the same property rights as any resident Kenyan. You can own land freehold (forever), you can buy agricultural land, and there’s no cap on the kind of title you hold. Being in the diaspora doesn’t shrink your rights; it just makes the logistics harder.

If you’re a non-citizen — say an American or Brit with no Kenyan passport — the Constitution caps you at 99-year leasehold. You cannot own freehold, and you cannot own agricultural land without a rare exemption. In practice that’s fine for most investors: city apartments sit on leasehold anyway, and a sectional-title flat registered in your own name is the clean, common route. But it rules out that “buy a farm upcountry” plan unless you take Kenyan citizenship or partner carefully. Our guide to whether foreigners can buy property in Kenya digs into the detail, including why the “register it through a Kenyan company” workaround usually doesn’t upgrade your rights.

One trap catches mixed families. If a non-citizen is married to a Kenyan, the foreign spouse does not automatically gain freehold rights through the marriage. Plan ownership deliberately, with an advocate, rather than assuming it sorts itself out.

The core problem: you’re not in the room

Everything that makes diaspora buying risky comes from one fact — you’re not there. You can’t:

- Walk the plot and see whether it’s vacant, occupied, or already has someone’s maize on it.

- Sit across from the seller and check they are who they say they are.

- Hand documents to the lands registry yourself and watch the search happen.

- Notice the small things — a neighbor who says “that land belongs to the church,” a boundary that doesn’t match the map.

So the whole diaspora playbook is about rebuilding presence at a distance: paying professionals to be your eyes, hands and signature, and structuring the money so no single person can run off with it. Done properly, it’s slower and costs a little more in fees. That cost is the cheapest insurance you’ll ever buy.

The remote-buying playbook

These are the safeguards that make buying from abroad safe. Skip one and you’ve opened a door. Use all of them and most diaspora horror stories simply can’t happen to you.

The remote-buying sequence. Each step protects the one after it.

The remote-buying sequence. Each step protects the one after it.

1. Hire your own independent advocate

This is the single most important decision you’ll make. An advocate (a licensed Kenyan lawyer) runs the legal side: searches, the sale agreement, consents, stamp duty and registration. The rule is simple — use your own, instructed only by you. Not the seller’s lawyer. Not the agent’s “guy who handles everything.” Not the developer’s in-house counsel. Their job is to protect their client; you need someone whose only client is you.

Find one through a firm you can verify with the Law Society of Kenya, or a referral you trust from someone who actually completed a purchase. Before you send a cent, confirm the firm’s bank details by calling a number you found independently — payment-redirection fraud, where a scammer emails you “updated” account details mid-deal, is real and ruthless. Our conveyancing guide explains exactly what your advocate should do at each stage.

2. Run an official title search — before any money moves

Never pay anything against a title you haven’t searched. An official search at the lands registry confirms who really owns the property, the tenure (freehold or leasehold), the size, and whether there are charges, caveats or court disputes attached. In Nairobi and a growing list of counties this runs through Ardhisasa (ardhisasa.lands.go.ke), the government’s online lands platform; elsewhere it’s done through eCitizen or the local lands office. It costs around KES 500 and takes a day or a few.

Your advocate orders it. Insist on seeing the result. A “copy of the title” the seller WhatsApps you proves nothing — fakes are easy. Only the official search, run against the live register, tells the truth. For land especially, read our buying land in Kenya guide before you commit; land carries far more fraud than a titled apartment.

3. Put deposits in escrow — never send cash to an “agent”

When you’re ready, the sale agreement should route your deposit — usually around 10% — into a stakeholder (escrow) account, normally held by an advocate, not paid directly to the seller. The advocate holds it until agreed conditions are met (clean search, consents, completion documents). If the deal collapses on the seller’s side, the money is recoverable.

Here’s the line that saves diaspora buyers the most money: never wire funds to an individual’s personal account or M-Pesa for a property purchase. Not the agent’s. Not a “facilitator’s.” Not even, informally, a relative’s. Money for property goes to a stakeholder account against a signed agreement, full stop. The “send a deposit to hold it” message, followed by silence, is the most common diaspora scam there is.

4. Grant a narrow power of attorney

Because you can’t sign in person, you’ll likely give someone a power of attorney (POA) — written authority to act for you. This is normal and useful. It’s also dangerous if it’s broad, so keep it narrow and specific: limited to this one transaction, this one property, with defined acts (sign the agreement, receive the title), ideally time-bound. Give it to your advocate or a genuinely trusted person — and think hard before handing sweeping powers to anyone, family included.

A POA should be properly drawn, signed, witnessed, and where required registered, so it’s valid in Kenya. Done abroad, it usually needs notarising and sometimes legalising or consularising at a Kenyan mission. Your advocate will tell you the exact form. A POA is a loaded instrument: it lets someone deal with your property as if they were you. Limit its blast radius.

5. Get independent eyes on the property

Pay for people whose interests aren’t tied to the sale to confirm reality on the ground:

- A licensed surveyor (registered with the Institution of Surveyors of Kenya) to confirm the beacons match the map — that the plot is where and what the title says, with no road reserve or riparian strip eating into it.

- A valuer to confirm you’re paying a sane price, not a “diaspora price” inflated because you’re far away.

- A trusted person with no stake in the deal to physically visit and send you photos and video. Crucially, this should not be the seller’s friend or the agent — find your own.

If you can fly in for even a few days around completion, do. If you genuinely can’t, this independent-eyes layer is what replaces your presence. Don’t let the one person arranging the whole deal also be your only source of truth about it.

The “let my family handle it” trap

Family help is normal and often essential — someone has to receive keys, check on a build, deal with the chief. But the informal version of this is the number-one way diaspora money is lost. Not by strangers. By the people closest to home.

It rarely starts as fraud. A brother is sent money to “buy the plot” and buys a smaller one, pocketing the difference. A cousin supervising a build skims each delivery of cement. An uncle registers the land in his own name “for safekeeping” and years later it’s genuinely, legally his. Sometimes it’s theft; often it’s drift, optimism and a slow blurring of whose money built what. From abroad, you can’t see it happening until it’s done.

The fix isn’t to cut out family. It’s to formalise. Even with relatives:

- The title goes in your name (or a structure your advocate sets up), never “temporarily” in theirs.

- Money flows through an advocate’s escrow account, against contracts — not hand to hand.

- A written, narrow power of attorney defines exactly what each person can do.

- Every shilling is documented — receipts, statements, a paper trail you keep.

- For a build, an independent quantity surveyor signs off each stage before funds release, so supervision isn’t a favor but a job with accountability.

Treat it as a transaction and most families respond well — good ones often prefer the clarity. If someone resists every safeguard and insists you “just trust them,” that resistance is your answer.

How to actually move the money

Getting funds to Kenya safely is its own skill. A few principles:

Use traceable, regulated channels. Bank wires and services like Wise move USD or GBP into Kenya cleanly, with a record of every transfer. Many banks offer diaspora accounts you can open and fund from abroad, which then feed the purchase. The golden rule from the escrow section holds: the money lands in a stakeholder/advocate account against a signed agreement, not in someone’s personal wallet.

Document everything. Keep proof of the source of funds and every transfer. It protects you in a dispute, satisfies the bank’s compliance checks, and matters for tax on both ends. If you’re a US person, remember the US taxes worldwide income and has reporting rules (FBAR, FATCA) on foreign accounts — loop in a cross-border tax adviser early. Our property taxes in Kenya guide covers the Kenyan side.

Mind the exchange rate. The shilling trades around KES 129 to the dollar in mid-2026 (about 129.4 on 1 July) after a volatile couple of years. On a large purchase, the rate you convert at can swing the price by thousands of dollars. You don’t need to gamble on timing, but for a big transfer it’s worth watching the rate (our USD–KES currency guide explains the drivers; the Central Bank of Kenya or Wise show the live number) rather than converting blind on a bad day.

Don’t drip cash informally. Sending small amounts repeatedly to a relative “for the project,” with no contract behind each one, is how budgets quietly balloon and accountability disappears. Fund against milestones and paperwork, not phone calls. For the mechanics of remittances and the cheapest, safest rails, see our guide to sending money to Kenya.

Getting your money back out

Most guides tell you how to get money into Kenya. The other half — getting rent and, one day, sale proceeds back out — is where Kenya quietly does well. There are no exchange controls. You can move money in and out freely, in the currency you choose, through your bank. That isn’t true everywhere, and it’s a real point in Kenya’s favor.

Moving money, both directions — 2026. Verify live figures before a large transfer.

Moving money, both directions — 2026. Verify live figures before a large transfer.

A few things worth knowing:

- Collect rent into a Kenyan or diaspora account, then sweep it to your home currency when the rate is reasonable. Don’t let a tenant pay a relative who “sends it on” — that’s the same informal trap as on the way in.

- The shilling drags on your yield. Rent is in shillings (around KES 129.4 to the dollar in mid-2026); if the shilling weakens, the same rent buys fewer dollars. For prime, expat or diplomatic tenants, a dollar-denominated lease is a common, legitimate hedge — see our USD–KES currency guide.

- Declare physical cash over USD 10,000 at the border, both ways. Wire transfers have no such cap; they’re also safer and leave the record you’ll want.

- When you sell, Capital Gains Tax of 15% on the net gain comes off before you take the proceeds home. It’s a final tax, and after it the money moves out without restriction. Our property taxes in Kenya guide has the detail, and sending money to Kenya covers the cheapest, safest rails in both directions.

Paying for it: cash or a diaspora mortgage?

Most Kenyan property is bought in cash — the mortgage market is small. As a diaspora buyer you have two broad routes.

Pay cash (often by saving abroad, or borrowing against an asset there). It’s clean, fast and gives you the strongest negotiating hand. The risk is concentration: a lot of money into one illiquid asset, far away. It also tempts people to skip professional steps to “save money” — don’t. The fees you save are the protection you lose.

Take a diaspora mortgage. Several banks — KCB, Equity, Co-operative Bank, Absa, Stanbic, Standard Chartered, NCBA and National Bank — run dedicated diaspora home-loan products. As of early 2026, expect:

| Feature | What to expect (2026) |

|---|---|

| Interest rate | ~13–16% on standard diaspora mortgages; KMRC-backed loans ~7–9.9%, for owner-occupied homes up to ~KES 10.5M (the income cap was scrapped in 2024) |

| Deposit | Typically 20–30% of the price (plus a ~10% earnest deposit at offer) |

| Proof of income | Offshore payslips/bank statements, usually 6–12 months |

| Also required | A Kenyan bank account, a valid Kenyan ID or passport, and a KRA PIN |

| Approval time | Roughly 4–7 days for an in-principle decision (KCB); the full process runs weeks to months |

Rates and terms change and vary by bank and profile — confirm the live offer directly. Figures verified mid-2026.

A KES mortgage repaid from dollar income carries currency risk: if the shilling weakens, your repayments cost more in your home currency. For a fuller breakdown of every financing route — local mortgage, diaspora mortgage, developer payment plans, and borrowing against a US asset to buy here in cash — see our property financing in Kenya guide.

The tax on renting it out: the non-resident’s 30%

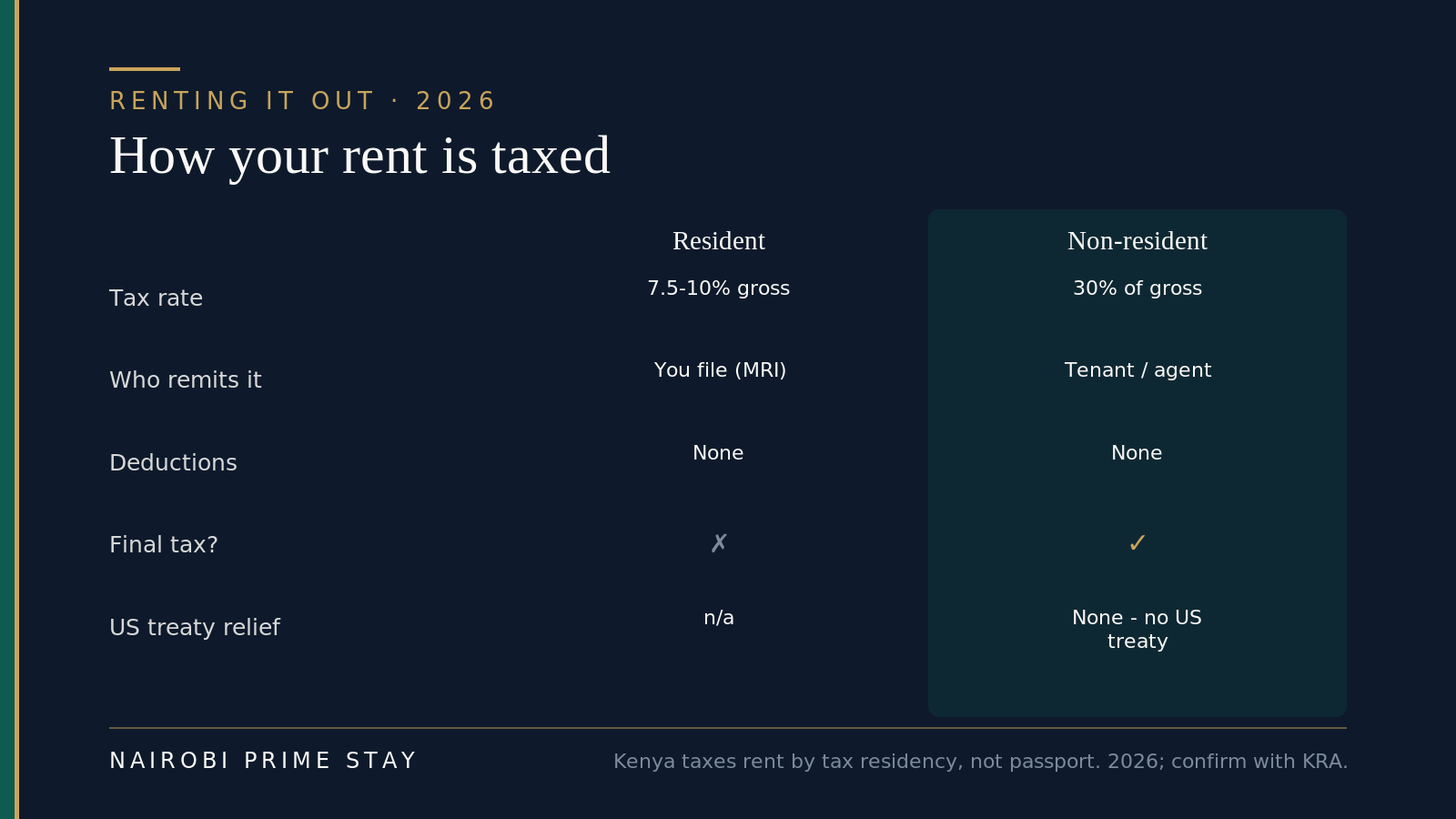

If you buy to rent, learn this before you run any numbers: how your rent is taxed depends on your tax residency, not your passport — and most people living abroad are non-resident for Kenyan tax. It’s the single most misunderstood figure in diaspora investing.

Kenya taxes rent by residency, not citizenship. 2026 — confirm with KRA.

Kenya taxes rent by residency, not citizenship. 2026 — confirm with KRA.

A resident landlord pays Kenya’s Monthly Rental Income (MRI) tax — 7.5% of gross rent, which the Finance Bill 2026 proposes to raise to 10%. A non-resident landlord is taxed at 30% of the gross rent. The tenant or letting agent withholds it at source and remits it to KRA, and it’s a final tax — no deductions, no annual return to soften it. So a Kenyan nurse in Texas letting a flat in Nairobi is, in most cases, taxed at 30%, not 7.5% — a nasty surprise if you budgeted like a resident.

Here’s the twist that matters for the diaspora specifically. Kenya has tax treaties with several countries where Kenyans cluster — the UK, Canada, Germany, France, the UAE, Mauritius and South Africa — and some cap the rate below 30%. There is no such treaty with the United States. So a US-based owner (Kenyan or American) pays the full 30%, then reports the income at home too, claiming a US foreign tax credit (IRS Form 1116) so the same money isn’t taxed twice. A UK-resident Kenyan, by contrast, may claim treaty relief. Same building, different tax, purely because of where you live.

What this means in practice: run your yield on the after-tax number. On a KES 100,000-a-month flat, a non-resident owner loses about KES 360,000 a year to the 30% before a shilling of costs. That doesn’t kill the case for buying — but it turns an optimistic “gross yield” into the real one. Loop in a cross-border tax adviser early, and read our taxes for expats in Kenya guide alongside the property taxes guide for the full picture.

Building a house from abroad

Building back home is a classic diaspora dream — and a classic diaspora heartbreak. The dream: more house for your money, exactly how you want it. The heartbreak: a half-finished shell, a budget that doubled, and a supervisor who’s “almost done” for two years.

It can be done well, but only with structure. The essentials: buy and title the land first, with full due diligence; hire a registered architect and a quantity surveyor (QS) who prices the works and certifies each stage; use an NCA-registered contractor on a written contract with a fixed scope, a milestone payment schedule and penalties for delay; and release money only against the QS’s sign-off, not the contractor’s say-so. Independent supervision is the whole game when you’re not on site. Our building a house in Kenya guide lays out costs (roughly KES 35,000–120,000 per square meter by finish), the approvals, and the milestone-contract approach in detail.

Honestly, building remotely is the highest-effort, highest-risk route on this list. If this is your first Kenyan project and you can’t visit regularly, consider buying a finished, titled home instead — and saving the build for when you’re on the ground.

The lower-hassle alternatives

Not everyone wants to be a long-distance landlord or client-of-record on a construction site. Two routes give you Kenyan property exposure with far less to go wrong.

REITs. A real estate investment trust lets you own a slice of professionally managed property — student housing, warehouses — and earn a share of the income, without touching title, tenants or contractors. The easy retail route is Acorn’s Vuka platform (CMA-regulated), where you can start from about KES 2,500 and sell your units when you want. No 99-year leasehold cap applies, because a REIT unit is a security, not land — so non-citizens can buy freely too. It won’t give you a house to sleep in, but for diversification and income it’s the lowest-stress way in. See our guide to investing in Kenyan REITs.

Buy ready, then hand it to a manager. If you want a real, tangible unit, buying a finished, titled apartment and putting it with a licensed property manager removes most of the remote headache — they find tenants, collect rent and handle repairs while you’re abroad. You still do the title diligence up front, but you avoid construction risk entirely.

Five routes, compared. Higher control usually means more effort and more risk.

Five routes, compared. Higher control usually means more effort and more risk.

| Route | Effort from abroad | Main risk | Best for |

|---|---|---|---|

| Ready, titled apartment | Low–medium | Overpaying; title fraud | A tangible home or steady rental |

| Off-plan unit | Medium | Developer delay or default | Lowest entry price, rising areas |

| Build a house | High | Overruns, supervision fraud | Those with land + reliable oversight |

| REIT (via Vuka) | Very low | Market/liquidity, lower control | Income and diversification, hands-off |

| Raw land | Medium | Land fraud is highest here | Patient buyers, citizens (freehold) |

The diaspora toolkit most guides skip

Buying a building isn’t the only way the diaspora is wired into Kenya’s economy. A few tools are built specifically for people sending money home — and most property guides never mention them. They’re worth knowing whether you use them to buy, to save toward a purchase, or simply to diversify around one.

Three hands-off routes. None replace a home to live in, but all are simpler than landlording.

Three hands-off routes. None replace a home to live in, but all are simpler than landlording.

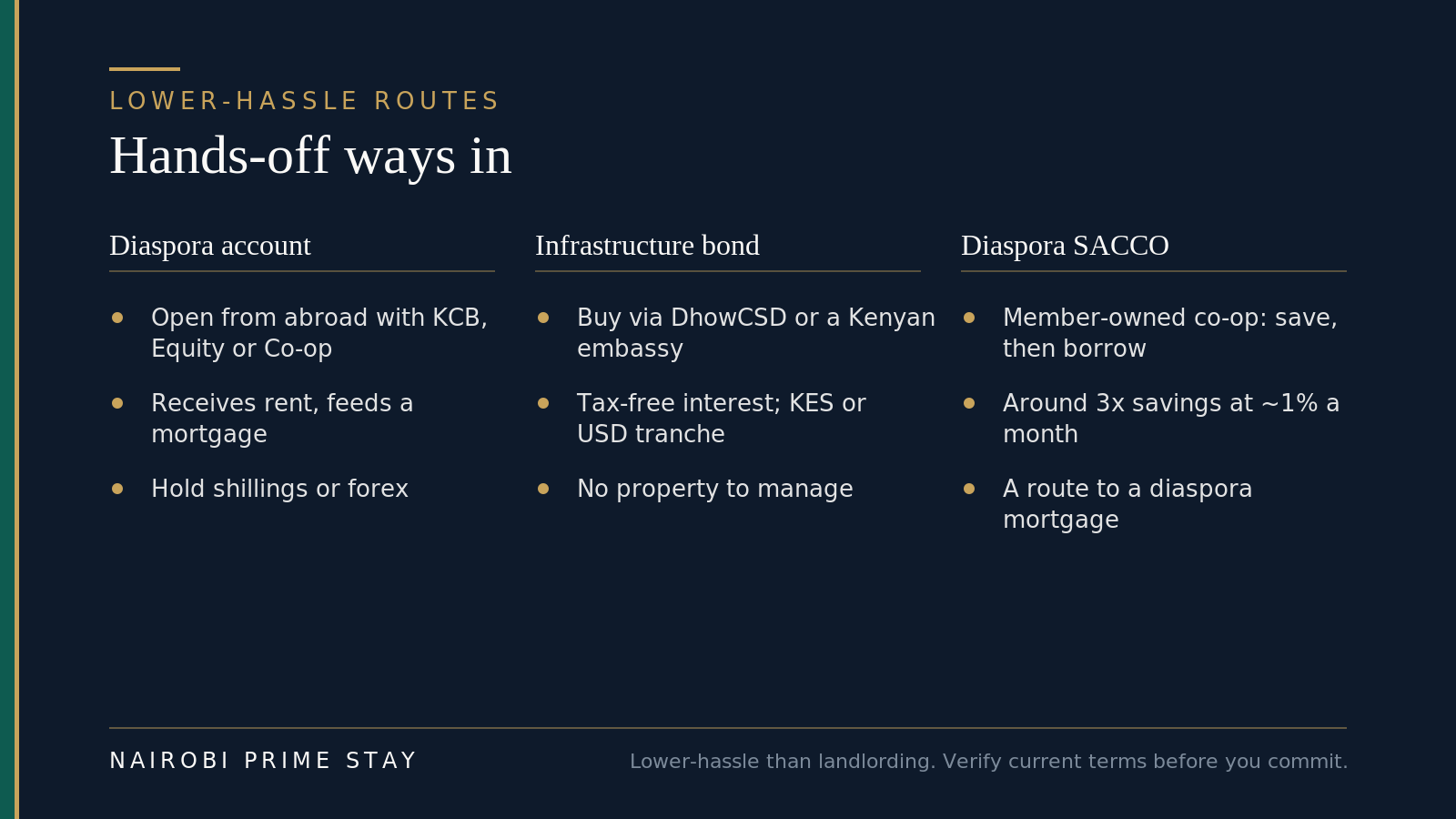

Diaspora bank accounts. Most big Kenyan banks — KCB, Equity, Co-operative and others — let you open an account from abroad, hold shillings or foreign currency, receive rent, and feed a mortgage. It’s the plumbing behind almost everything else here.

Diaspora and infrastructure bonds. Kenyan government infrastructure bonds pay tax-free interest and are a genuinely low-hassle way to earn from Kenya with no tenants or title. In early 2026 the Treasury issued a diaspora-targeted infrastructure bond, subscribable through Kenyan embassies and the State Department for Diaspora Affairs, in both shilling and US-dollar tranches — the shilling side pays the full tax-free yield, the dollar side a lower yield with currency-stable returns. More broadly, you can buy government securities online from abroad through the Central Bank’s DhowCSD platform. This is about as hands-off as Kenyan investing gets.

Diaspora SACCOs. A SACCO is a member-owned savings-and-credit cooperative — a huge part of how Kenyans actually finance homes, and a route most foreign-buyer guides skip. You save first, then borrow around three times your savings at roughly 1% a month on a reducing balance, leaning on your savings record rather than a credit score. Several run diaspora products (Kenya USA Diaspora SACCO, Stima and others); stick to SASRA-regulated ones. It’s mainly a route for Kenyan citizens abroad, and often a cheaper path to a deposit or a diaspora mortgage than a bank.

If any of these appeals more than being a long-distance landlord, that’s a perfectly good answer — and often the smart first step. For property exposure without owning a unit, pair this with our guide to Kenyan REITs; to move the money cleanly either way, see sending money to Kenya.

A worked example

Say you’re a Kenyan nurse in Texas with about $120,000 to put to work back home, and you want a rental in Nairobi without flying back twice.

You instruct an advocate in Nairobi you found through the Law Society and a colleague who completed a purchase last year. You shortlist a finished two-bed in Kileleshwa at around KES 14 million (~$108,000). Your advocate runs the Ardhisasa search — clean leasehold title, no caveats. You hire a valuer (it confirms the price is fair) and a cousin and a surveyor both visit; photos and beacons check out. You sign a narrow power of attorney, notarised in Houston and legalised at the Kenyan embassy, so your advocate can sign at completion.

Your 10% deposit goes into the advocate’s stakeholder account, not the seller’s pocket. You wire the balance through your diaspora bank account, timed on a reasonable shilling rate, against the signed agreement. Stamp duty (4% in Nairobi) and legal fees run roughly 5–8% on top. The title is transferred and registered in your name; your advocate does a post-registration search to confirm it. You hand the unit to a licensed property manager who lets it for about KES 90,000–110,000 a month — and because you live in the US, you budget on the net after the non-resident landlord’s 30% tax, not the headline rent. You never gave anyone unsupervised cash, and you never sent a shilling against an unsearched title. That’s the whole game.

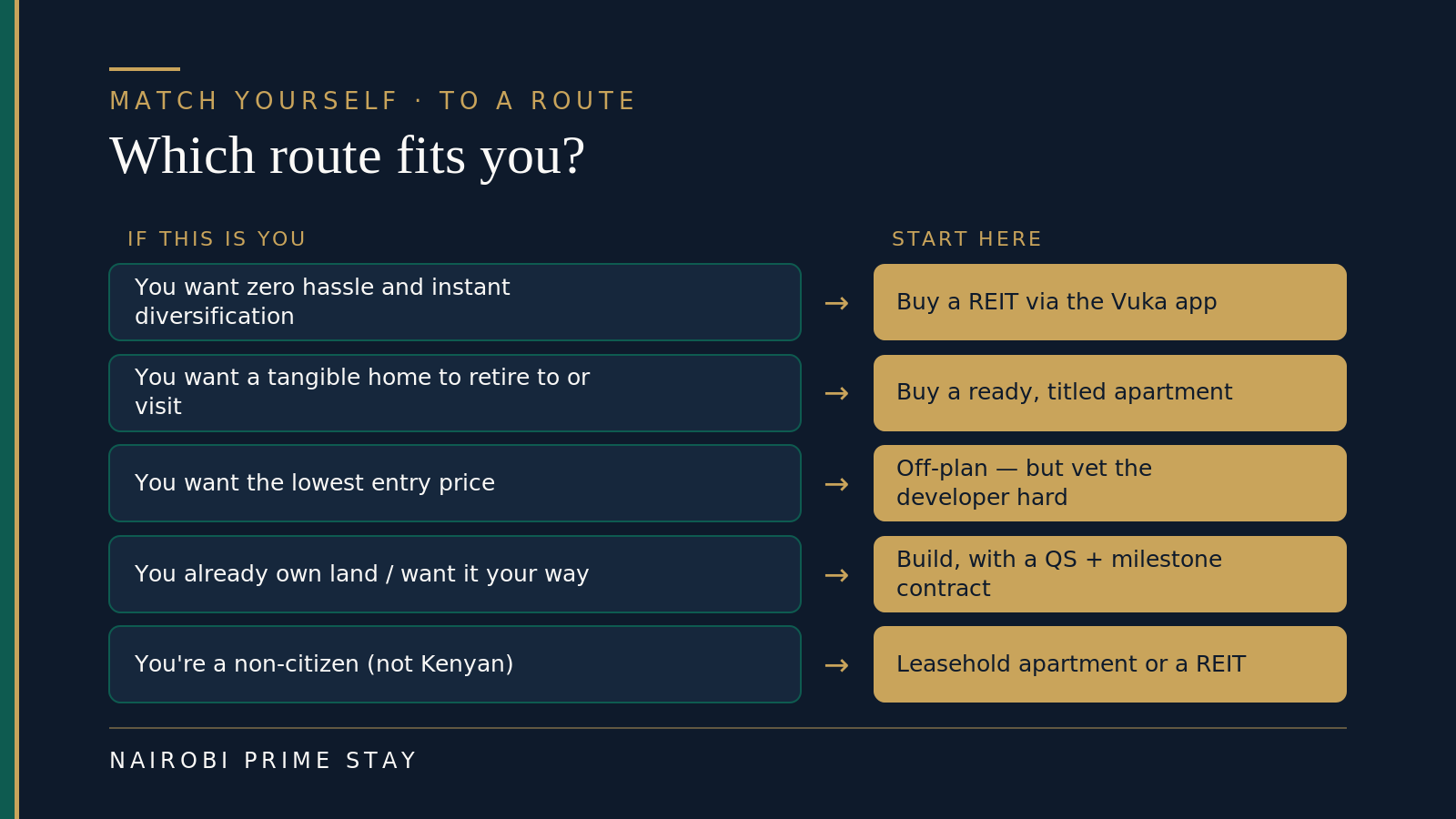

Which route fits you?

There’s no single “best” diaspora investment — it depends on how much hassle you’ll tolerate, whether you want a tangible home, and whether you’re a citizen.

A rough match of goal to route. Most people start hands-off and add direct property later.

A rough match of goal to route. Most people start hands-off and add direct property later.

Red flags vs green lights

After the safeguards, this is the most useful thing to internalise. Remote deals live or die on whether you read these signs — and act on them instead of explaining them away.

Read the signs. Any single red flag is reason to slow down and verify.

Read the signs. Any single red flag is reason to slow down and verify.

The honest pros and cons

| Pros | Cons |

|---|---|

| A real anchor at home — for retirement, visits, or an eventual return | You can’t inspect or supervise in person; you rely on others |

| Rental income, often in a shilling that has steadied around 129 | Land and off-plan fraud target the diaspora specifically |

| Citizens can hold freehold and farmland; strong long-term land demand | Property is illiquid and slow to unwind from abroad if it goes wrong |

| Lower-hassle routes (REITs, managed lettings) exist if you want them | Currency risk on a KES mortgage repaid from foreign income |

| Diaspora mortgages and accounts make financing and transfers workable | Informal family arrangements cause most diaspora losses |

Property is a real asset, not advice to buy. Match it to your wider plan, your timeline and your appetite for hassle — and never invest money you can’t afford to have tied up for years.

Your diaspora due-diligence checklist

Work down this list and you’ve removed most of the ways a remote purchase goes wrong:

- Confirm whether you’re buying as a citizen (freehold OK) or non-citizen (99-year leasehold).

- Instruct your own advocate, verified with the Law Society of Kenya — never the seller’s or agent’s.

- Verify the firm’s bank details by phone using a number you found yourself, before any transfer.

- Get an official title search (Ardhisasa/eCitizen) and read it — never trust a forwarded “copy.”

- Commission a licensed surveyor to confirm beacons, and a valuer to confirm the price.

- Have a trusted, disinterested person visit and send photos/video — not the seller’s friend.

- Route the deposit into an escrow/stakeholder account, against a signed agreement.

- Never wire property money to an individual’s personal account or M-Pesa.

- Grant a narrow, specific, registered power of attorney — limited to this one deal.

- Move funds through regulated channels (bank wire, Wise, diaspora account) and document every shilling.

- For a build, use a QS and milestone contract; release money only against certified stages.

- Budget 5–8% over the price for stamp duty, legal and registration costs, and do a post-registration search.

Frequently asked questions

Can I buy property in Kenya while living abroad?

Yes. Plenty of diaspora and overseas buyers complete a purchase without ever flying in, using an advocate, a power of attorney and an escrow account. The catch is that the due diligence you’d normally do in person has to be done by professionals you hire — so the safeguards matter more when you’re remote, not less.

Do I have to fly to Kenya to buy?

No, but someone independent should physically see the property before you pay. You can grant a narrow power of attorney to a trusted advocate or person to sign on your behalf. A site visit by you, a hired licensed surveyor, or a trusted person with no stake in the sale is non-negotiable — never rely solely on the seller or agent for the truth about a plot.

As a Kenyan in the diaspora, can I own land outright?

Yes. Kenyan citizens — including dual citizens living abroad — can own land freehold and can buy agricultural land, with the same rights as any resident. Non-citizens (for example an American with no Kenyan passport) are capped at 99-year leasehold and cannot own farmland without a rare exemption. Work out which applies to you before you start.

How do diaspora mortgages work and what do they cost?

Several banks — KCB, Equity, Co-operative, Absa, Stanbic, Standard Chartered, NCBA and National Bank — offer dedicated diaspora home loans. As of early 2026 expect around 13–16% interest, a deposit of 20–30%, and proof of offshore income plus a KRA PIN and a Kenyan account. KMRC-backed loans can be about 7–9.9%, for owner-occupied homes up to roughly KES 10.5M — and the income cap was scrapped in 2024, opening them to more buyers. Confirm live terms with the bank.

What’s the safest way to send the money?

Through traceable, regulated channels: a bank wire or a service like Wise into an escrow/stakeholder account held by your advocate, against a signed agreement — never to an individual’s personal or M-Pesa account. Document every transfer. For a large purchase, watch the USD/KES rate (about 129.4 in mid-2026) rather than converting blind on a bad day.

How do diaspora buyers get scammed, and how do I avoid it?

The classics are fake or duplicate title deeds, double sales, an ‘agent’ or relative who pockets the deposit, and off-plan projects that never finish. Defend yourself with an official title search before any money moves, your own independent advocate, an escrow account, independent verification of the site, and a flat refusal to pay cash to any individual. Any single red flag — pressure, a rush, a personal-account request — is reason to stop and verify.

Should I let a family member handle the purchase?

Carefully. Family help with logistics is normal, but informal ‘just send the money to my cousin’ arrangements are the single biggest cause of diaspora loss. If you involve family, still use an advocate, a written narrow power of attorney, an escrow account and a documented money trail, and keep the title in your own name. Treat it as a transaction, not a favor — good relatives usually prefer the clarity.

Is a REIT a better option than buying a building from abroad?

For many diaspora investors, yes — at least to start. A REIT bought through the CMA-regulated Vuka app (from about KES 2,500) gives you property exposure, income and the ability to sell out, with none of the title, tenant or contractor risk, and no leasehold cap for non-citizens. Buy a physical unit when you want a specific home or more control — and put it with a licensed manager so you’re not landlording from another time zone.

If I rent out my Kenyan property from abroad, how is the rent taxed?

It depends on your tax residency, not your passport — and most people living abroad are non-resident for Kenyan tax. A non-resident landlord’s rent is taxed at 30% of the gross, withheld by the tenant or agent and remitted to KRA as a final tax, with no deductions. A resident pays the lighter Monthly Rental Income tax (7.5%, which the Finance Bill 2026 proposes to raise to 10%). Kenya has treaties with the UK, Canada, Germany and others that can cap the 30%, but none with the United States — so a US-based owner pays the full rate and claims a US foreign tax credit. Budget on the net, not the headline.

Can I get my rental income and sale proceeds out of Kenya?

Yes. Kenya has no exchange controls, so you can move rent and eventual sale proceeds out freely through your bank, in the currency you choose. Declare physical cash over USD 10,000 at the border, though wire transfers have no such cap. When you sell, Capital Gains Tax of 15% on the net gain comes off first; the rest repatriates without restriction. Keep records for both tax authorities.

What are diaspora infrastructure bonds, and can I buy them from abroad?

They’re government bonds that fund infrastructure and pay tax-free interest — a low-hassle way to earn from Kenya without owning property. In early 2026 the Treasury issued a diaspora-targeted infrastructure bond you can subscribe to through Kenyan embassies or the State Department for Diaspora Affairs, in shilling or US-dollar tranches. More generally, you can buy Kenyan government securities online from abroad through the Central Bank’s DhowCSD platform. It won’t give you a home to use, but for income and diversification it’s about as hands-off as it gets.

Final thoughts

Distance is the only thing that makes diaspora investing risky — and every safeguard in this guide is a way to close that distance. Your own advocate, an official search, escrow, a narrow power of attorney, independent eyes, and money that only ever moves against paperwork. Do those, and you’re buying like a professional rather than hoping like a stranger.

Start with how much hassle you actually want. If you’d rather not manage anything, a REIT or a managed, ready apartment gets you in cleanly. If you want a home to return to, buy finished and titled, and save the build for when you can be on the ground. Either way, slow is safe: the deals that fall apart are almost always the ones someone rushed.

If your investment is also the first step toward moving — including African Americans weighing a return — pair this with our guide to relocating to Nairobi and an honest look at the African-American relocation experience. This is general guidance, not legal, tax or investment advice; confirm the specifics for your situation with a Kenyan advocate and a cross-border tax adviser.

Related reading

- Property investing in Kenya: the complete guide — the cluster pillar, start here

- Can foreigners buy property in Kenya? — citizen vs non-citizen rights

- Property financing & diaspora mortgages in Kenya — every funding route

- Investing in Kenyan REITs — property exposure without the landlording

- Buying land in Kenya — the due-diligence and anti-fraud playbook

- Conveyancing in Kenya — what your advocate actually does

- Building a house in Kenya — costs and project-managing a build

- Common property scams in Kenya — and how to avoid them

- Sending money to Kenya — the cheapest, safest rails

- Moving to Nairobi: the complete guide — the relocation hub

When you’re ready to be on the ground

When you fly in to view properties, sign at completion or check on a build, you’ll want a secure, fully equipped base — not a hotel. A serviced apartment gives you Wi-Fi, cleaning, a backup generator and 24/7 security, on flexible monthly terms, so you can run your viewings and meetings from a real home. A $50 deposit reserves your dates and the balance is paid on arrival — nothing more before you travel.

Not sure which area or which route fits your budget and plans? Our AI relocation assistant can talk through neighborhoods, shortlist apartments and point you to the right guides, day or night.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.