Guides · Property investment

Financing Property in Kenya: Mortgages for Foreigners & Diaspora (2026)

Financing Property in Kenya: Mortgages for Foreigners & Diaspora (2026)

Here’s the honest answer most sites bury: the vast majority of property in Kenya is bought with cash, not a mortgage. The whole country has only about 30,000 active mortgages. So if you’re an American or a diaspora Kenyan wondering how to fund a home here, the real question isn’t only “can I get a loan?” — it’s “which way of paying makes sense for me?”

You can get a mortgage. Foreigners with the right permit can borrow from a Kenyan bank, and Kenyans living abroad have dedicated diaspora home-loan products. But local interest rates are high by US standards, the deposit is steep, and if you earn dollars and borrow shillings you take on real currency risk. For many buyers, cash — or borrowing cheaply against an asset back home — works out simpler and cheaper.

This guide lays out every route, with the 2026 numbers and who each one suits. It’s written for the foreign and diaspora buyer, and it’s deliberately even-handed: a mortgage is a tool, not a trophy, and sometimes the smart move is not to take one.

One note up front: this is general information, not financial advice. Rates and lending rules change with every budget cycle and every bank promotion. Treat this as the map, then get quotes from two or three lenders and, if the cross-border picture is involved, a financial adviser who knows both systems.

TL;DR: Most foreigners and diaspora buyers in Kenya pay cash — the mortgage market is tiny (~30,000 loans nationwide). You can borrow: a resident foreigner with a 2-year-plus permit can take a local KES mortgage (typically 14–18%, occasionally near 9% on a promo, deposit 10–20%), and Kenyans abroad can use a diaspora mortgage (deposit usually 20–30%, tenor up to 25 years). Government-backed KMRC loans are cheaper (9–11%) but aimed at lower-income Kenyan owner-occupiers, so most expats won’t qualify. Developer payment plans fund off-plan units without a bank. If you earn dollars, weigh the currency risk of a shilling loan — and consider borrowing against a US asset to buy here in cash.

There’s no single best way to pay — it depends on where you live, what you earn, and what you already own.

There’s no single best way to pay — it depends on where you live, what you earn, and what you already own.

Why this matters

How you finance a purchase shapes the whole deal — your budget, your timeline, even which properties you can realistically chase. A cash buyer can move fast and negotiate hard. A mortgage buyer needs the bank’s valuation, the bank’s lawyers, and the bank’s blessing, which adds weeks and conditions. Get the financing decision right early and everything downstream is smoother.

It matters even more for foreigners because the rules and the maths are different from home. US mortgage rates and a 30-year fixed loan don’t exist here. A Kenyan home loan is shorter, dearer, and priced off the Central Bank Rate, so the monthly number can move. And because most foreigners can only hold property on leasehold, your loan term and the lease term have to line up. Knowing all this before you fall for an apartment saves you from a financing plan that quietly falls apart at the bank.

The honest reality: Kenya is a cash market

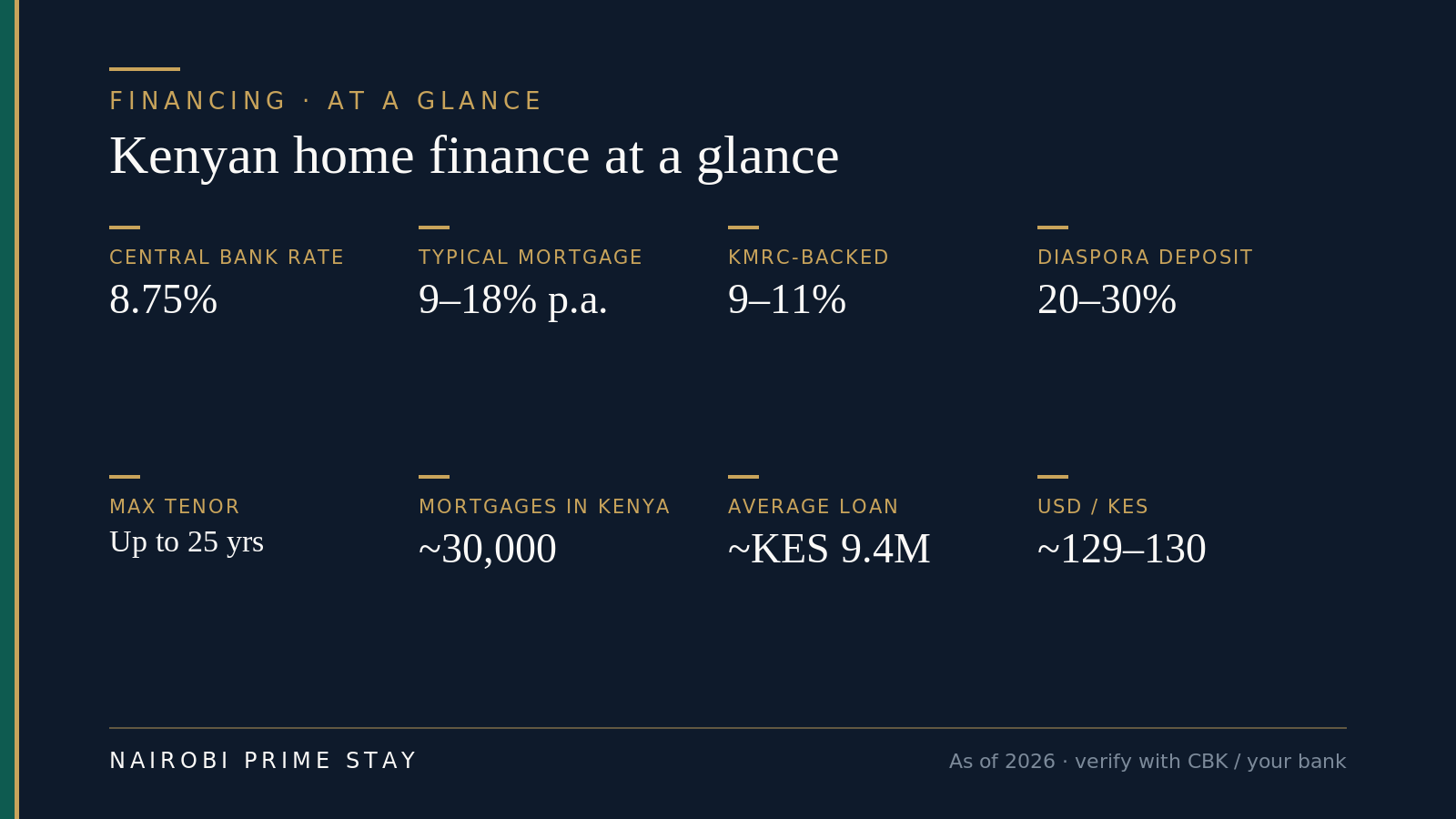

Before we get into mortgages, hold this fact: Kenya had only about 30,000 mortgage accounts at the last full count, in a country of more than 50 million people. The total mortgage book was around KES 279 billion in the Central Bank’s 2024 report, and the average loan was about KES 9.4 million. Compare that to the US, where a mortgage is the default way to buy a home, and you see the difference. In Kenya, the loan is the exception.

Why so few? Rates are high, deposits are large, formal payslips aren’t universal, and land-title complications make banks cautious. So most Kenyans — and most foreign buyers — save up, sell another asset, or use family money, and buy outright. As a foreigner, you’re stepping into a market where cash is normal and expected. That’s good news for you: cash buyers are taken seriously and can negotiate.

None of this means a mortgage is wrong. It means a mortgage is a deliberate choice you make when the leverage helps you, not a default you reach for. The rest of this guide walks the choices.

The headline numbers, as of 2026 — verify the live figures with the Central Bank of Kenya and your chosen lender.

The headline numbers, as of 2026 — verify the live figures with the Central Bank of Kenya and your chosen lender.

Route 1: Paying cash (what most foreigners actually do)

Paying cash is the simplest route, and for many foreigners it’s the best one. You agree a price, your advocate runs the due diligence and conveyancing, you transfer the funds, and the title moves into your name. No bank valuation, no loan conditions, no currency mismatch, no decades of interest. For a typical Nairobi apartment bought by an overseas buyer, this is the standard path.

The mechanics are easy. You move money in through a regular bank transfer or a service like Wise, which handles USD-to-KES at a fair rate, and your advocate holds the deposit as a stakeholder until completion. Our guide to sending money to Kenya covers the cheapest, cleanest ways to move it. Bringing larger sums, keep clean records of the source of funds — your Kenyan bank and the law require it, and it makes the eventual sale cleaner too.

The honest trade-off is opportunity cost. Cash tied up in a Nairobi flat isn’t invested elsewhere, and Kenyan property is not as liquid as a US brokerage account — selling can take months. So paying cash suits you if you have the funds spare, want a clean and fast purchase, and value simplicity over leverage. If you’d rather keep your capital working, read on.

Route 2: A local mortgage from a Kenyan bank

Yes, a foreigner can get a mortgage from a Kenyan bank — but you generally need to be resident, with a valid work or residence permit (most banks want at least two years left to run), a KRA PIN, and provable income. Lenders that do these loans include KCB, Stanbic, Absa, Co-operative Bank, Equity, NCBA, Standard Chartered and HF Group. The property itself — usually a completed apartment or house with a clean title — is the security.

Expect these terms, as of 2026:

- Interest rate: roughly 14–18% a year for a standard variable loan. Rates are mostly variable, quoted as “Central Bank Rate plus a margin.” With the CBR at 8.75% (held again in June 2026, after a long run of cuts), a typical mortgage lands in the mid-to-high teens depending on the bank and your profile. Banks periodically run promotional fixed rates as low as 8.9–9% — KCB advertised an 8.9% fixed deal running to mid-September 2026, for instance — but those rates are time-limited, so ask what’s actually live when you apply.

- Deposit: commonly 10–20% for residents; expect the higher end as a foreigner. A bigger deposit often shaves the rate.

- Tenor: up to 20–25 years on paper, though the real average is around 12 years. Your age and your permit length can cap it.

- Loan-to-value: typically 80–90% of the bank’s valuation, which may come in below your purchase price.

The rate is the headline. A 14–17% mortgage is normal here and simply costs more than a US loan — over a long tenor you can pay back well over double what you borrowed. That’s not a scam; it reflects Kenyan inflation and the cost of money. It does mean you should run the monthly figure honestly before you commit, and treat the loan as expensive leverage, not cheap money.

Route 3: Diaspora mortgages (for Kenyans living abroad)

If you’re a Kenyan citizen living in the US or elsewhere, you have your own lane: the diaspora mortgage. Most big banks run dedicated products for Kenyans abroad — KCB, Equity, Co-operative, Absa, Stanbic, NCBA, Standard Chartered and National Bank all advertise them. They’re designed around the reality that your income, payslips and bank statements are foreign, and they let you buy or build back home while you’re away.

The terms are broadly the local terms with a diaspora twist:

- Deposit: usually 20–30% — higher than for a resident, because you’re further from the bank’s reach.

- Income proof: foreign payslips and 6–12 months of bank statements, an employment contract or letter, and often a record of consistent remittances home.

- Rate: similar KES rates, roughly 9–16% depending on the bank, the product and any promotion.

- Tenor: up to 25 years, subject to age limits.

- Documents: a valid Kenyan passport or dual-citizenship papers, KRA PIN, the property’s sale agreement and title, and a credit check.

Diaspora mortgages make most sense when you’re a dual citizen with a clear plan to return or to hold long-term, and you’d rather keep your overseas savings invested than ship them all home at once. They still carry the same currency risk if you earn dollars and repay in shillings — more on that below. A foreign national who isn’t a Kenyan citizen will usually be steered toward the resident mortgage in Route 2 instead, and will need to be living here. For the wider diaspora-buyer picture, see our diaspora property investment guide.

Route 4: KMRC and the affordable-housing scheme (and why it probably isn’t for you)

You’ll see the cheapest rates in Kenya — around 9–11% — attached to the Kenya Mortgage Refinance Company (KMRC). It’s worth understanding, and worth knowing why it likely won’t apply to you. KMRC is a government-backed body that lends cheap, long-term money to banks and SACCOs so they can offer cheaper mortgages. It doesn’t lend to you directly; you borrow from a participating bank or SACCO, and KMRC refinances the loan behind the scenes.

The catch is who it’s for. KMRC-backed loans are an affordable-housing tool aimed at ordinary Kenyan owner-occupiers. To qualify, your household income generally has to fall under about KES 200,000 a month (the cap was raised from KES 150,000 in late 2023), and the property has to sit under set price caps — broadly around KES 8 million in the Nairobi area and KES 6 million elsewhere. A foreign professional buying a prime Nairobi apartment won’t meet the income test, and the scheme expects you to live in the home, not let it out. So treat KMRC as useful context for how Kenya is trying to lower mortgage costs — and as a route for diaspora Kenyans of modest income buying a first home — rather than the deal you’ll get on a Gigiri two-bed.

Route 5: Developer payment plans (the off-plan route)

Here’s the financing tool many foreign buyers actually use instead of a bank: the developer’s own payment plan. Buy a unit off-plan — before or during construction — and most Nairobi developers let you pay in installments rather than all at once. A typical structure is a deposit of 10–20% to reserve, then staged payments across the construction period (often 12–36 months), with the balance due on completion. Some plans are interest-free; others carry a modest charge.

The appeal is obvious: no bank, no permit-tenor hurdle, no credit check, and you spread the cost while the building goes up. It’s often the most accessible way for a foreigner to buy without a lump sum on day one.

The honest risks are real, though. You’re handing money to a developer for something that doesn’t exist yet, so completion risk and delays are the main danger — projects do stall. Protect yourself: buy from a developer with a finished track record, insist your payments are tied to construction milestones, get an advocate to vet the contract and the title, and understand what happens to your money if the project is late or abandoned. Our off-plan property guide covers how to do this safely.

Route 6: Borrowing at home to buy here in cash

This is the route most US buyers overlook, and for some it’s the smartest. Instead of taking an expensive shilling mortgage, you borrow cheaply against an asset you already own at home — a home-equity line of credit, a cash-out refinance, a securities-backed loan against a brokerage account — then bring those funds to Kenya and buy in cash.

The logic is simple arithmetic. If you can borrow in dollars at a US rate well below a 14–17% Kenyan mortgage, and you’re confident in the repayment, the dollar loan is cheaper money. You also sidestep the currency mismatch, because both your loan and your income are in dollars, and you arrive as a clean cash buyer in Nairobi with all the speed and negotiating power that brings.

It isn’t free of risk. You’re putting a US asset on the line for an overseas purchase, and if Kenyan property underperforms you still owe the home loan. But for an American with home equity or investments, comparing a US-based loan against a Kenyan mortgage is a calculation worth doing before you assume the local bank is your only option. This is a conversation for your financial adviser, not a blog — but it belongs on your list.

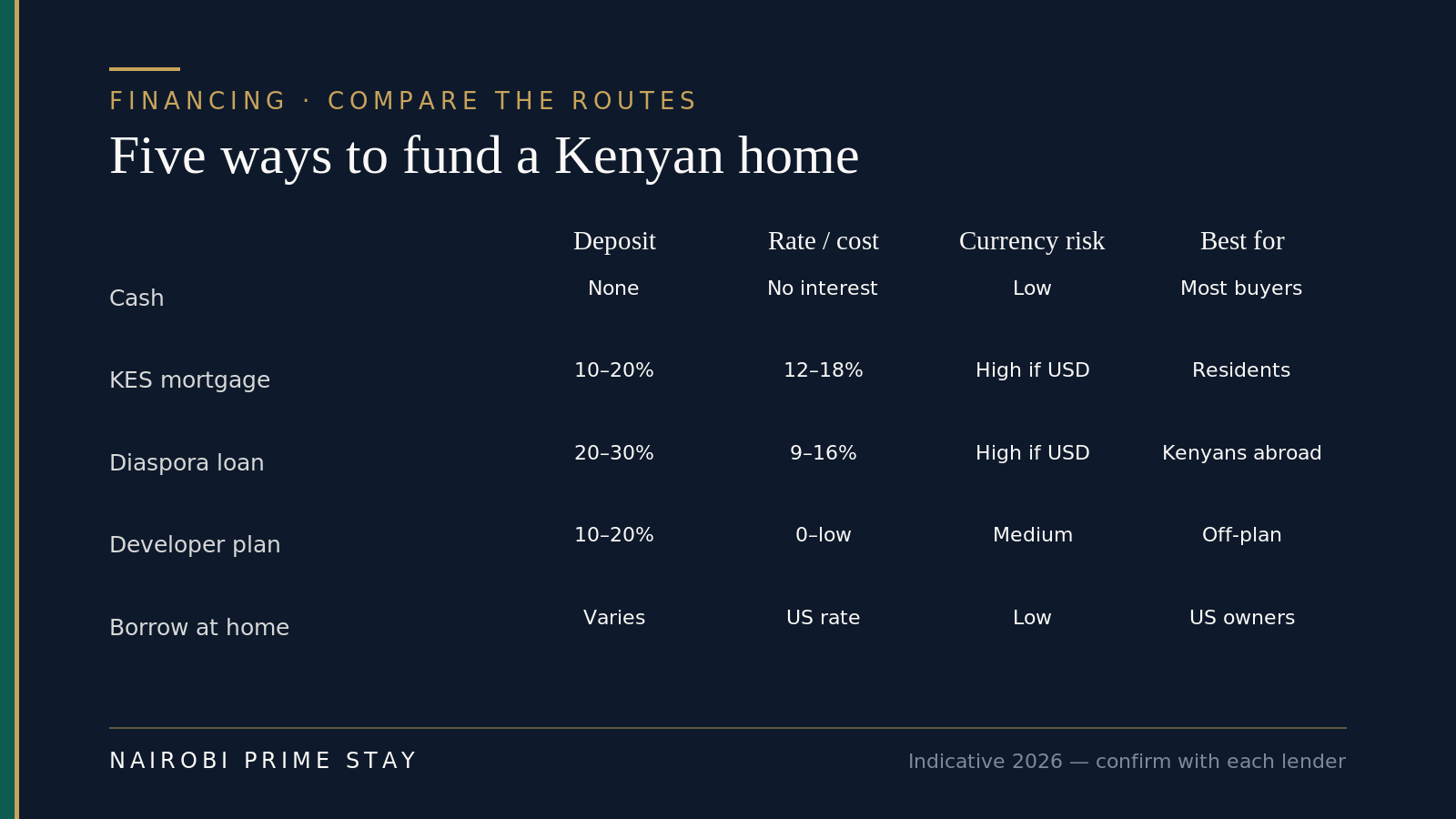

The five routes, side by side

Indicative 2026 figures — confirm every number with the specific lender or developer.

Indicative 2026 figures — confirm every number with the specific lender or developer.

| Route | Deposit | Typical cost | Currency risk | Speed | Best for |

|---|---|---|---|---|---|

| Cash | None | No interest | Low | Fast | Most foreign buyers |

| Local KES mortgage | 10–20% | 14–18% p.a. | High if you earn USD | Slow (weeks+) | Resident foreigners |

| Diaspora mortgage | 20–30% | 9–16% p.a. | High if you earn USD | Slow (weeks+) | Kenyan citizens abroad |

| Developer payment plan | 10–20% | 0–low | Medium | Staged | Off-plan buyers |

| Borrow at home (US) | Varies | US loan rate | Low | Fast | US owners with equity |

Read this as orientation, not gospel — your bank, your developer and your own finances decide the real numbers. But the shape of the decision is clear: cash and borrowing-at-home are the low-friction routes; local and diaspora mortgages are dearer and slower but let you keep capital back; the developer plan is the middle path for a new build.

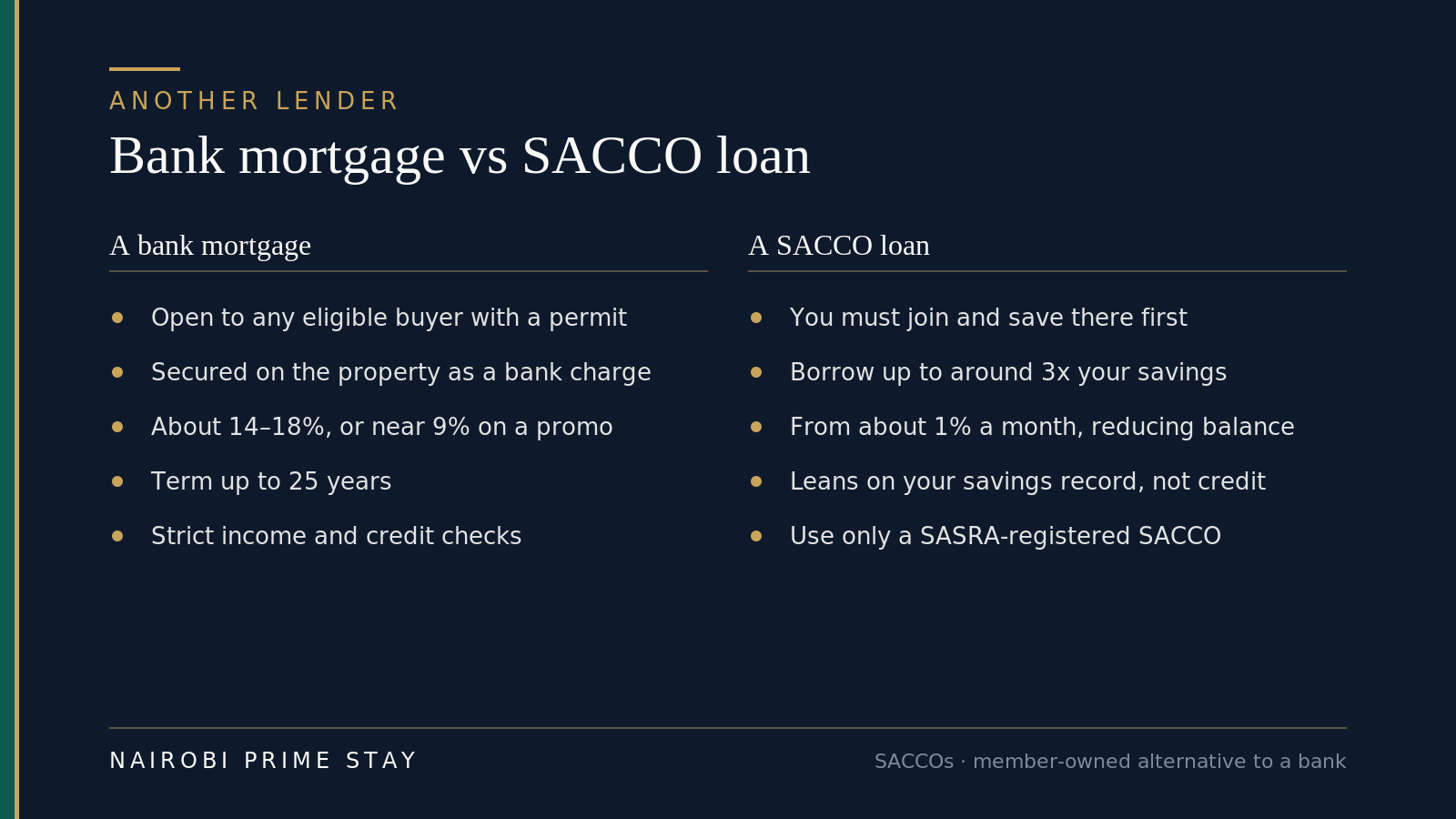

SACCOs: the lender most foreigners miss

Beyond the five routes above, there’s one more source of home finance that almost no foreign-buyer guide mentions, yet it funds a huge share of Kenyan homes: the SACCO. A SACCO — a savings and credit cooperative — is a member-owned mutual where people save together and borrow from the common pool. For property, that often means cheaper money and gentler hurdles than a bank.

A bank lends against the property; a SACCO lends against your savings record — often cheaper, but you have to be a member first.

A bank lends against the property; a SACCO lends against your savings record — often cheaper, but you have to be a member first.

The mechanics differ from a bank. You join the SACCO and build up savings first, then borrow a multiple of what you’ve saved — commonly around three times. Rates are quoted per month on a reducing balance, often from about 1% a month, and approval leans on your contribution history rather than a formal credit score. Many SACCOs lend specifically for land, construction or a finished home.

For the diaspora this is real, not theoretical. Several SACCOs run dedicated products for Kenyans abroad — Stima, Username, Imarisha and the Kenya USA Diaspora SACCO among them — built around remitted savings. The honest caveats: you have to commit to membership and saving before you can borrow, you may need fellow members as guarantors, the loan sizes are smaller than a big bank mortgage, and you must stick to a SASRA-registered SACCO (the regulator’s public list is the test). A non-citizen foreigner usually can’t join, so this is mainly a diaspora-Kenyan route — but for that buyer it can beat a bank on cost. See the diaspora property guide for how it fits the wider plan.

The currency-risk trap (earn dollars, borrow shillings)

This is the part US buyers underestimate. If your income is in US dollars and you take a Kenyan mortgage, your loan is in shillings — so you’re betting on the exchange rate every single month. When the shilling weakens against the dollar, your repayment gets cheaper in dollar terms. When it strengthens, it gets dearer. You don’t control which way it moves.

The shilling has had a bumpy few years. It slid sharply in 2023 and into 2024, then recovered, and has sat around 129–130 to the dollar through the first half of 2026. That recovery actually worked against dollar-earners who’d hoped a weak shilling would shrink their repayments. The point isn’t to predict the rate — nobody can — it’s that a KES loan adds a variable you can’t manage on top of an already-high interest rate.

There are only really two clean ways to avoid it: pay cash, or borrow in the currency you earn (Route 6). If you do take a shilling mortgage as a dollar-earner, keep a buffer for the months the rate moves against you, and don’t borrow to your absolute limit. For the live rate and the full picture, check the Central Bank of Kenya or Wise, or see our USD–KES currency guide, rather than trusting any figure quoted in an article.

What a Kenyan mortgage actually costs (beyond the rate)

The interest rate isn’t the whole bill. Budget for the same closing costs as any Kenyan purchase, plus a few lender charges on top:

- Arrangement / negotiation fee: roughly 1% of the loan, charged by the bank to set it up.

- Valuation fee: the bank insists on its own valuer; you pay for it.

- Legal fees: the bank’s advocate prepares the charge document, on the standard fee scale, and you usually cover it as well as your own conveyancing.

- Stamp duty on the charge: a small duty applies to registering the mortgage itself, separate from the duty on the purchase.

- Mortgage protection and property insurance: lenders require life cover for the loan and insurance on the building, paid annually.

Add these to the ordinary buying costs — stamp duty of 4% in Nairobi, legal fees, valuation and registration — and the cost of getting into a financed purchase is meaningfully more than a cash one. Our property taxes guide breaks down the duty and the how-to-buy guide covers the full closing-cost stack.

The habits that keep a financed purchase clean — and the ones that cost money.

The habits that keep a financed purchase clean — and the ones that cost money.

What a shilling mortgage really costs each month

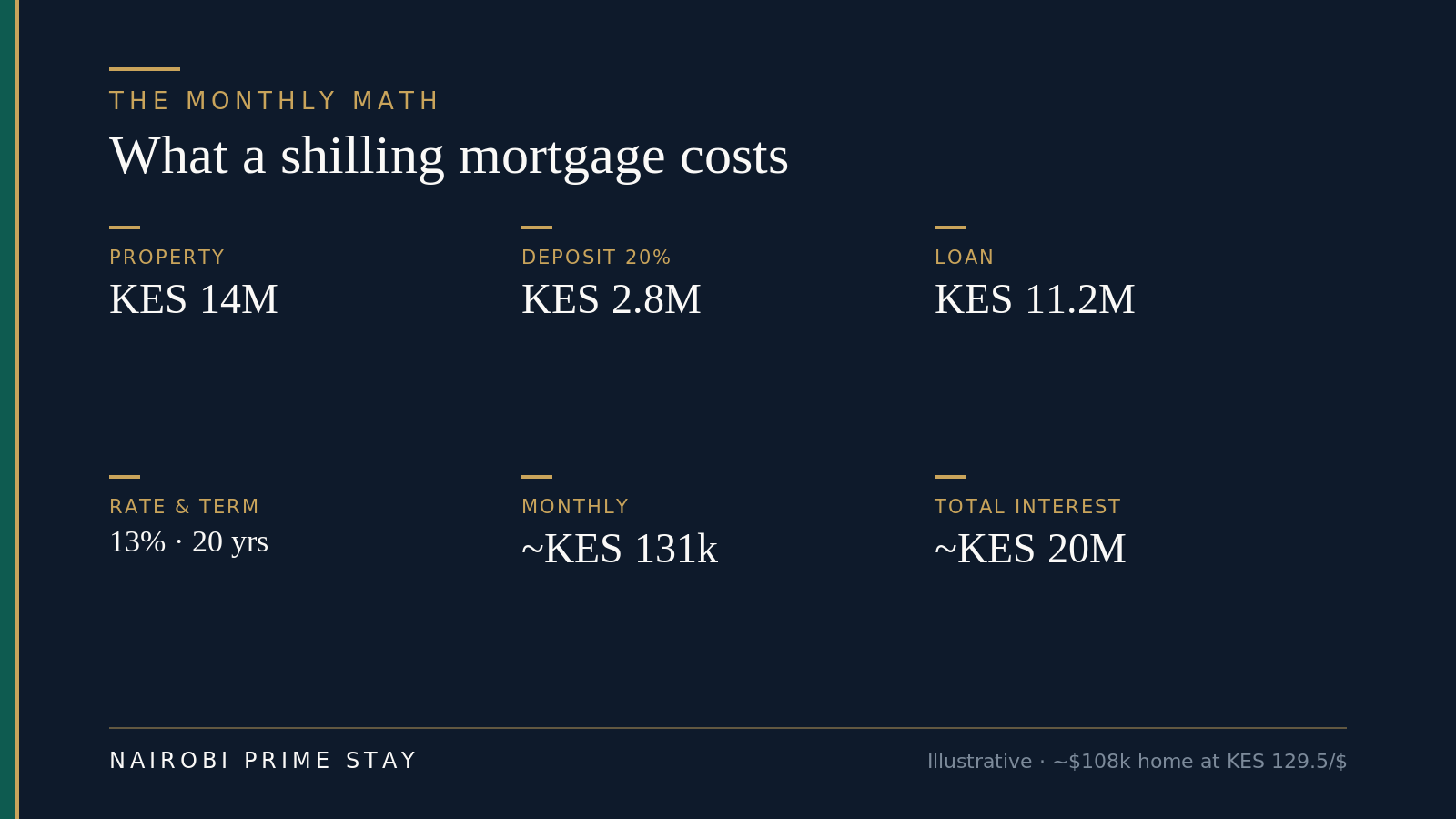

Numbers make the rate real. Take a KES 14 million apartment — about a two-bed in Kilimani, and roughly $108,000 at today’s rate. Put 20% down (KES 2.8 million) and you borrow KES 11.2 million. At a typical 13% over 20 years, here’s how it lands.

Illustrative figures at about KES 129.5 to the dollar — run your own on the lender’s calculator before you commit.

Illustrative figures at about KES 129.5 to the dollar — run your own on the lender’s calculator before you commit.

Your repayment is about KES 131,000 a month — roughly $1,010. Over the full term you’d pay around KES 20 million in interest, repaying about KES 31.5 million all in: close to three times the loan. That’s not a trick; it’s what a high rate does over two decades.

Now see what the rate alone changes. Drop it to a KMRC-style 9.5% and the same loan costs about KES 104,000 a month and roughly KES 13.9 million in interest — a saving of about KES 27,000 every month and around KES 6 million over the life of the loan. That gap is exactly why the promotional and KMRC-backed rates are worth chasing, and why a 14–18% standard rate deserves a hard look before you sign. Whatever you’re quoted, plug it into the bank’s own calculator with your real deposit and term, then compare the monthly figure to what the same place would rent for — our Nairobi property prices guide has the price and rent anchors.

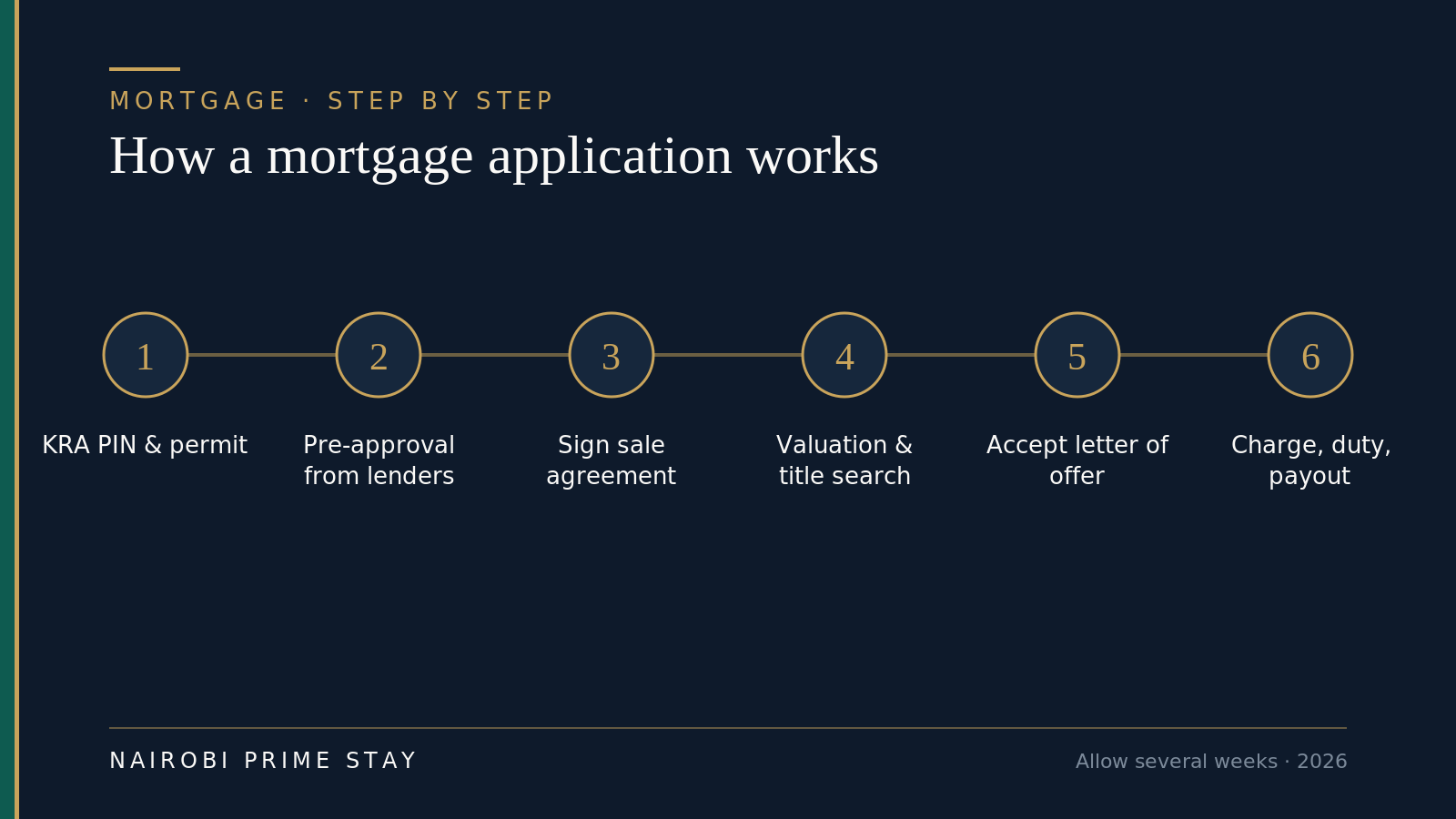

How to actually apply for a mortgage, step by step

If you do go the bank route, the process is fairly standard across lenders. Knowing the order keeps you from wasting weeks.

The usual order — allow several weeks from application to disbursement.

The usual order — allow several weeks from application to disbursement.

- Get your paperwork straight. A KRA PIN is non-negotiable, and a resident foreigner needs a work or residence permit with at least two years left. A diaspora Kenyan swaps the permit for a passport (or dual-citizenship papers) and foreign income documents. Sort your tax registration early — the PIN underpins the whole purchase.

- Get pre-approved. Take your income proof to two or three lenders and ask for a pre-approval, an “approval in principle.” It tells you your real budget and your actual rate before you fall for a place.

- Find the property and sign. Agree the price and sign the sale agreement, usually with a deposit your advocate holds in trust.

- Valuation and title search. The bank sends its own valuer and runs a title search. Its valuation can come in below your price, which changes how much it will lend.

- Letter of offer. If it all checks out, the bank issues a formal letter of offer setting the amount, rate, term and conditions. Read every line — this is the loan.

- Charge, duty and disbursement. You accept, the bank’s advocate registers a charge over the title, you pay stamp duty on that charge, and the loan is released to complete the purchase.

The honest timeline is several weeks, sometimes longer if the title needs cleaning up. A cash buyer skips steps two, four and five entirely — which is exactly why cash moves faster and negotiates harder.

How this plays out: two buyers, two routes

The diaspora buyer. Grace is a Kenyan citizen and a nurse in Texas. She wants a two-bedroom apartment in Kilimani for about KES 14 million to rent out now and live in later. She takes a diaspora mortgage: 25% deposit (KES 3.5 million) from her US savings, a 20-year loan at around 13%, proven with a year of US payslips and bank statements and her record of sending money home. Her rent helps cover the repayment, and she keeps the rest of her US savings invested. The currency risk is real — she earns dollars, repays shillings — so she keeps a few months’ cushion. For her, leverage and a foothold back home are worth it.

The American cash buyer. Mark is a US citizen, not a Kenyan, eyeing a similar Kilimani apartment as an investment. He doesn’t live in Kenya, so a resident KES mortgage isn’t open to him, and a 14%+ shilling loan with currency risk looks ugly anyway. Instead he draws on a home-equity line against his Denver house at a far lower US rate, wires the funds through his bank, and buys in cash. He completes in weeks, negotiates a small discount as a cash buyer, and owes only his dollar loan — no shilling exposure. Same apartment, completely different financing, each right for the person.

Neither bought the way the other did, and neither was wrong. That’s the whole lesson: the right route follows your citizenship, your residence and what you already own.

Your property-financing checklist

Work through these before you commit to a way of paying:

- Decide cash vs. borrow first — it shapes your budget, timeline and target list.

- If borrowing locally, check eligibility — residence/work permit with 2+ years to run, KRA PIN, provable income.

- Get quotes from two or three lenders — rate, deposit, tenor and all fees, in writing.

- Ask whether a KMRC-backed rate applies — only if you meet the income and price caps.

- Price the full cost, not just the rate — arrangement, valuation, legal, stamp duty on the charge, insurance.

- Match loan currency to income — or accept and budget for the currency risk.

- For off-plan, vet the developer — track record, milestone-linked payments, advocate-checked contract and title.

- Compare a US-based loan against the Kenyan mortgage if you own assets at home.

- Confirm the loan term fits the lease term — leasehold property can’t outlast its lease.

- Keep clean source-of-funds records for every shilling you bring in.

- Get advice — a Kenyan mortgage adviser, and a cross-border financial adviser if dollars are involved.

Frequently asked questions

Can a foreigner get a mortgage in Kenya?

Yes. A foreigner who is resident in Kenya, with a valid work or residence permit (most banks want at least two years still to run), a KRA PIN and provable income, can take a mortgage from a Kenyan bank such as KCB, Stanbic, Absa, Co-operative, Equity or Standard Chartered. Expect a deposit of 10 to 20 percent and a rate of roughly 12 to 18 percent a year as of 2026. The property’s clean title is the security, and the bank will value it before lending.

Can a diaspora Kenyan get a mortgage in Kenya?

Yes, and there are dedicated products for it. Most major banks offer diaspora mortgages for Kenyan citizens living abroad, built around foreign payslips and bank statements. They typically need a larger deposit of around 20 to 30 percent, 6 to 12 months of statements, proof of consistent income, and your passport or dual-citizenship papers. Tenors run up to 25 years, subject to age limits.

What are mortgage interest rates in Kenya in 2026?

Most Kenyan mortgages run at roughly 12 to 18 percent a year as of 2026, with the full market ranging from about 9 to 18 percent. Rates are usually variable, quoted as the Central Bank Rate plus a margin, and the CBR was held at 8.75 percent in June 2026. Government-backed KMRC loans are cheaper at about 9 to 11 percent, and banks sometimes run time-limited promotional rates near 9 percent. Confirm the live rate with the lender, because it moves.

How much deposit do you need for a mortgage in Kenya?

Resident borrowers usually need a deposit of about 10 to 20 percent of the property value, and diaspora or non-resident foreign buyers are typically asked for 20 to 30 percent. That maps to a loan-to-value of around 70 to 90 percent of the bank’s own valuation, which can come in below your purchase price. A larger deposit often earns a slightly lower interest rate.

Is it better to pay cash or take a mortgage in Kenya?

For most foreign buyers, cash is simpler and cheaper. Kenya is largely a cash market — there are only about 30,000 mortgages in the whole country — and a 12 to 18 percent shilling loan is expensive over time. Cash avoids interest, currency risk and weeks of bank conditions, and gives you negotiating power. A mortgage makes sense only when you want to keep your capital invested elsewhere and can comfortably carry the repayment.

What is KMRC and can foreigners use it?

KMRC, the Kenya Mortgage Refinance Company, is a government-backed body that funds banks and SACCOs cheaply so they can offer mortgages at around 9 to 11 percent. You borrow from a participating bank or SACCO, not from KMRC directly. It is an affordable-housing scheme aimed at Kenyan owner-occupiers with household income under about KES 200,000 a month, so most foreign professionals buying prime property will not qualify, though lower-income diaspora Kenyans buying a first home might.

Can you buy property in Kenya with a payment plan?

Yes — many developers offer payment plans on off-plan units, which is how a lot of foreign buyers fund a purchase without a bank. A common structure is a 10 to 20 percent deposit to reserve, then staged installments over the 12 to 36 month construction period, with the balance due on completion. The main risk is completion risk, so buy from a developer with a track record, tie payments to construction milestones, and have an advocate vet the contract and title.

What is the maximum mortgage term in Kenya?

Kenyan mortgages can run up to about 20 to 25 years on paper, though the average loan in practice is closer to 12 years. Your age and, for foreigners, your permit length can shorten the maximum a bank will offer. On leasehold property the loan term also cannot run past the remaining lease, so check the unexpired years before you borrow.

Should I take a Kenyan mortgage if I earn US dollars?

Be careful. A Kenyan mortgage is in shillings, so if you earn dollars you take on currency risk on every repayment — the shilling has sat near 129 to 130 to the dollar in 2026 but has swung in recent years. Combined with a high local interest rate, that makes a shilling loan an expensive and unpredictable choice for a pure dollar-earner. Many US buyers instead pay cash or borrow against a US asset at a lower dollar rate, and only take a KES loan if they have shilling income to match it.

How do I apply for a mortgage in Kenya?

Start by getting your KRA PIN and, if you’re a foreigner, a work or residence permit with at least two years to run; diaspora Kenyans use a passport and foreign income documents instead. Then get a pre-approval from two or three lenders so you know your budget, find the property and sign the sale agreement, and let the bank run its valuation and a title search. If it all checks out the bank issues a letter of offer; once you accept, its advocate registers the charge, you pay stamp duty on that charge, and the loan is disbursed to complete the purchase. Allow several weeks from start to finish.

How much would a Kenyan mortgage cost each month?

More than a US loan of the same size, because the rate is higher. Take a KES 14 million apartment with a 20 percent deposit, so a KES 11.2 million loan at 13 percent over 20 years: the repayment is roughly KES 131,000 a month, you pay about KES 20 million in interest, and you repay around KES 31.5 million in total, close to three times the loan. Drop the rate to a KMRC-style 9.5 percent and the monthly figure falls to about KES 104,000. Always run your own numbers on the lender’s calculator before you commit.

Can I use a SACCO to buy property in Kenya?

Yes, and many Kenyans do. A SACCO is a member-owned savings cooperative that lends to its members, often more cheaply and with gentler credit checks than a bank, typically letting you borrow around three times your savings at rates from about 1 percent a month on a reducing balance. Several run dedicated diaspora products for Kenyans abroad. You have to join and save first, you may need guarantors, and you should only use a SASRA-registered SACCO. It suits diaspora Kenyans more than non-citizen foreigners, who usually cannot join.

Final thoughts

The honest headline for a foreign buyer is that financing in Kenya usually comes down to cash or a clever loan from home, not the local mortgage. The mortgage market is small, rates are high, and a shilling loan against a dollar income adds risk you don’t need. Where a mortgage does fit — a resident foreigner who wants leverage, or a diaspora Kenyan keeping savings invested abroad — the products are there and the banks know the diaspora well. Just price the whole thing, currency risk and all, before you sign.

Whatever route you choose, the order is the same: decide how you’ll pay before you fall for a property, get real quotes in writing, and line the loan term up with the lease. Do that and the money side of buying in Kenya is calm and predictable.

A reminder, kindly meant: this is general information, not financial, tax or legal advice, and your situation may differ. Confirm current rates and rules with the lenders themselves and the Central Bank of Kenya, and take advice from a qualified adviser — especially across the US–Kenya border — before you commit.

Related reading

- Property investing in Kenya — the cluster overview this guide sits under.

- Can foreigners buy property in Kenya? — the leasehold rules that shape your loan term.

- How to buy property in Kenya — the step-by-step process and the full closing-cost stack.

- Property taxes in Kenya — stamp duty and the other levies a financed purchase still pays.

- Off-plan property in Nairobi — how developer payment plans work, and how to buy off-plan safely.

- Diaspora property investment in Kenya — the wider picture for Kenyans buying from abroad.

- Buy-to-let in Nairobi — the rental numbers if your loan is covered by rent.

- Moving to Nairobi: the complete guide — the hub for everything relocation.

Before you borrow, land softly

You don’t need to finance anything to start. The smartest buyers spend their first weeks on the ground — viewing properties, testing commutes, getting a feel for the market and the mortgage options — before they commit a shilling. A serviced apartment makes that easy: all-inclusive and furnished, with Wi-Fi, cleaning, security and a backup generator handled, so you can focus on the search.

When you’re ready, browse our serviced apartments for an honest monthly rate, or let our AI relocation assistant line up a base near the areas you’re weighing. A $50 deposit reserves your place and the balance is paid on arrival — nothing more before you travel.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.