Guides · Property investment

How to Buy Property in Kenya: A Step-by-Step 2026 Guide

How to Buy Property in Kenya: A Step-by-Step 2026 Guide

Buying a home in Kenya is more orderly than most newcomers expect. There’s a clear legal process, a set sequence of steps, and one professional — your advocate — whose whole job is to protect you through it. Get the order right and it’s calm. Skip a step to save time, and that’s where people lose money.

This guide walks you through the whole thing, start to finish: how to find a place, who to hire, the official searches that protect you, the sale agreement and deposit, the taxes, and the transfer that finally puts the title in your name. It’s written for Americans and other foreigners buying an apartment or house in Nairobi, but the process is the same countrywide.

Two things up front. First, this is general information, not legal advice — Kenyan land law is specific and the stakes are real, so hire your own advocate before you sign anything. Second, if you’re a non-citizen you can only hold land on a lease of up to 99 years, and you can’t buy farmland; we cover what that means in can foreigners buy property in Kenya. An apartment sidesteps most of it.

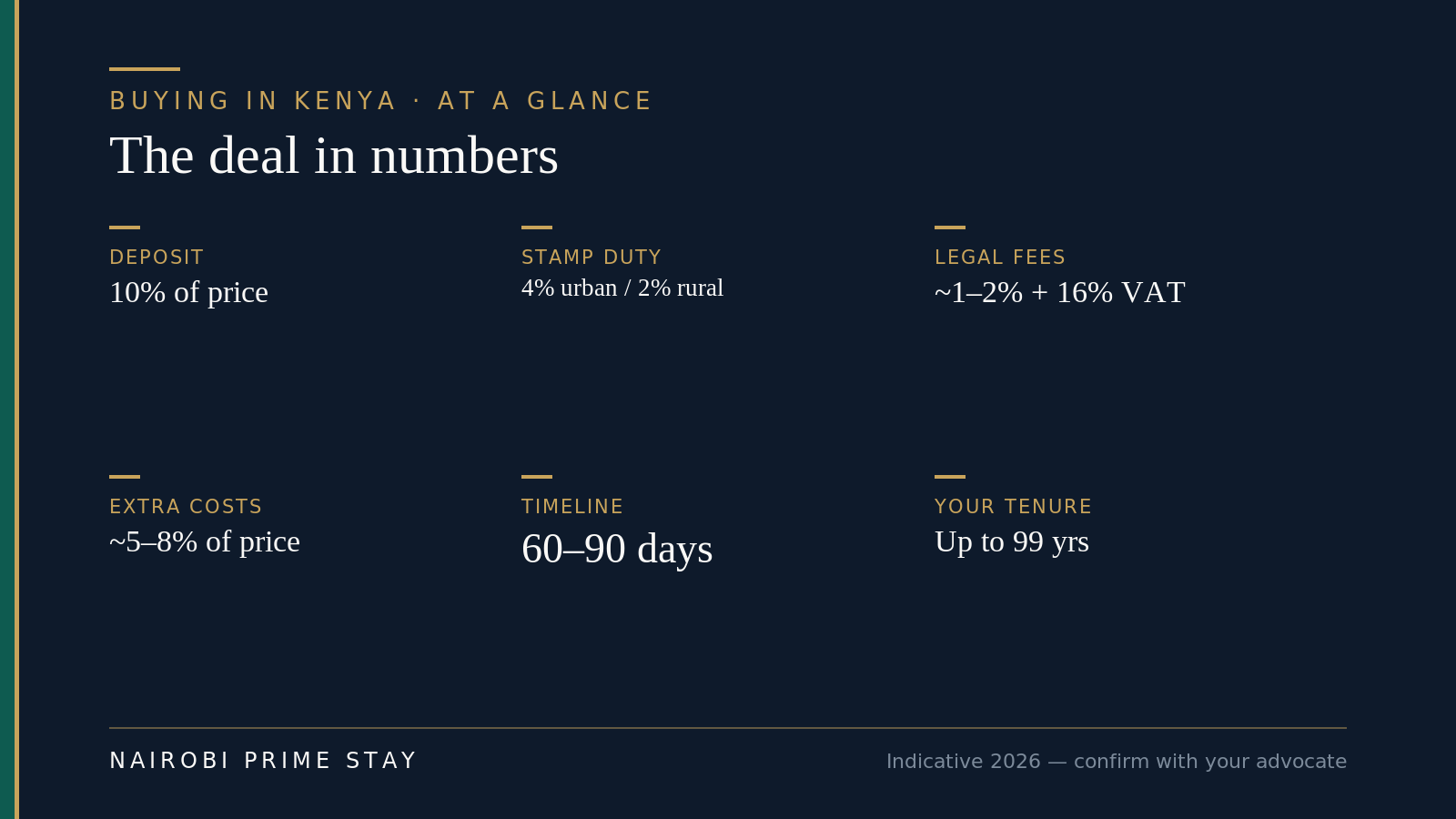

The short version (TL;DR). Buying property in Kenya runs in a set order: find the property and agree a price, get your KRA PIN, hire your own advocate, run an official title search, sign a sale agreement and pay a deposit (usually 10%, held by the advocate), complete due diligence and any consents, pay stamp duty (4% in towns, 2% rural), then lodge the transfer so a new title is issued in your name. Budget roughly 60–90 days and about 5–8% of the price in taxes and fees on top. The single most important rule: use your own advocate, and never send money for a property nobody has verified.

The whole purchase in six numbers. Everything below explains where each one comes from.

The whole purchase in six numbers. Everything below explains where each one comes from.

The whole process on one screen. Timelines stretch if consents or a leasehold transfer approval are needed — your advocate will flag that early.

The whole process on one screen. Timelines stretch if consents or a leasehold transfer approval are needed — your advocate will flag that early.

Before you start: what you’re actually buying

First, know what you can own. As a foreigner you buy on leasehold (up to 99 years), not freehold, and you can’t buy agricultural land without rare State consent. In practice that points most foreign buyers toward a city apartment on a sectional title — registered in your own name, no farmland complication, and far lighter due diligence than a plot of land. A house or land is doable, but the checks are heavier; see buying land in Kenya.

Second, most Kenyan home purchases are cash. Mortgages exist but are expensive and slow, and harder for non-residents, so the majority of expat and diaspora buyers pay in full from savings or a sale back home. Plan your funds — and the foreign-exchange transfer — early.

Third, you’ll need a KRA PIN (a Kenyan tax number) to register a property in your name. More on that in Step 2.

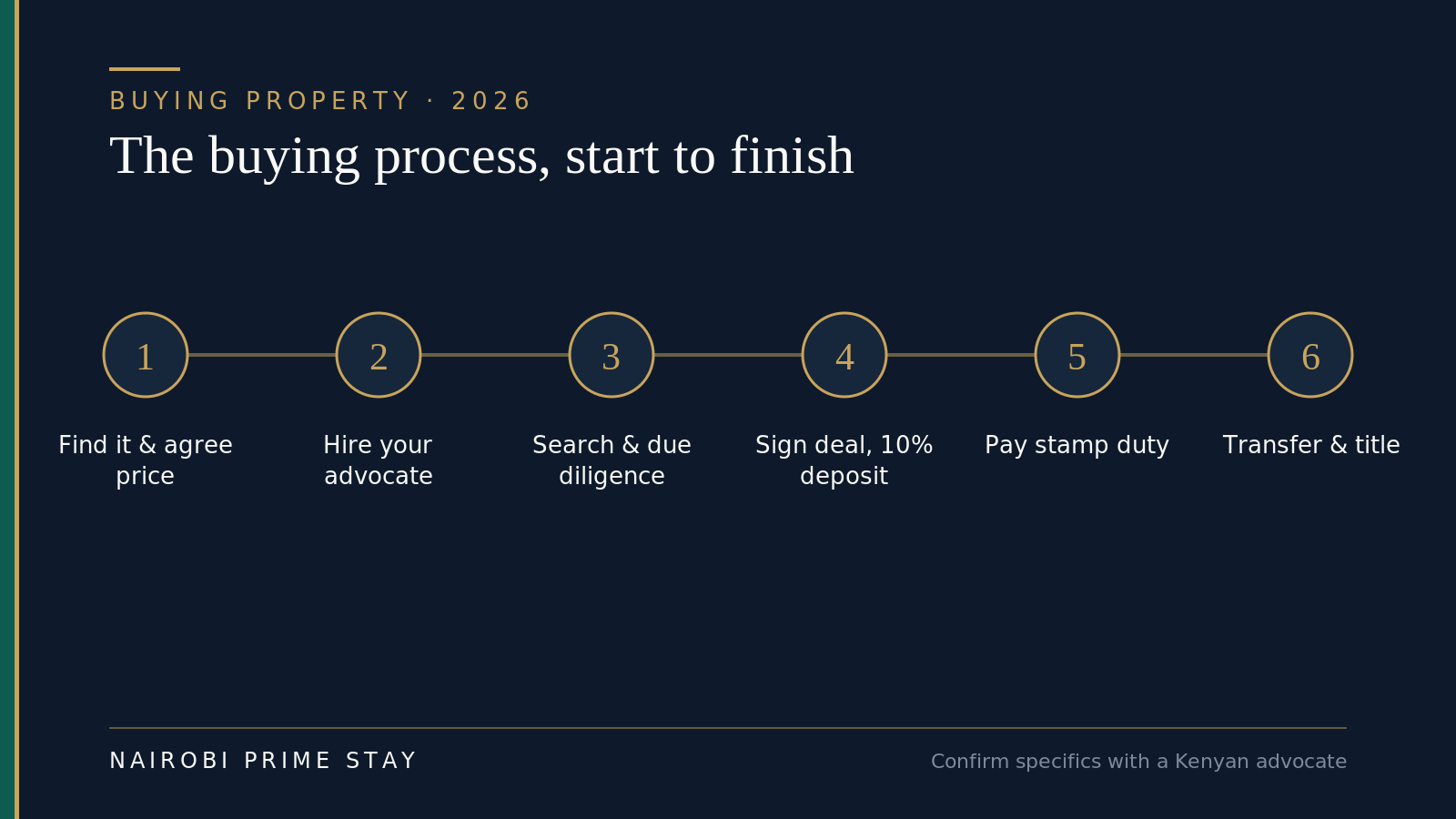

The buying process, step by step

Here’s the full sequence. Most purchases follow it in this order.

Step 1 — Find the property and agree a price

See places in person, not just online. Distances in Nairobi are short but traffic isn’t, so the same listing feels very different depending on where you’ll actually spend your days. Many buyers spend their first weeks in a serviced apartment while they view homes and learn the neighborhoods — a soft landing that beats deciding from a hotel room or, worse, from abroad.

When you find the one, you agree a price with the seller or their agent. It’s common to pay a small reservation or “commitment” fee to take the property off the market while your advocate gets involved. Keep this modest, get a receipt, and make sure it’s clearly refundable if the title doesn’t check out. Don’t pay a real deposit yet — that comes after the search, in Step 5.

Step 2 — Get your KRA PIN and the basics in order

You can’t register property in Kenya without a KRA PIN — the tax identification number issued by the Kenya Revenue Authority. Both buyer and seller need one to transfer a title. Foreigners register through the iTax portal (itax.kra.go.ke), usually with help from your advocate or a tax agent; holding a residence permit makes it straightforward, and there are routes for non-resident buyers too. Sort this early, because stamp duty is later paid under your PIN.

While you’re at it, get your funds ready. If money is coming from abroad, line up the transfer (a bank wire or a service like Wise) and keep the paper trail. Large inbound transfers are normal, but your bank may ask about the source.

Step 3 — Hire your own advocate

This is the step that protects you, so don’t skip it or share the seller’s lawyer. In Kenya a property purchase is handled by an advocate (the Kenyan term for a lawyer), and you want one acting only for you. Their job: run the official search, draft or review the sale agreement, hold your deposit safely, handle consents and completion, and lodge the transfer.

Choose an advocate who does conveyancing regularly and is in good standing with the Law Society of Kenya. Agree fees up front — they follow a regulated scale (more in Step 7 and the costs table). A good advocate earns their fee many times over by catching a bad title before your money moves. We cover their role in detail in conveyancing in Kenya.

Step 4 — Run an official title search and start due diligence

Before any real money changes hands, your advocate conducts an official search at the land registry to confirm the seller truly owns the property and that it’s free of loans, caveats or court disputes. In Nairobi this now runs through the government’s ardhisasa platform, which in 2026 became mandatory for searches, transfers, leases and charges in Nairobi (and in Kiambu, Kajiado and Mombasa) — so the registry there is fully digital. In counties not yet on ardhisasa, it’s an eCitizen or manual registry search that returns the same official certificate. A search costs only a few hundred to about a thousand shillings — the cheapest protection you’ll ever buy.

The search is the start of due diligence, not the end. Your advocate also confirms the seller’s identity against the title, checks that land rates and (for leasehold) land rent are paid up, and reviews the lease terms — crucially, how many years are left to run. For an apartment, they confirm the sectional title and the management arrangements. For land or a house, add a licensed surveyor to confirm boundaries and beacons. Take this seriously; see buying land in Kenya for the deeper checks land needs.

Step 5 — Sign the sale agreement and pay the deposit

Once the title checks out, your advocate prepares or reviews the sale agreement — the contract that sets the price, the payment schedule, the completion date and any conditions. Both sides sign, and you pay a deposit, usually 10% of the price.

Here’s the part that matters: that deposit should be held by an advocate as a stakeholder, not handed straight to the seller. It stays in the lawyer’s account until completion, which protects your money if something goes wrong before the deal closes. The agreement also sets a completion period — often 60 to 90 days — during which the balance is paid and the transfer is processed.

Step 6 — Clear consents and completion documents

With the agreement signed, the seller’s side gathers the completion documents: the original title, signed transfer forms, recent land-rate and land-rent clearance certificates, the seller’s PIN and ID, and passport photos. Your advocate checks every one.

Some properties need a consent before they can transfer. Leasehold titles often require the lessor’s (or the National Land Commission’s) consent to transfer. Land classified as agricultural needs Land Control Board consent — and as a foreigner you generally can’t buy agricultural land at all, which is another reason apartments are simpler. Your advocate identifies any consents needed and obtains them. This is often where timelines stretch, so build in slack.

Step 7 — Valuation and stamp duty

Before the title can transfer, the government assesses stamp duty — the main tax on a purchase. A government valuer (and usually your own registered valuer) values the property, and KRA assesses duty on that value or the purchase price, whichever is higher.

The rate is 4% of value for property in a town or municipality — which covers Nairobi and almost any apartment a foreigner would buy — and 2% for rural land. One thing to confirm: as counties gazette new towns and municipalities, land that once attracted 2% can move to the 4% urban rate — parts of Kiambu did exactly that — so check which rate applies to your specific property. Commercial property is higher. The buyer pays. Since February 2026, stamp duty valuation and payment have moved fully online to Ardhipay on the ardhisasa platform — physical processing is no longer accepted in the digitized counties — so you settle it by M-Pesa, bank transfer or card. You pay the balance of the purchase price around the same time. For a fuller breakdown of every levy, see property taxes in Kenya.

Step 8 — Transfer, registration and your new title

After the balance is paid and stamp duty is cleared, your advocate lodges the signed transfer and supporting documents at the land registry — on ardhisasa in Nairobi, where the transfer is now electronic end to end. The registry processes the transfer and issues a new title in your name. That registration is the moment you legally own the property — not the handshake, not the deposit, the registration.

Your advocate then does a final search to confirm the title is now in your name and clean, and hands you the registered title and the completion documents. Keep certified copies somewhere safe.

Step 9 — Handover and the first things after

On completion you get the keys and, for a house, vacant possession. A few housekeeping jobs follow: transfer the utilities and (for apartments) register with the management company, move the land-rates and service-charge accounts into your name, and if you’re renting it out, plan for rental-income tax. If you bought as an investment, our guide to property investment in Kenya covers yields, management and the tax side.

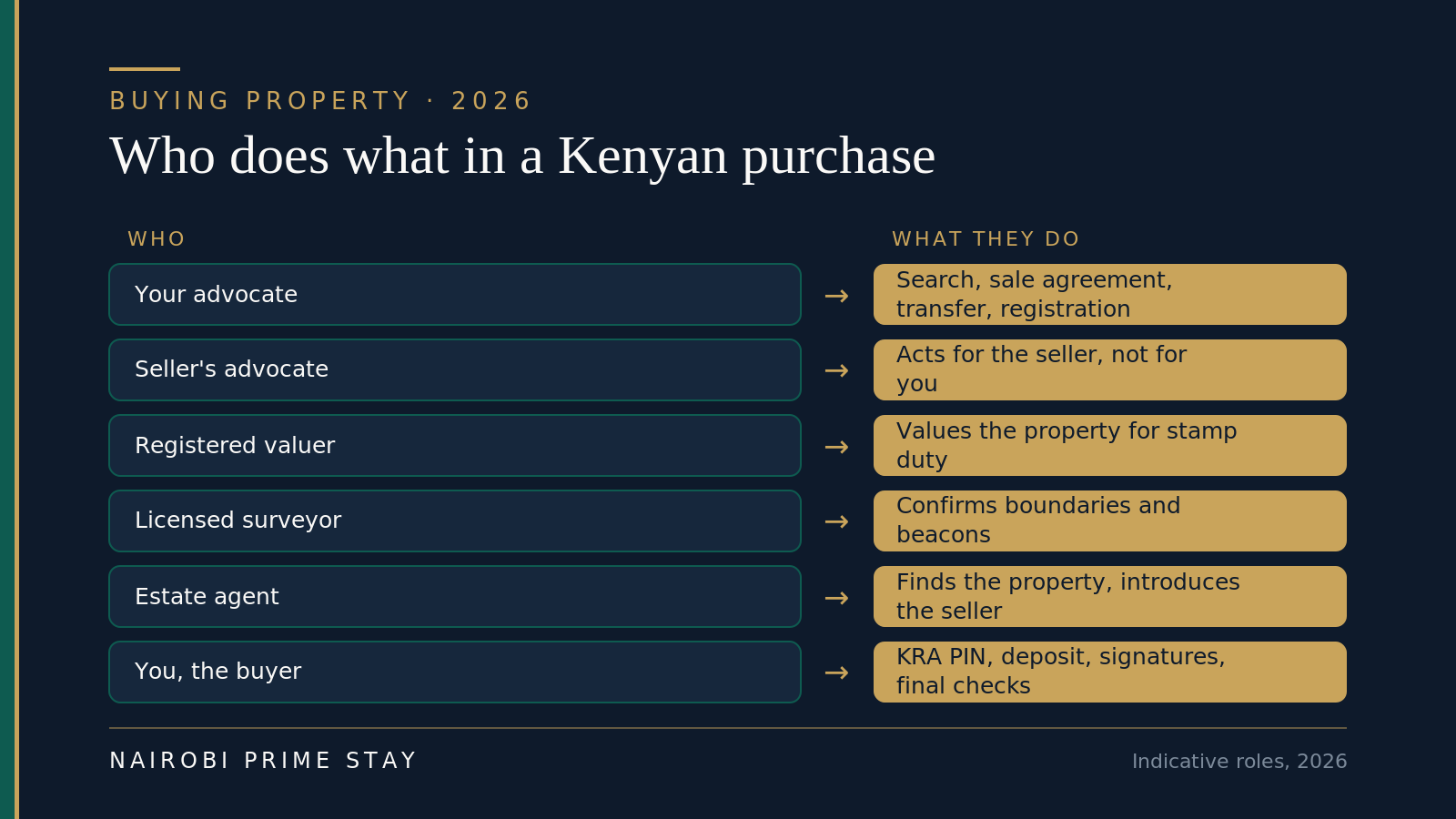

Who does what: your buying team

You won’t do this alone, and you shouldn’t. A typical purchase involves a handful of professionals, each with a clear job.

Your advocate is the one person acting solely for you. Everyone else has another master — choose your own lawyer and let them quarterback the deal.

Your advocate is the one person acting solely for you. Everyone else has another master — choose your own lawyer and let them quarterback the deal.

- Your advocate (your lawyer). The most important hire. Runs the search, drafts or reviews the agreement, holds your deposit, handles consents, lodges the transfer, and confirms your clean title at the end.

- The seller’s advocate. Acts for the seller. Perfectly normal, but never your protection — that’s why you bring your own.

- A registered valuer. Values the property so stamp duty can be assessed; a private valuation also sanity-checks the price.

- A licensed surveyor. Confirms boundaries, beacons and that the land on the ground matches the title — essential for land and houses, less so for an apartment.

- An estate agent. Finds the property and introduces the seller. Helpful, but paid by the seller, so verify everything independently.

- You. Get your KRA PIN, fund the deposit and balance, sign, and never wire money for something nobody has verified.

How long does it take?

Plan for about 60 to 90 days from agreed price to a title in your name for a clean, straightforward apartment purchase. Cash deals are faster than mortgaged ones. The clock stretches when a consent is needed, when a leasehold transfer needs the lessor’s sign-off, when rates or rent arrears have to be cleared, or when the registry is slow. Here’s a realistic timeline.

| Stage | What happens | Rough time |

|---|---|---|

| Find & reserve | View, agree price, pay a small reservation fee | Days to weeks |

| Engage advocate & search | Hire your advocate; official title search | 3–7 days |

| Sale agreement & deposit | Sign; pay ~10% to the advocate as stakeholder | 1–2 weeks |

| Due diligence & consents | Completion docs, rates/rent clearance, any consents | 2–6 weeks |

| Valuation & stamp duty | Government valuation; pay 4% (or 2% rural) duty | 1–4 weeks |

| Transfer & registration | Lodge transfer; new title issued in your name | 2–4 weeks |

These stages overlap in practice, and any single one can run long. Treat the total as two to three months, occasionally more.

What it costs (beyond the price)

Budget for the price plus roughly 5–8% in taxes and fees. The big line is stamp duty; the rest are smaller but add up.

Indicative 2026 costs on top of the purchase price. Confirm current figures with your advocate and the property-taxes guide.

Indicative 2026 costs on top of the purchase price. Confirm current figures with your advocate and the property-taxes guide.

| Cost | Who / what | Indicative (2026) |

|---|---|---|

| Stamp duty | Government tax on transfer (buyer pays) | 4% urban / 2% rural of value |

| Legal fees | Your advocate (regulated scale) | ~1.5% on the first KES 2.5M, less above, + 16% VAT |

| Official search | Land registry / ardhisasa | ~KES 500–1,000 per search |

| Valuation | Registered valuer (for duty + sanity check) | From ~KES 10,000 |

| Registration & misc | Registry fees, bank charges, courier | Small fixed fees |

| Reservation / commitment | To hold the property pre-search | Modest — keep it refundable |

Legal fees follow the Advocates Remuneration Order, a published scale — roughly 1.5% on the first KES 2.5 million of value and lower percentages above that, plus 16% VAT. Ask your advocate for a written quote against the scale before you instruct them. For the full tax picture — stamp duty, land rates, capital gains and rental-income tax — see property taxes in Kenya.

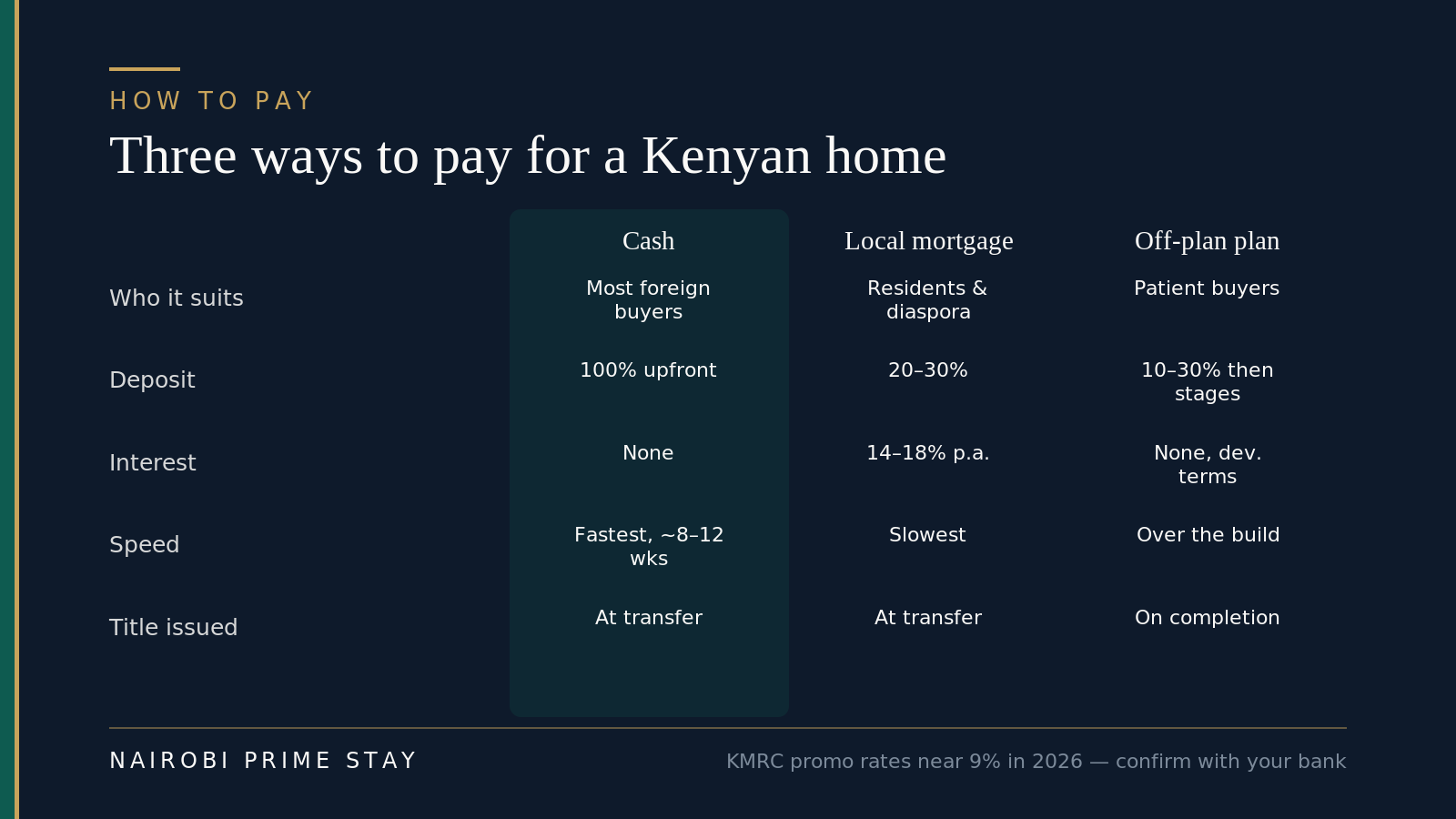

Paying cash or taking a mortgage?

Most foreign buyers pay cash. It’s the norm in Kenya, it’s faster, and it sidesteps the cost of borrowing locally. If you’re selling a home back in the US or moving savings across, plan to buy outright.

A mortgage is possible, but go in with open eyes. Kenyan home loans are expensive by American standards — most banks charge roughly 14–18% a year in 2026, though promotional rates backed by the Kenya Mortgage Refinance Company (KMRC) have dipped toward 9% at lenders like KCB and Stanbic. Several banks — KCB, Stanbic, Co-operative Bank, Absa and Standard Chartered — run dedicated diaspora mortgage products you can apply for from abroad using foreign income. Expect to put down more than a resident would, usually 20–30%, and remember the loan is advanced in shillings, so you carry some currency risk. A local mortgage also slows the purchase, because the bank runs its own valuation and registers a charge over the title before releasing funds.

Three common ways to fund a Kenyan home. Cash is simplest; a local mortgage is dearer and slower; off-plan lets you pay in stages as the building goes up.

Three common ways to fund a Kenyan home. Cash is simplest; a local mortgage is dearer and slower; off-plan lets you pay in stages as the building goes up.

For which banks lend to non-residents, what they ask for and how the numbers actually work, see property financing and mortgages in Kenya. Diaspora buyers should also read diaspora property investment in Kenya.

Buying ready or off-plan?

You’re choosing between two things: a finished home you can transfer now, or an off-plan unit you buy during construction and pay for in installments. This guide describes the ready, resale path — agree a price, search the title, transfer it into your name. Off-plan works differently. You sign with a developer, pay a deposit and then stage payments tied to construction milestones, and the title is issued to you only once the project is complete and the units are sub-divided.

Off-plan can be cheaper and lets you spread payments, but it carries completion risk — the building has to actually finish, on time and to spec. So the due diligence shifts from “does this person own this title?” to “will this developer deliver?” You check the developer’s track record, the title the project sits on, the approvals, and what the contract gives you if they run late. First-time foreign buyers often prefer a ready apartment for the certainty. If off-plan is your route, read buying off-plan property in Nairobi before you pay a shilling.

Getting your money into Kenya

Move the bulk of your money by transfer, not in a suitcase. A bank wire or a service like Wise lands your funds in a Kenyan account with a clean paper trail, which is exactly what your advocate and the banks want to see. Cash works for small sums, but you must declare cash or monetary instruments over USD 10,000 (or the equivalent) to customs on the way in — and on the way out — or risk seizure and a fine.

The clean way to fund a purchase from abroad. Keep every confirmation — banks ask about the source of large inbound transfers, and that’s normal.

The clean way to fund a purchase from abroad. Keep every confirmation — banks ask about the source of large inbound transfers, and that’s normal.

A few practical points. Pay the deposit and balance into your advocate’s account, not the seller’s. Watch the exchange rate — the shilling traded around 129–130 to the dollar in mid-2026 — and time larger transfers when you can. The good news for investors and retirees: Kenya has no exchange controls, so once you own the property you can convert shillings back to dollars and send rental income or sale proceeds home, paying only the conversion spread. For the mechanics, see our USD–KES currency guide and sending money to Kenya.

The buyer’s checklist

Work through these and you’ll avoid almost every common problem:

- Decide leasehold apartment vs house or land, and confirm what you (as a foreigner) can legally own.

- See the property in person; don’t decide from photos or from abroad.

- Register your KRA PIN before you reach completion.

- Line up your funds and the foreign-exchange transfer early.

- Hire your own advocate — never share the seller’s.

- Get an official title search done before paying a real deposit.

- Confirm the seller’s identity matches the title exactly.

- For leasehold, check how many years are left to run, and that ground rent and rates are clear.

- Pay the deposit into the advocate’s account as stakeholder, not to the seller direct.

- Confirm any required consents (lessor / Land Control Board) before completion.

- Pay stamp duty and the balance, then make sure the transfer is registered.

- Get a final search confirming the clean title is now in your name.

How it plays out: a Nairobi apartment

Say you’re an American buying a two-bed apartment in Kilimani for KES 18 million (about $139,000 at mid-2026 rates). You spend your first month in a serviced apartment, view a dozen places, and settle on one. You pay a small reservation fee, get a receipt, and instruct an advocate who does conveyancing weekly.

Her official search comes back clean: the seller’s name matches the sectional title, no caveats, rates paid. You sign the sale agreement and move a 10% deposit (KES 1.8 million) into her account, not the seller’s. Over the next six weeks she gathers the completion documents, confirms the management and service-charge position, and arranges valuation. Stamp duty at 4% comes to KES 720,000; legal fees and the search add roughly KES 280,000 plus VAT. You pay the balance, she lodges the transfer, and about ten weeks after you agreed the price, the registry issues a title in your name. Total over the price: a little under 6%.

That’s the whole game — slow, verified and uneventful, which is exactly how a property purchase should feel.

Common mistakes to avoid

Almost every horror story traces back to a shortcut. Here are the ones that cost people real money — and for the wider catalog of cons, from double-sold plots to forged titles and grabbed land, see property scams in Kenya.

The pattern behind nearly every Kenyan property loss: someone skipped a check to move faster. Don’t.

The pattern behind nearly every Kenyan property loss: someone skipped a check to move faster. Don’t.

- Using the seller’s advocate. They act for the seller. You need someone whose only duty is to you.

- Wiring money for an unseen property. Never send funds for a place you or your advocate haven’t physically verified.

- Skipping the official search. A few hundred shillings confirms ownership and surfaces loans or disputes. There’s no excuse to skip it.

- Trusting a nominee instead of a title. “Put it in a friend’s name” or “we’ll arrange freehold for you” are how foreigners lose money. Own a real title in your own name.

- Ignoring arrears. Unpaid land rates or land rent can block a transfer or follow the property to you. Confirm the clearance certificates.

- Forgetting the lease term. A 99-year lease with 40 years left is a very different asset. Always check the unexpired term, not the original grant.

Frequently asked questions

How do I buy property in Kenya as a foreigner?

You follow a set process: find the property and agree a price, get a KRA PIN, hire your own advocate, run an official title search, sign a sale agreement and pay a deposit (usually 10%), clear due diligence and any consents, pay stamp duty, then lodge the transfer so a new title is issued in your name. As a non-citizen you buy on leasehold of up to 99 years, not freehold, and an apartment on a sectional title is the simplest route. Always use your own advocate and never pay for a property nobody has verified.

How long does it take to buy property in Kenya?

Plan for about 60 to 90 days from agreed price to a registered title for a clean, cash apartment purchase. It’s faster without a mortgage and slower if a consent is required, a leasehold transfer needs the lessor’s approval, or rates and rent arrears must be cleared. Treat two to three months as normal and build in slack.

Do I need a lawyer to buy property in Kenya?

Yes, in practice. A property purchase is handled by an advocate who runs the official search, drafts or reviews the sale agreement, holds your deposit, manages consents and lodges the transfer. Hire your own advocate who acts only for you, and never share the seller’s. Their fee follows a regulated scale and is the best protection money you’ll spend.

What is stamp duty when buying property in Kenya?

Stamp duty is the government tax on transferring a property, paid by the buyer. It’s 4% of the value for property in a town or municipality, which covers Nairobi and most apartments, and 2% for rural land; commercial property is higher. It’s charged on the government-assessed value or the price, whichever is higher, and paid through the KRA and eCitizen system before the title can transfer.

Do I need a KRA PIN to buy property in Kenya?

Yes. You can’t register a property in your name without a KRA PIN, the Kenyan tax number from the Kenya Revenue Authority. Both buyer and seller need one. Foreigners register through the iTax portal, usually with help from an advocate or tax agent, and you should sort it early because stamp duty is paid under your PIN.

Can I buy property in Kenya from abroad without visiting?

It’s possible, and many diaspora buyers purchase through an advocate, sometimes using a power of attorney, but it raises the risk, so verify everything. Insist on an official title search, confirm the seller’s identity, and have someone you trust inspect the property. Never wire money for a place you or your advocate haven’t checked, and hold the deposit in the advocate’s account. Visiting first, even briefly, is far safer.

What is an official land search and why does it matter?

An official search is a check at the land registry that confirms who really owns a property and whether it carries loans, caveats or disputes. In Nairobi it’s done through the ardhisasa platform; elsewhere via eCitizen or a manual registry search. It costs only a few hundred to about a thousand shillings and should be done before you pay any real deposit. It’s the cheapest protection in the whole process.

How much deposit do I pay when buying property in Kenya?

Usually 10% of the purchase price, paid when you sign the sale agreement. Crucially, it should be held by an advocate as a stakeholder, sitting in the lawyer’s account until completion, not handed to the seller. That protects your money if the deal falls through. You pay the balance during the completion period, often 60 to 90 days.

What does it cost to buy property in Kenya beyond the price?

Budget roughly 5 to 8% of the price in taxes and fees. The big one is stamp duty (4% in towns, 2% rural). On top sit legal fees (about 1.5% on the first KES 2.5 million plus 16% VAT, on a regulated scale), an official search (a few hundred to about KES 1,000), a valuation (from around KES 10,000), and small registration and bank charges. See the property taxes guide for the full picture.

Can I get a mortgage to buy property in Kenya as a foreigner?

Yes, but most foreign buyers pay cash, because local mortgages are expensive and slower. In 2026, Kenyan home-loan rates run about 14–18% a year, with promotional KMRC-backed rates dipping toward 9% at some banks. Several banks — KCB, Stanbic, Co-operative, Absa and Standard Chartered — offer diaspora mortgages you can apply for from abroad, but expect a 20–30% deposit, the loan advanced in shillings, and extra time while the bank values the property and registers its charge. See our property financing guide for the details.

Should I buy a ready apartment or off-plan in Kenya?

A ready (resale) home transfers into your name now, so your main job is verifying the seller’s title — the process in this guide. Off-plan means buying during construction and paying in installments, with the title issued only when the project is complete. Off-plan can be cheaper and easier to fund, but it carries completion risk, so the due diligence shifts to the developer’s track record, approvals and contract. First-time foreign buyers often prefer a ready apartment for the certainty.

Final thoughts

Buying property in Kenya isn’t risky because the country is risky — it’s risky only if you skip the steps that exist to protect you. Follow the order: see it, search it, sign with your own advocate, pay through their account, clear the taxes, register the transfer. Do that and the worst case is that a search turns something up and you walk away a few thousand shillings poorer but a fortune wiser. The buyers who get hurt are the ones who rushed. Go at the pace of the paperwork, and Kenya is a calm place to own a home.

Related reading

- Property investment in Kenya: the complete guide — the hub for buying, investing, yields and taxes.

- Can foreigners buy property in Kenya? — what you’re legally allowed to own.

- Conveyancing in Kenya — what your advocate actually does, and the fees.

- Property taxes in Kenya — stamp duty, land rates, CGT and rental tax.

- Buying land in Kenya — the heavier due diligence land demands.

- Title deeds in Kenya explained — freehold, leasehold and sectional title.

- Property financing and mortgages in Kenya — rates, deposits and diaspora home loans.

- Buying off-plan property in Nairobi — paying in stages, and the completion risk.

- Property scams in Kenya — the cons to know, and how to steer clear.

- Moving to Nairobi: the complete guide — the life side of the move.

Buy with a soft landing

You don’t have to choose a home in a hurry. A serviced apartment for your first month gives you a secure, fully furnished base — Wi-Fi, cleaning, backup generator and security included — while you view properties, meet your advocate and get to know the neighborhoods before you commit a single shilling. Browse our serviced apartments, or let our AI relocation assistant line up options for your budget and timeline in a couple of minutes. A $50 deposit reserves your place and the balance is due on arrival — nothing more before you travel.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.