Guides · Property investment

Buying Off-Plan Property in Nairobi: The Honest 2026 Guide

Buying Off-Plan Property in Nairobi: The Honest 2026 Guide

Off-plan means buying an apartment before it’s built. You pay against the architect’s drawings and a show unit, often two or three years before you get the keys. In Nairobi, it’s how a large share of new apartments are sold. The pitch is simple: pay less now, spread the cost while you wait, and move into a home worth more than you paid.

Sometimes that’s exactly how it goes. Other times the crane stops turning, the WhatsApp updates dry up, and the deposit you wired is gone. Both stories are true in Nairobi, and the difference is rarely luck. It’s due diligence.

This is the honest version. What off-plan actually gets you, what it really costs, the risks the sales suite skips, and the handful of contract terms and checks that separate a good buy from a cautionary tale. It’s written for Americans and diaspora buyers who can’t drop by the site on a Saturday.

TL;DR — buying off-plan in Nairobi (2026)

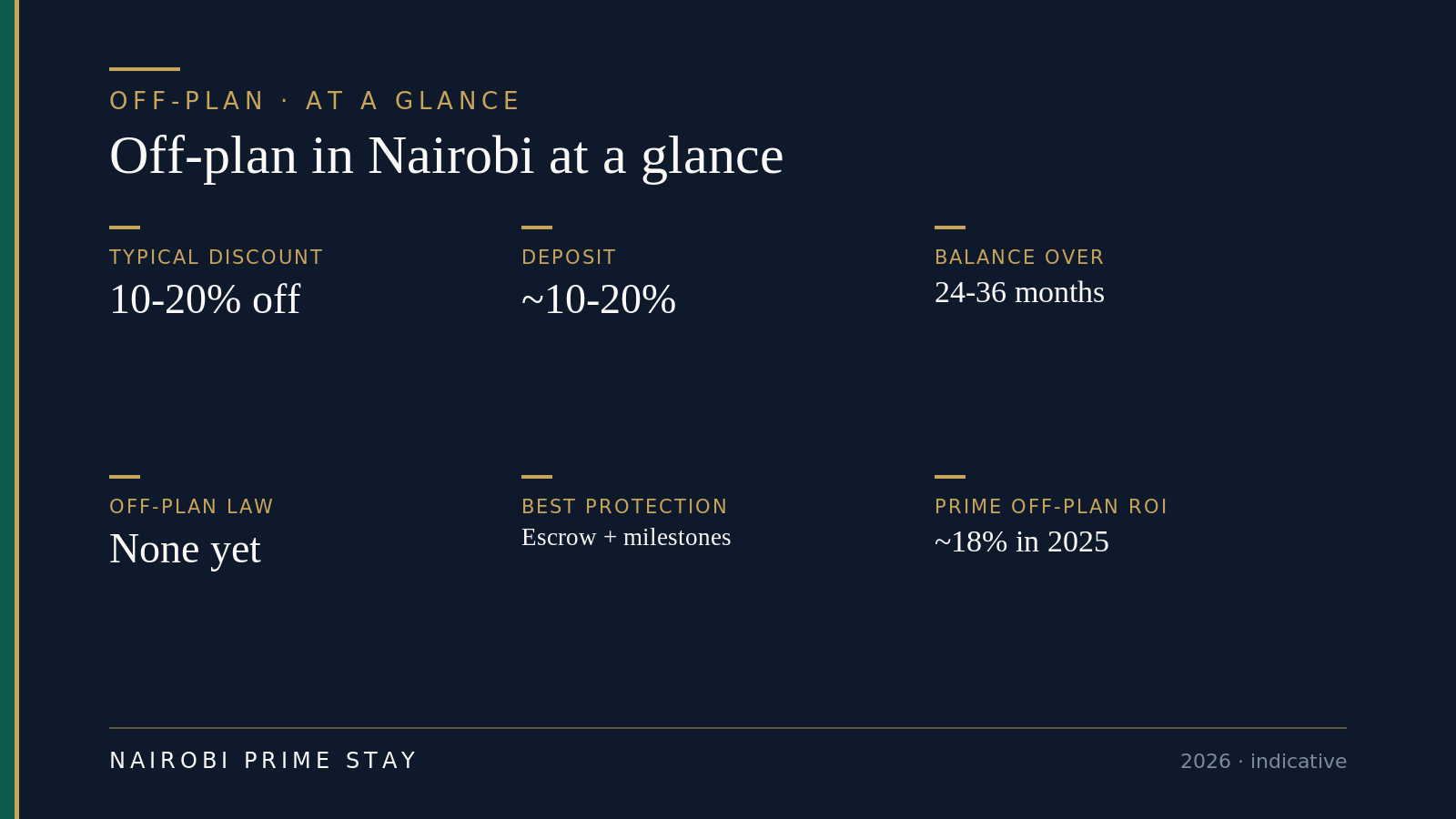

- Off-plan = buying before or during construction, off the plans. You usually pay a deposit of about 10–20%, then the balance in installments over the 24–36 months it takes to build.

- The upside is real. Off-plan units often sell 10–20% below a finished equivalent, the payment plan needs no mortgage, and a good project can appreciate before you move in. HassConsult’s eight tracked prime off-plan schemes averaged about 18% (18.06%) returns in 2025.

- The downside is also real. Delays, spec changes, developer insolvency and outright fraud. Kenya has no dedicated off-plan law, so your protection lives entirely in the contract you sign.

- Vet the developer harder than the apartment. Check NCA registration, county and NEMA approvals, a clean title on Ardhisasa, and — above all — finished projects you can walk through today.

- Insist on escrow. Payments held in a stakeholder account and released on construction milestones, a firm completion date with a real penalty, and a refund clause. Use your own independent lawyer, never the developer’s.

- Foreigners can buy off-plan apartments on sectional (leasehold) title. If you can’t stomach delay risk or oversee from afar, a ready unit — or renting first — may suit you better.

Why this matters

Off-plan is where the cheapest entry prices and the biggest losses both live. Get it right and you buy below market with a payment plan a bank would never give you. Get it wrong and you join the Kenyans — thousands of them — who paid deposits for homes that never arrived.

The stakes are higher if you’re buying from abroad. You can’t drop by to see whether the foundation is really poured. You’re wiring money across borders, often dollars into a shilling project, on the strength of renders and a sales agent’s reassurance. That’s exactly the buyer fraudsters look for. The good news: the checks that protect you are knowable, and most disasters were avoidable.

What “off-plan” actually means

Off-plan property is a home you buy before it’s finished — sometimes before the ground is broken. Instead of viewing a real apartment, you’re buying off floor plans, a specifications sheet, renders and maybe a show unit. You commit early, pay in stages as construction proceeds, and take possession on completion, often two to three years later.

It’s different from buying a ready, completed unit, where you see the actual apartment, pay in full or with a mortgage, and move in within weeks. It’s also different from building your own house, where you own the land and run the project. With off-plan you’re buying a finished product on a promise, funding the developer’s build as you go. (If you want the full purchase process either way, start with how to buy property in Kenya.)

Here’s why developers sell this way: pre-sales fund construction. Your installments are often the cash that pours the slab. That’s the whole model — and the whole risk. You become an early financier of a building that doesn’t exist yet, with far less protection than a bank would demand for the same role.

The upside: why people buy off-plan

Off-plan in Nairobi at a glance, 2026. Figures are indicative; verify the discount and terms on your specific project.

Off-plan in Nairobi at a glance, 2026. Figures are indicative; verify the discount and terms on your specific project.

The price is lower. Off-plan units commonly list 10–20% below a comparable finished apartment, and in a rising market the gap to completion value can be wider. Developers discount early to build momentum and raise capital.

The payment plan is the real draw. You reserve with a deposit — often around 20%, sometimes as low as 10% — then pay the balance in installments across the build, with no bank and no 14–18% mortgage interest. For a diaspora buyer with steady income but no Kenyan credit history, that’s frequently the only realistic path into a new-build. (See financing and mortgages in Kenya for the alternatives.)

There’s appreciation potential. Buy early in a well-located, well-run project and the unit can be worth meaningfully more by handover. HassConsult, which tracks the market, found its sample of eight prime off-plan developments returned about 18% (18.06%) in 2025 — evidence the model still works when the project does.

You get new, and you get choice. First buyers pick the best units — floor, view, aspect — and move into a brand-new apartment under warranty, with modern layouts and amenities.

One honest caveat ties all of these together: every upside assumes the project completes on time and to spec. None of them survives a stalled build. The discount is compensation for the risk you’re taking on, not a free lunch.

How the payment plan works

The off-plan payment journey. Terms vary by developer — get yours in writing.

The off-plan payment journey. Terms vary by developer — get yours in writing.

The mechanics are fairly standard across Nairobi developers, though the details vary. Get yours in writing.

- Reserve. You pay a booking fee to take a specific unit off the market while paperwork is drawn up. Make sure it’s documented and, ideally, refundable within a short window.

- Deposit. On signing the sale agreement you pay the deposit — commonly 10–20% of the price. This should sit in a stakeholder or escrow account, not the developer’s spending account.

- Sign the sale agreement. Your own advocate reviews and signs on your behalf. This document governs everything: price, schedule, and what happens if either side defaults. (This is core conveyancing work.)

- Milestone installments. You pay the balance in tranches tied to construction stages — foundation, slab, walls, roofing, finishes. Linking money to verified progress is your single best protection. Avoid plans that demand fixed monthly sums regardless of whether anything is being built.

- Completion and snagging. When the unit is finished you inspect it — a “snagging” walk-through — list the defects, and the developer fixes them. A defects liability period, usually around six months, keeps them on the hook after handover.

- Title transfer. You pay stamp duty (4% in Nairobi) and the final balance, and the unit’s sectional title transfers into your name. For apartments, individual titles flow from the Sectional Properties Act 2020 — confirm the developer is set up to deliver one. (More in title deeds explained.)

The pattern to insist on: money follows progress, not the calendar. If installments fall due on fixed dates no matter what’s built, you’re financing the developer with none of a bank’s safeguards.

A worked payment plan: a KES 12M off-plan two-bed

Numbers make it concrete. Say you reserve a KES 12 million two-bedroom off-plan, roughly 10–20% below a finished comparable at about KES 14–15 million.

A KES 12M off-plan two-bed, in round numbers. Illustrative only — your project’s price and terms will differ.

A KES 12M off-plan two-bed, in round numbers. Illustrative only — your project’s price and terms will differ.

You put down about KES 2.4 million (20%), ideally into an escrow account. The remaining KES 9.6 million is spread across the roughly 30-month build, each installment tied to a milestone — foundation, slab, walls, roof, finishes. On completion you pay stamp duty of 4% (about KES 480,000 in Nairobi) plus legal fees, and the sectional title transfers to you. If the market cooperates the finished unit is worth KES 14–15 million or more; if it doesn’t, that gap can shrink or vanish. Run the numbers on your own project, and price in the currency swing if you’re paying in dollars.

The real risks (the part the sales suite skips)

Off-plan’s risks are not hypothetical in Nairobi. Know them before you wire anything.

Delays. The most common problem by far. A “12-month” build runs 24; a 24-month build runs 40, or stops. You carry the cost of waiting — rent elsewhere, capital tied up, plans on hold. Build delay into both your expectations and your contract.

Stalled or abandoned projects. Worse than slow is never. Developers run out of money, mismanage pre-sale funds, or fold, and half-built blocks sit for years. Your installments may already be spent.

Spec downgrades. The finished unit doesn’t match the render. Cheaper finishes, smaller rooms, a clubhouse that never appears, a different layout. Without a detailed specification annexed to the contract, an “artist’s impression” is all you’re owed.

Developer insolvency or fraud. At the dark end, the company collapses — or it was a scam from the start. Money paid into a personal or company account, with no escrow, is extremely hard to recover. Kenya has seen high-profile cases where hundreds of buyers lost their deposits. (See property scams in Kenya.)

No dedicated off-plan law. This is the structural problem. Kenya has no specific legislation governing off-plan sales. You rely on general land law and the Law of Contract Act, and standard developer contracts tend to favor the developer. Legal commentators have openly called for an escrow law to protect buyers; until one exists, your protection is only as strong as the contract you negotiate. Reform has been floated: a Real Estate Regulation Bill would license developers under a new regulatory authority, register every project on a public platform, and force buyer funds into project-specific escrow accounts — some drafts, modeled on Dubai’s law, would ring-fence the bulk of sale proceeds. As of 2026 none of it is enacted, so don’t count on it; negotiate escrow into your own contract.

Market risk. Prices can fall while you wait. Nairobi’s apartment segment is oversupplied: As of HassConsult’s Q1 2026 index (released April 2026), the apartment market was soft and clearly split by area — a few suburbs edged up (Muthangari about 3.8%, Riverside 1.8%) while premium apartment corridors like Westlands and Upper Hill fell about 2.8% and 2.5% in the quarter, and satellite towns slipped 0.9% overall. The appreciation you were promised isn’t guaranteed — in the wrong corridor, the unit can be worth less at handover than you agreed to pay. (For the full picture, see Nairobi property prices.)

Off-plan projects that stalled: honest stories

Names matter here, because they’re a warning the brochures won’t give you.

Suraya Property Group, once a prominent Nairobi developer, faced lawsuits from buyers over stalled and undelivered units. Banda Homes left buyers at developments like Oak Park Estate (Kenyatta Road) and Maple Ridge Estate (Kikuyu) waiting for homes promised in roughly 12 months that remained incomplete years later, with final deposits long paid. And a company marketing cheap off-plan houses under the “Simple Homes” name took deposits from hundreds of buyers and turned out to be a scam.

The thread running through all of them: buyers paid up front, into projects they couldn’t verify, under contracts and structures that gave them little recourse when things went wrong. None of this means off-plan is a trap. It means the gap between an 18% return and a total loss is the homework you do before you pay. The next sections are that homework.

If the crane stops: what recourse you actually have

Here’s the part most guides skip: if your project stalls, getting your money back is slow, costly and often only partial. Plan as if the contract is your only real protection, because in Kenya today it mostly is.

What recourse looks like if a project stalls. The earlier protections — escrow, milestones, a refund clause — are worth far more than any of these.

What recourse looks like if a project stalls. The earlier protections — escrow, milestones, a refund clause — are worth far more than any of these.

If a build stops, the path usually runs like this. Your advocate sends a formal demand letter citing the contract. You try to negotiate — a revised schedule, a partial refund, a swap to another unit. Buyers often band together into an association to share legal costs and press the developer; the well-known Kenyan cases, from Suraya to Banda Homes, were fought this way. From there it’s a civil claim, and if the developer is insolvent you join the queue of creditors — usually an unsecured one, behind the banks, recovering cents on the shilling if anything.

That’s why the protections earlier in this guide matter so much. Money held in escrow and released on milestones can’t be quietly spent on another project. A long-stop completion date with a refund clause gives you a clean exit. An independent advocate catches the weak contract before you sign it. None of these help once the money has gone into a personal account — they only work if you insist on them before you pay. If a developer won’t agree to them, that refusal is your answer.

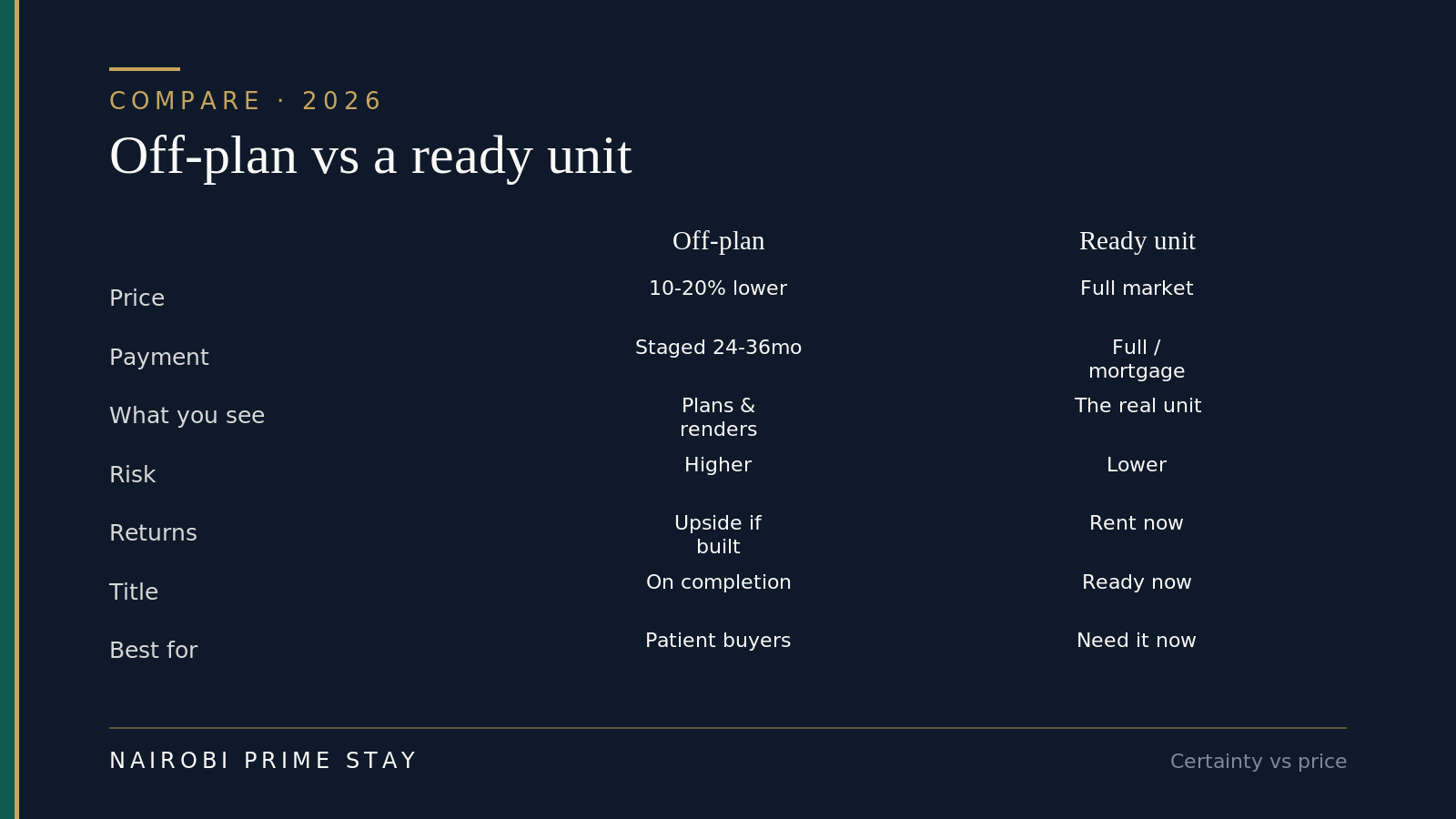

Off-plan vs a ready unit: the honest trade-off

Off-plan trades certainty for price and a payment plan. Which side fits depends on your timeline and risk appetite.

Off-plan trades certainty for price and a payment plan. Which side fits depends on your timeline and risk appetite.

| Off-plan | Ready (completed) unit | |

|---|---|---|

| Price | ~10–20% below finished value | Full market price |

| Payment | Staged over 24–36 months, no mortgage | Full payment or mortgage up front |

| What you see | Plans, renders, a show unit | The actual apartment |

| Risk | Higher — delay, spec, completion | Lower — it exists, you inspect it |

| Return profile | Appreciation upside if it completes well | Immediate rent or use |

| Title | Issues on completion (confirm sectional title) | Usually ready to transfer now |

| Best for | Patient buyers who can oversee and wait | Buyers who need a home or certainty now |

The honest summary: off-plan trades certainty for price and a payment plan. If the discount and the installments are what make the purchase possible, and you can wait and verify, off-plan can be the smart buy. If you need a home now, can’t monitor the build, or can’t afford to have capital stuck in a stalled project, a ready unit is the calmer choice — and in today’s soft apartment market, there are plenty to choose from.

How to vet a developer and project

This is where you earn the discount. Spend more time on the developer than on the apartment.

Walk their finished projects. The single best test. A real developer has completed buildings you can visit, with residents you can ask: was it on time? On spec? Any problems since? If the whole portfolio is “coming soon,” that’s a red flag.

Check registrations and approvals. The developer and contractor should be registered with the National Construction Authority (NCA). The project needs county government approval of plans, NEMA environmental approval, and zoning compliance. Ask for the documents. Don’t accept “it’s all in order” on faith.

Verify the land title. Run an official search on Ardhisasa, the Ministry of Lands portal that is live for Nairobi, to confirm the developer actually owns the land, the tenure, and that there are no caveats or charges that could swallow the project. (Our guides to buying land in Kenya and title deeds walk through searches.)

Probe the finances. Pre-sales fund the build, so a project that isn’t selling can stall. Ask how many units are sold, whether construction is funded beyond your installments, and who the financing bank is. A bank-financed project has had a second set of professional eyes on it.

Confirm the sectional title path. For apartments, your eventual title comes through the Sectional Properties Act 2020 — the developer must survey sectional plans, register them, and constitute a management company before unit titles can issue. Ask exactly how and when you get your title. “We’ll sort it out later” has stranded many buyers on old share certificates.

Use your own lawyer. Not the developer’s, and not the one the agent recommends. An independent advocate reviews the contract, runs the searches, and represents only you. It’s the cheapest insurance in the whole transaction. (This is what good conveyancing buys you.)

What to put in the contract

A strong off-plan contract is your real protection. Push for these terms — and be ready to walk if a developer refuses them.

Escrow / stakeholder account. Your money goes into an independently held account and is released to the developer only as verified milestones are met. A developer who resists escrow is asking you to trust them with unprotected cash. Escrow isn’t yet legally required in Kenya, so you have to negotiate it in.

Milestone-linked payments. Each installment tied to a specific, verifiable construction stage — not a calendar date. No progress, no payment.

A firm completion date with a real penalty. Not “within a reasonable time.” A dated handover with liquidated damages — a genuine financial penalty — if the developer is late, plus your right to exit and be refunded after a defined grace period.

A detailed specification. The finishes, sizes, materials and amenities annexed in writing, so “not as rendered” becomes a breach, not just a disappointment.

A defects liability period. Typically about six months after handover, during which the developer fixes structural and finishing faults at their own cost.

A refund clause. Clear terms for getting your money back, with interest where possible, if the project stalls, the developer defaults, or completion blows past a long-stop date.

Sectional title obligation. The developer’s written commitment to deliver a clean sectional title in your name, with the timeline and a breakdown of who pays what.

A note for American and diaspora buyers

A few realities specific to buying off-plan from the US.

You can own it. Foreigners can buy off-plan apartments on sectional title, which is leasehold for 99 years — the standard, fully legal route. You can’t buy freehold or agricultural land, but apartments aren’t affected. (See can foreigners buy property in Kenya?)

Remote oversight is the hard part. You can’t inspect the slab yourself. Appoint someone you trust — your advocate, a hired project monitor, or a relative — to do site visits and verify each milestone before a payment releases. Don’t pay on the strength of photos a sales team sends you.

Mind the currency. If you earn dollars and pay for a shilling-priced unit in installments, the exchange rate moves under you. The shilling has traded around 130 to the dollar in mid-2026 after a volatile couple of years; budget for swings, and confirm the live rate before each transfer. (See our USD/KES currency guide.)

You’re a target. Diaspora buyers are prime marks for off-plan scams — far away, eager, paying remotely. Slow down. Verify the developer’s bank account by phone using independently sourced numbers, never wire to a personal account, and treat any “pay today for this price” pressure as a reason to walk. (More in property scams in Kenya.)

Paying from the US: money, currency and the tax you’ll owe

Buying off-plan from abroad adds a money layer the brochure won’t mention. Get it clear before the first transfer.

Getting the money in is easy; timing it isn’t. Kenya has no exchange controls, so you can wire dollars in and later send rent or sale proceeds back out freely. Move money through a bank or a licensed remitter, keep every receipt for your KRA and IRS records, and declare cash over USD 10,000 at the border. Because you pay a shilling-priced unit in installments over two or three years, the exchange rate is a moving target — the shilling sat near 130 to the dollar in mid-2026 after a rocky stretch. A unit that pencils out at today’s rate can cost more, or less, in dollars by the final installment. (See sending money to Kenya and our USD/KES currency guide.)

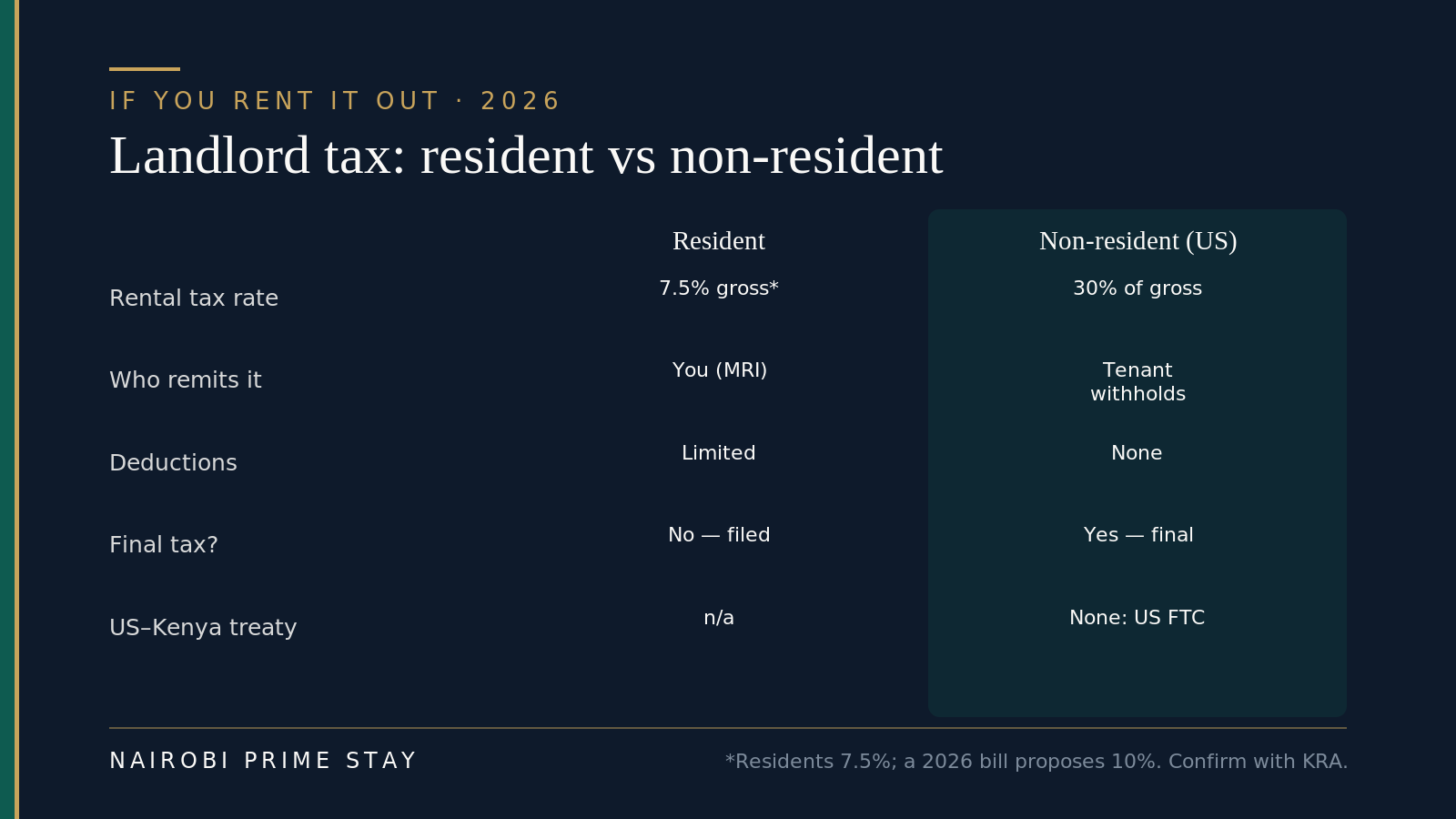

If you’ll rent it out, the tax bill is bigger than a resident’s. This is the number most off-plan pitches leave out. A landlord living in the US is a non-resident landlord, and Kenya taxes non-resident rental income at a flat 30% of the gross rent — withheld at source by your tenant or agent, with no deductions, as a final tax. A resident pays 7.5% on gross residential rent (a 2026 bill proposes 10%, not yet law). There’s no comprehensive US–Kenya tax treaty, so you claim the Kenyan tax as a US foreign tax credit (IRS Form 1116) against the same income you must still report to the IRS. Budget your yield after the 30%, not before.

If you let the finished unit, a US-based owner is taxed as a non-resident landlord — 30% of gross. Confirm current rates with KRA and your advocate.

If you let the finished unit, a US-based owner is taxed as a non-resident landlord — 30% of gross. Confirm current rates with KRA and your advocate.

You can’t run it from the US alone. Whether you’re monitoring the build or letting the finished unit, you need trusted people on the ground — an advocate, a project monitor, and later a letting or property manager (usually 8–10% of rent). Sign remotely with a power of attorney if you must, but never release a payment on photos alone. For the fuller picture, see our guides to buying property as a diaspora investor, property management in Nairobi, buy-to-let returns and taxes for expats in Kenya.

Red flags vs green lights

Run any off-plan offer past this list before you pay a shilling.

Run any off-plan offer past this list before you pay a shilling.

If you see the left column, slow down or walk. If you see the right column, you’re dealing with a serious developer.

Red flags

- No completed projects you can visit

- No NCA, county or NEMA approvals on file

- Refuses escrow or milestone-linked payments

- Payment requested to a personal or unfamiliar account

- A price far below everything comparable

- A vague completion “timeline,” no penalty for delay

- Pressure to “pay today before the price goes up”

- No clear answer on how you get your sectional title

Green lights

- Finished buildings you can walk through and ask residents about

- Registrations and approvals produced on request

- An escrow / stakeholder account with milestone releases

- Bank-financed, with units genuinely selling

- A dated completion with liquidated damages for delay

- A detailed specification annexed to the contract

- Your own advocate welcomed, not resisted

- A clear, written path to your sectional title

An off-plan buyer’s checklist

- Visited at least one of the developer’s completed projects and spoken to residents

- Confirmed NCA registration (developer and contractor) plus county and NEMA approvals

- Ran an Ardhisasa title search on the land — ownership, tenure, no caveats or charges

- Checked how many units are sold and whether the build is funded beyond installments

- Engaged my own independent advocate, not the developer’s

- Negotiated an escrow / stakeholder account with milestone-linked payments

- Secured a firm completion date with liquidated damages and a refund clause

- Annexed a detailed specification and a defects liability period

- Confirmed the sectional title path and timeline in writing

- Arranged independent site monitoring if I’m buying from abroad

- Budgeted stamp duty (4%), legal fees and currency swings into the total

- If I plan to let it, ran my yield after the 30% non-resident rental tax, not before

- Walked away from any pressure to “pay today” or wire to a personal account

Final thoughts

Off-plan in Nairobi is neither a scam nor a sure thing. It’s a genuine way to buy below market with a payment plan no bank would offer — and a genuine way to lose a deposit if you skip the homework. The deciding factor isn’t the apartment. It’s the developer, the contract, and your willingness to verify before you pay.

If you can vet a track record, insist on escrow and milestones, and wait out a build you’re able to monitor, off-plan can be the smartest entry into Nairobi property. If certainty matters more to you than a discount, a finished unit — or renting while you learn the city — is the honest alternative. There’s no wrong answer here, only the one that fits your risk appetite.

This is general guidance, not legal or financial advice. Off-plan rules, taxes and the market all shift — confirm current details with a licensed Kenyan advocate and the official portals before you commit.

Related reading

- Property investing in Kenya — the cluster pillar that ties land, tax, financing and returns together.

- How to buy property in Kenya — the full step-by-step purchase process.

- Financing and mortgages in Kenya — how developer payment plans compare with a loan.

- New developments and satellite cities — where the off-plan projects actually are.

- Property scams in Kenya — how the deposit-and-disappear schemes work, and how to avoid them.

- Buying property as a diaspora investor and buy-to-let returns in Nairobi — the money case if you’re buying to let.

- Taxes for expats in Kenya, sending money to Kenya and the USD/KES currency guide — the cross-border money mechanics.

- Property management in Nairobi, best areas to invest and building a house in Kenya — running it after handover, or other routes into the market.

- Buying land in Kenya and Nairobi property prices — the wider market and the tenure picture.

- Conveyancing in Kenya and title deeds explained — the legal mechanics behind your purchase and your title.

- Moving to Nairobi — the complete relocation hub if you’re planning the bigger move.

While you wait for the keys

Off-plan buyers still need somewhere to live while the building goes up — and a secure base to inspect it from. A serviced apartment gives you an all-inclusive home (Wi-Fi, cleaning, backup generator, 24/7 security) on flexible monthly terms, with no furniture or utility setup. Browse our serviced apartments in Nairobi, or let our AI relocation assistant shortlist one near your project in a couple of minutes. A $50 deposit reserves your place, and you pay the balance on arrival.

Frequently asked questions

Is buying off-plan in Nairobi safe?

It can be, but only with serious due diligence. Off-plan is legal and common in Nairobi, and a good project can deliver strong returns, but Kenya has no dedicated off-plan law, so buyers carry real risk of delays, spec changes and even developer failure. Safety comes from vetting the developer’s completed projects, confirming the approvals and a clean land title, and insisting on an escrow account with milestone-linked payments. Buy from a proven developer with the right contract and it’s reasonably safe; buy on a brochure and a promise and it isn’t.

How much cheaper is off-plan than a finished apartment in Nairobi?

Off-plan units are commonly 10 to 20% cheaper than a comparable finished apartment, and in a rising market the discount to the projected completion value can be larger. Developers price early-stage units low to build sales momentum and fund construction. The discount is real, but it is compensation for the risk you take on - it only pays off if the project completes on time and to spec.

What deposit do I need to buy off-plan in Nairobi?

Usually about 10 to 20% of the price to reserve and sign, with the balance paid in installments over the 24 to 36 months of construction. Some developers offer plans with as little as 10% down. Insist that the deposit goes into a stakeholder or escrow account rather than the developer’s operating account, and that later installments are tied to verified construction milestones.

What happens if an off-plan project stalls or the developer goes bust?

It depends almost entirely on your contract and how you paid. If your money sat in escrow and was released on milestones, and you have a refund clause and a long-stop completion date, you have real recourse. If you paid lump sums into a developer’s own account with no escrow, recovery is slow, costly and often incomplete - Kenya has seen buyers lose deposits when developers collapsed. This is why escrow, milestone payments and an independent lawyer matter before you pay, not after.

Can foreigners buy off-plan property in Kenya?

Yes. Foreigners can buy off-plan apartments on sectional title, which is leasehold for up to 99 years - the standard, fully legal route for non-citizens. Foreigners cannot own freehold or agricultural land, but apartments are unaffected. Use your own Kenyan advocate and confirm the developer can deliver an individual sectional title in your name.

How do I check if an off-plan developer is legitimate?

Start by visiting their completed buildings and talking to residents about whether they delivered on time and on spec. Confirm the developer and contractor are registered with the National Construction Authority (NCA), that the project has county and NEMA approvals, and that an Ardhisasa title search shows the developer owns the land with no caveats. Ask how many units are sold and whether a bank is financing the build. A serious developer answers all of this with documents; a risky one deflects.

What is an escrow account, and why does it matter for off-plan?

An escrow, or stakeholder, account is an independently held account that receives your payments and releases them to the developer only when a named construction milestone is verified - the foundation or the roof, for example. It stops your money funding anything other than your building, and it gives you leverage if work stalls. Escrow is not yet legally required in Kenya, so you have to negotiate it into your contract; a developer who refuses it is a warning sign.

How long does an off-plan apartment take to complete in Nairobi?

Most off-plan projects are sold on a 24 to 36 month build timeline, but delays are common, so plan for longer and write a firm completion date into your contract. Protect yourself with liquidated damages - a real financial penalty - for late delivery, and the right to a refund if the project blows past a long-stop date. Treat any promise of a 12-month build with healthy skepticism.

Is off-plan a good investment in Nairobi in 2026?

It can be, but it is selective. HassConsult’s eight tracked prime off-plan schemes returned about 18% (18.06%) in 2025, yet the wider apartment market is oversupplied and soft - as of its Q1 2026 index, premium apartment corridors like Westlands and Upper Hill were still slipping while a few suburbs edged up. Location and developer quality decide the outcome far more than the off-plan label. A well-run project in a strong corridor can pay off; an average apartment in an oversupplied area may not, off-plan or not.

Do I pay tax if I rent out my off-plan apartment in Nairobi?

If you live in the US, yes - and more than a resident pays. A non-resident landlord’s Kenyan rental income is taxed at a flat 30% of the gross rent, withheld at source by the tenant or agent and treated as a final tax, with no deductions. A resident pays 7.5% on gross residential rent (a 2026 bill proposes 10%, not yet law). Because there’s no comprehensive US-Kenya tax treaty, you claim the Kenyan tax as a US foreign tax credit and still report the income to the IRS. Work out your yield after the 30%, and confirm current rates with KRA and your advocate.

Can I buy off-plan in Nairobi from the US without visiting?

Yes, and many diaspora buyers do, but only with people you trust on the ground. Appoint an independent Kenyan advocate to run the searches and sign under a power of attorney, and a project monitor or relative to verify each construction milestone before any payment is released. Never pay on the strength of photos a sales team sends, always send money to an escrow or stakeholder account rather than a personal one, and confirm bank details by phone using independently sourced numbers.

Is Kenya bringing in an escrow law to protect off-plan buyers?

Reform has been proposed but not enacted. A Real Estate Regulation Bill would license developers under a new regulatory authority, register every project on a public platform, and require buyer funds to sit in project-specific escrow accounts released against construction progress. As of 2026 it isn’t law, so buyers still can’t rely on it - you have to negotiate escrow and milestone payments into your own contract. Check the current status with a licensed Kenyan advocate before you buy.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.