Guides · Property investment

Conveyancing in Kenya: What Your Property Lawyer Does (2026)

Conveyancing in Kenya: What Your Property Lawyer Does (2026)

Conveyancing is the legal work of moving a property from the seller’s name into yours — safely, and with a clean title at the end. In Kenya, a licensed advocate handles it, and engaging a good one is the single best thing you can do to protect your money. This is where careful buyers stay out of trouble and careless ones lose deposits.

This guide explains exactly what your advocate does, in what order, and what it costs, as of 2026. You’ll see how the sale agreement and deposit work, what an official search and the “completion documents” actually are, which consents a transfer needs, how stamp duty is assessed, and how the title finally gets registered in your name. It’s written for Americans and other foreigners buying in Nairobi, but the process is the same countrywide.

One honest note up front: this is general information, not legal advice. Conveyancing is exactly the part you should not do alone. Use a Kenyan advocate for your purchase — this guide just helps you understand what they’re doing and ask the right questions.

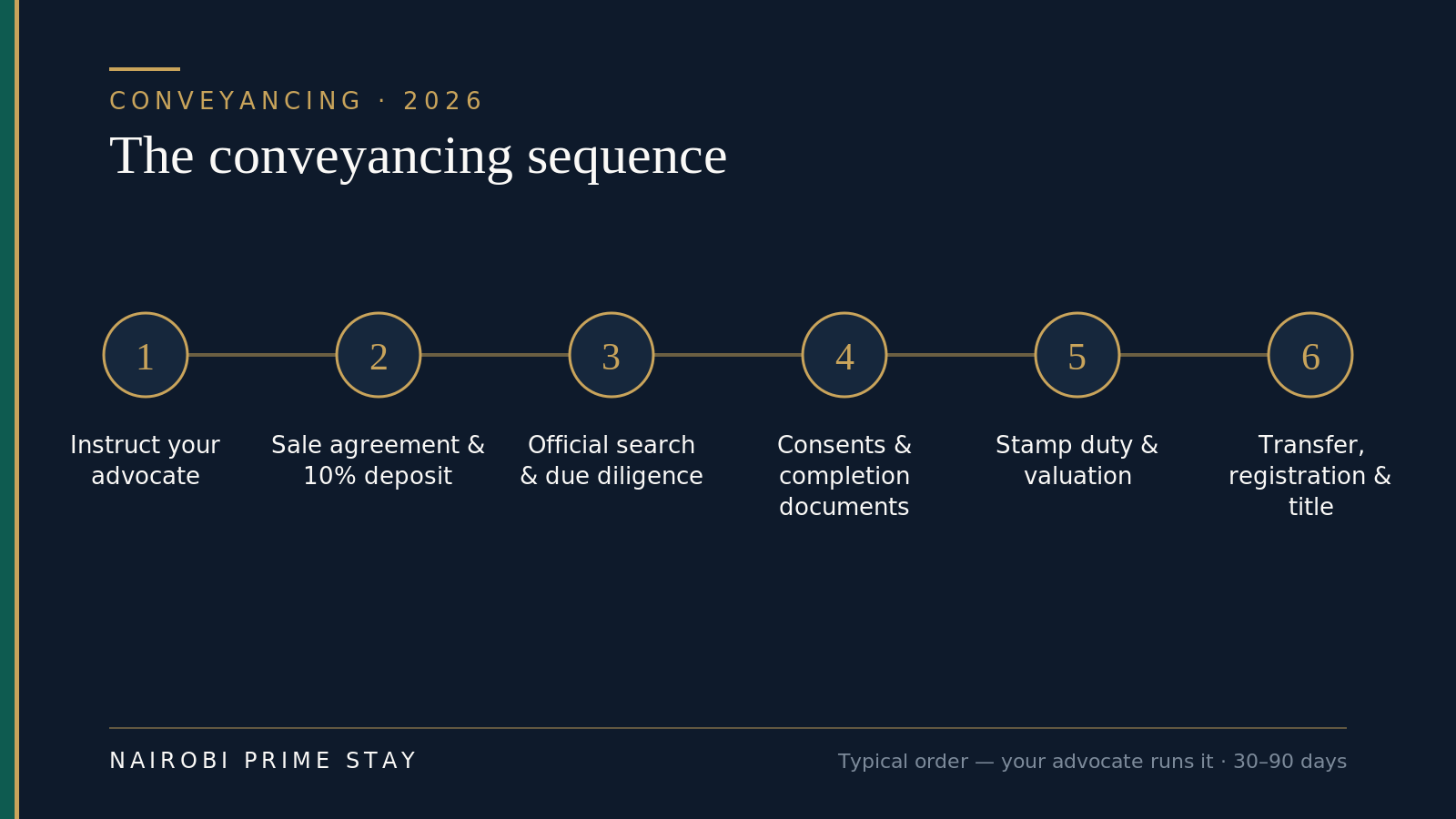

TL;DR: In Kenya, a licensed advocate does your conveyancing. The usual order: you agree a price, your advocate runs an official search to confirm the seller really owns it, then drafts a sale agreement under which you pay a deposit (commonly 10%) that the advocate holds as a stakeholder. You then gather completion documents and any consents (Land Control Board for agricultural land, spousal, lessor, rates and rent clearances), pay stamp duty (4% of value in towns including Nairobi, 2% rural) after a government valuation, and your advocate registers the transfer so the title is issued in your name. Legal fees follow the Advocates’ Remuneration Order scale — roughly 1.5% on the first KES 2.5M (tapering above) plus 16% VAT. Budget 30–90 days start to finish.

The conveyancing sequence — your advocate runs each step, typically over 30–90 days.

The conveyancing sequence — your advocate runs each step, typically over 30–90 days.

What is conveyancing, and why it matters

Conveyancing is the legal transfer of ownership from seller to buyer. It starts the moment you agree to buy and ends when a new title is registered in your name. Everything in between — checking the title is real, drafting the contract, handling the money, clearing taxes and consents, and registering the transfer — is conveyancing.

Why does it matter so much in Kenya? Because the biggest property risks here are legal, not physical. The land may be lovely and the building sound, but if the seller doesn’t truly own it, if there’s a hidden charge or court caveat on the title, or if a required consent is missing, you can pay in full and still not own the property. A proper conveyancing process catches all of that before your money is gone.

It’s also where the money actually moves. Done right, your deposit is protected and only released when the deal is real. Done carelessly — paying a seller directly, skipping the search, trusting a photocopy — and you’re exposed to Kenya’s most common property frauds. We cover those in detail in the guide to property scams in Kenya; conveyancing is how you avoid nearly all of them.

This guide focuses on the legal process and the lawyer’s role. For the buyer’s wider journey — finding a place, getting a KRA PIN, viewing, negotiating — see how to buy property in Kenya, step by step. For the title document itself, see title deeds in Kenya explained.

What your advocate actually does

Your advocate is the engine of the whole transaction. A good one is part lawyer, part project manager, part safeguard for your money. Here’s the job, in plain terms.

They verify ownership by running an official search at the land registry, confirming the registered owner matches the person selling, and flagging any charges, cautions or caveats. They draft and negotiate the sale agreement, the contract that sets the price, the deposit, the completion period and the conditions that protect you. They hold your deposit as a stakeholder, meaning it sits in their account and is only released when agreed milestones are met — not handed to the seller on a promise.

They then assemble the completion documents — the signed transfer, the original title, tax clearances and every consent the deal needs — and chase whichever party is missing one. They handle stamp duty: getting the property valued by a government valuer, calculating the duty and paying it to the KRA. Finally, they register the transfer at the lands registry so a new title issues in your name, and hand you a clean, complete file.

Two more quiet but important roles: advocates give each other formal “professional undertakings” — binding promises (for example, the seller’s advocate undertaking to hand over the title once payment clears) that keep a deal moving safely. And your advocate is your honest brake: the person whose job is to say “don’t pay yet” when something isn’t right.

What an independent buyer’s advocate does — and the protection each step buys you.

What an independent buyer’s advocate does — and the protection each step buys you.

Use your own advocate, not just the seller’s

This is the rule that saves people the most grief: instruct your own independent advocate. In Kenya, the buyer and seller each normally appoint their own. The seller’s advocate works for the seller’s interests; yours works for yours. If you “save money” by relying on the seller’s lawyer alone, nobody in the room is checking the deal on your behalf.

A good buyer’s advocate is independent of the seller, the agent and the developer. Ask how long they’ve practiced conveyancing, whether they’re in good standing with the Law Society of Kenya, and — crucially — get their firm’s account details directly from the firm, never from a WhatsApp message or an email you can’t verify. Payment-redirection fraud, where a scammer poses as your lawyer and sends new “bank details,” is real. Confirm any account by calling the office on a number you looked up yourself.

If you don’t have an advocate yet, a reputable agent, your embassy’s list, or the Law Society of Kenya can point you to firms that do conveyancing for foreign buyers. You can also ask the Nairobi Prime Stay team to suggest where to start.

The sale agreement: deposit, stakeholder and conditions

Once you’ve agreed a price and your advocate’s first checks look clean, the deal is written into a sale agreement (sometimes preceded by a short letter of offer). This is the contract, and the details matter.

The deposit. You typically pay a deposit of around 10% of the price on signing, with the balance on completion — the day ownership actually transfers. The exact split is negotiable, but 10% down, 90% on completion is the common shape.

Held as a stakeholder. Here’s the protection: that deposit is normally held by an advocate as a stakeholder (in effect, an escrow), not paid to the seller directly. It’s only released when the agreed conditions are met. If the deal collapses through no fault of yours, a well-drafted agreement says you get your deposit back. Never wire a deposit to a seller’s personal account — that’s how money disappears.

The completion period. The agreement sets a completion deadline — often 60 to 90 days — by which all documents, consents and the balance must be ready. It also says what happens if someone is late.

Conditions and warranties. Good agreements are conditional on the things that protect you: a clean official search, the seller delivering valid completion documents, vacant possession, all rates and rent cleared, and — where needed — Land Control Board or other consent being obtained. If a condition fails, you can walk away with your deposit. Your advocate earns their fee here, so read the agreement with them and make sure your protections are written in, not assumed.

The official search and due diligence

Before any real money moves, your advocate runs an official search on the title. This is the heart of due diligence. In Nairobi, searches are now done on the government’s digital land platform, ardhisasa (ardhisasa.lands.go.ke). As of early 2026, transacting on ardhisasa is mandatory in Nairobi, Kiambu, Kajiado and Mombasa — the search, the transfer and the stamp duty all run through it. Elsewhere, searches are still done at the relevant land registry, sometimes on paper. A search is cheap — on the order of KES 500 — and it’s the most valuable few hundred shillings you’ll spend.

The search confirms the registered owner (their name must match the seller exactly), the tenure and term (freehold, or leasehold with a stated number of years left), the size of the parcel, and any encumbrances — charges (mortgages), cautions, caveats or court restrictions. If the seller’s name doesn’t match, or there’s an undisclosed charge or a caveat, you’ve just found a problem before it cost you.

Due diligence goes a little wider than the search. For land, your advocate (with a licensed surveyor) confirms the beacons and boundaries against the registry map, and checks the parcel isn’t on a road reserve, riparian (river) strip or public land — the kind of traps covered in the buying land in Kenya guide. For an apartment, they confirm you’ll receive a proper sectional title in your own name rather than an old company “share certificate.” And throughout, they confirm you can legally hold the property at all — as a non-citizen, that means leasehold, not freehold, and not agricultural land. See can foreigners buy property in Kenya? for the ownership rules.

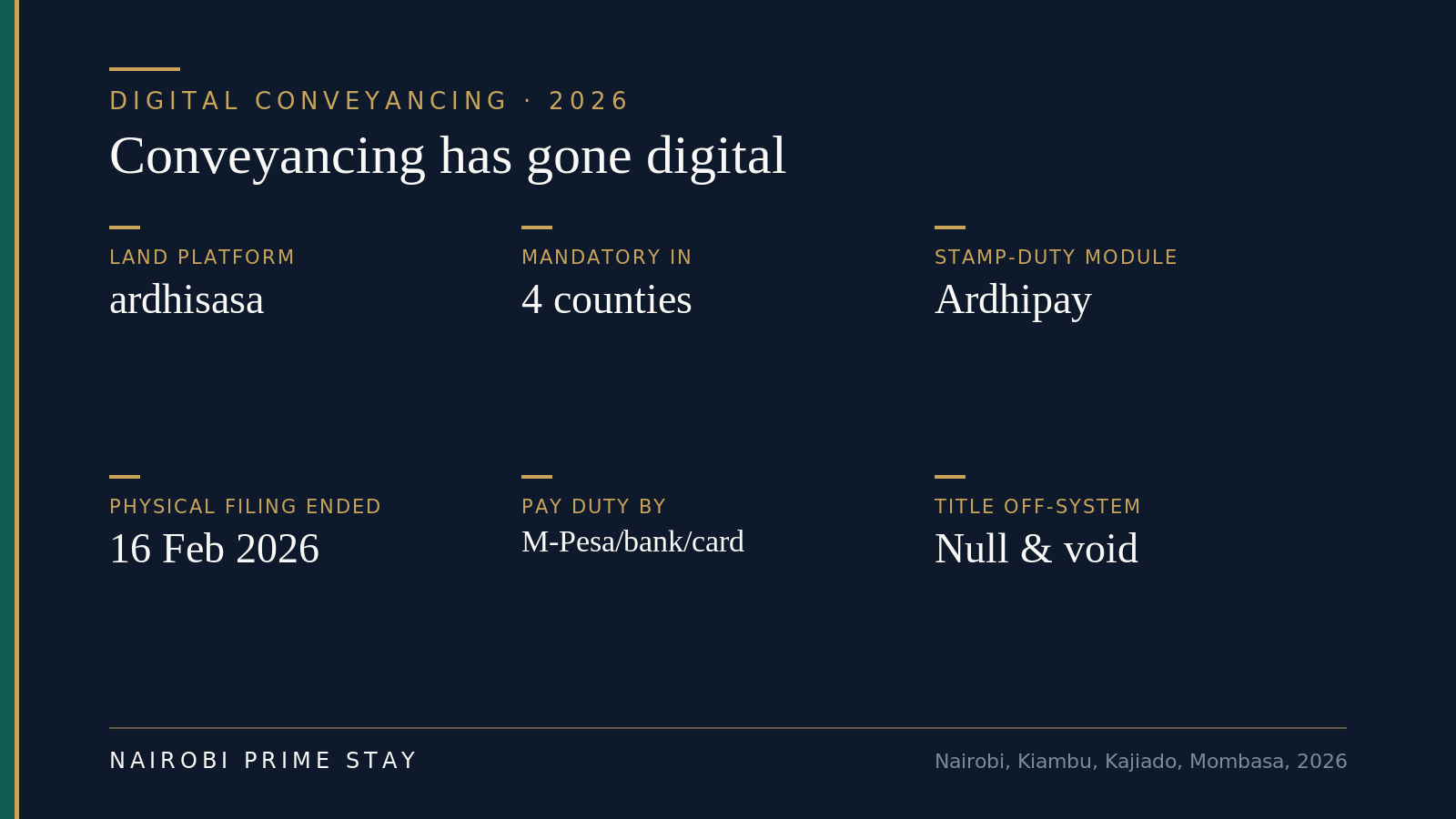

Conveyancing has gone digital: ardhisasa and Ardhipay (2026)

The biggest change to Kenyan conveyancing in years happened quietly in 2026: the process moved online. If a friend describes buying a few years ago, some of the steps below will sound different.

What’s changed in 2026 — confirm the live details with your advocate, as the rollout is still settling.

What’s changed in 2026 — confirm the live details with your advocate, as the rollout is still settling.

Searches and transfers run on ardhisasa. Since early 2026, transacting through ardhisasa is mandatory in Nairobi, Kiambu, Kajiado and Mombasa. Your advocate runs the official search, lodges the transfer and tracks the file on the platform, and you’ll often get a digital link to watch progress rather than waiting blind.

Stamp duty is paid through Ardhipay. As of 16 February 2026, the valuation, assessment and payment of stamp duty all happen online through the Ardhipay module on ardhisasa — the ministry stopped accepting physical submissions at land registries. You can pay by M-Pesa, bank transfer (RTGS or EFT) or Visa/Mastercard, and the electronic receipt links automatically to the transfer, so there’s no manual stamping to chase.

Why this matters to you. Digital filing is faster and far harder to fake, and the government has said a title issued outside the approved online system will be treated as null and void. That’s reassuring for an overseas buyer — but it makes one thing essential: use an advocate who works on ardhisasa daily and can show you the file moving. The rollout is still settling, so ask what’s live for your specific county and title before you bank on a timeline.

Completion documents: what your advocate assembles

“Completion” is the day the property becomes yours. To get there, your advocate gathers a specific set of completion documents from the seller and prepares the transfer. If any are missing, completion waits. Here’s the core set you’ll hear about.

| Document | What it is | Who provides it |

|---|---|---|

| Executed transfer | The transfer of ownership, signed and witnessed by the seller | Seller (drafted by advocates) |

| Original title | The original Certificate of Title or Certificate of Lease | Seller |

| Land rent clearance certificate | Proof annual land rent is paid up (leasehold only) | Seller |

| Land rates clearance certificate | Proof county land rates are paid up | Seller |

| Consent to transfer | Lessor / Commissioner of Lands consent where the lease requires it | Seller’s advocate applies |

| Land Control Board consent | Required to transfer agricultural land (not most apartments) | Both, via the LCB |

| Spousal consent | Where the property is a matrimonial home | Seller |

| KRA PINs & IDs | Tax PINs and ID/passport for both parties (needed to register) | Both |

| Passport photos | Required for registration | Both |

| Certificate of occupation/completion | For newly built units, proof it’s signed off | Seller/developer |

Not every deal needs every item — a standard apartment transfer won’t need Land Control Board consent, for instance, but will need rates clearance and the original title. Your advocate’s job is to know which apply and to refuse to complete until they’re all in hand. That discipline is exactly what you’re paying for.

Consents to transfer: LCB, spousal and lessor

Some transfers can’t legally complete until a third party formally consents. Missing a required consent is one of the most common reasons a Kenyan deal stalls — or, worse, completes and is later void.

Land Control Board (LCB) consent is required to transfer agricultural land. The board meets periodically, the seller’s advocate applies, and the consent letter is typically valid for six months. Two things matter for our readers: a transfer of agricultural land without LCB consent is void, and an LCB cannot consent to a sale of agricultural land to a non-citizen. So if you’re a foreigner being offered “agricultural” land, that’s a stop sign — read the land guide first.

Lessor or Commissioner of Lands consent applies to many leasehold titles: the lease itself says you need the lessor’s written consent to transfer or charge the property. Since most foreign buyers hold leasehold, this one comes up often. Your advocate applies for it as part of completion.

Spousal consent is needed where the property is a matrimonial home — the selling spouse must consent in writing, protecting against a quiet sale. It’s a quick item, but a real one.

Stamp duty: valuation and assessment

Stamp duty is the government tax on the transfer, and the buyer pays it. It’s assessed on the higher of the purchase price or the government’s own valuation of the property, so the exact figure isn’t set until a government valuer inspects the property. Build that step into your timeline.

The rates, as of 2026: 4% of the value for property in cities, municipalities and gazetted towns — which includes all of Nairobi and satellite towns like Ruiru, Kitengela and Machakos — and 2% in rural areas. So on a KES 15,000,000 Nairobi apartment, stamp duty is about KES 600,000. Since 16 February 2026, stamp duty is assessed and paid entirely online through the Ardhipay module on ardhisasa — physical processing at the registries has stopped — and you can settle it by M-Pesa, bank transfer or card. The transfer can’t be registered until the duty is paid and the electronic receipt is linked.

A note for US buyers: stamp duty is just the transfer tax. Owning and eventually selling brings other taxes — annual land rates and land rent, capital gains tax on a future sale, and rental income tax if you let the place out. We lay all of those out in the property taxes in Kenya guide. And because the US taxes its citizens on worldwide income, get cross-border tax advice early — this guide isn’t tax advice.

Transfer and registration: getting the title in your name

With completion documents in hand and stamp duty paid, your advocate lodges the transfer for registration at the land registry (on ardhisasa in Nairobi). On completion, the balance of the price is paid — typically released by your advocate against the seller’s advocate’s professional undertaking to deliver the registered title. Registration is the moment ownership legally passes: a new title issues showing you as the registered proprietor. Registration fees are nominal, on the order of KES 500.

When it’s done, your advocate should hand you a complete file: the registered title in your name, a certified copy of the stamped transfer, the stamp-duty receipt, the clearance certificates, and a final official search showing you as owner with no surprise encumbrances. Keep that file safe — it’s the proof of everything. Do a post-registration search a week or two later to confirm the register reflects the transfer cleanly. That final check closes the loop.

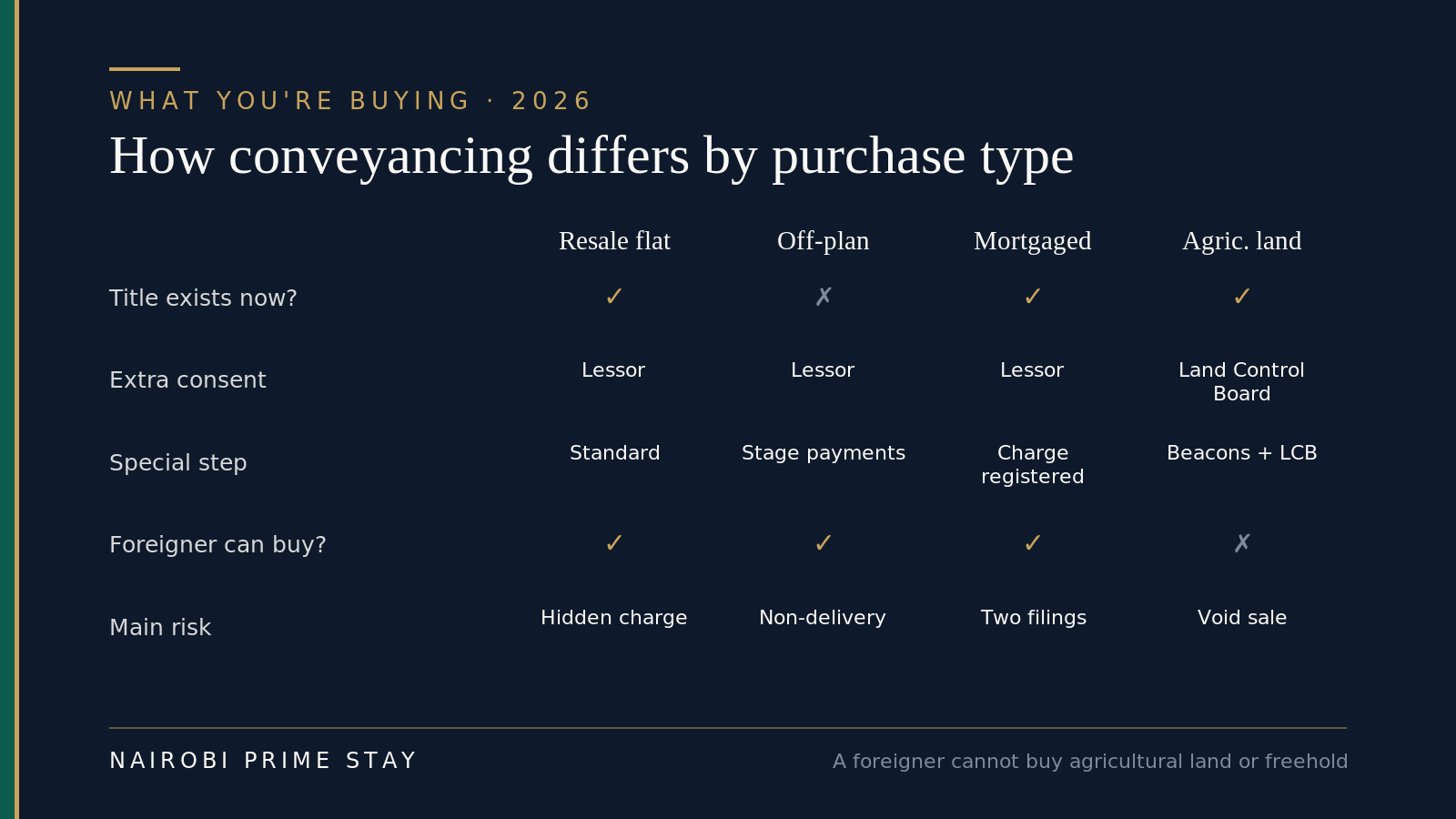

How conveyancing differs: off-plan, mortgage and land

The flow above is the standard resale purchase. Three common situations change it, and it’s worth knowing how before you sign.

How the process shifts by what you’re buying — a foreigner cannot buy agricultural land or freehold.

How the process shifts by what you’re buying — a foreigner cannot buy agricultural land or freehold.

Buying off-plan. With an off-plan apartment, there’s no title to transfer yet — you’re buying a promise to build. The conveyancing centers on the sale agreement: staged payments tied to construction milestones, what happens if the developer is late or fails, and a clear path to your own sectional title on completion. Due diligence shifts from the title to the developer — their track record, the land they’re building on, and whether your payments are protected. Your advocate should release deposits against milestones, not hand everything over up front.

Buying with a mortgage. If a Kenyan bank is financing the purchase, a second legal track runs alongside yours: the bank’s advocate prepares a charge over the property, registered at the same time as the transfer. You’ll pay stamp duty on the charge as well as on the transfer (a smaller percentage), and completion is coordinated so the bank releases funds against the registered security. It adds a few weeks and a second set of fees, but the mechanics are routine.

Buying land. Vacant land needs a surveyor to confirm the beacons and boundaries against the registry map, plus a check that the parcel isn’t on a road reserve, a riparian strip or public land. If the land is classified agricultural, the transfer needs Land Control Board consent — and the board cannot consent to a sale of agricultural land to a non-citizen. For a foreigner, “agricultural land” is a stop sign.

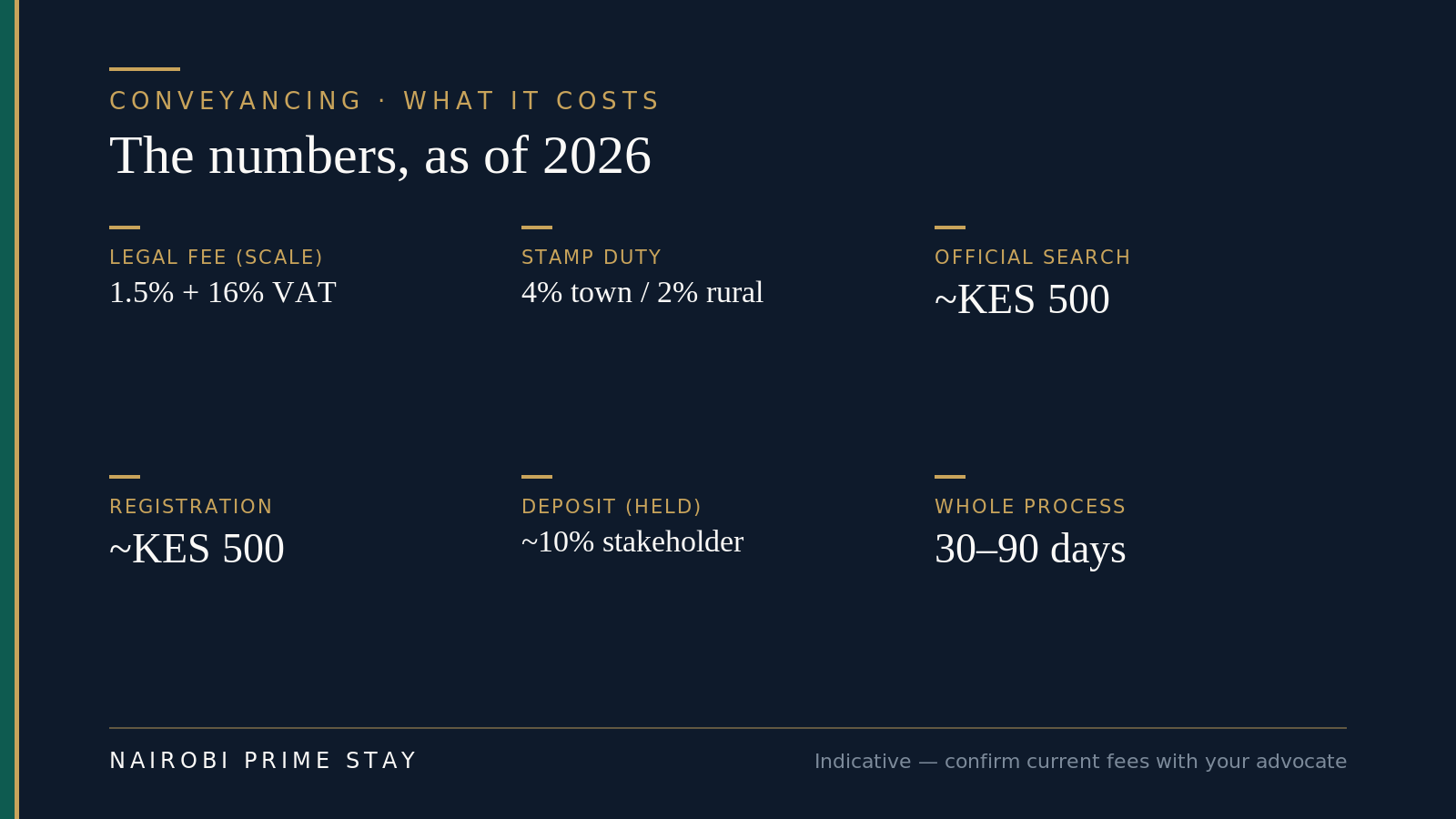

What conveyancing costs

Legal fees for conveyancing aren’t a free-for-all in Kenya — they follow a published scale, the Advocates’ Remuneration Order, which ties the fee to the value of the property. That’s good for buyers: it makes fees predictable and comparable. One nuance worth knowing: the scale is a legal minimum, not a ceiling — an advocate can’t quote below it, so a fee that sounds suspiciously cheap is a red flag, not a bargain. If the same advocate were to act for both seller and buyer (uncommon, and not what we’d advise), the order allows the fee to be cut by one-sixth. Expect honest variation at the edges, and always get a written fee quote up front.

The cost of conveyancing at a glance — indicative 2026 figures; confirm current fees with your advocate.

The cost of conveyancing at a glance — indicative 2026 figures; confirm current fees with your advocate.

Here’s the legal-fee scale for a sale or purchase, by property value (plus 16% VAT on the fee):

| Property value (KES) | Advocate’s fee on the scale |

|---|---|

| Up to 2,500,000 | 1.5% (minimum around KES 20,000–35,000) |

| 2,500,001 – 5,000,000 | 1.25% |

| 5,000,001 – 10,000,000 | 1% |

| 10,000,001 – 25,000,000 | 0.75% |

| Above 25,000,000 | ~0.65%, tapering |

So on a KES 15,000,000 apartment, the advocate’s professional fee works out at roughly KES 130,000–150,000 before VAT, plus VAT and disbursements. On top of the legal fee you’ll meet the other line items — stamp duty (much the biggest), the government valuation, search and registration fees, and small disbursements for clearances. Add it together and total transaction costs usually land around 5–8% of the price, with stamp duty doing most of the work. Budget toward the top of that range so nothing surprises you.

| Cost | Rate / amount (2026) | Who pays |

|---|---|---|

| Stamp duty | 4% urban / 2% rural, on the higher of price or valuation | Buyer |

| Advocate’s legal fee | Scale above (from ~1.5%) + 16% VAT | Each side pays their own |

| Government valuation | Modest fee for the duty assessment | Buyer |

| Official search | ~KES 500 | Buyer |

| Registration | ~KES 500 | Buyer |

| Clearance certificates | Small disbursements | Seller (usually) |

How long conveyancing takes

For a straightforward deal, budget 30 to 90 days from signing the sale agreement to a registered title. A clean apartment purchase with a willing seller and no consent complications can run at the faster end; anything involving Land Control Board consent, a lessor’s consent, arrears to clear, a mortgage on either side, or a title that needs migrating to the digital register runs longer.

| Stage | Typical time |

|---|---|

| Official search & drafting the sale agreement | A few days to 2 weeks |

| Sign agreement, pay deposit, gather completion documents | 2–6 weeks |

| Consents (LCB / lessor / spousal) where needed | 2 weeks to 2 months+ |

| Government valuation & paying stamp duty | 1–3 weeks |

| Registration of the transfer | 1–2 weeks |

The honest variables are consents and government turnaround, not your advocate’s drafting. Start the consent applications early and keep your own documents (KRA PIN, passport, photos) ready so you’re never the bottleneck.

Buying from the US: conveyancing by power of attorney

You don’t have to be in Kenya for completion day. Plenty of diaspora and overseas buyers run the whole purchase remotely, and the legal tool that makes it work is a power of attorney (PoA).

Buying remotely — the power of attorney is notarized and legalized abroad, then registered in Kenya before it’s used.

Buying remotely — the power of attorney is notarized and legalized abroad, then registered in Kenya before it’s used.

A PoA lets a trusted person in Kenya — often your advocate, or a relative — sign documents and complete steps on your behalf. The authentication matters, so get it right. Kenya is not part of the Apostille Convention, so a PoA you sign in the US must be notarized (the US Embassy in Nairobi offers notarial services), then legalized for use in Kenya — that’s consular legalization, not an apostille. A power of attorney made abroad must also be registered with the Registrar of Documents in Kenya before it can be used in a land transaction. Your advocate will tell you exactly what they need and handle the Kenyan registration.

On the money side, move funds the safe way. Pay your deposit and balance by bank transfer (or a service like Wise) into your advocate’s verified stakeholder account — never a personal account, and never to “updated details” sent by email. Confirm the account by phone on a number you looked up yourself. If you ever carry cash, you must declare amounts over USD 10,000 at customs, both into and out of Kenya. For how the shilling moves and the cheapest way to send money, see the USD–KES currency guide and sending money to Kenya. Kenya has no exchange controls, so when you eventually sell, you can convert and repatriate the proceeds freely.

One honest caveat: buying a place you’ve never stood in is how people end up with a “view” that faces a wall. If you possibly can, have someone you trust view it in person, or spend your first week in a serviced apartment and see it yourself before you commit.

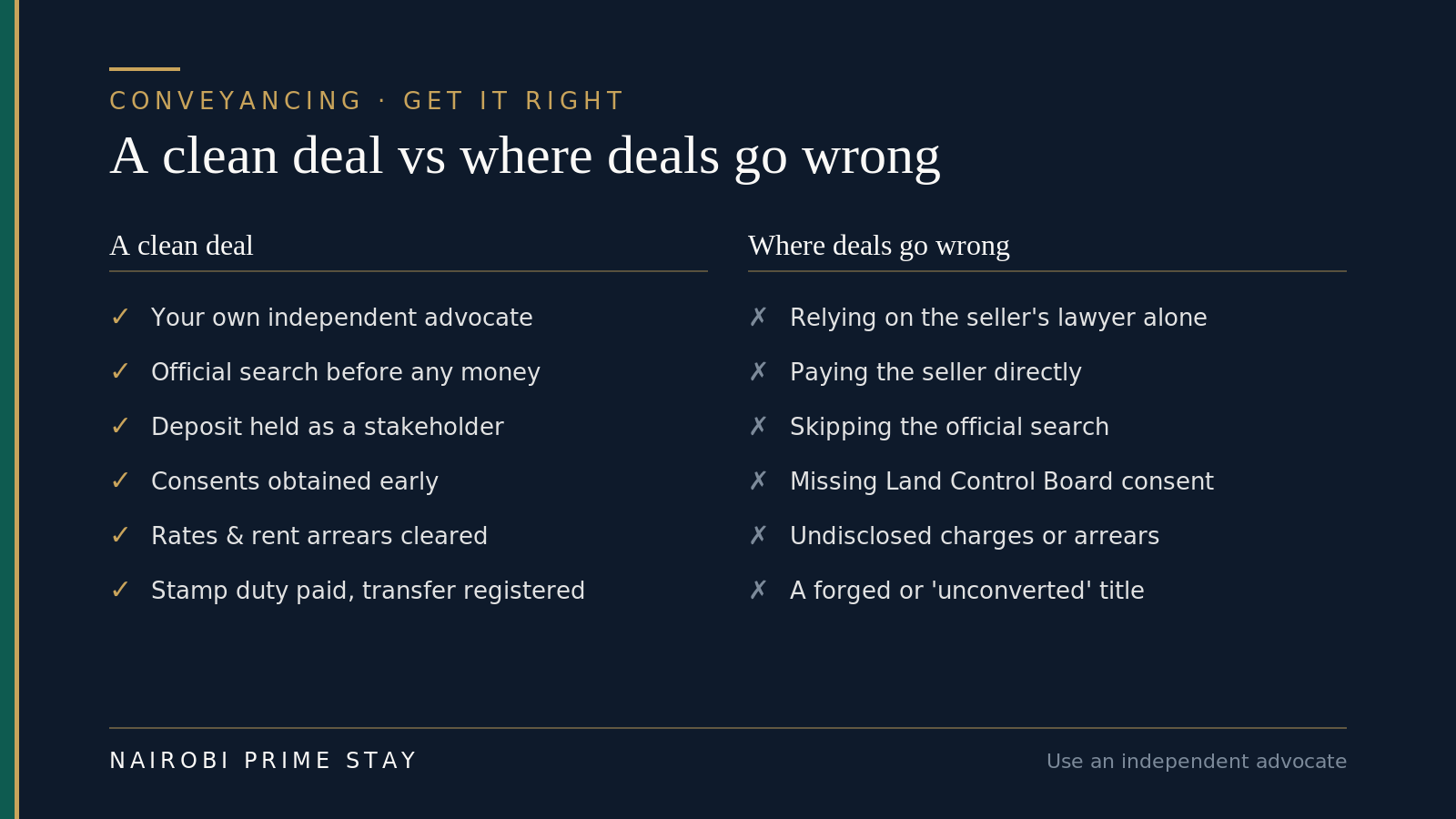

What can go wrong — and how conveyancing prevents it

Most Kenyan property disasters trace back to a step that got skipped. Here’s the short list, and how a proper process heads each one off.

A clean deal versus where deals go wrong — the difference is almost always the process, not luck.

A clean deal versus where deals go wrong — the difference is almost always the process, not luck.

A forged or “borrowed” title. Fake titles and impersonation of the real owner are the classic frauds. The official search and confirming the seller’s identity against the title defeat most of them. Kenya’s own lands ministry has acknowledged that a meaningful share of titles have been irregular, so this check is not optional.

Paying the wrong person. Wiring a deposit to a seller’s personal account, or to “new bank details” sent by email, is how money vanishes. Pay only into your advocate’s verified stakeholder account, confirmed by phone on a number you found yourself.

A hidden charge or caveat. A mortgage, court order or caveat already on the title can stop you ever getting clean ownership. The search surfaces it; a good agreement makes clearing it the seller’s condition before completion.

A missing consent. No Land Control Board consent on agricultural land, or no lessor’s consent on a leasehold, can make a transfer void. Your advocate applies for the right consents as part of completion.

Undisclosed arrears. Unpaid land rates or rent block a transfer and can land on you. Clearance certificates, required as completion documents, prove they’re settled.

An “unconverted” apartment. Buying into an old block still on a company share certificate rather than a sectional title leaves you a shareholder, not an owner. Make conversion to a sectional title the seller’s job before you complete — see title deeds in Kenya.

How this plays out: a real scenario

Say you’re an American renting in Kilimani and you’ve decided to buy a two-bedroom apartment there for KES 14,000,000. Here’s the conveyancing, start to finish.

You instruct your own advocate — not the seller’s. She runs an official search on ardhisasa: the seller’s name matches the title, it’s a 99-year leasehold with 81 years left, and there’s a bank charge on it from the seller’s old mortgage. Not a dealbreaker, but a condition: the agreement will require the charge to be discharged before completion.

She drafts the sale agreement at KES 14,000,000, you pay a 10% deposit (KES 1,400,000) into her account as stakeholder, and the clock starts on a 60-day completion. Over the next weeks she gathers the completion documents — the seller’s discharge of charge, the original title, land rates and rent clearance certificates, the lessor’s consent to transfer, and both parties’ KRA PINs and IDs. A government valuer inspects the flat; stamp duty at 4% comes to about KES 560,000, which you pay online through the Ardhipay module. Her professional fee on the scale is roughly KES 125,000 plus VAT.

On completion day you pay the KES 12,600,000 balance, released against the seller’s advocate’s undertaking to deliver the registered title. She lodges the transfer; a couple of weeks later a new title issues showing you as proprietor. A post-registration search confirms it — your name, no charge, no caveat. About ten weeks, no drama, because every step was done in order.

Your conveyancing checklist

- Appoint your own independent advocate — not just the seller’s — and confirm they’re in good standing with the Law Society of Kenya.

- Verify the firm’s bank details directly with the office by phone; ignore any “updated details” sent by email or message.

- Insist on an official search before any money changes hands; confirm the owner, tenure, term and any charges or caveats.

- Pay the deposit only to your advocate as a stakeholder — never to a seller’s personal account.

- Read the sale agreement with your advocate: deposit, completion period, and conditions that let you exit and recover your deposit.

- Confirm which consents apply (Land Control Board, lessor, spousal) and that they’re being obtained.

- Check rates and rent clearance certificates are in the completion documents.

- Budget 5–8% of the price for total costs, stamp duty being the biggest; get a written fee quote.

- For an apartment, confirm you’ll receive a sectional title in your own name, not a share certificate.

- Do a post-registration search to confirm the title now shows you as owner, clean.

Final thoughts

Conveyancing in Kenya isn’t mysterious, and it isn’t a formality. It’s the ordered set of legal steps that turns “we agreed a price” into “the title is in my name,” with your money protected the whole way. The single decision that matters most is the first one: appoint your own competent advocate and let them run it. Do that, insist on the official search, keep your deposit with a stakeholder, and clear every consent and arrear before you complete — and the worst Kenyan property stories simply don’t happen to you.

Take it in order, ask questions, and don’t let anyone rush you past a step. A property deal that takes ten patient weeks beats a fast one that unravels. The process exists to protect you. Use it.

Related reading

- Property investment in Kenya: the complete guide — the cluster hub; start here.

- How to buy property in Kenya, step by step — the full buyer’s journey.

- Title deeds in Kenya explained — freehold, leasehold and sectional title.

- Property taxes in Kenya — stamp duty, rates, land rent, CGT and rental tax.

- Property scams in Kenya — the frauds, and how to avoid them.

- Can foreigners buy property in Kenya? — the ownership rules.

- Buying land in Kenya safely — due diligence and beacons.

- Property financing and mortgages in Kenya — buying with a loan.

- Buying off-plan in Nairobi — paying in stages before it’s built.

- Diaspora property investment in Kenya — buying from abroad.

- Moving to Nairobi: the complete guide — the relocation hub.

Before you buy, give yourself a soft landing

Most foreign buyers rent first, get to know the city and meet their advocate in person before they commit to a purchase. A furnished serviced apartment is the easy way to do that — all-inclusive, flexible, and a secure base while you view homes, test commutes and run the conveyancing without pressure. Browse our serviced apartments in Nairobi with honest monthly pricing, or let the AI relocation assistant shortlist a few in a couple of minutes. A $50 deposit reserves a place and the balance is paid on arrival — nothing more before you travel.

Frequently asked questions

What is conveyancing in Kenya?

Conveyancing is the legal process of transferring property ownership from the seller to the buyer, ending with a new title registered in your name. In Kenya a licensed advocate handles it. The work includes an official title search, drafting the sale agreement, holding the deposit, gathering completion documents and consents, paying stamp duty, and registering the transfer.

Do I need a lawyer to buy property in Kenya?

Yes — in practice you should always use a licensed advocate, and buyer and seller each appoint their own. Your advocate verifies the seller really owns the property, drafts and negotiates the sale agreement, holds your deposit safely, and registers the transfer. Doing conveyancing without your own advocate is the single biggest way foreign buyers lose money in Kenya.

How much does conveyancing cost in Kenya?

Legal fees follow the Advocates’ Remuneration Order scale, which is tied to the property value — roughly 1.5% on the first KES 2.5 million, tapering to about 0.65% on higher values, plus 16% VAT. On top of the legal fee you pay stamp duty (the biggest cost), a government valuation, and small search and registration fees. Total transaction costs usually come to about 5–8% of the price.

How much deposit do I pay when buying property in Kenya?

The deposit is commonly around 10% of the purchase price, paid on signing the sale agreement, with the balance paid on completion. Critically, the deposit should be held by an advocate as a stakeholder (in effect an escrow), not paid to the seller directly, and released only when the agreed conditions are met. Never wire a deposit to a seller’s personal account.

How long does conveyancing take in Kenya?

A straightforward purchase usually takes 30 to 90 days from signing the sale agreement to a registered title. A clean apartment deal can be quicker; transfers that need Land Control Board consent, a lessor’s consent, arrears cleared, or a title migrated to the digital register take longer. The main delays are consents and government turnaround, not the drafting.

What are completion documents in Kenya conveyancing?

Completion documents are the set of papers needed to transfer the property, assembled by your advocate before completion day. They typically include the executed transfer, the original title, land rates and (for leasehold) land rent clearance certificates, any required consents, both parties’ KRA PINs and IDs, and passport photos. If any required document is missing, completion waits until it is in hand.

Who pays stamp duty in Kenya, and how much is it?

The buyer pays stamp duty. As of 2026 it is 4% of the value for property in cities, municipalities and gazetted towns — including all of Nairobi — and 2% in rural areas, charged on the higher of the price or the government valuation. It is paid to the KRA, and the transfer cannot be registered until the duty is stamped as paid.

Can I use the seller’s lawyer in Kenya?

You shouldn’t rely on the seller’s lawyer alone. In Kenya the buyer and seller each appoint their own advocate, and the seller’s advocate works for the seller’s interests, not yours. Instruct your own independent advocate so someone is checking the title, the agreement and the money on your behalf. Confirm their bank details by phone, since payment-redirection fraud is real.

What is an official search, and why does it matter?

An official search is your advocate’s check of the land register — done on ardhisasa in Nairobi or at the registry elsewhere — and it is the heart of due diligence. It confirms the registered owner matches the seller, shows the tenure and unexpired term, and reveals any charges, cautions or caveats on the title. It costs only around KES 500 and should always be done before any money changes hands.

Can I buy property in Kenya remotely from the US?

Yes. Many overseas buyers complete a purchase without flying over by granting a power of attorney to a trusted person or their advocate in Kenya. Sign the power of attorney before a notary (the US Embassy in Nairobi offers notarial services), have it legalized for use in Kenya — Kenya isn’t in the Apostille Convention, so this is consular legalization, not an apostille — and registered with the Registrar of Documents. Pay all money by transfer into your advocate’s stakeholder account, never a personal account.

Is ardhisasa mandatory, and how is stamp duty paid in 2026?

As of early 2026, transacting through ardhisasa is mandatory in Nairobi, Kiambu, Kajiado and Mombasa — searches, transfers and stamp duty all run on the platform. Since 16 February 2026, stamp duty is assessed and paid online through the Ardhipay module, and the registries no longer accept physical submissions. You can pay by M-Pesa, bank transfer or card, and the government has said a title issued outside the approved system will be treated as void.

How does conveyancing differ for off-plan or mortgaged property?

Off-plan, there’s no title to transfer yet, so the sale agreement does the heavy lifting — staged payments tied to construction, protections if the developer is late, and a clear path to your own sectional title on completion. With a mortgage, the bank’s advocate registers a charge over the property at the same time as the transfer, you pay stamp duty on the charge as well, and completion is timed so the bank releases funds against the registered security.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.