Guides · Property investment

Building a House in Kenya vs Buying: Costs and the Process (2026)

Building a House in Kenya vs Buying: Costs and the Process (2026)

Building is usually cheaper than buying a finished home in Kenya — often 20 to 30 percent cheaper — but only if you already own the land and you manage the project well. Get either of those wrong and the gap closes fast, sometimes the other way.

That’s the honest headline, and most “build vs buy” advice skips the conditions. Building lets you get exactly the home you want for less money per square metre. It also hands you a second job: hiring the right people, pulling permits, watching a budget that wants to run 15 percent over, and waiting six months to a year-plus before you can move in.

This guide is for Americans and diaspora buyers weighing the two. What a build really costs per square metre in 2026, the step-by-step process from land to keys, how long it takes, how to finance it, and the pitfalls — especially if you’re trying to run the whole thing from another continent.

TL;DR — building vs buying in Kenya (2026)

- Building can be 20–30% cheaper than buying a comparable finished home — but mainly if you already own the land and manage the build well. Underestimate the cost and that edge disappears.

- Budget by finish level. As of 2026, construction runs roughly KES 35,000–49,000/m² for basic finishes, KES 50,000–65,000 for mid-range, KES 70,000–95,000 for high-end and KES 100,000+ for luxury — about $270–920 per square metre. Land, fees and connections are extra.

- A basic three-bedroom house (around 100–120 m²) costs roughly KES 4.8–6 million to build, excluding land. Mid-range and larger homes run well into the tens of millions.

- The process: secure land with a clean title, hire an architect and a quantity surveyor, get county, NEMA and NCA approvals, appoint an NCA-registered contractor, build, snag, and get an occupation certificate.

- It takes 6–12 months for a standard house, longer for custom or larger builds — and weather, materials and labour can stretch that.

- Add a 10–15% contingency. Cost overruns average around 15%. The single best cost control is an NCA-registered contractor working under a professional (an architect or quantity surveyor).

- Building from abroad is doable but risky. Use a lawyer-drafted power of attorney, a written milestone contract, independent supervision, and never wire cash to an unverified “agent.”

Buying instead? Start with how to buy property in Kenya, or weigh a new-build you don’t have to manage in buying off-plan in Nairobi.

Why this matters

For many buyers, building is the difference between affording a home and not. Land plus a self-managed build can deliver a house worth more than it cost — real equity, on your terms. That’s the dream, and in Kenya it’s a common one.

The catch is that a build is a project, not a purchase. Money leaves your account in stages over many months, against work you often can’t see if you live overseas. Costs creep, timelines slip, and trusting the wrong contractor is expensive. The people who come out ahead treat it like running a small business: clear contracts, professional oversight, and a budget with room to breathe. The people who lose money skipped those steps. This guide is about being the first kind.

Build or buy? The honest trade-off

Build if you already own land, you have time, and you can manage risk. Buy if you want price certainty, you need a home soon, or land where you want to live is expensive. That’s the short version.

Build trades certainty and convenience for a lower price and a home built to your spec. Which side wins depends on whether you own land and how much oversight you can give.

Build trades certainty and convenience for a lower price and a home built to your spec. Which side wins depends on whether you own land and how much oversight you can give.

Building wins on cost and control. You pay per square metre rather than a finished-home premium, you choose the layout and finishes, and a well-run build can be worth more than it cost the day it’s done. If you already hold the land — inherited, bought years ago, or picked up cheap on the city’s edge — the math tilts hard toward building.

Buying wins on speed and certainty. The price is fixed, you can inspect what you’re getting, and you move in within weeks instead of waiting out a build. In high-land-cost prime suburbs, where plots are scarce and pricey, buying a finished house or apartment is often the only realistic route — and in today’s soft apartment market there’s plenty of finished stock to choose from.

| Build | Buy a ready home | |

|---|---|---|

| Upfront cost | Lower per m², often 20–30% less (if you own land) | Full market price |

| Price certainty | Low — final cost emerges as you go | High — you know it before you commit |

| Time to move in | 6–12+ months | Weeks |

| Customization | Full — your design, your finishes | What’s already built |

| Effort & risk | High — you run the project | Low — one transaction |

| Cost overruns | Common (~15% average) | None after purchase |

| Best for | Owners of land with time to oversee | Buyers who want certainty and speed |

There’s a middle path worth naming: a turnkey contract, where a developer or builder delivers a finished house on your land for an agreed price. You give up some control and pay a premium over self-managing, but you cap your risk and hand off the headache. For diaspora buyers especially, a reputable turnkey builder can be the sane compromise between building and buying.

What it costs to build in 2026

Construction in Kenya runs roughly KES 35,000 to KES 120,000 per square metre in 2026, depending almost entirely on your finishes. That’s about $270 to $920 per square metre at the mid-2026 exchange rate of about 129.5 shillings to the dollar (it has held near KES 129–130 through 2026 — see the USD/KES guide for the live rate). The structure costs similar money whatever you do; the spread comes from what you put on it — tiles, fittings, joinery, windows, roofing.

Indicative build cost per square metre, 2026. Excludes land. Get a quantity surveyor to price your actual design before you commit.

Indicative build cost per square metre, 2026. Excludes land. Get a quantity surveyor to price your actual design before you commit.

Here’s how the bands break down, as a rule of thumb:

| Finish level | Cost per m² (KES) | Per m² (USD) | What you get |

|---|---|---|---|

| Basic | 35,000–49,000 | ~$270–375 | Simple finishes, standard fittings, no frills |

| Mid-range | 50,000–65,000 | ~$385–500 | Good tiles, decent joinery, the comfortable norm |

| High-end | 70,000–95,000 | ~$540–730 | Quality materials, better kitchens and bathrooms |

| Luxury | 100,000–120,000+ | ~$770–920+ | Imported finishes, bespoke design, premium everything |

Two more variables move the number. House type: a single-storey bungalow (roughly KES 48,000–65,000/m²) is cheaper to build than a two-storey maisonette (around KES 60,000–85,000/m²), which is cheaper than a luxury home. Location: building in central Nairobi can run 25–30% above the national average for labour and logistics, while plots on the city’s outskirts can be 10–15% cheaper.

To make it concrete: a basic three-bedroom house of about 100–120 m² costs roughly KES 4.8–6 million to build, excluding land. Move up to mid-range and a three-bed bungalow runs more like KES 6.5–9.5 million, a standard 100 m² maisonette about KES 6.5–8 million, and a four-bedroom maisonette KES 8–16 million or more — the figures Kenyan builders quote most often in 2026. A generous family home with high-end finishes easily reaches the tens of millions of shillings. Always price your specific drawings with a quantity surveyor — per-square-metre figures are a starting point, not a quote.

What actually drives the cost: materials and labor

Two things move a build budget more than anything else: materials and labor. Get a feel for them and the per-square-metre bands stop looking like guesswork.

Indicative Nairobi material prices, early 2026. Confirm live prices with your quantity surveyor and suppliers before you budget.

Indicative Nairobi material prices, early 2026. Confirm live prices with your quantity surveyor and suppliers before you budget.

Materials. As of early 2026, a 50kg bag of ordinary cement runs about KES 750 in Nairobi (higher-grade 42.5 or premium blends KES 1,200–1,350), and structural steel is roughly KES 95,000–120,000 a ton, with a D12 reinforcement bar near KES 1,020. Prices swung hard in 2023–24 but broadly steadied through late 2025 into 2026, which helps budgeting — though a weaker shilling or a fuel spike can still nudge imported items up. Cement, steel, sand and ballast make up most of the structure; the reason two houses of the same size can cost wildly different amounts is almost always the finishes — imported versus local tiles, fittings, joinery, windows and roofing.

Labor and location. Skilled-labor shortages in Nairobi push wages above the upcountry rate, and city logistics add cost, so building in central Nairobi typically runs 15–20% above the national average. Plots on the city’s outskirts are cheaper to build on — one reason so many diaspora builds happen in satellite towns like Kitengela, Juja, Ruiru and Ngong. Weigh a build against finished-home prices in the same area with our Nairobi property prices guide.

The costs people forget

The per-square-metre figure is only the build. Budget for the rest, or it becomes your overrun:

- Land. Usually the biggest line, and entirely separate. See buying land in Kenya for prices and the searches that keep you safe.

- Professional fees. Architect, structural engineer and quantity surveyor together typically run a single-digit percentage of construction cost. Skipping them to save money is how budgets blow up later.

- Approvals. County plan-approval fees, plus a NEMA environmental fee of about 0.1% of project cost where an assessment is required. More on these below.

- Connections. Water, electricity (Kenya Power), and often a borehole, septic system or solar — these can add up quickly on an undeveloped plot.

- Contingency. Hold back 10–15%. Cost overruns in Kenyan builds average around 15%, driven by material-price swings, design changes and delays. Treat the contingency as spent until proven otherwise.

- Finance costs. If you’re borrowing, interest during the build is real money (see financing).

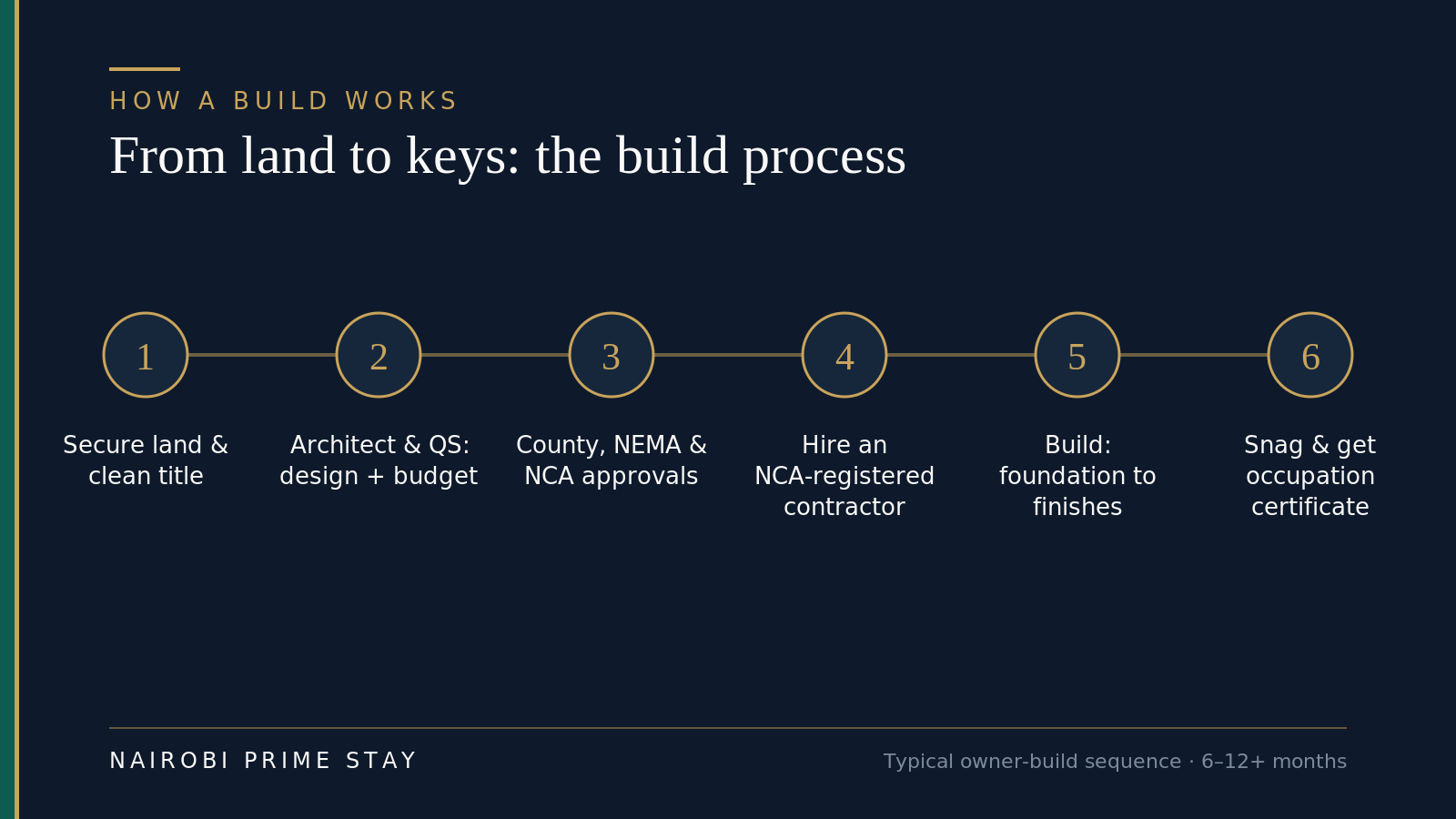

The build process, step by step

The path from empty plot to finished home follows a fairly standard order in Kenya. Here it is end to end.

A typical owner-managed build runs through these six stages over six to twelve-plus months.

A typical owner-managed build runs through these six stages over six to twelve-plus months.

1. Secure land and confirm a clean title. You can’t build on land you don’t securely own. Run an official search, confirm the title and tenure, and check the zoning allows residential building before you part with money. This is where the worst losses happen — read title deeds in Kenya and common property scams first.

2. Design — hire an architect. A registered architect turns your brief and budget into drawings that work on your plot and meet the rules. A structural engineer designs the foundations and frame. Good design saves money; it’s not where to cut.

3. Cost it — hire a quantity surveyor. The QS prepares a Bill of Quantities (BQ) — an itemized priced breakdown of every material and trade. The BQ is your budget, your tender document, and your defense against being overcharged. Don’t build without one.

4. Get approvals — county, NEMA and NCA. Your stamped architectural and structural drawings go to the county for plan approval; larger projects need a NEMA environmental sign-off; and your contractor and project must be registered with the National Construction Authority. Details below.

5. Choose a contractor. Tender the BQ to a few NCA-registered contractors, check their completed work and references, and sign a detailed written contract — scope, price, timeline, payment milestones, penalties for delay, and how disputes get resolved. Never start on a handshake.

6. Build — foundation to finishes. Construction moves through substructure (foundation and slab), walling, roofing, then finishes (plastering, plumbing, electrical, tiling, fittings). Pay against verified milestones, not the calendar, and keep an architect or QS supervising on your behalf.

7. Snag and complete. Before the final payment, walk the house and list every defect — a “snagging” inspection — and have the contractor fix them. Then obtain a certificate of occupation from the county, which confirms the building is fit to live in. Only then is the build truly done.

Approvals and permits, explained

Three approvals matter for a Kenyan home build, and skipping them risks fines, demolition or an unsellable house.

County plan approval. Your registered architect and structural engineer submit stamped drawings to the county physical-planning office where the plot sits. The county quotes a fee, you pay, and after review it issues an approval (in Nairobi, the PPA forms). This is the core building permit — construction shouldn’t start without it.

NEMA environmental approval. The National Environment Management Authority assesses a project’s environmental impact. For a single home it’s often a lighter project report rather than a full impact assessment, but where it applies, NEMA charges roughly 0.1% of total project cost. Confirm whether your build needs it before you start.

NCA registration. The National Construction Authority regulates contractors. Your contractor must be NCA-registered for their class of work, and the project itself is registered with the NCA before building begins. There’s no NCA registration fee for the project, but the requirement is real — an unregistered contractor is an immediate red flag.

A note on honesty: some self-builders skip or shortcut these to save time and money. It’s common, and it’s a mistake. Unapproved buildings can’t be financed or cleanly sold, can be flagged in any future search, and leave you exposed if anything goes wrong. Do it properly the first time.

How long it takes

A standard house in Kenya takes about 6 to 12 months to build once approvals are in hand. A simple bungalow can land near the short end; a larger or custom home, or one with a tricky site, runs to 12–16 months or more. Add the lead time for design and approvals before the first block is laid — that alone can be a couple of months.

Building remotely from abroad doesn’t have to take longer, but it’s less forgiving of slack. Weather (the long rains, March to May, slow site work), material-price swings, labour availability and cash-flow gaps are the usual causes of delay. Build a realistic schedule with your contractor, write it into the contract with a penalty for late delivery, and assume some slippage. If you’re renting while you build, factor those months of rent into the true cost — a serviced apartment can be a flexible base for the early stretch.

Financing a build

Construction is harder to finance than a straight purchase, because the asset doesn’t exist yet. A few routes:

- Cash, in stages. Most self-builds in Kenya are funded from savings, released milestone by milestone. It avoids interest but demands discipline and a real contingency.

- Construction loan. Several Kenyan banks offer milestone-based construction financing — Equity, KCB and others — that disburses as the build hits verified stages and often converts to a mortgage on completion. You’ll typically need approved drawings, a BQ, proof of land ownership and income verification.

- Diaspora mortgage. Most major banks run home-loan products designed for Kenyans abroad, and some extend to construction. As of 2026, standard home-loan rates run roughly 14–18%, with KMRC-backed and promotional rates nearer 9–11% — compare the real all-in cost, and see our financing and mortgages guide.

- Boma Yangu / affordable housing. The government’s affordable-housing programme lets buyers, including diaspora savers, register and save toward a home through the Boma Yangu portal; the required deposit was cut to about 5% of the unit price in 2026. The 1.5% Affordable Housing Levy is deducted from Kenyan salaries — if you’re not employed in Kenya you generally don’t pay it, though voluntary saving can help your allocation. Worth a look at the entry level.

Whatever the source, lenders want the same things that protect you anyway: proper drawings, a costed BQ, a clean title, and an NCA-registered contractor. If you can’t satisfy a bank, that’s a signal your build isn’t ready to start.

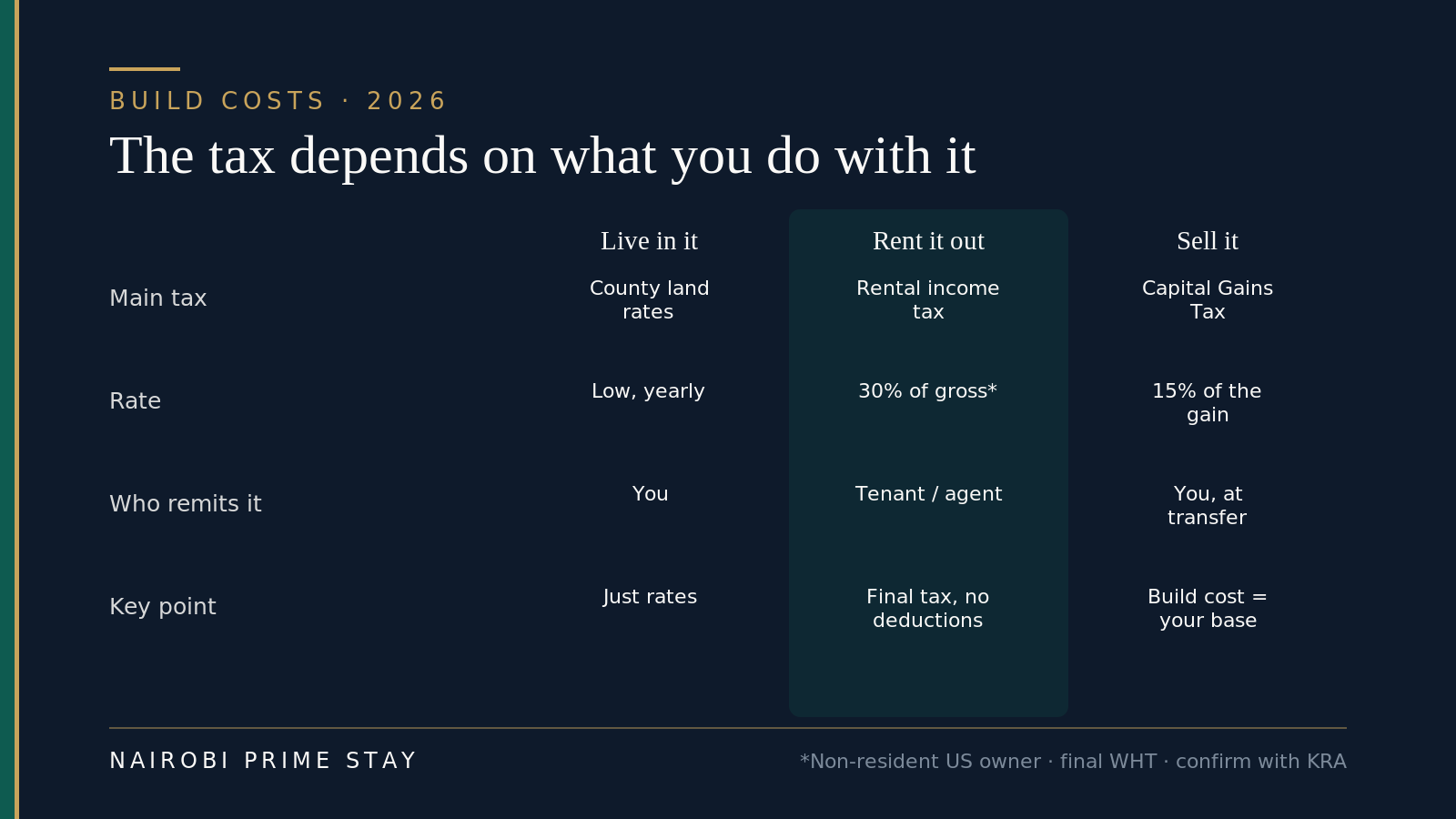

The tax side of building: living in it, renting it out, or selling

The tax you’ll owe on your finished house depends entirely on what you do with it — and for US-based owners there’s one number worth knowing before you break ground.

What you do with the house sets the tax. The rent-it-out figure surprises most US owners — confirm current rules with KRA.

What you do with the house sets the tax. The rent-it-out figure surprises most US owners — confirm current rules with KRA.

If you live in it, there’s no income tax on a home you occupy. You’ll pay annual county land rates and, in some areas, service charges — modest, ongoing, and nothing like a US property-tax bill. Stamp duty was already paid when you bought the land, not on the build.

If you rent it out, the tax is bigger than most expect. A US-based owner is a non-resident landlord, and Kenya taxes non-resident rental income at a flat 30% of gross rent — a final withholding tax, with no deductions, that your tenant or agent is meant to withhold and remit to KRA by the 20th of the following month. A Kenyan-resident landlord pays far less (residential rental income tax is 7.5%, with a proposed rise to 10% — confirm the current rate). Because there’s no comprehensive US–Kenya tax treaty, you can’t claim a reduced treaty rate, but you can usually take a US foreign tax credit (IRS Form 1116) so you’re not fully taxed twice. If a rental is the plan, read buy-to-let in Nairobi and property taxes in Kenya, and get cross-border tax advice early.

If you sell it, capital gains tax is 15% of the net gain (introduced at 5%, raised to 15% in 2023). Here’s where good build records pay off: your documented land cost plus the priced build — the Bill of Quantities, invoices and receipts — form your cost base, and a higher base means a smaller taxable gain. Keep every paper.

Building from abroad: the diaspora reality

You can build in Kenya without setting foot on the site — many do — but it’s exactly the scenario where money goes missing. Distance, trust and money moving across borders are catnip for the dishonest. Done right, it works; done casually, it’s a cautionary tale.

The single best cost control when you’re far away: an NCA-registered contractor working under independent professional supervision.

The single best cost control when you’re far away: an NCA-registered contractor working under independent professional supervision.

A few rules earn their keep:

- Appoint someone with legal authority. A power of attorney, drafted by a Kenyan lawyer, lets a trusted person sign and act for you — a US power of attorney must be notarized and consular-legalized, then registered in Kenya before it works (see conveyancing in Kenya). Define its limits tightly.

- Hire professionals, not just goodwill. An NCA-registered contractor under an architect or QS who supervises and certifies each stage is worth far more than a relative “keeping an eye on it.” Pay for the oversight.

- Put everything in writing. A detailed contract with milestones, a fixed scope priced off the BQ, a completion date with penalties, and a dispute clause. Even with family.

- Pay against verified progress. Release funds as an independent professional confirms each stage is done — never large sums up front, and never to a personal account you can’t verify by phone.

- See the site remotely. Insist on dated photos, video walk-throughs, and even drone footage at each milestone. Modern project tools make this easy and normal to ask for.

- Slow down on pressure. “Send the deposit today to lock the price” is the oldest line in the book. For more, read how property scams work in Kenya, and consider a property manager to run things on the ground.

Paying for a build from the US: money, currency and the $10,000 rule

Funding a build from America is mostly about moving money safely and not losing a chunk of it to the exchange rate. The mechanics are simple once you see them.

Move the bulk by transfer, release it against verified work, and keep the paper trail. Never wire lump sums to a personal account you can’t verify.

Move the bulk by transfer, release it against verified work, and keep the paper trail. Never wire lump sums to a personal account you can’t verify.

Move money by transfer, not cash. Wise, a bank wire or a diaspora remittance service moves USD into shillings cleanly, into either your own Kenyan account or your advocate’s client account — from which you release funds against certified milestones. Never wire a lump sum to a contractor’s or relative’s personal account you can’t verify by phone. See sending money to Kenya for the routes and their real costs.

Mind the currency drag. A build is priced in shillings but paid over 12–18 months, while your income is in dollars. At about KES 129.5 to the dollar in mid-2026 the shilling has been stable, but it doesn’t have to stay that way — budget the whole project at a slightly conservative rate, and move larger tranches when the rate suits rather than converting everything at the end. The USD/KES currency guide covers timing and how to hold the money.

The $10,000 rule and no exchange controls. Declare cash or monetary instruments over USD 10,000 (or the equivalent) when you enter or leave Kenya — that’s a reporting rule, not a limit. Kenya has no exchange controls, so you can bring build funds in freely and, if you sell later, convert shillings back and repatriate the proceeds, paying only the exchange spread. That freedom is a real advantage for diaspora property investors.

The honest pitfalls

Nobody who has built in Kenya will tell you it was smooth. Know the common failure modes:

- Cost overruns. The big one. Underestimated budgets, mid-build design changes and rising material prices push the average overrun toward 15%. The fix: a real BQ, a fixed-scope contract and a held-back contingency.

- Delays. Builds slip. Rain, cash-flow gaps and material shortages all add weeks. Plan for it and penalize it in the contract.

- Contractor trust. Cutting corners on materials, inflating quantities, or vanishing mid-build. Vetting, references, milestone payments and professional supervision are your defenses.

- Quality problems. Hidden later as cracks, leaks or failed finishes. Independent supervision and a snagging inspection before final payment catch most of them.

- Approval shortcuts. Tempting and common, and they come back to bite at sale or finance time. Don’t.

A realistic example

Say you’re a Kenyan-American in Atlanta who inherited a quarter-acre plot in Kitengela, on Nairobi’s southern edge, and wants a four-bedroom maisonette. You hire a Nairobi architect (found through references, not Facebook) and a quantity surveyor. The design is about 200 m²; the QS prices it at mid-range finishes for roughly KES 13–15 million, and you set aside another 12% as contingency.

You get county approval and confirm NEMA isn’t required for a single home of this size, then register the project and an NCA contractor. You sign a milestone contract with a completion date and a penalty clause, give your sister a narrow power of attorney, and pay your architect to supervise and certify each stage. Money releases against photos, drone footage and the architect’s sign-off — never ahead of the work. Eleven months later, after one rain delay and one finishes change that ate part of the contingency, you have a finished home that cost meaningfully less than buying the equivalent. That’s a build done right: professionals, paperwork, patience.

A build-it-right checklist

- Confirmed clean title, tenure and residential zoning on the land before spending

- Hired a registered architect and a structural engineer

- Commissioned a quantity surveyor and a priced Bill of Quantities

- Obtained county plan approval (and NEMA sign-off if required)

- Confirmed the contractor and project are NCA-registered

- Tendered the BQ and checked the contractor’s completed work and references

- Signed a detailed contract: scope, price, milestones, completion date, penalties, disputes

- Set aside a 10–15% contingency, treated as spent

- Arranged milestone-based payments tied to verified progress

- Lined up independent supervision (architect or QS), especially if building from abroad

- Put a lawyer-drafted power of attorney in place if I can’t be on site

- Budgeted land, fees, approvals, connections, finance and rent-while-building into the true cost

- Planned a snagging inspection and the occupation certificate before final payment

Final thoughts

Building in Kenya can deliver a better home for less money than buying — that part is real. What it asks in return is management: the right professionals, the right paperwork, a budget with slack, and the patience to pay only for work that’s actually done. Owners of land with time and oversight to give are the natural builders. If you need certainty, speed, or a home you don’t have to run as a project, buying — or a turnkey contract — is the honest, often smarter, choice.

Either way, don’t decide on per-square-metre headlines alone. Price your actual design with a quantity surveyor, weigh it against finished homes on the market, and be ruthless about the conditions: do you own the land, and can you manage the build? Answer those two honestly and the right path usually picks itself.

This is general guidance, not legal, financial or construction advice. Costs, fees and rules reflect 2026 and shift — confirm current figures with a licensed Kenyan architect, quantity surveyor, advocate and the relevant county, NEMA and NCA offices before you commit.

Related reading

- Property investing in Kenya — the cluster pillar tying land, tax, financing and returns together.

- Buying land in Kenya — get the plot right before you build a thing.

- How to buy property in Kenya — the full purchase process if you’d rather buy than build.

- Buying off-plan in Nairobi — a new-build someone else manages, with its own risks.

- Financing and mortgages in Kenya — construction loans, diaspora mortgages and the real all-in cost.

- Title deeds in Kenya and property scams in Kenya — protecting your land and your money.

- Property management in Nairobi — eyes on the ground when you can’t be there.

- Nairobi property prices — what finished homes cost, to weigh against building.

- Diaspora property investment in Kenya — the full playbook for buying and building from abroad.

- Taxes for expats in Kenya and sending money to Kenya — the money and tax side of a build.

- Moving to Nairobi — the complete relocation hub if you’re planning the bigger move.

Somewhere to live while you build

A build means months before you have keys — and you’ll want a secure, comfortable base to oversee it from. A serviced apartment gives you an all-inclusive home (Wi-Fi, cleaning, backup generator, 24/7 security) on flexible monthly terms, with no furniture or utility setup. Browse our serviced apartments in Nairobi, or let our AI relocation assistant match one near your plot in a couple of minutes. A $50 deposit reserves your place, and you pay the balance on arrival.

Frequently asked questions

Is it cheaper to build or buy a house in Kenya?

Building is usually cheaper than buying a comparable finished home - often by 20 to 30 percent - but mainly if you already own the land and you manage the build well. Buying wins when land is expensive where you want to live, or when you value price certainty and speed over a lower cost. Building also takes 6 to 12 months and carries real overrun risk, so the savings only hold if you can oversee the project and keep the budget in check.

How much does it cost to build a house in Kenya in 2026?

As of 2026, construction costs roughly KES 35,000 to KES 120,000 per square metre - about $270 to $920 - depending almost entirely on your finishes, with basic at KES 35,000-49,000, mid-range at KES 50,000-65,000, high-end at KES 70,000-95,000 and luxury at KES 100,000 and up. A basic three-bedroom house of about 100 to 120 square metres costs roughly KES 4.8 to 6 million to build, excluding land. These figures are a starting point - price your actual drawings with a quantity surveyor.

How long does it take to build a house in Kenya?

A standard house takes about 6 to 12 months to build once approvals are in hand, with simple bungalows near the short end and larger or custom homes running 12 to 16 months or more. Add a couple of months beforehand for design and approvals. Rain, material-price swings, labour availability and cash-flow gaps are the usual causes of delay, so build slack into the schedule and a penalty for late delivery into the contract.

Can foreigners and diaspora build a house in Kenya?

Yes. Kenyans abroad build regularly, and foreigners can build on land they are entitled to own - foreigners cannot own freehold or agricultural land but can hold leasehold and own apartments. The hard part is not eligibility but oversight: building remotely is exactly where money goes missing, so use a lawyer-drafted power of attorney, an NCA-registered contractor under independent supervision, and milestone payments against verified progress.

What approvals do I need to build a house in Kenya?

Three matter: county plan approval, where your registered architect and engineer submit stamped drawings to the county and pay an approval fee; NEMA environmental approval where required, charged at about 0.1% of project cost; and NCA registration, since your contractor and the project must be registered with the National Construction Authority before building. Skipping these can mean fines, demolition, or a house you cannot finance or cleanly sell, so do it properly.

How do I build a house in Kenya from abroad safely?

Appoint a trusted person with a narrow, lawyer-drafted power of attorney, hire an NCA-registered contractor working under an architect or quantity surveyor who certifies each stage, and sign a detailed written contract with milestones, a completion date and penalties. Pay only against verified progress, never large lump sums up front or to an unverified personal account, and insist on dated photos, video and even drone footage at each milestone. Treat any pressure to send money quickly as a reason to slow down.

How much contingency should I budget for building in Kenya?

Hold back 10 to 15 percent of the construction budget as contingency, because cost overruns on Kenyan builds average around 15 percent. Overruns come from underestimated budgets, mid-build design changes and rising material prices. Treat the contingency as already spent so you are not tempted to design up to it, and protect the rest with a priced Bill of Quantities and a fixed-scope contract.

Do I need an architect and a quantity surveyor to build?

Yes - they save more than they cost. A registered architect designs a home that works on your plot and meets the rules, a structural engineer designs the foundations and frame, and a quantity surveyor prepares the Bill of Quantities that becomes your budget, your tender document and your defense against being overcharged. Banks also require approved drawings and a BQ before they will finance a build, and skipping these professionals is a leading cause of blown budgets and quality problems.

How much do building materials cost in Kenya in 2026?

As of early 2026, a 50kg bag of ordinary cement runs about KES 750 in Nairobi, higher-grade 42.5 or premium cement KES 1,200 to 1,350, and structural steel roughly KES 95,000 to 120,000 per ton, with a D12 reinforcement bar near KES 1,020. Prices broadly steadied through late 2025 into 2026 after big swings earlier. Materials and labor are the bulk of a build, but the wide gap between cheap and expensive homes comes mostly from finishes - tiles, fittings, joinery and roofing - so price your actual specification rather than relying on averages.

Do I pay tax if I build a house in Kenya to rent it out?

Yes. A US-based owner is a non-resident landlord, and Kenya taxes non-resident rental income at a flat 30% of gross rent - a final withholding tax with no deductions that the tenant or agent remits to KRA. A Kenyan resident pays far less (7.5%, with a proposed rise to 10%). There is no comprehensive US-Kenya tax treaty, so you generally claim a US foreign tax credit rather than a reduced treaty rate. If you sell the house instead, capital gains tax is 15% of the gain, and your documented land and build costs form the cost base - so keep the Bill of Quantities and every invoice.

How do I pay for a build in Kenya from the US?

Move money by transfer - Wise, a bank wire or a diaspora remittance - into your own Kenyan shilling account or your advocate’s client account, then release funds against certified milestones. Never wire lump sums to a personal account you cannot verify. Declare cash or instruments over USD 10,000 when you enter or leave Kenya; there are no exchange controls, so funds move in freely and a later sale repatriates freely. Because a build is priced in shillings but paid over many months while you earn dollars, budget at a slightly conservative rate - around KES 129.5 to the dollar in mid-2026 - and move larger tranches when the rate suits.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.