Guides · Money

Taxes for Expats in Kenya: The 2026 Guide for Americans

Taxes for Expats in Kenya: The 2026 Guide for Americans

Here’s the part most people moving to Nairobi get wrong: as an American, you never have one tax system to think about. You have two. Kenya taxes what happens here, the US taxes you wherever you are, and there is no treaty between them to smooth the seam. That sounds alarming. It usually isn’t — but only if you set it up right from the start.

This guide is for Americans living in or moving to Nairobi: remote workers, people on a local salary, retirees, and anyone trying to work out what they actually owe. We’ll cover when Kenya starts taxing you, what its rates are, what remote pay from a US employer means here, and how your US filing keeps going no matter what.

One honest caveat up front: this is general guidance, not tax advice. Cross-border tax is the one area where a few hundred dollars spent on a professional saves you thousands and a lot of sleep. We’ll tell you exactly where the lines are blurry so you know which questions to ask.

TL;DR — what American expats owe in Kenya

Spend 183 days or more in Kenya in a calendar year (or keep a home here) and you become a Kenyan tax resident, taxed in principle on your worldwide income. Kenya’s income tax is progressive, from 10% up to 35%, with an automatic personal relief of KES 28,800 a year. You’ll need a KRA PIN (free, on iTax) and you file your annual return by 30 June.

Your US obligations don’t pause. US citizens and green-card holders file a Form 1040 every year on worldwide income, wherever they live. There is no US–Kenya tax treaty, so you lean on two tools instead: the Foreign Earned Income Exclusion (up to $132,900 of earned income for the 2026 tax year — but note the return you file in 2026 is your 2025 one, where the cap is $130,000) and the Foreign Tax Credit (credit for Kenyan tax you’ve paid). Add FBAR if your foreign accounts ever top $10,000. Done properly, you rarely pay tax twice — but you do file twice.

The numbers that shape an American’s tax life in Nairobi, as of 2026. Always confirm against KRA and the IRS.

The numbers that shape an American’s tax life in Nairobi, as of 2026. Always confirm against KRA and the IRS.

Why this matters before you move

Tax is the quiet thing that decides whether your Nairobi budget works. Get residency and timing right and the system is manageable. Get it wrong — assume “foreign income, so I owe nothing,” or forget you still file in the US — and you can face a surprise assessment, penalties, or double tax you could have avoided.

It also shapes practical choices: when you arrive in the year, whether you take a local contract or stay on US payroll, how you hold your money, and when to get a KRA PIN. None of it is hard. It just rewards planning over hoping.

Are you even a Kenyan taxpayer? The 183-day rule

You become a Kenyan tax resident the moment one of three things is true in a year of income (Kenya’s tax year is the calendar year, January to December):

- You have a permanent home in Kenya and you’re present here at any point in the year.

- You don’t have a permanent home here but you’re present for 183 days or more in that year.

- You’re present in the year and, averaged across that year and the two before it, you spend more than 122 days a year in Kenya.

The 183-day test is the one most movers hit. Cross it and KRA treats you as resident from your day of arrival, not from day 183. The “122-day average” rule catches frequent back-and-forth travellers who never stay long in one stretch but are clearly based here over time.

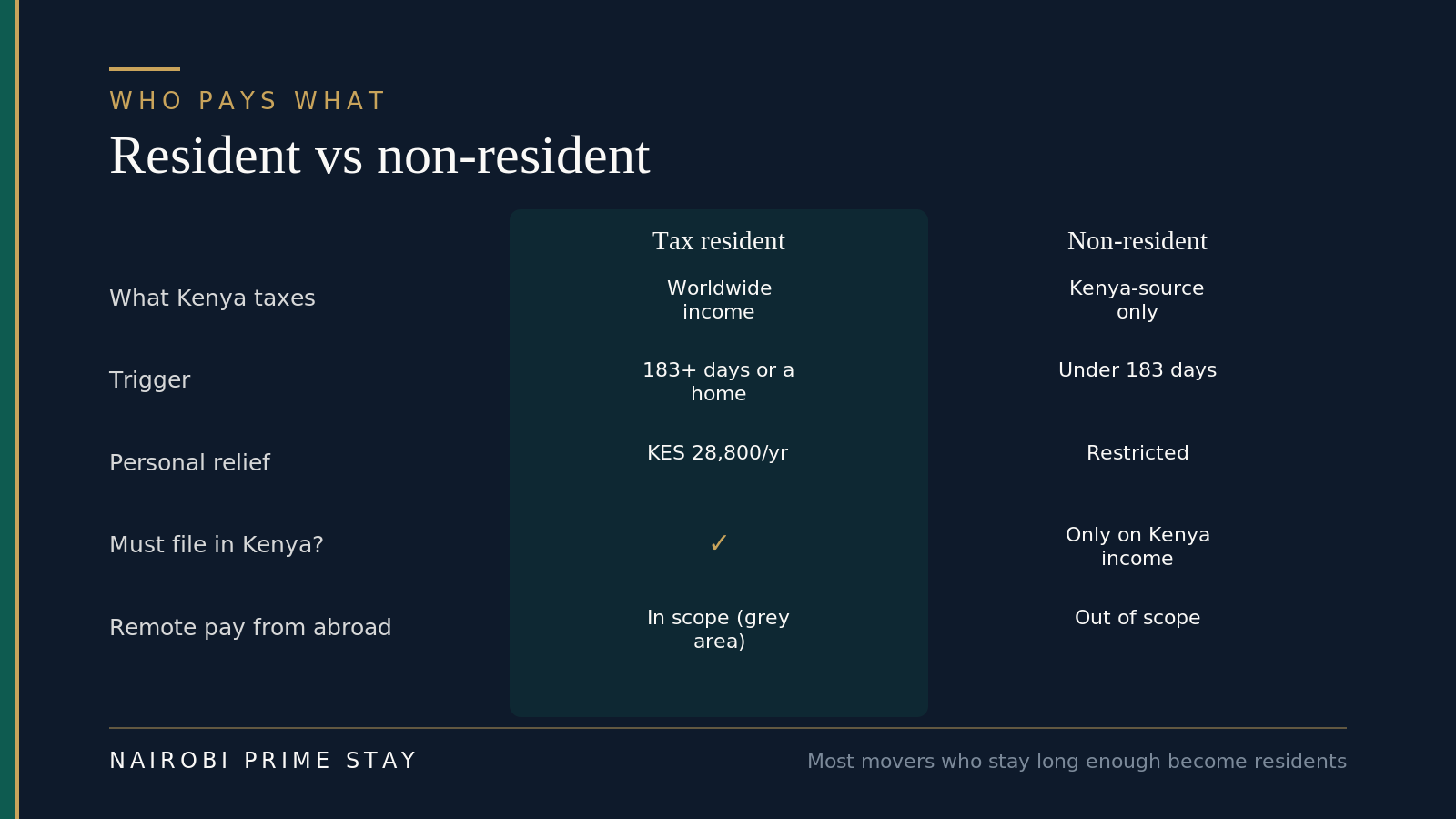

Why it matters so much: a resident is taxed on worldwide income; a non-resident is taxed only on income that’s accrued in or derived from Kenya. So the same salary can be fully in Kenya’s net or fully outside it, depending on one number — how many days you spent here.

Resident vs non-resident is the hinge the whole system turns on. Most people who actually move here become residents.

Resident vs non-resident is the hinge the whole system turns on. Most people who actually move here become residents.

If you’re only scouting on an eTA for a few weeks and then leaving, you’re a non-resident — Kenya isn’t taxing your US salary. If you settle in for the year, the calculus changes. Planning your arrival date around the calendar can matter: land in October and you may stay under 183 days for that first calendar year, which can ease your first-year position. A tax adviser can model this in an afternoon.

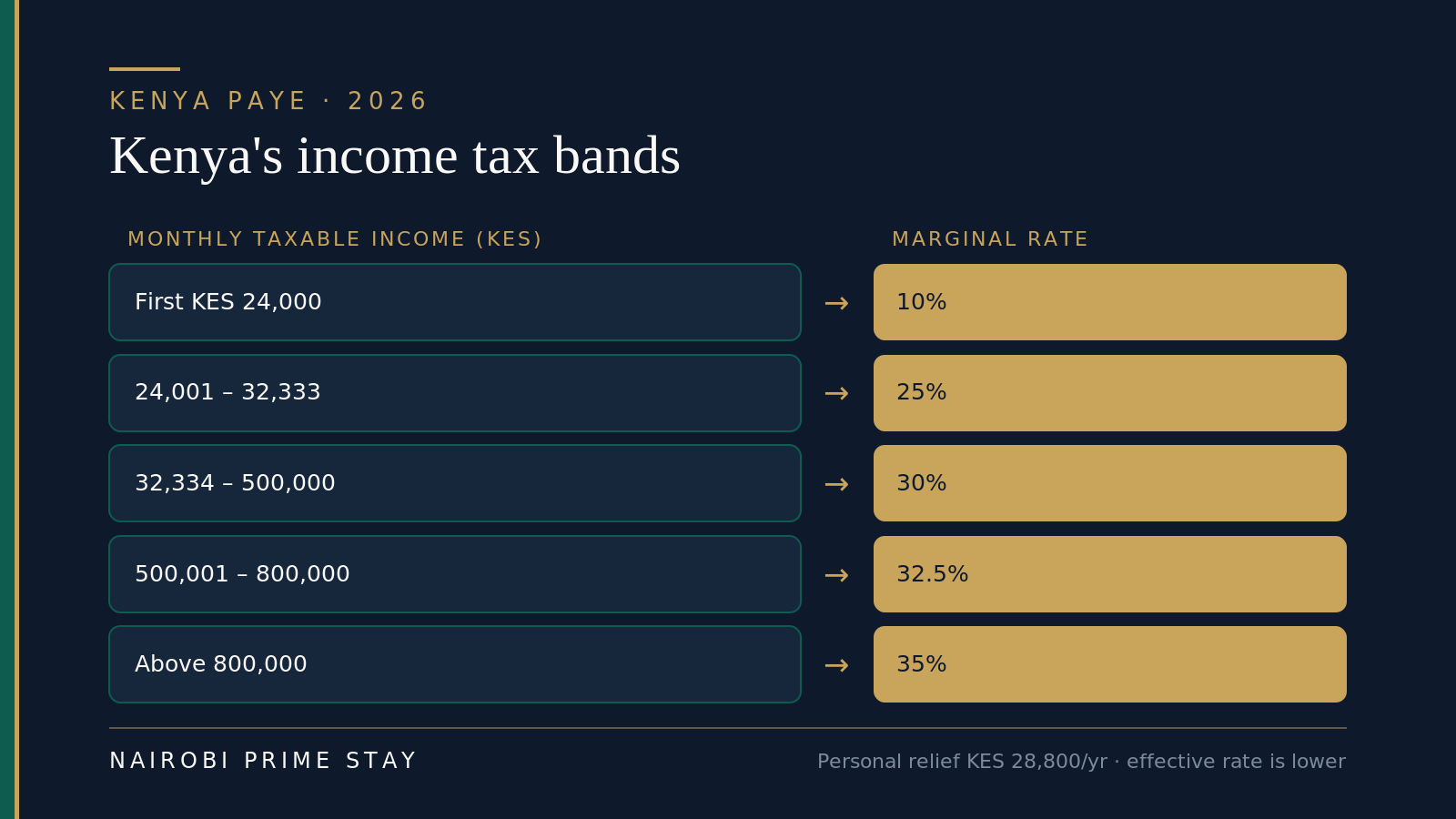

Kenya’s income tax: the bands, in plain numbers

Kenya runs a progressive PAYE (Pay As You Earn) system. The 2026 monthly bands, in force since 1 July 2023, are:

| Monthly taxable income (KES) | Marginal rate |

|---|---|

| First 24,000 | 10% |

| 24,001 – 32,333 | 25% |

| 32,334 – 500,000 | 30% |

| 500,001 – 800,000 | 32.5% |

| Above 800,000 | 35% |

Everyone resident gets a personal relief of KES 2,400 a month (KES 28,800 a year), knocked straight off the tax due. Because the bands are marginal, your effective rate is always lower than your top band — only the slice of income inside each band is taxed at that band’s rate.

Kenya’s marginal income tax bands for 2026. Verify the current figures on itax.kra.go.ke — Treasury has floated changes.

Kenya’s marginal income tax bands for 2026. Verify the current figures on itax.kra.go.ke — Treasury has floated changes.

A worked example, so the table feels real. Say you’re on a local Kenyan salary of KES 400,000 a month (roughly $3,100 at about 129.4 to the dollar). Your PAYE works out at roughly KES 112,000 a month before reliefs net out — about a 28% effective rate on gross. That’s the headline tax. On top, anyone on a Kenyan payroll also pays the Affordable Housing Levy (1.5% of gross) and SHIF, the health fund (2.75% of gross), plus NSSF pension contributions. So a local-contract take-home is meaningfully below gross — budget for it. One 2026 wrinkle worth knowing if you’re on a Kenyan payroll: KRA now lets you deduct your SHIF and NSSF contributions before PAYE is calculated, which softens the blow a little, but the housing-levy relief was repealed at the end of 2024, so that 1.5% no longer reduces your taxable pay.

One more figure worth knowing: KRA’s late-filing penalty is the higher of 5% of the tax due or KES 2,000, plus interest. Filing on time, even a nil return, is cheap insurance.

The KES 30,000 exemption that didn’t happen: accountants and the banking industry pushed hard during the Finance Bill 2026 process to lift the tax-free floor from KES 24,000 to KES 30,000 a month. In mid-2026 MPs rejected it, so the bands above stand unchanged. It’s a live debate that could return in a future Finance Bill, so confirm the current bands on itax.kra.go.ke before you rely on any number here.

What foreign-paid remote workers actually owe (the honest grey area)

This is the question we get most, and the honest answer has an asterisk. If you live in Nairobi but draw a salary from a US employer or US clients, what does Kenya want?

The clean rule first. While you’re a non-resident — under 183 days, no home here — your foreign-source income sits outside Kenya’s net. Many remote workers stop reading there and assume they’re tax-free. That’s only true until you cross 183 days.

Once you’re a resident, the default reading of Kenya’s rules — and the line KRA and most local tax advisers take in 2026 — is that you declare worldwide income, including remote pay from abroad. That’s the conservative, safer assumption to plan around.

Now the asterisk. The Class N digital nomad permit is new (Kenya opened applications in April 2025), and how it interacts with residency-based taxation isn’t fully settled. Some advisers argue genuinely foreign-source nomad income shouldn’t be taxed locally; the permit was pitched partly as a welcome mat. Others read the residency rules at face value. There’s no clean, tested answer yet, and KRA has been given broader powers to pursue employment and digital income. So:

- Don’t assume you owe nothing just because the money lands in a US account.

- Don’t assume you owe full PAYE either — your situation may differ.

- Do get a cross-border tax opinion before your first Kenyan filing, especially if you’re on the Class N permit or earning well into the higher bands.

The reassuring part: even in the worst case, where Kenya taxes your remote income in full, you generally don’t pay twice. The Kenyan tax you pay becomes a credit against your US tax (more on that below). The risk isn’t double tax — it’s getting surprised by a Kenyan bill you didn’t budget for, or missing a filing. Both are avoidable.

For context on the remote-work setup itself — fibre, backup power, time-zone overlap — see our guide to internet and remote work in Nairobi.

Getting set up: your KRA PIN, iTax and the filing calendar

Your first practical step is a KRA PIN — Kenya’s tax ID. It’s free, you get it on the iTax portal (itax.kra.go.ke), and you’ll need it for almost everything: opening a bank account, signing a lease, buying a car, setting up utilities. Foreigners usually register the PIN once they hold a permit or pass; the portal asks for your immigration details, and a KRA-registered tax agent often provides a short introduction letter to get a foreigner’s PIN issued.

After that, the rhythm is simple:

The yearly cycle. Kenya’s tax year is the calendar year; returns are due the following 30 June.

The yearly cycle. Kenya’s tax year is the calendar year; returns are due the following 30 June.

- Get the PIN once you have a permit/pass.

- Keep records through the year — payslips, bank statements, any Kenyan tax withheld, and what you paid Kenya so you can claim it back on the US side.

- File your individual return on iTax after year-end. Even with nothing to pay, file a nil return — skipping it triggers penalties.

- Pay any balance by 30 June. KRA has been firm that the deadline doesn’t move.

- Then handle the US side — your 1040, and a Foreign Tax Credit for whatever Kenya took.

If you’re employed by a Kenyan company (a Class D work permit), your employer runs PAYE for you monthly and much of this is automatic. If you’re self-employed or on foreign payroll, the responsibility — and the record-keeping — is yours.

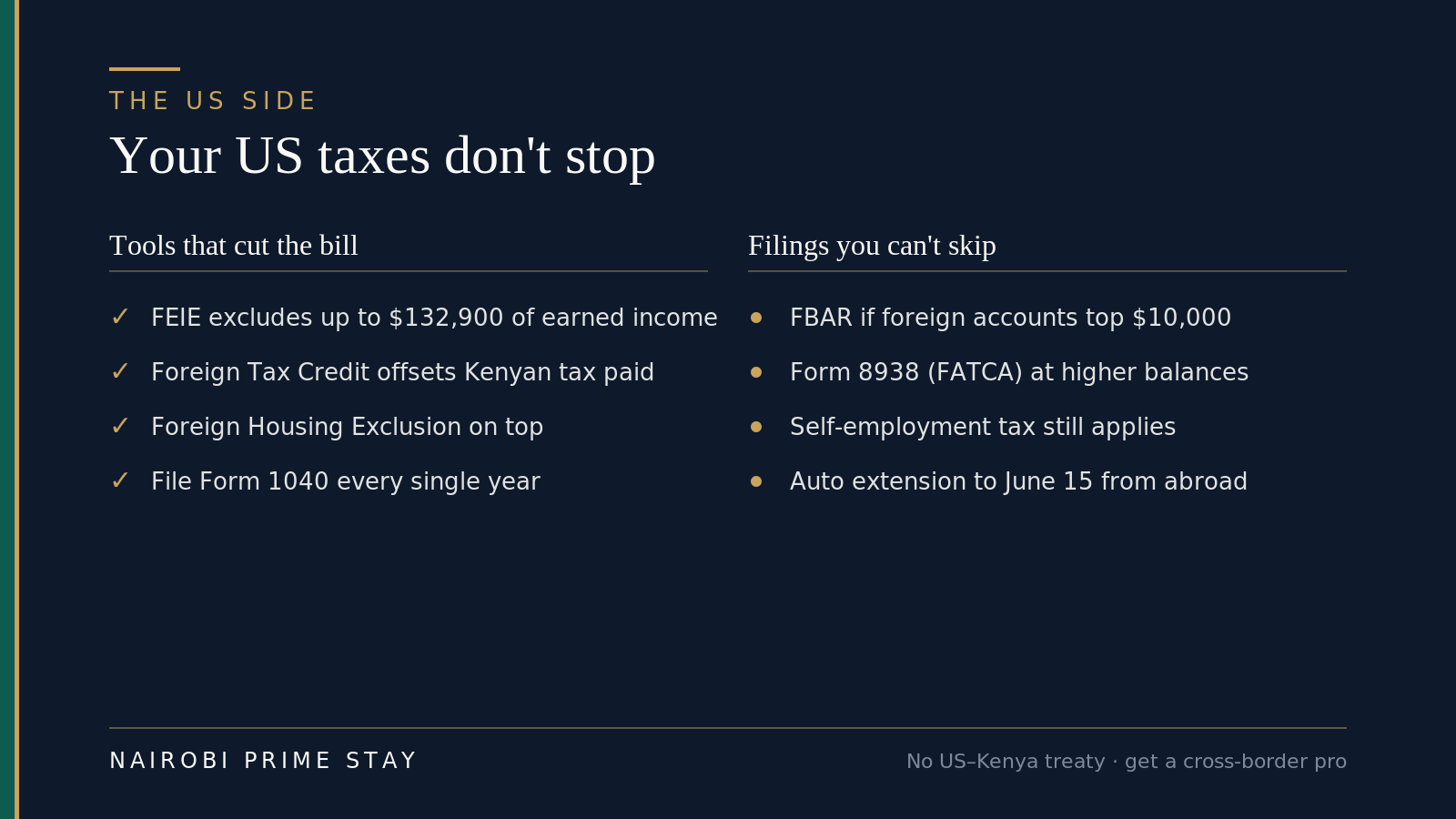

Your US taxes don’t stop — what Uncle Sam still wants

This surprises people every year, so it’s worth stating plainly: the US taxes its citizens and green-card holders on worldwide income, no matter where they live. Moving to Nairobi doesn’t end your US filing. You file a Form 1040 every year, reporting what you earn globally — including your Kenyan salary if you take one.

The good news is a set of tools that, used together, usually wipe out actual US tax owed:

- Foreign Earned Income Exclusion (FEIE, Form 2555). Exclude up to $132,900 of foreign earned income in 2026 (wages, self-employment) from US tax. You qualify by passing either the physical presence test (330 full days abroad in a 12-month window) or the bona fide residence test. It covers earned income only — not dividends, interest, capital gains, or most rental income.

- Foreign Tax Credit (FTC, Form 1116). A dollar-for-dollar credit for income tax you’ve paid to Kenya. This is your main shield if you’re a Kenyan resident actually paying KRA — Kenya’s rates are high enough that the credit often covers any remaining US tax on the same income.

- Foreign Housing Exclusion/Deduction. On top of the FEIE, you can exclude part of your housing costs above a base amount — useful given Nairobi rents.

The exclusions cut what you owe; the information forms are mandatory whether or not you owe a cent.

The exclusions cut what you owe; the information forms are mandatory whether or not you owe a cent.

Then the information forms — separate from your tax, and easy to forget:

- FBAR (FinCEN Form 114). If your foreign financial accounts add up to more than $10,000 at any single moment in the year, you report them. It’s filed online with the Treasury, not the IRS, and the penalties for skipping it are steep. Your Kenyan bank account and M-Pesa balance both count.

- FATCA (Form 8938). Filed with your 1040 if your foreign assets pass higher thresholds — from $200,000 on the last day of the year for a single filer living abroad, more for joint filers.

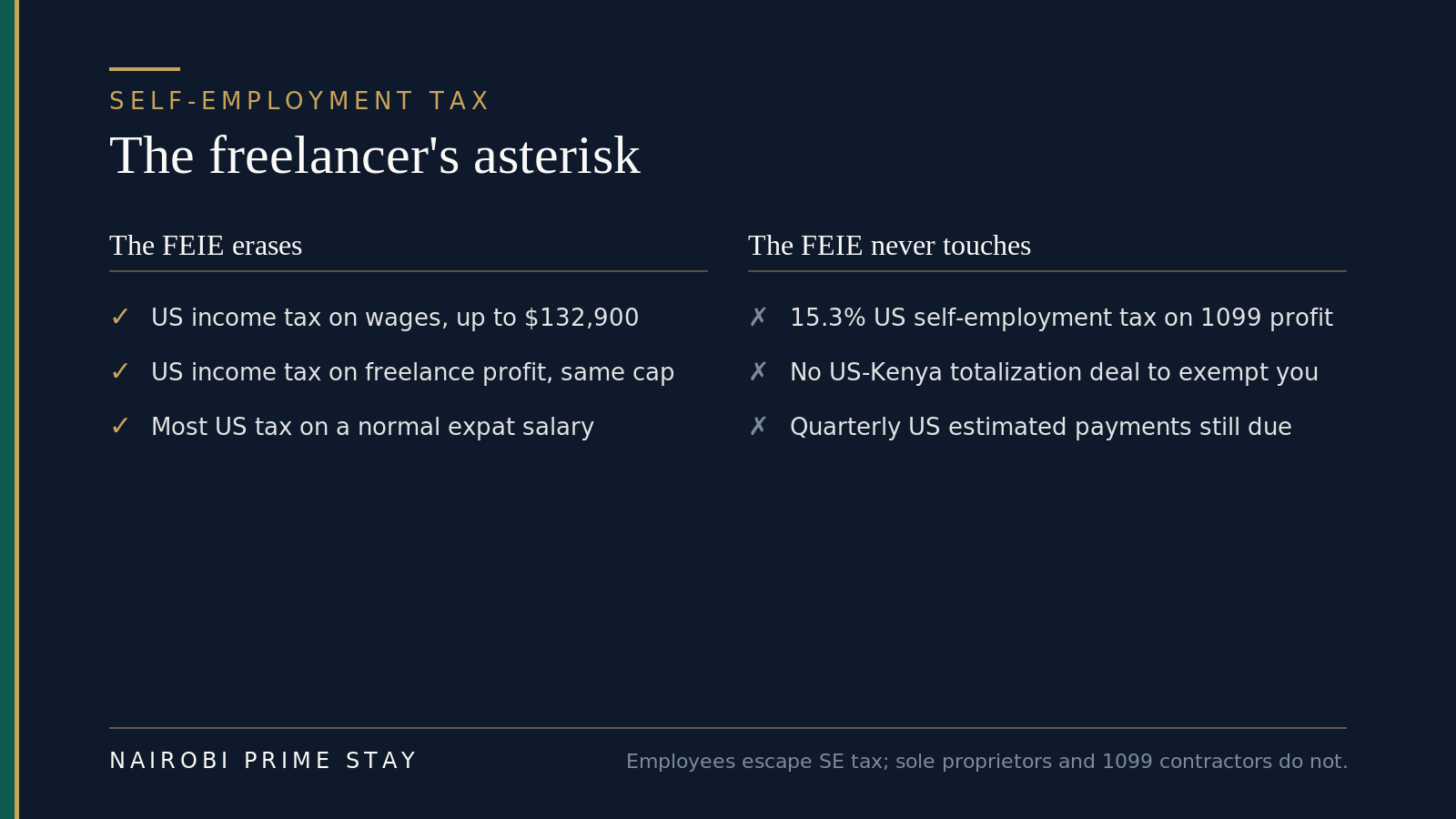

- Self-employment tax. If you freelance, the FEIE doesn’t touch the 15.3% US self-employment tax — there’s no US–Kenya social-security totalization agreement to exempt you. Budget for it.

Two timing notes: expats get an automatic extension to June 15 to file (you can push to October 15), and some US states keep taxing you until you formally cut ties — check your last state of residence.

The self-employment tax trap for freelancers

If you’re a US employee — on a W-2, or on a Kenyan company’s payroll — you can skip this section. If you freelance, contract, or run your own LLC, read it twice, because it’s the single most common surprise on an American expat’s return.

The Foreign Earned Income Exclusion is generous with your income tax. It does nothing for self-employment tax — the 15.3% that covers Social Security and Medicare on your net self-employment profit. You can exclude every dollar of a $120,000 freelance income from US income tax with the FEIE and still owe roughly $18,000 in SE tax on it. The exclusion simply doesn’t reach that far.

Normally, a tax treaty’s “totalization agreement” would let you pay into one country’s social-security system instead of both. The US and Kenya have no totalization agreement, so there’s no way to swap your US SE tax for Kenyan NSSF. You pay the US SE tax, full stop.

The FEIE is a shield against income tax, not self-employment tax. Freelancers feel the difference.

The FEIE is a shield against income tax, not self-employment tax. Freelancers feel the difference.

Two practical moves soften it. First, because no employer is withholding for you, the IRS expects quarterly estimated payments — miss them and you face an underpayment penalty on top of the bill. Second, some higher-earning freelancers form an S-corporation and pay themselves a “reasonable salary,” which can cut the base that SE tax applies to; whether it’s worth the cost and paperwork is exactly the kind of question a cross-border preparer earns their fee answering. Don’t DIY the S-corp decision.

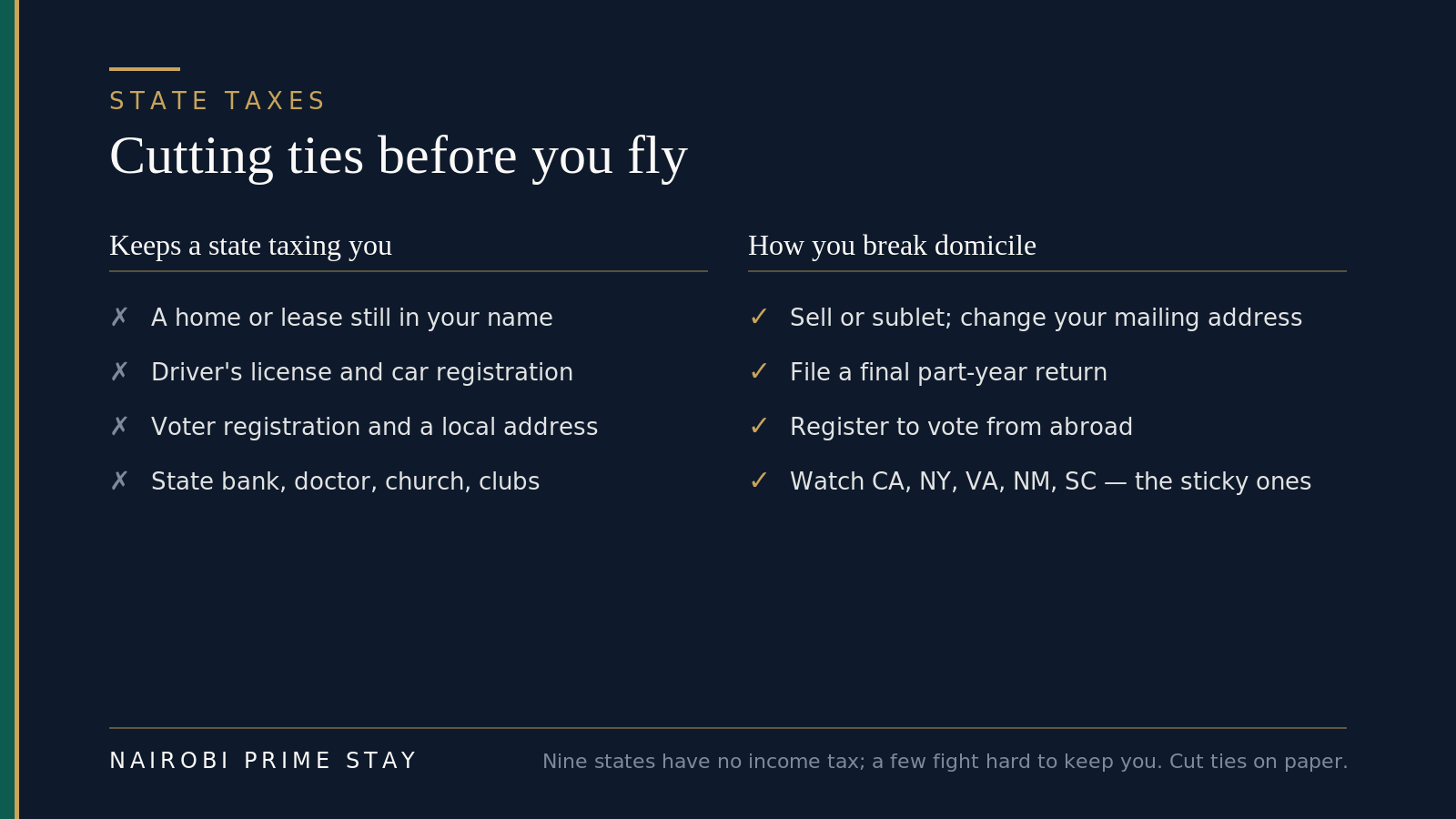

Don’t forget your old state — the residency tail

Federal tax is only half the US picture. Your state may keep taxing you long after you’ve landed in Nairobi, because most states tax on domicile — your true, fixed home — not on where you physically are. Moving abroad doesn’t automatically end it. You have to actively cut ties.

Some states let go easily. Nine — including Texas, Florida, Washington and Nevada — have no personal income tax at all, so there’s nothing to escape. A handful of others are famously sticky: California, New York, Virginia, New Mexico and South Carolina are known for treating a move abroad as “temporary” and continuing to bill you until you’ve clearly broken domicile.

Breaking state domicile is about paper trails. Cut the ties before you fly, not after.

Breaking state domicile is about paper trails. Cut the ties before you fly, not after.

Before you leave, do the unglamorous admin: change your mailing address off your old state, wind down a lease or rent out the house, move your voter registration, and file a final part-year return that marks the date you left. Keep evidence of your Nairobi life — lease, KRA PIN, utility bills. If your last state is one of the sticky ones, this is another five-minute question for your preparer that can save a multi-year headache.

Your two-country tax calendar

The deadlines that trip people up are the ones that don’t line up. Kenya runs a January-to-December tax year; the US runs its own calendar with expat-specific extensions layered on top. Hold both in view at once:

Two calendars, one year. Note how Kenya’s 30 June deadline sits right beside the US June 15 extension — plan for both in the same fortnight.

Two calendars, one year. Note how Kenya’s 30 June deadline sits right beside the US June 15 extension — plan for both in the same fortnight.

The one to circle is 30 June — KRA’s individual filing deadline, and it doesn’t move. It happens to land two weeks after your automatic US filing extension (June 15), so early summer is your busy tax fortnight in Nairobi. Get your records in order in May and neither one sneaks up on you.

How the two systems stack without a treaty

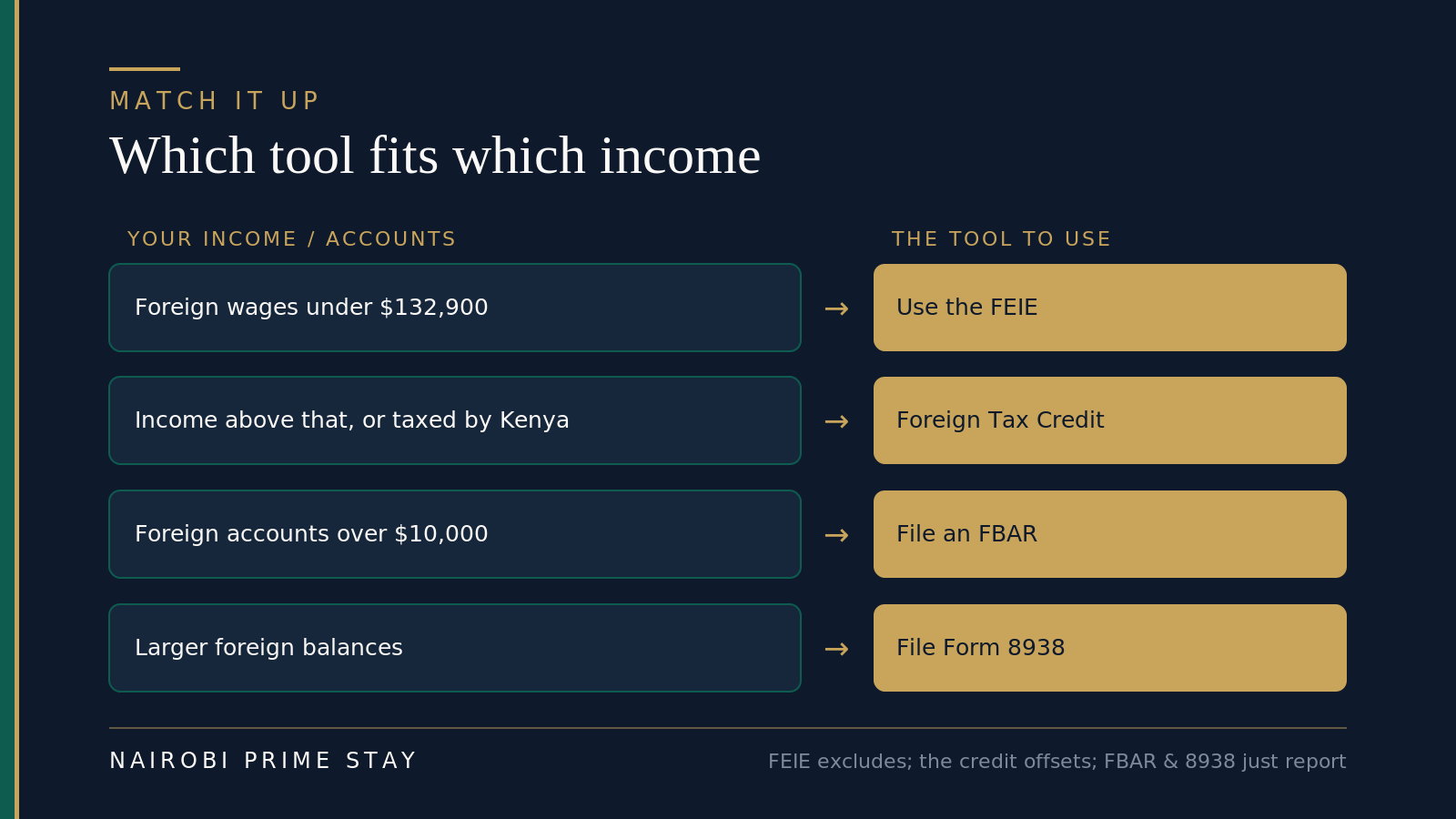

Here’s the thing the “no treaty” headline gets wrong. No treaty doesn’t mean you’re taxed twice on everything. It means you don’t get a treaty’s tidy tie-breakers — instead you stack the exclusion and the credit to reach roughly the same place.

In practice, for most American remote workers in Nairobi:

- FEIE first. If your earned income is under $132,900 and you pass the presence test, the exclusion alone can zero out your US income tax on that salary.

- FTC on the rest. Earn more than the exclusion, or owe Kenyan tax on the same money? The Foreign Tax Credit offsets your US bill with what you paid Kenya. Because Kenya’s top rates (30–35%) sit above many US brackets, the credit frequently covers the remainder.

- What’s left over is usually US tax on passive income — US dividends, interest, capital gains — which neither tool fully shelters. That’s normal, and usually small.

A rough map of which tool fits which kind of income. A cross-border preparer fits them to your real numbers.

A rough map of which tool fits which kind of income. A cross-border preparer fits them to your real numbers.

The takeaway: the no-treaty gap is mostly a paperwork problem, not a double-tax problem — provided you file both sides correctly and on time.

A realistic scenario

Maya, a US software engineer, moves to Nairobi on the Class N permit. She earns about $95,000 a year, paid by her US employer into a US account, and rents a furnished two-bed in Kilimani. She plans to stay two years.

Year one, she arrives in March, so she’s in Kenya well past 183 days — a Kenyan tax resident from arrival. That puts her remote salary, in principle, within Kenya’s net (the grey area we flagged), so she gets a KRA PIN and a local tax adviser before her first 30 June filing. Whatever Kenyan tax she ends up paying, she logs it carefully.

On the US side, she files her 1040, claims the FEIE to exclude the bulk of her $95,000, and uses the Foreign Tax Credit for any Kenyan tax on top — so she pays the US almost nothing on that salary, but still files. She files an FBAR because her Kenyan account and M-Pesa together cross $10,000 mid-year. Total extra US tax: roughly zero. Total peace of mind: high, because nothing’s hidden and nothing’s late.

Her one real cost beyond the tax itself? A few hundred dollars for a preparer who knows both systems. Money well spent.

Resident vs non-resident: a side-by-side

| Kenyan tax resident | Non-resident | |

|---|---|---|

| Trigger | 183+ days in the year, a home in Kenya, or the 122-day average | Under 183 days, no home here |

| What Kenya taxes | Worldwide income (in principle) | Only Kenya-source income |

| Personal relief | KES 28,800/year | Restricted |

| Files a KRA return? | Yes, by 30 June | Only if you have Kenya-source income |

| US filing | Still required (1040, FBAR, etc.) | Still required |

| Main US tools | FEIE + Foreign Tax Credit | FEIE if you qualify abroad |

The honest balance

| What’s easy about it | What to watch |

|---|---|

| KRA PIN is free and quick on iTax | Foreign remote-income treatment is a genuine grey area |

| FEIE often zeroes out US tax on a normal salary | No US–Kenya treaty means more forms, not fewer |

| The Foreign Tax Credit stops most double taxation | FBAR/FATCA are easy to forget and costly to miss |

| One clear Kenyan deadline: 30 June | Self-employment tax (15.3%) isn’t excluded by FEIE |

| English-speaking advisers and online filing | Kenyan rates are high (up to 35%) once you’re resident |

Your expat-tax checklist

- Count your days — know whether you’ll cross 183 this calendar year.

- Plan your arrival month if your first-year residency is close to the line.

- Get a KRA PIN on itax.kra.go.ke once you hold a permit or pass.

- Line up a cross-border tax adviser before your first filing — especially on Class N.

- Keep a running file of payslips, Kenyan tax paid, and account statements.

- Register on iTax and file your Kenyan return (even a nil one) by 30 June.

- File your US 1040; claim the FEIE and/or Foreign Tax Credit.

- File an FBAR if foreign accounts ever top $10,000; check if Form 8938 applies.

- Check whether your old US state still considers you a resident.

- Re-confirm every figure here against KRA and the IRS — rules move.

Frequently asked questions

Do American expats pay tax in Kenya?

Yes, if you become a Kenyan tax resident, which happens once you spend 183 days or more in Kenya in a calendar year or keep a permanent home here. Residents are taxed on worldwide income; people who stay under 183 days are taxed only on Kenya-source income. Either way, you keep filing US taxes.

What is the 183-day rule in Kenya?

It is Kenya’s main tax-residency test. Spend 183 days or more in Kenya during the calendar year and you are treated as a tax resident from your day of arrival. A separate rule catches people who average more than 122 days a year across three years. Residency decides whether Kenya taxes your worldwide income or only local income.

Is there a double-tax treaty between the US and Kenya?

No. There is no income tax treaty between the United States and Kenya as of 2026. You avoid double taxation instead by using US provisions, mainly the Foreign Earned Income Exclusion and the Foreign Tax Credit, which usually offset most or all of the overlap. It means more forms, not necessarily more tax.

Do I owe Kenyan tax on a salary paid by my US employer?

While you are a non-resident, no, because foreign-source income sits outside Kenya’s net. Once you become a resident by passing 183 days, the default reading is that your worldwide income, including remote pay, is in scope. How this applies to Class N digital nomad permit holders is not fully settled, so get a cross-border tax opinion before your first filing.

What are Kenya’s income tax rates in 2026?

Kenya’s PAYE is progressive: 10% on the first KES 24,000 a month, 25% to KES 32,333, 30% to KES 500,000, 32.5% to KES 800,000, and 35% above that. Every resident gets a personal relief of KES 28,800 a year. Because the bands are marginal, your effective rate is lower than your top band.

How do I get a KRA PIN as a foreigner?

Register free on the iTax portal at itax.kra.go.ke once you hold a work permit or pass. The portal asks for your immigration details, and a KRA-registered tax agent often supplies a short introduction letter for a foreigner’s PIN. You need the PIN to open a bank account, sign a lease, or buy a car.

When is the Kenyan tax return due?

Individual returns are due by 30 June following the calendar tax year, filed on iTax. File even if you owe nothing, because a nil return avoids penalties. Late filing costs the higher of 5% of the tax due or KES 2,000, plus interest.

Do I still have to file US taxes while living in Nairobi?

Yes. US citizens and green-card holders file a Form 1040 on worldwide income every year, wherever they live. You also file an FBAR if your foreign accounts top $10,000 at any point, and possibly Form 8938. Expats get an automatic extension to June 15, and the FEIE and Foreign Tax Credit usually cut the actual tax owed to little or nothing.

Will I be taxed twice on the same income?

Rarely, if you file correctly. The Foreign Earned Income Exclusion can remove up to $132,900 of earned income from US tax in 2026, and the Foreign Tax Credit offsets your US bill with Kenyan tax you have already paid. Even without a treaty, these usually prevent genuine double taxation. The cost is paperwork and a good preparer, not a double bill.

Do freelancers pay US self-employment tax while living in Kenya?

Yes. The Foreign Earned Income Exclusion wipes out US income tax on your earned income up to $132,900, but it does not touch the 15.3% US self-employment tax on your net freelance profit. Because there is no US-Kenya totalization agreement, you cannot swap it for Kenyan NSSF. Budget for the SE tax and make quarterly estimated payments to avoid penalties.

Do I still owe US state taxes after moving to Kenya?

Maybe. Most states tax on domicile, so a move abroad does not automatically end your state filing. Nine states have no income tax, but a few — California, New York, Virginia, New Mexico and South Carolina — are sticky and keep billing you until you clearly break domicile. Cut ties before you go: change your mailing address, end leases, move your voter registration, and file a final part-year return.

Is the Foreign Earned Income Exclusion $130,000 or $132,900?

It depends on which tax year. The exclusion is $132,900 for the 2026 tax year, which you file in early 2027. The return you file in 2026 covers 2025 income, where the cap is $130,000. The IRS raises the figure each year for inflation, so always match the number to the year you are actually filing.

Final thoughts

Two systems, no treaty — it sounds heavier than it is. In practice, the work is mostly bookkeeping: know your day count, get a KRA PIN, file on both sides, and keep the receipts that let the Foreign Tax Credit do its job. Do that and you’ll almost never pay tax twice.

The one place not to cut corners is advice. Cross-border tax is full of edge cases — the digital-nomad grey area, state-residency tails, self-employment tax — where a professional pays for themselves many times over. Treat the few hundred dollars as part of your moving cost, like shipping or a deposit.

And the figures here move. Kenyan bands, the US exclusion amount, and the rules around new permits all change. Use this as your map, then confirm the live numbers with KRA and the IRS before you act. This is general guidance, not legal or tax advice.

Related reading

- Moving to Nairobi: the complete guide — the hub that ties visas, money, housing and healthcare together.

- Kenya visas for Americans — the eTA, the Class N digital nomad permit and the work routes.

- Banking in Nairobi and opening a Kenyan bank account as a foreigner — what you need, including your KRA PIN.

- Sending money to Kenya — moving dollars to shillings without losing money to fees.

- Property taxes in Kenya — if you’re buying, the separate set of levies that apply.

- Cost of living in Nairobi — build your real monthly budget around take-home numbers.

- Internet and remote work in Nairobi — the setup side of working from here.

When you’re ready to land softly

Sorting out tax is easier when you’re not also scrambling for somewhere to live. A serviced apartment for your first month gives you a secure, all-inclusive base — Wi-Fi, cleaning, backup power and security included — while you get your KRA PIN, open a bank account and find a longer-term home. Browse our serviced apartments, or tell our AI relocation assistant your timeline and budget and it’ll shortlist options in a couple of minutes.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.