Guides · Property investment

Buy-to-Let in Nairobi: Rental Yields and the Real ROI (2026)

Buy-to-Let in Nairobi: Rental Yields and the Real ROI (2026)

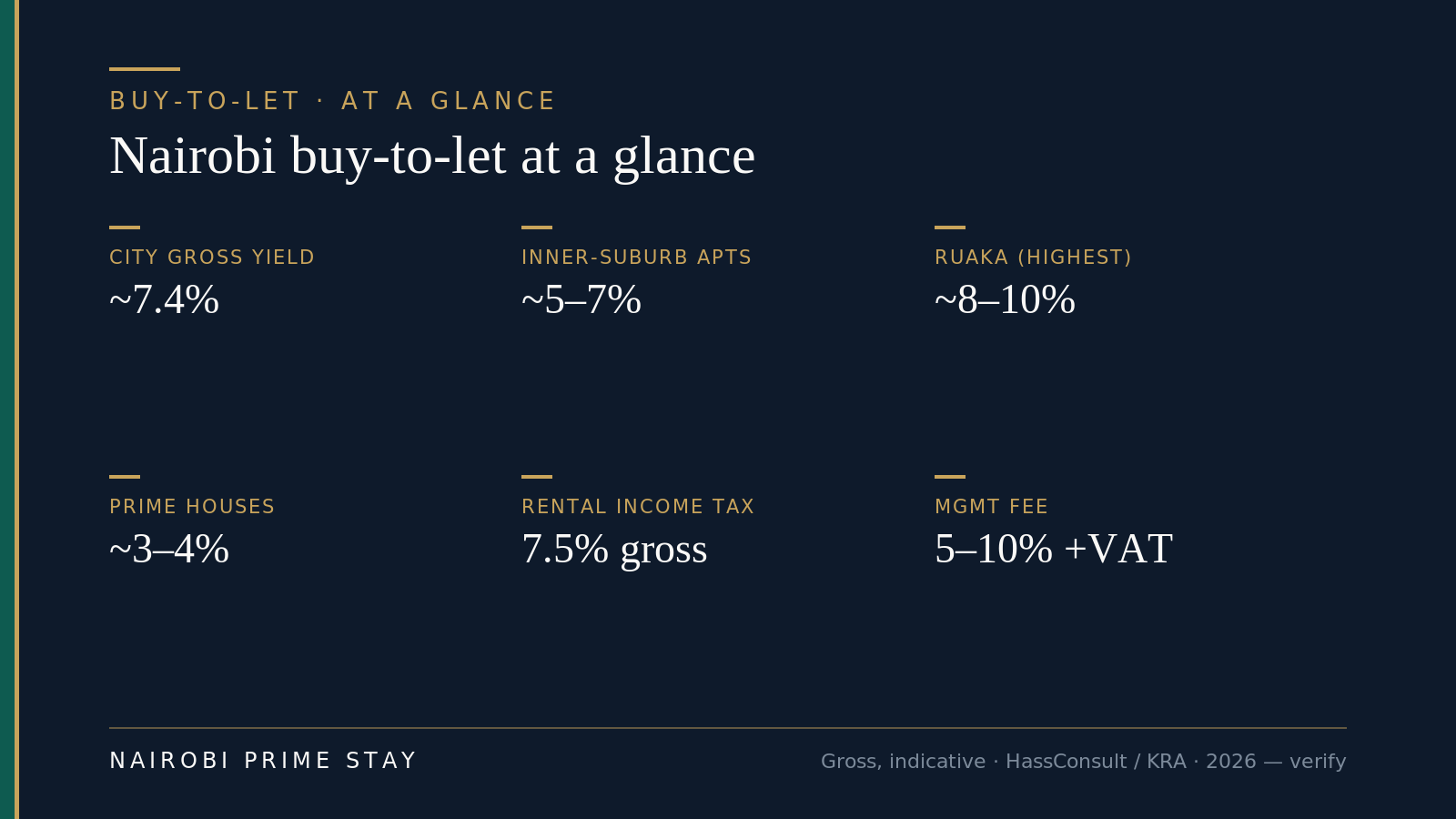

A well-bought Nairobi apartment earns a gross rental yield of about 5% to 7.5% a year, and a bit more in a few high-demand pockets like Ruaka. After costs and tax, the figure you actually keep — the net yield — is usually around 2 to 3 points lower, so think 4% to 5% on a typical prime apartment. That’s a decent income return by global standards, but it’s not the 10% some agents quote. The trick is knowing the difference between the headline number and the money in your pocket.

This guide shows you how to work out both, gives honest 2026 yields by area and property type, lists every cost that quietly eats your return, and walks through a full worked example on a real-world Kilimani two-bed. It’s written for Americans and diaspora buyers who want rental income from Nairobi, whether you plan to let long-term, furnish for corporates, or run a short-let.

Short version: buy-to-let in Nairobi can work, but only if you run the net numbers before you buy, pick an area with deep tenant demand, and budget for the costs most first-time landlords forget. The prettiest unit rarely gives the best return — and gross yield, on its own, is a half-truth.

TL;DR — buy-to-let in Nairobi (2026)

Gross rental yields run about 5–7.5% on most prime Nairobi apartments, roughly 7.4% city-wide (the highest since 2007), up to 7–10% in a few hot spots like Ruaka, and as low as 3–4% on big prestige houses in Karen or the diplomatic belt. Net yield — after management, rental-income tax, service charge, rates, vacancy and repairs — is usually 2 to 3 points lower, so a 7.7% gross apartment nets around 4.9%. Residential rental income is taxed at 7.5% of gross rent as of mid-2026, with a Finance Bill 2026 proposal to raise it to 10% from 1 July 2026 — so it may be rising right now; confirm the live rate with KRA. If you live in the US you’re a non-resident landlord, taxed at a flat 30% of gross rent instead, which is the single biggest thing that changes your real return. Furnished and short-let earn more rent but cost more and sit empty more often. For most absentee or diaspora owners, a licensed manager taking 5–10% plus VAT is worth it. Treat every figure as “as of 2026” and verify against HassConsult, Cytonn and KRA.

Why this matters

Rental yield is the single number that tells you whether a Nairobi apartment is an investment or a trophy. Two units bought for the same price can deliver very different income depending on area, finish and how you let them. Get it right and the rent covers your costs and pays you a real return; get it wrong and you’re topping up a service-charge bill on an empty flat.

It matters more here than in the US because the market is less transparent. There’s no MLS, no public record of what rents were actually achieved, and parts of the city are oversupplied with new apartments chasing the same tenants. A glossy brochure yield means nothing until you’ve subtracted the costs and stress-tested the vacancy. This guide is the honest version of that math. For the bigger picture on the whole investment, start with our complete guide to property investment in Kenya; for where the demand actually is, see the best areas to invest in Nairobi.

Gross yield vs net yield: read both

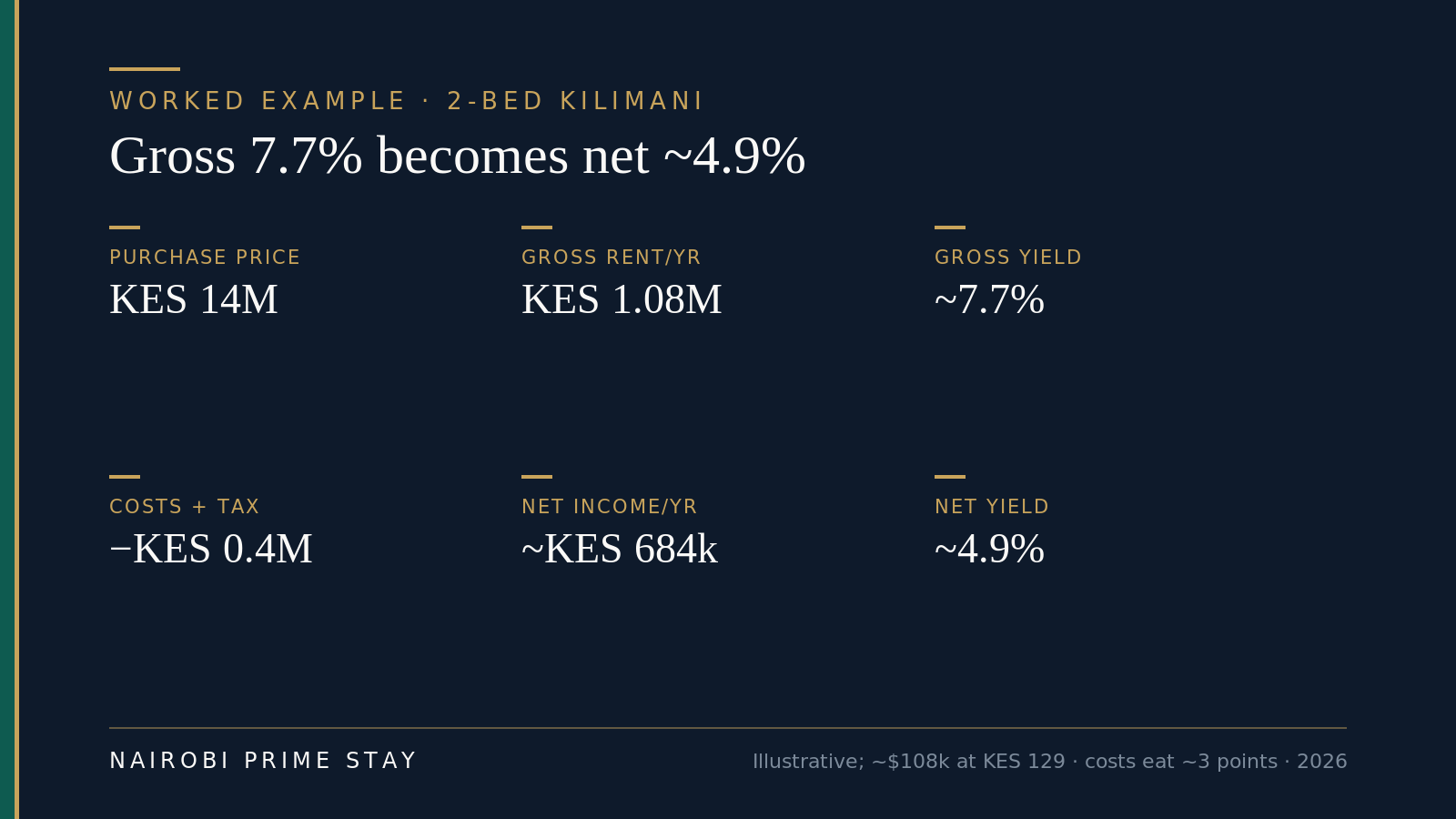

Gross yield is annual rent divided by the purchase price, before any costs. If you pay KES 14 million for an apartment and rent it for KES 90,000 a month — KES 1,080,000 a year — your gross yield is about 7.7%. It’s the number you’ll see in every listing and pitch, because it’s the flattering one.

Net yield is what’s left after the running costs, divided by the total you actually invested. Take the same flat, subtract management, rental-income tax, service charge, land rates, repairs and a month of vacancy, and divide by the price plus your buying costs. The net yield on that apartment lands closer to 4.9%. That’s the number that pays you.

Always work out net yield before you buy. The formulas are simple:

- Gross yield = (annual rent ÷ purchase price) × 100

- Net yield = (annual rent − annual running costs) ÷ (purchase price + buying costs) × 100

The denominator matters too. Buying costs in Kenya add roughly 5–8% on top of the price — stamp duty at 4% in towns, legal fees, valuation and registration — so your real capital outlay is bigger than the sticker. We break those down in the property taxes guide. Use the full figure, or your net yield will flatter you.

Indicative 2026 figures — gross yields and headline costs. Verify against HassConsult, Cytonn and KRA.

Indicative 2026 figures — gross yields and headline costs. Verify against HassConsult, Cytonn and KRA.

What yields can you actually get in Nairobi?

Yields vary more by area and property type than almost anything else. Smaller, well-located apartments with deep tenant demand earn the most. Big prestige houses earn the least — they tie up huge capital for modest rent. Here’s the honest 2026 picture, gross, drawn from HassConsult’s index, Cytonn’s reports and live listings.

| Segment / area | Indicative price | Typical monthly rent | Gross yield | Notes |

|---|---|---|---|---|

| 2-bed apartment, Kilimani | KES 10–16M | KES 70–110k | ~5.5–7.5% | Deep tenant pool, easy to let; watch new-build supply |

| 2-bed apartment, Kileleshwa | KES 11–18M | KES 80–130k | ~6–8% | Quieter, central, strong demand |

| 1–2 bed apartment, Ruaka | KES 5–11M | KES 45–80k | ~7–10% | Highest yields in the city; near Two Rivers |

| Apartment, satellite town (Ruiru, Syokimau, Athi River) | KES 4–9M | KES 30–60k | ~6–9% | Higher yield, thinner liquidity, more volatility |

| 3-bed apartment, Westlands/Riverside | KES 18–35M | KES 130–250k | ~5–6.5% | Corporate tenants; some oversupply pressure |

| Town house, Lavington/Loresho | KES 30–60M | KES 180–320k | ~4–5.5% | Families; steadier capital growth than yield |

| Prestige house, Karen/Runda/Muthaiga | KES 45–150M+ | KES 250–600k | ~3–4% | Trophy assets; lowest yields, blue-chip tenants |

A few honest takeaways. The city-wide gross average is about 7.4%, the best in nearly two decades, but that headline is lifted by busy mid-market and satellite areas — not the suburbs people dream about. Apartments out-yield houses almost everywhere, because rent doesn’t scale with land. And the highest-yield areas carry the most risk: satellite towns can see prices wobble even as rents rise, so they suit a longer hold. For a full area-by-area breakdown, see the best areas to invest in Nairobi and the Nairobi property prices and trends guides. All figures are indicative for 2026 — verify before you commit.

What eats your return

This is where most first-time landlords get a nasty surprise. The gap between gross and net is real money, and in Nairobi it’s typically 2 to 3 percentage points of yield. Here’s where it goes.

Management fees. A licensed agent who finds tenants, collects rent, handles repairs and files your rental tax charges about 5–10% of the rent collected, plus 16% VAT on their fee. Finding a new tenant often costs an extra fee of around one month’s rent. Worth it for absentee owners; a drag if you over-pay.

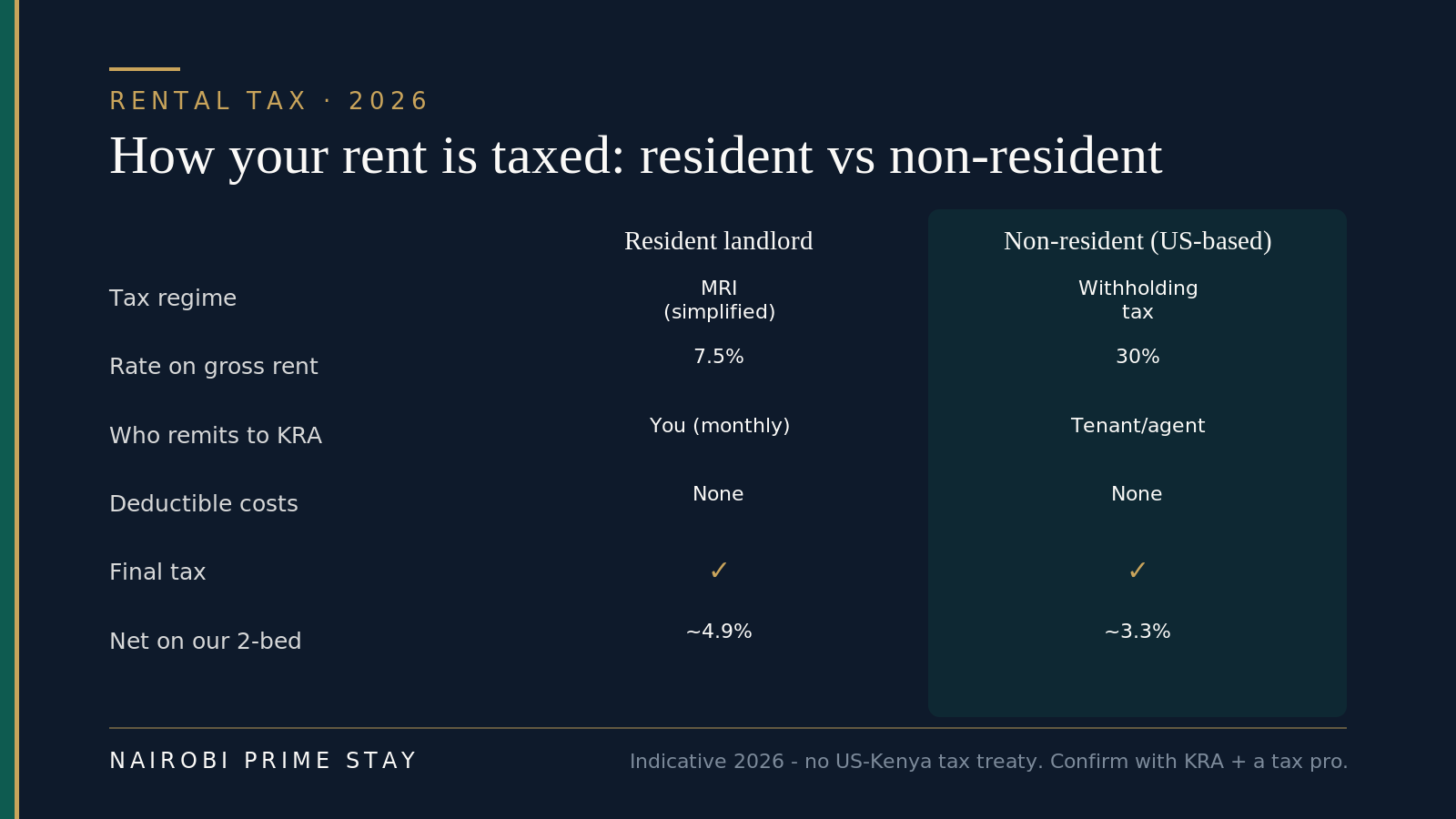

Rental-income tax. Residential rent is taxed under Monthly Rental Income (MRI) at 7.5% of gross rent as of mid-2026, for landlords earning between KES 288,000 and KES 15 million a year. It’s a final tax with no deductions — you pay on the rent, not the profit — and it’s filed monthly by the 20th, increasingly through KRA’s new eRITS portal. A Finance Bill 2026 proposal would raise the rate to 10% from 1 July 2026, so confirm the current figure with KRA. And note: that 7.5% is the resident rate — if you live in the US, your rate is different and higher, which we cover next. Full detail is in our property taxes in Kenya guide.

Service charge and land rates. Apartment blocks levy a monthly service charge for security, water, garbage and common-area upkeep — often KES 5,000–15,000 and sometimes excluded from the quoted rent. The tenant may cover it while occupying, but you eat it during voids. Land rates (county) and, on leasehold, land rent (national) are annual bills the owner always pays.

Vacancy and voids. No apartment is let every single day. Budget at least one month empty per year — more for furnished or short-let — plus the gap between tenants. An empty month is lost rent and a service-charge bill you still pay.

Repairs, maintenance and a sinking fund. Wear happens — taps, paint, appliances, the geyser that dies in year three. Set aside roughly one month’s rent a year for upkeep and a sinking fund. Furnished units cost more; tenants are harder on someone else’s sofa.

Insurance and the rest. Building and contents insurance, the odd legal or valuation fee, and currency conversion if you’re sending rent home to the US. None is huge alone; together they trim the edge.

A worked example: a two-bed in Kilimani

Numbers beat adjectives. Here’s a realistic long-let on an unfurnished two-bedroom apartment in Kilimani, one of the city’s deepest rental markets.

- Purchase price: KES 14,000,000 (about $108,000 at KES 129 to the dollar)

- Monthly rent: KES 90,000 → KES 1,080,000 a year if let every month

- Gross yield: 1,080,000 ÷ 14,000,000 = 7.7%

Now the real world. Assume one month vacant, so you collect 11 months — KES 990,000 — and subtract the running costs:

| Line | Amount (KES/yr) |

|---|---|

| Rent collected (11 of 12 months) | 990,000 |

| Less: management (8% + 16% VAT) | −92,000 |

| Less: rental-income tax (7.5% of gross) | −74,000 |

| Less: repairs, maintenance & sinking fund | −90,000 |

| Less: land rates, insurance, void service charge | −50,000 |

| Net income | ≈ 684,000 |

| Net yield (684,000 ÷ 14,000,000) | ≈ 4.9% |

So a headline 7.7% gross becomes about 4.9% net — and that’s before you add the 5–8% buying costs to the denominator, which nudges it lower still. Add or subtract capital growth on top: a well-chosen Kilimani or Kileleshwa unit may appreciate modestly, while an oversupplied block may flatline or fall. A US owner also carries currency risk — your rent is in shillings, your home costs are in dollars, and KES has been broadly stable near 129 in 2026 but isn’t guaranteed to stay there.

Is 4.9% net plus modest growth good? By US rental standards, it’s competitive — and the entry price is a fraction of a comparable US city. But it’s a world away from the “10% returns” marketing, and it only holds if you let consistently and control costs. Run this same table on any unit before you buy. If a deal only works at 100% occupancy and zero repairs, it doesn’t work.

Illustrative only — your numbers will vary. The point: costs and tax take roughly 3 points off the gross.

Illustrative only — your numbers will vary. The point: costs and tax take roughly 3 points off the gross.

The tax trap for US-based owners: non-resident landlords pay 30%

If you live in the US, the 7.5% rate above probably isn’t yours. A landlord who isn’t tax-resident in Kenya pays 30% of gross rent as a final withholding tax — four times the resident rate, and the single biggest thing that changes a US buyer’s real return.

Here’s how it works. You’re generally treated as tax-resident in Kenya if you spend 183 days or more in the country in a year (or a long average across years). Live in the US and visit now and then, and you’re a non-resident for this purpose. Kenya then taxes your rental income under Section 35 of the Income Tax Act: your tenant or managing agent withholds 30% of the gross rent and remits it to KRA by the 20th of the following month. It’s a final tax — no deductions for your costs, no annual return for that income, nothing to reclaim.

There’s no softening treaty, either. The US and Kenya have no double-tax treaty, so unlike a UK or German landlord you can’t apply for a reduced Kenyan rate. The one relief that does help is on the US side: you can usually claim a foreign tax credit (IRS Form 1116) for the Kenyan tax, so the same rental income isn’t fully taxed twice. That credit only helps if you have US tax to offset, and it doesn’t put the cash back in your Kenyan account — the 30% is gone before the rent ever leaves Kenya.

What does that do to the numbers? Take the same Kilimani two-bed. As a resident you’d lose about KES 74,000 a year to the 7.5% MRI tax and net roughly 4.9%. As a US-based non-resident, the tax line jumps to about KES 297,000 — 30% of the rent collected — and the net yield falls to about 3.3%. Same flat, same rent, a point and a half of yield gone purely to your tax status.

The audience for this guide is mostly US-based — which means the 30% column, not the 7.5% one. Confirm your status with a cross-border tax professional.

The audience for this guide is mostly US-based — which means the 30% column, not the 7.5% one. Confirm your status with a cross-border tax professional.

None of this kills the case for a Nairobi rental — a 3% net income return on a low entry price, plus any growth, is still respectable. But it has to be in your math from day one. Two fixes are common: some owners who plan to spend real time in Kenya arrange their affairs so they’re tax-resident, or hold through a local company (get advice — both carry their own costs and filings), and almost everyone in this position uses a licensed agent who handles the withholding correctly, because a tenant who forgets to withhold leaves you exposed. Our property taxes in Kenya and taxes for expats in Kenya guides go deeper, but the rule of thumb is simple: budget 30%, not 7.5%, and confirm with a pro.

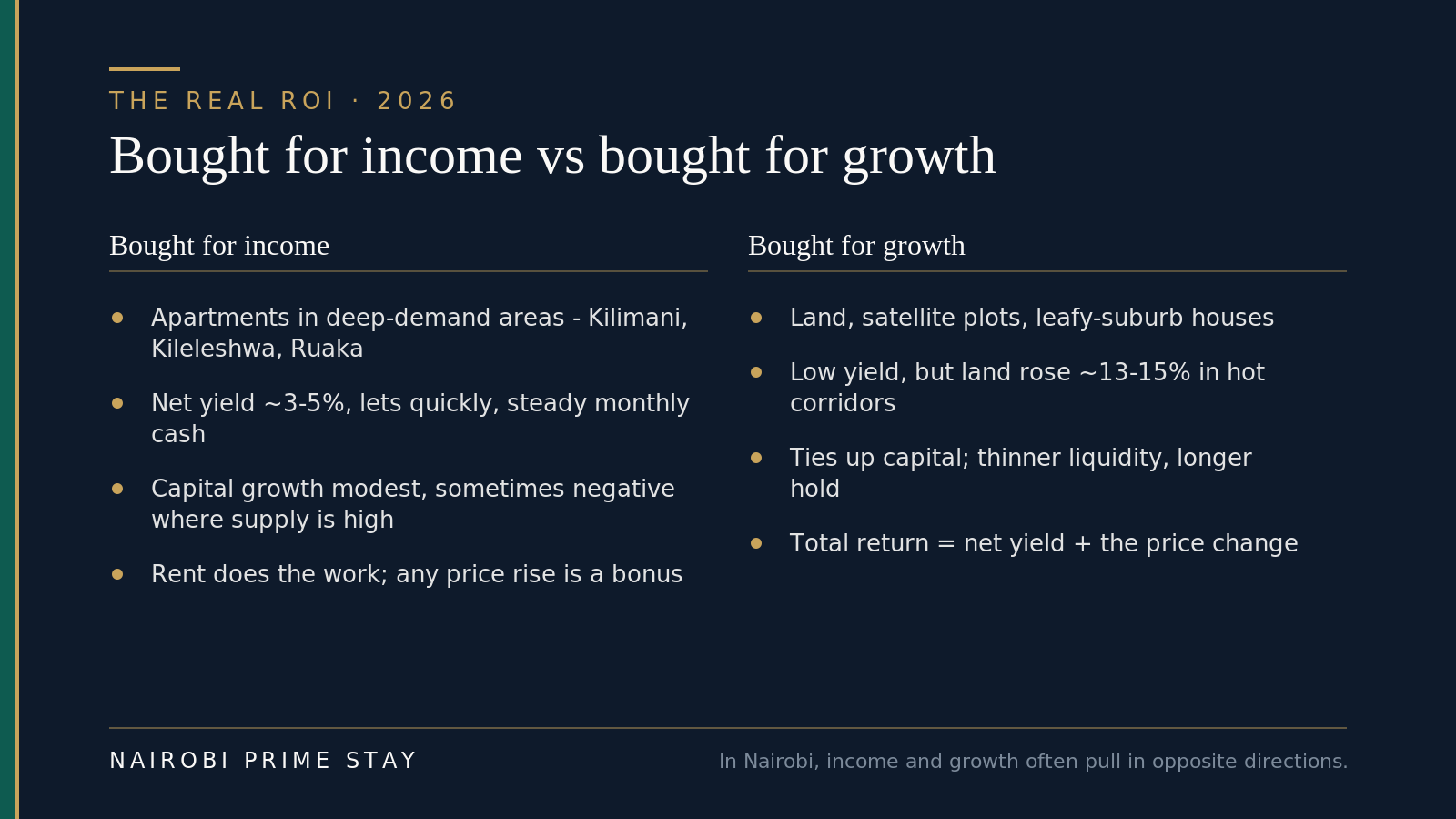

Rental income is only half the return: capital growth and total return

Your real ROI is the net yield plus whatever the property does in value — and in Nairobi the two often pull in opposite directions. Total return is simple to state: net yield + annual price change. A 4% net yield with 3% appreciation is a 7% total return; the same 4% net yield in a block that loses 5% of its value is a 1% year, even though the rent looked fine.

The honest 2026 picture is a tale of two markets. The areas with the deepest rental demand — mid-market apartments in Kilimani, Kileleshwa and the satellite corridors — are also the most built-up, so prices in several oversupplied pockets have been flat or falling even as rent holds. HassConsult had premium apartment suburbs like Westlands, Kileleshwa and Parklands down roughly 7% to 11.5% as supply caught up with demand. Meanwhile land in growth corridors like Juja, Syokimau and Ruiru rose about 13% to 15% a year — but land pays no rent while you hold it, and apartment yields out there are thinner. Average suburban rents, for their part, crossed KES 200,000 a month for the first time in 2026 (about KES 201,832, per HassConsult), so the income side is genuinely strong.

The takeaway: you usually choose income or growth, rarely both at once. Apartments in deep-demand areas are an income play — buy them for the yield and treat any price rise as a bonus, not a plan. Land, satellite plots and leafy-suburb houses are a growth play — low yield, slow steady appreciation, a longer hold. Don’t let a broker sell you “great yield and huge capital gains” on the same unit; that combination is rare, and in an oversupplied block it’s fiction.

In Nairobi, income and growth usually live in different postcodes. Decide which you’re buying before you offer.

In Nairobi, income and growth usually live in different postcodes. Decide which you’re buying before you offer.

One more layer for a US owner: your return is in shillings, your home life is in dollars. KES has been broadly stable near 129–130 to the dollar through 2026, but any future weakness quietly trims your dollar return on both the rent and the eventual sale. We cover that in the USD/KES currency guide, and the area-by-area price detail sits in Nairobi property prices and market trends and the best areas to invest in Nairobi guide.

Furnished, serviced or long-let?

How you let the apartment changes the math as much as where it is. There are three broad plays.

Long-let, unfurnished is the simplest. You sign a one-year lease, the tenant brings their own furniture, and you collect a steady rent with the lowest effort and the fewest voids. Yields run about 5–7%, and your tenants are usually families, expats and professionals who stay put. This is the default for hands-off and diaspora owners.

Furnished long-let earns more — often 20–40% above the unfurnished rent — and suits relocating corporates, embassy staff and medical visitors who want to move straight in. But you fund the furniture, replace it as it wears, and accept more frequent turnover and voids. Net yields can edge to 6–8% if you keep it occupied, but the extra rent is partly an extra workload.

Short-let or Airbnb chases the highest headline rent — gross yields of 8–12% on paper in tourist and corporate hot spots like Westlands and Kilimani. The catch is heavy: nightly management, cleaning, platform fees, county licensing, higher wear, and real oversupply that pushes occupancy and rates down. It’s a small business, not passive income. We weigh it properly in the short-let and Airbnb investment guide, and our own serviced apartments page shows what the furnished end of the market looks like done well.

Higher rent comes with higher effort, cost and void risk. Short-let yields are gross, before the bigger running costs.

Higher rent comes with higher effort, cost and void risk. Short-let yields are gross, before the bigger running costs.

Do you need a property manager?

If you live abroad, yes — almost always. A good manager is the difference between rental income and a remote headache.

A licensed manager handles tenant-finding and vetting, rent collection, repairs, inspections, the service-charge relationship and your monthly KRA rental filing. For that they take 5–10% of rent collected plus 16% VAT, and usually a one-off letting fee when they place a tenant. On our worked example, that’s the KES 92,000 line — real money, but cheaper than a botched tenancy or missed tax filing from 12,000 km away.

Choose one registered with the Estate Agents Registration Board (EARB) — registration is the law, and it gives you recourse. Ask exactly what the fee covers, how often you get statements, and whether maintenance is marked up. Self-managing only makes sense if you’re local, have time, and enjoy the calls. For the full breakdown of fees and how to vet an agent, see our property management in Nairobi guide. If you’re financing the purchase rather than paying cash, the property financing guide covers how a loan changes the return.

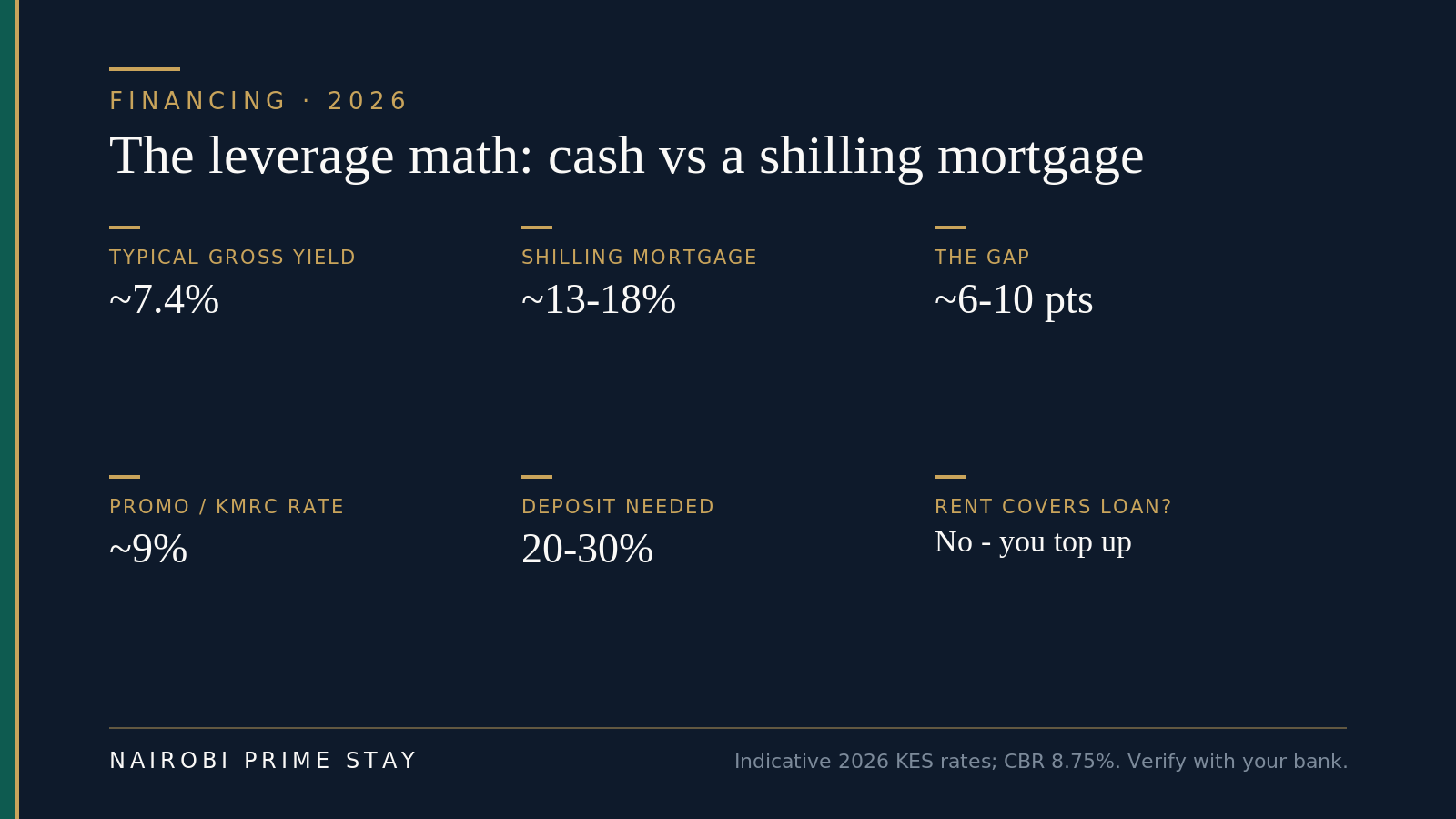

Should you borrow to buy a rental? The leverage trap

For most buy-to-let buyers in Nairobi, cash beats a shilling mortgage — because the mortgage rate is roughly double the rental yield. This is the opposite of the US playbook, where cheap borrowing magnifies returns, so it catches a lot of American buyers out.

Run the numbers. Gross yields sit around 7%, while a standard shilling mortgage costs about 13% to 18% (the Central Bank rate is 8.75%, but retail mortgages price well above it). Borrow at 15% to buy an asset that earns 7%, and you’re underwater on the borrowed portion by some 6 to 10 points a year — the rent doesn’t cover the repayment, so you top up the loan from your own pocket every month. That’s negative cash flow, the reverse of what you wanted.

Leverage can still make sense in a few cases. If you land a sub-market promotional or diaspora rate near 9%, or a KMRC-backed affordable-housing loan, the gap narrows. If you put down a big deposit (20–30% is normal anyway) so the loan is small relative to the rent, the drag shrinks. And if you’re genuinely betting on capital growth to outrun the interest, borrowing is a leveraged bet on prices — fine if you know that’s the game, dangerous in an oversupplied segment. For most foreign and diaspora buyers, though, the math points to cash or a large deposit, with any local loan kept small.

When the loan costs more than the asset earns, borrowing erodes the return instead of boosting it.

When the loan costs more than the asset earns, borrowing erodes the return instead of boosting it.

If you do want to finance — or you’re a diaspora Kenyan with access to a diaspora-mortgage product — our property financing in Kenya guide covers the routes, rates and deposits in full, and the diaspora property investment guide covers buying remotely without getting burned.

Pros and cons of buy-to-let in Nairobi

| The case for | The case against |

|---|---|

| Decent income returns — ~5–7.5% gross, the best yields in years | Net yield is 2–3 points lower; the headline flatters |

| Low entry price vs comparable US cities — apartments from KES 5–16M | Oversupply in parts of the city caps rent and price growth |

| Deep tenant demand from expats, diplomats, students and professionals | Less market transparency — no MLS, harder to value and resell |

| Rents have been rising, especially in satellite corridors | Currency risk for USD earners; rent is in shillings |

| Hands-off possible with a licensed manager | Tax on gross rent, plus service charge, rates and voids |

| Diversifies a US-heavy portfolio into a growth economy | Title and developer due diligence is essential, not optional |

The honest read: buy-to-let in Nairobi is a solid income play for a buyer who does the homework, picks demand over prestige, and runs net numbers. It’s a poor fit for anyone expecting passive 10% returns or quick flips.

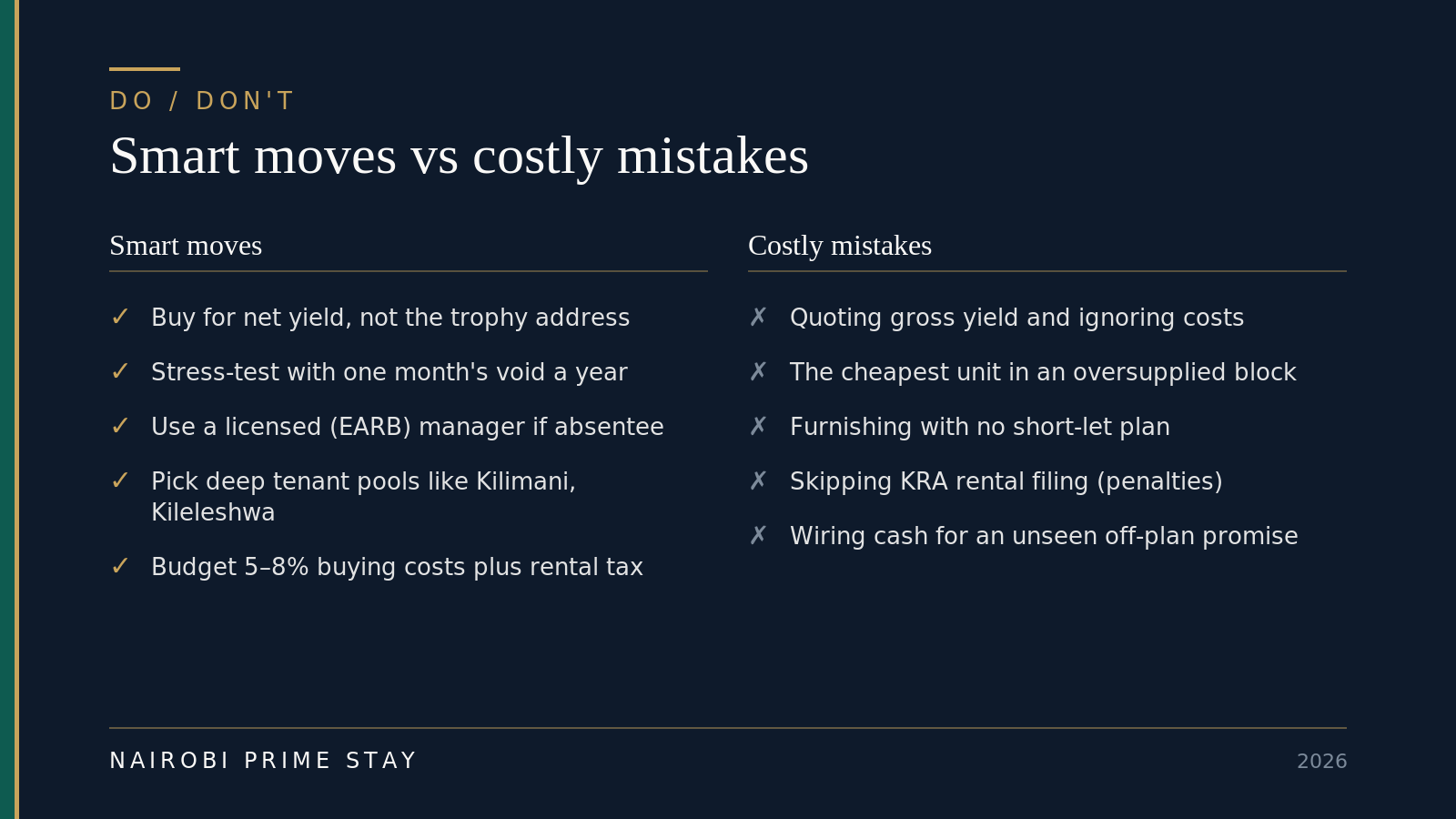

Smart moves vs costly mistakes

The difference between a yield that holds and one that disappoints is mostly discipline.

The difference between a yield that holds and one that disappoints is mostly discipline.

The winners buy for net yield, not the trophy address, and stress-test every deal with a month of vacancy and a full cost list before they offer. They pick areas with deep, reliable tenant pools — Kilimani, Kileleshwa, Ruaka — over the prettiest block in a thin market. They use a licensed manager if they’re absentee, and they budget the 5–8% buying costs and the rental tax from day one.

The losers quote themselves the gross yield and ignore the costs. They buy the cheapest unit in an oversupplied new development because the price looks good, then can’t let it. They furnish without a plan, skip the KRA rental filing and collect penalties, or — worst of all — wire cash for an unseen off-plan promise. Protect yourself with proper due diligence and a real advocate; our property investment guide and the property prices data are the place to sanity-check any pitch.

Your buy-to-let checklist

Work through this before you commit to any Nairobi rental:

- Calculate the net yield, not just gross — subtract every running cost

- Confirm the realistic monthly rent from live listings, not the agent’s estimate

- Add 5–8% buying costs to your capital outlay in the math

- Budget at least one month’s vacancy a year (more if furnished/short-let)

- Check the area for oversupply — count the new blocks going up nearby

- Verify the title and the developer before any money moves

- Get a written service-charge history and the sinking-fund balance

- Decide your strategy up front: long-let, furnished, or short-let

- Line up a licensed (EARB) manager if you’ll be absentee

- Register for KRA rental-income tax and plan the monthly filing

- Factor currency risk if your costs are in dollars

- Visit, or send a trusted proxy — never buy a Nairobi rental sight-unseen

Frequently asked questions

What rental yield can I expect from a Nairobi apartment?

Gross rental yields run about 5% to 7.5% on most prime Nairobi apartments, averaging roughly 7.4% city-wide in 2026 — the highest since 2007. A few high-demand pockets like Ruaka reach 7% to 10%, while big prestige houses in Karen or the diplomatic belt yield only 3% to 4%. Net yield, after management, tax, service charge, rates and vacancy, is usually 2 to 3 points lower — so think 4% to 5% net on a typical apartment. Always run the net figure before you buy.

What is the difference between gross and net rental yield?

Gross yield is annual rent divided by the purchase price, before any costs — the flattering number in every listing. Net yield is what’s left after running costs (management, rental tax, service charge, rates, repairs and vacancy), divided by the price plus your buying costs. In Nairobi the gap is typically 2 to 3 percentage points, so a 7.7% gross apartment often nets around 4.9%. Net yield is the money you actually keep, so it’s the one that matters.

How much tax do I pay on rental income in Kenya?

Residential rent is taxed under Monthly Rental Income (MRI) at 7.5% of gross rent as of mid-2026, for landlords earning between KES 288,000 and KES 15 million a year. It’s a final tax with no deductions — you pay on the rent, not the profit — and it’s filed monthly by the 20th, increasingly through KRA’s eRITS portal. A Finance Bill 2026 proposal would raise the rate to 10%, so confirm the current figure with KRA. This is general information, not tax advice.

Is buy-to-let in Nairobi a good investment in 2026?

It can be, if you buy the right unit and run the net numbers. Apartments in deep-demand areas like Kilimani, Kileleshwa and Ruaka deliver solid gross yields of about 6% to 10% and let quickly. But parts of the city are oversupplied — Westlands apartment prices fell about 11.5% across 2025 — which caps rent and price growth, and costs plus tax take 2 to 3 points off the gross. It suits a disciplined income investor, not someone expecting passive 10% returns.

Should I rent my Nairobi apartment furnished or unfurnished?

Unfurnished long-lets are simplest — steady rent, low effort, the fewest voids, yields around 5% to 7%, and tenants who stay. Furnished units earn 20% to 40% more rent and suit relocating corporates and embassy staff, but you fund and replace the furniture and accept more turnover. Short-let or Airbnb chases the highest rent (8% to 12% gross on paper) but is a hands-on small business with cleaning, licensing and oversupply risk. Match the strategy to how involved you want to be.

Do I need a property manager for a Nairobi rental?

If you live abroad, almost always. A manager handles tenant-finding, rent collection, repairs, inspections and your monthly KRA filing for about 5% to 10% of rent collected plus 16% VAT, with a one-off letting fee when they place a tenant. Choose one registered with the Estate Agents Registration Board (EARB), which is a legal requirement and gives you recourse. Self-managing only makes sense if you’re local and have the time.

What costs reduce rental returns in Nairobi?

The main ones are management fees (5% to 10% plus VAT), rental-income tax (7.5% of gross), service charge and land rates, vacancy (budget at least a month a year), and repairs plus a sinking fund (around a month’s rent a year). Insurance and currency conversion trim a little more. Together they typically cut 2 to 3 percentage points off the gross yield, which is why net yield is always lower than the headline.

Can foreigners earn rental income from property in Kenya?

Yes. Foreigners can own apartments on 99-year leasehold — the common sectional-title route — and let them out for income, just like citizens. You need a KRA PIN to register and to pay rental-income tax, and non-resident landlords are taxed under separate withholding rules, so get local advice. Buying costs add about 5% to 8% on top of the price, so factor those into your yield. This is general information, not legal or tax advice.

Do US-based landlords pay more tax on Nairobi rental income?

Yes — a lot more. If you live in the US you’re a non-resident landlord, and Kenyan rent is taxed at a flat 30% of gross, withheld by your tenant or agent and paid to KRA by the 20th of each month. It’s a final tax with no deductions, and because there’s no US-Kenya tax treaty there’s no Kenyan relief — though you can usually claim a US foreign tax credit so the same income isn’t taxed twice. On our Kilimani example the 30% rate drops the net yield from about 4.9% to about 3.3%. Get cross-border tax advice before you buy.

Should I take a mortgage to buy a rental in Nairobi?

Usually no, if income is your goal. Shilling mortgage rates run about 13% to 18%, while gross rental yields are around 7% — so the loan costs roughly double what the apartment earns, and the rent won’t cover the repayment. Most foreign and diaspora buy-to-let here is cash or a large deposit. Borrowing only makes sense if you secure a sub-yield promotional or diaspora rate near 9%, put down a big deposit, or you’re deliberately betting on capital growth to outrun the gap.

What total return can I expect from a Nairobi rental?

Think net yield plus capital growth. After costs and tax a resident nets about 3% to 5% on a well-bought apartment, or nearer 3% as a US-based non-resident. Capital growth is a separate question — modest in steady suburbs and actually negative lately in oversupplied apartment pockets like Westlands, while satellite land has risen 13% to 15% a year. Income and growth rarely come together, so buy where rent demand is deep and treat any price rise as a bonus. For a US owner, shilling weakness can also trim dollar returns.

Final thoughts

Buy-to-let in Nairobi rewards the patient and the numerate. The income is real and the entry price is low by Western standards, but the return lives in the net yield, not the gross — and in the discipline of buying demand over prestige. Pick an apartment in an area people actually want to rent, budget honestly for costs, tax and the odd empty month, and let a licensed manager handle the day-to-day if you’re far away. Do that and a Nairobi rental can pay a steady 4% to 5% net plus modest growth for years. This is general information, not legal, tax or investment advice — confirm the specifics with a Kenyan advocate and a cross-border tax professional before you commit.

Related reading

- The big picture: property investment in Kenya — the complete guide

- Where the demand is: best areas to invest in Nairobi real estate

- What things cost: Nairobi property prices and market trends

- Every levy: property taxes in Kenya

- Hands-off letting: property management in Nairobi

- The short-let question: Airbnb and short-let investment in Nairobi

- Furnished done well: serviced apartments in Nairobi

- New to Kenya? Start with the complete guide to moving to Nairobi

Thinking of buying a rental but want to learn the ground first? A serviced apartment for your first weeks lets you walk the neighborhoods, meet agents and test the tenant demand before you commit a big cheque. Browse our serviced apartments — a $50 deposit reserves your dates and the balance is due on arrival — or ask our AI relocation assistant to shortlist areas that fit your budget and goals.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.