Guides · Property investment

Commercial Property Investment in Nairobi: An Honest 2026 Guide

Commercial Property Investment in Nairobi: An Honest 2026 Guide

Commercial property in Nairobi can pay better than a flat — gross yields of 8 to 9.5 percent on the right asset, often in US dollars — but it’s a bigger, slower, riskier game than buying an apartment, and the segment you pick matters more than the city you pick.

That’s the honest headline. In 2026, Nairobi’s commercial market is split in two. Offices spent years oversupplied and are only now recovering, with a clear flight to quality. Industrial and logistics space, meanwhile, is the quiet winner — full warehouses, real tenant demand, and the highest yields in the market. Retail sits in the middle. Mixed-use is the most ambitious and the hardest to get right.

This guide is for Americans and diaspora investors deciding whether to put money into Nairobi commercial property, and which kind. We’ll cover what each segment really earns, how leases and taxes work, what foreigners can own, and who this suits — and who should stick to an apartment or a REIT instead.

TL;DR — commercial property in Nairobi (2026)

- The market is two stories. Offices are recovering from a long glut; industrial and logistics is the standout performer. Pick the segment before you pick the building.

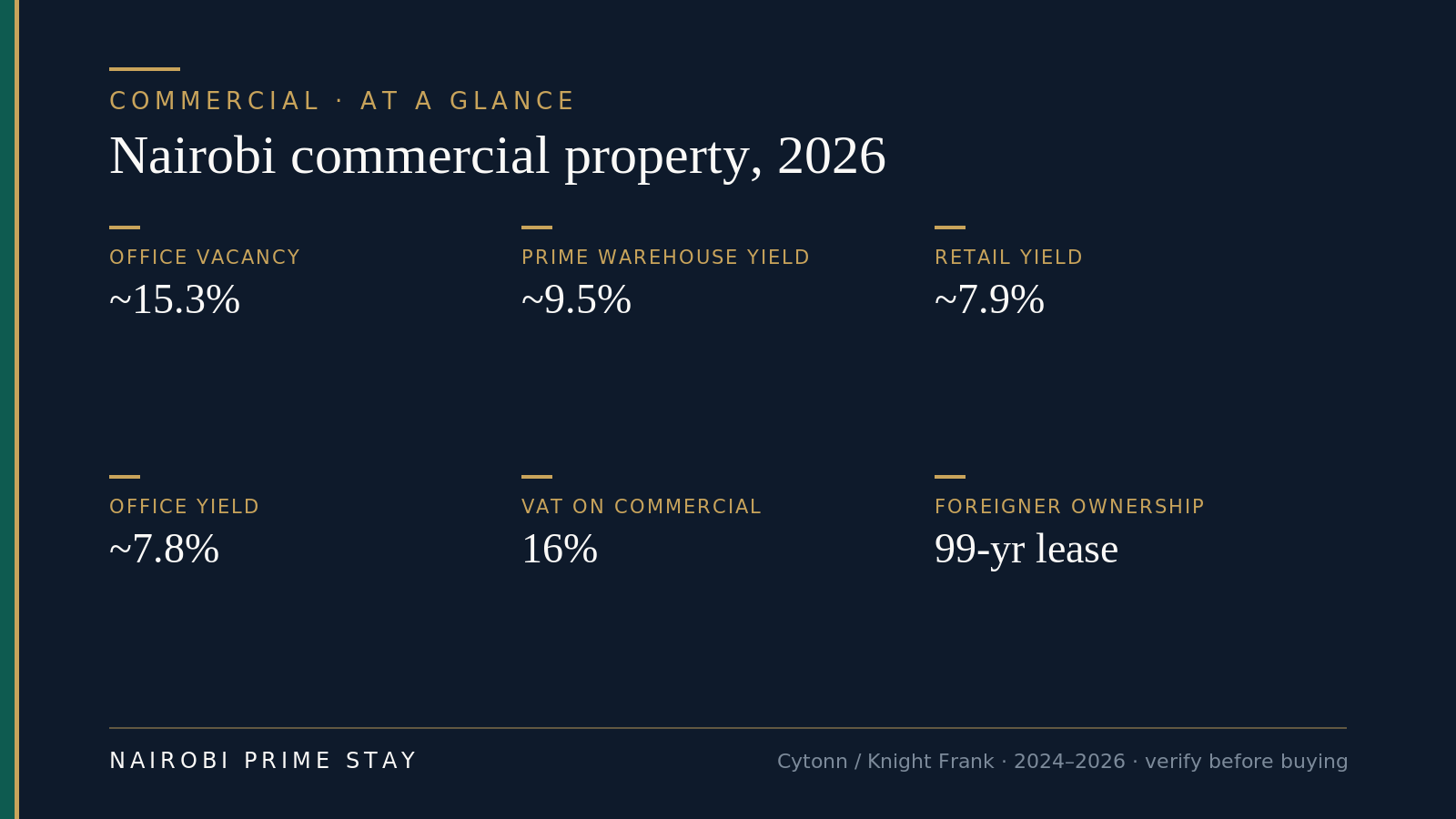

- Yields, roughly. On 2024–2025 data, prime offices run about 7 to 8.5 percent, retail about 7.9 percent, and prime warehouses about 9 to 9.5 percent — the highest of the three. Hedge these; they move, and one bad tenant changes everything.

- Office vacancy is falling but still real. Nairobi office vacancy dropped to about 15.3 percent at the end of 2025, from roughly 19.3 percent a year earlier. Grade A buildings are filling; older Grade B blocks are not.

- Leases are bigger and longer. Commercial leases often run 3 to 10 years and are frequently quoted in US dollars — good for a dollar-earning investor, but tenants are harder to replace.

- Tax is heavier than residential. Commercial sale and rent carry 16 percent VAT (residential is exempt), plus stamp duty, capital gains tax and rental income taxed as business income.

- Foreigners can invest — on 99-year leasehold, through a company, or hands-off through a listed REIT — but this is a large-ticket, illiquid asset. Most first-time investors are better served by an apartment or a REIT.

The numbers that frame a Nairobi commercial decision in 2026. Treat them as starting points, and verify before you buy.

The numbers that frame a Nairobi commercial decision in 2026. Treat them as starting points, and verify before you buy.

Why this matters

Commercial property is where the bigger money in Nairobi real estate sits — and where the bigger mistakes happen. An apartment that sits empty for a month costs you a month. A half-empty office floor or a warehouse in the wrong location can cost you for a year, because commercial tenants are fewer, larger and slower to find.

The upside is real. A good commercial asset throws off more income than residential, on a longer lease, often in dollars, with the tenant covering more of the running costs. The downside is just as real: you’re making a concentrated bet on one or two tenants and one location, in a market where some segments are still digging out of oversupply.

So this isn’t a starter investment. It rewards investors who can write a large cheque, wait, and manage — or who buy exposure the easy way, through a REIT.

What counts as commercial property in Nairobi?

Commercial property is anything you buy to earn business rent rather than to house a family. In Nairobi it falls into four broad buckets, and they behave very differently.

Office space. Floors or whole buildings let to companies, NGOs, embassies and professional firms. Graded A (modern, prime, full amenities), B (older but decent) and C (basic). This is the segment that was badly oversupplied and is now recovering — unevenly.

Retail. Shop units and space in malls and on high streets, let to shops, restaurants, banks and supermarkets. The big malls — Two Rivers, Sarit, The Hub, Garden City, Westgate, Village Market — anchor this segment. E-commerce is a slow headwind.

Industrial and logistics. Warehouses, distribution centres and light-manufacturing units along the main corridors and in special economic zones. This is the part of the market with the strongest 2026 demand and the best yields.

Mixed-use. Schemes that combine offices, shops, apartments and sometimes a hotel in one development — Two Rivers and Garden City are the landmark examples. Higher ambition, higher complexity, and usually only within reach of large investors or funds.

The big picture: a two-speed market in 2026

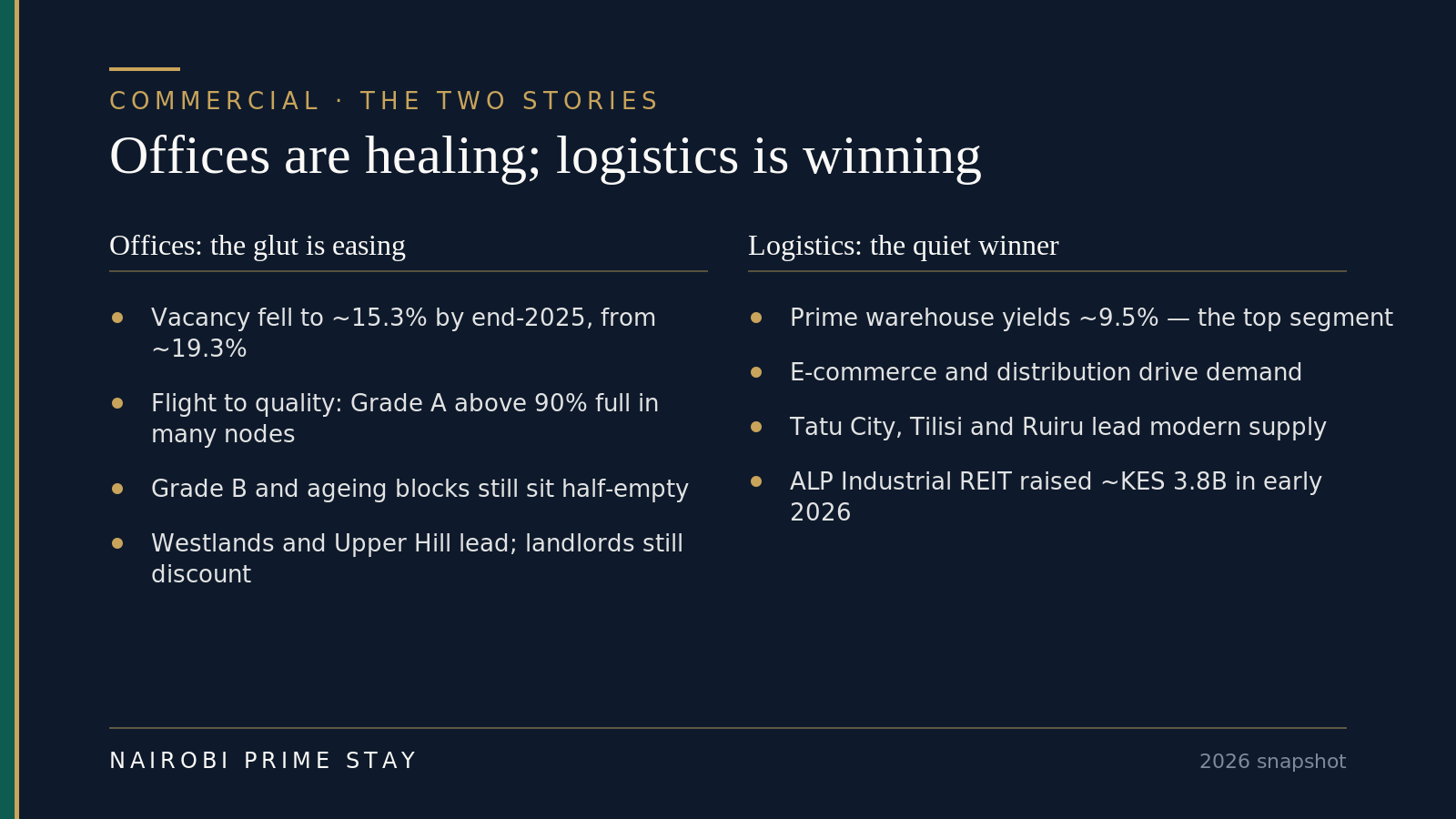

Nairobi’s commercial market in 2026 is recovering, but not evenly. The single most useful thing to grasp before you buy is that the headline “Nairobi commercial” hides two very different stories.

Offices spent the better part of a decade oversupplied. Developers built faster than demand grew, vacancy climbed, and rents softened. That glut is now easing. According to Cytonn Research, office vacancy in the Nairobi Metropolitan Area fell to about 15.3 percent at the end of 2025, down from roughly 19.3 percent a year earlier, and the oversupply shrank to about 3.4 million square feet from 5.7 million. Knight Frank expects prime office occupancy to keep rising in 2026, with limited new high-quality supply in Westlands and Upper Hill. The catch: an estimated 2.5 million square feet is due to come online in 2027 and 2028, which could test the recovery.

Industrial and logistics, meanwhile, has quietly become the best-performing commercial segment. Prime warehouse yields sat around 9.5 percent in the first half of 2025 — higher than offices or retail — and demand is driven by real economic activity: e-commerce, distribution and manufacturing. In March 2026, the ALP Industrial REIT listed on the Nairobi Securities Exchange as East Africa’s first industrial REIT and the exchange’s first US-dollar-denominated security, after an offer that was about 115 percent oversubscribed and raised roughly KES 3.82 billion ($29.5 million) — a clear signal of investor appetite for logistics.

The two stories inside “Nairobi commercial” in 2026: offices healing, logistics winning.

The two stories inside “Nairobi commercial” in 2026: offices healing, logistics winning.

The practical takeaway: don’t buy “commercial property” in the abstract. Decide which of these stories you want exposure to, then pick the building.

Offices: a recovering market, but only at the top

Offices are worth owning in 2026 if — and only if — you buy quality. The recovery is real, but it’s a flight to quality, not a rising tide that lifts every building.

Here’s what’s happening. Companies are leaving ageing, poorly serviced blocks and moving into modern Grade A space with better amenities, lower running costs and greener credentials. Knight Frank reports that top-tier office stock in more than half the markets it tracks now runs above 90 percent occupancy, while Grade B buildings face long vacancies. So the same city has near-full prime towers and half-empty older ones at the same time. Prime Nairobi office occupancy reached about 81.6 percent by the end of 2025, led by newer towers like Purple Tower and The Mandrake filling up, and Knight Frank puts prime office yields in a stable 8 to 9 percent band, with prime asking rents around $13 per square metre a month.

Where. Westlands and Upper Hill are the prime office nodes, with Gigiri, Riverside and Kilimani also in the mix. Westlands has consistently been one of the strongest office locations. The old CBD is weakest — tenants have been leaving for years.

What it earns. Average asking office rents in the metropolitan area were around KES 105 per square foot in recent Cytonn data, with prime nodes higher and often quoted in US dollars. Office rental yields have hovered near 7.8 percent, with Westlands stronger at roughly 8.5 percent. Treat these as 2024–2025 reference points and confirm current figures with a valuer.

The risk. Oversupply hasn’t gone away; it has eased. Buy a Grade B building cheaply and you may struggle to fill it, because the market is voting for quality. And the 2.5 million square feet due in 2027 and 2028 is a reminder that supply can outrun demand again. Buy the best building you can in the best node, or don’t buy offices at all.

Retail: steady, but watch the anchor

Retail property in Nairobi is a steady middle performer — Kenya’s malls have done better than the “death of retail” headlines suggest, but the segment lives and dies by its anchor tenants.

Nairobi has been the best-performing retail region in Kenya, with average mall rental yields around 7.9 percent and average rents near KES 133 per square foot in recent data. Formal retail keeps expanding as supermarket chains and international brands take space. The malls that work — Sarit, Two Rivers, The Hub, Garden City, Village Market, Westgate — combine a strong anchor (a supermarket or department store), a good catchment of nearby spending households, and decent management.

The risks are specific. When a major anchor fails or pulls out — as happened when several regional supermarket chains collapsed — the mall around it can empty fast, because smaller shops rely on the footfall the anchor brings. E-commerce is a slow, steady headwind on some categories. And a few sub-markets are simply over-malled, with too much retail space chasing the same shoppers. If you buy retail, buy into a proven scheme with a strong anchor on a long lease — not a half-let new mall hoping to fill up.

Industrial and logistics: the quiet winner

If one part of Nairobi commercial property deserves the word “momentum” in 2026, it’s industrial and logistics — and it’s no accident that this is where the smart institutional money is going.

Warehousing and distribution space is in genuine demand. E-commerce platforms, third-party logistics firms, manufacturers and distributors all need modern, well-located sheds with good power, height and access. Prime warehouse yields were around 9.5 percent in the first half of 2025, the highest of any commercial segment. The Nairobi Metropolitan Area holds roughly 90 percent of Kenya’s industrial space, and the action has shifted from the old, congested Industrial Area to planned parks on the edges.

Where. The growth is along the corridors and in special economic zones: Tatu City and Nairobi Gate around Ruiru, Tilisi on the Nairobi–Nakuru highway, Northlands, and the Mombasa Road–Athi River belt. Modern logistics parks at Tatu City (The Link) and Tilisi (ALP West) have quoted space from around $6 per square metre per month. Tatu City’s status as an operating special economic zone adds tax and customs advantages for the right tenant.

Why it’s strong. Unlike offices, this demand isn’t speculative — it tracks real trade and consumption. The heavy oversubscription of the ALP Industrial REIT in early 2026 shows institutions want this exposure. For an individual, a single well-let warehouse on a long lease to a solid tenant can be one of the cleaner commercial bets in the market.

The catch. Location and specification are everything — the wrong access road, ceiling height or power supply makes a shed hard to let. Tickets are large. And buying or building industrial well usually means partnering with people who know the segment.

Mixed-use: ambitious, complex, mostly for big players

Mixed-use schemes are the most ambitious commercial properties in Nairobi — and the least suitable for a first-time individual investor. These combine offices, retail, apartments and sometimes a hotel in one master-planned development. Two Rivers and Garden City are the landmark examples.

Done well, mixed-use is resilient: if offices soften, the retail and residential parts keep paying. Done badly, it multiplies every risk at once and is hard to manage. Entry tickets are very high, and most individual investors who want a piece of these schemes do so by buying a single unit — an apartment or a shop — within them, or by buying shares in the developer or a fund, not the whole thing. See our guide to new developments and satellite cities for where these schemes are clustering.

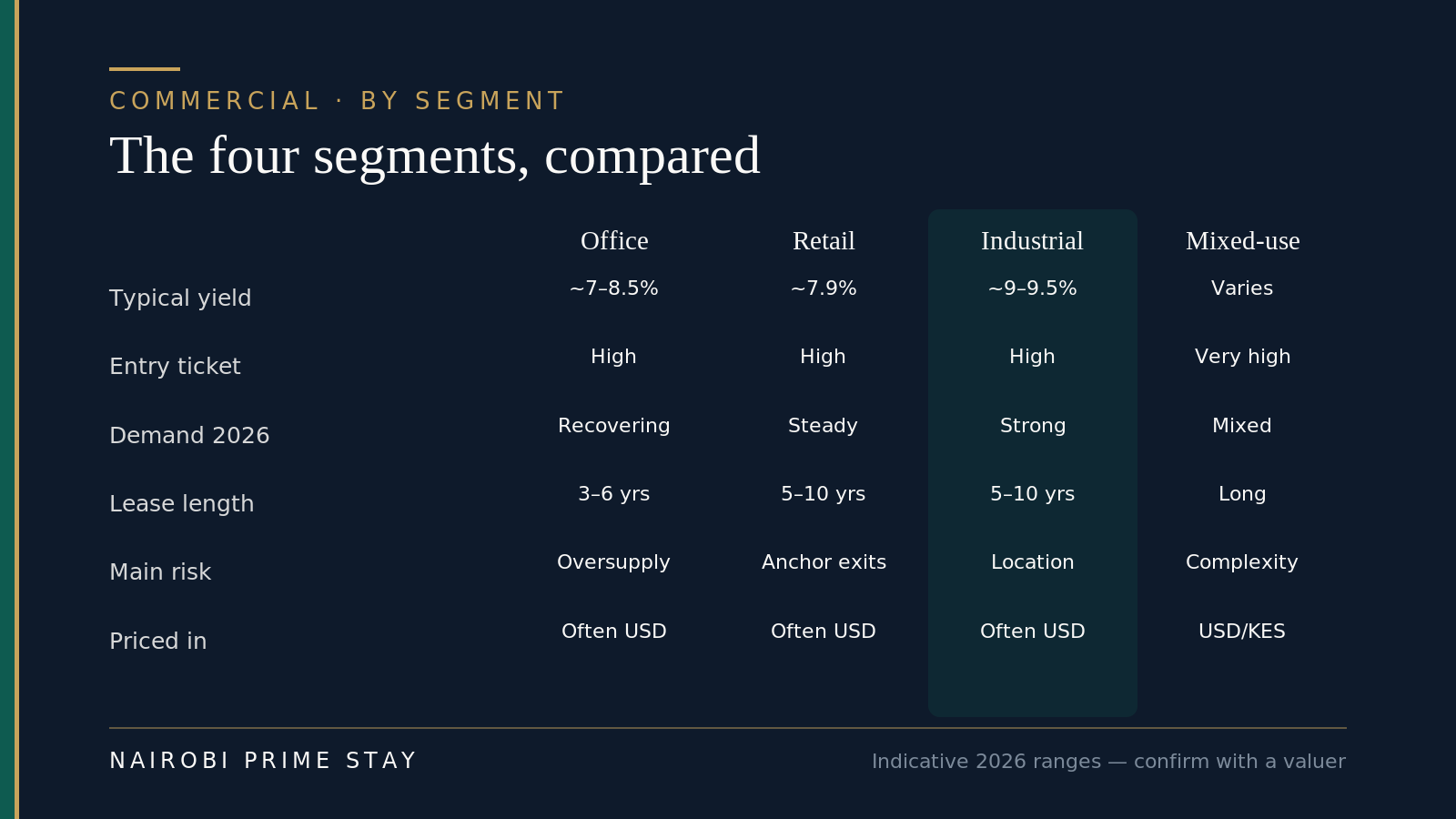

The four segments compared

| Segment | Indicative gross yield (2026) | Entry ticket | Typical lease | Priced in | Main risk | Best for |

|---|---|---|---|---|---|---|

| Office | ~7–8.5% | High | 3–6 years | Often USD | Oversupply; Grade B vacancy | Investors who buy only prime Grade A |

| Retail | ~7.9% | High | 5–10 years | Often USD | Anchor-tenant failure; e-commerce | Buyers of proven, anchored malls |

| Industrial / logistics | ~9–9.5% | High | 5–10 years | Often USD | Wrong location or specification | Investors wanting the strongest demand |

| Mixed-use | Varies | Very high | Long | USD/KES mix | Complexity; execution | Large investors and funds |

Indicative 2026 ranges drawn from Cytonn and Knight Frank reporting; confirm current figures with a valuer before you commit. A single tenant can change any of these numbers.

Industrial and logistics leads on both yield and demand in 2026; offices reward quality only.

Industrial and logistics leads on both yield and demand in 2026; offices reward quality only.

What you actually earn: yields, leases and dollars

Commercial property pays you in three ways that differ from residential, and each cuts both ways.

Higher yields. Gross yields of roughly 7.5 to 9.5 percent on the right commercial asset beat the typical Nairobi apartment, which runs nearer 5 to 7.5 percent. (For the residential comparison, see our buy-to-let guide.) But “gross” is doing a lot of work — service charge, management, rates, insurance and void periods all eat into it, and a long vacancy in commercial hurts far more than in residential.

Longer leases. Commercial tenants typically sign 3 to 10 years, often with built-in rent escalations and a deposit of several months. That’s income you can plan around. The flip side: when a commercial tenant does leave, the space can sit empty for many months, because there are far fewer replacement tenants than for a flat.

Dollar income. Prime office, retail and logistics leases are frequently quoted and paid in US dollars. For an American or diaspora investor who earns and thinks in dollars, that removes the currency risk that comes with a shilling-denominated apartment rent, and makes the rent more stable in real terms. Confirm the lease currency before you buy — it’s one of the most valuable features of a prime commercial asset.

Taxes and costs: heavier than residential

Commercial property is taxed more heavily than a home, and you should price that in from the start. This is general information, not tax advice — confirm everything with a Kenyan tax advisor and, because the US taxes its citizens worldwide, a cross-border accountant. Our property taxes guide goes deeper.

The headline differences:

- VAT at 16 percent. Commercial property sale and rent attract 16 percent VAT. Residential sale and long-term residential rent are exempt. This is the single biggest tax difference between owning a shop or office and owning a flat, and it affects both your purchase and your rental invoicing.

- Rental income as business income. Commercial rent isn’t eligible for the simplified residential rental-income tax — which itself rose to a flat 10 percent of gross for 2026, up from 7.5 percent. It’s taxed as business income, with deductions, at the normal rates — so good bookkeeping matters. And if you own it as a US-based non-resident, a different rule bites first: see the section on buying from the US below.

- Stamp duty of 4 percent on property in towns (including all of Nairobi) applies on purchase, the same as residential, charged on the higher of price or valuation.

- Capital gains tax of 15 percent applies on the net gain when you sell.

- Land rates (county) and, on leasehold, land rent (national) are annual, and a commercial service charge is usually higher than a residential one.

Add legal, valuation and agent costs, and your all-in transaction cost typically lands around 5 to 8 percent of the price on top of the headline figure — see our conveyancing guide for the mechanics.

Can foreigners own commercial property in Kenya?

Yes — under the same rule that applies to all land. A non-citizen can hold commercial property on a leasehold of up to 99 years, and most commercial land is leasehold anyway, so this is less of a constraint here than it is for someone who wants freehold farmland. You can’t hold freehold as a foreigner, and a company counts as “Kenyan” only if it’s 100 percent citizen-owned. Our guide on whether foreigners can buy property in Kenya covers the detail and the company-structure question.

In practice, foreigners reach Nairobi commercial property three ways. They buy a unit or building directly on leasehold (large ticket, hands-on). They invest through a company. Or — most realistically for the majority — they buy exposure through a listed REIT, which is liquid, regulated and needs no landlording. More on that below.

How to buy commercial property — the short version

The buying process mirrors residential, with more due diligence because the stakes are higher. In brief: agree heads of terms, instruct your own independent advocate, run an official title search, check the lease and any existing tenancies in detail, value the building, sign a sale agreement with a deposit held by the advocate as stakeholder, clear the consents and stamp duty, and register the transfer. For the full step-by-step, see how to buy property in Kenya and the conveyancing guide.

Two checks matter more for commercial than for a home. First, the tenant covenant: who is the tenant, how strong is their business, how long is left on the lease, and what happens if they leave? Your income is only as safe as that tenant. Second, the building’s grade and services — power, backup generation, water, parking, lifts, internet, compliance certificates — because a poorly specified commercial building is hard to let at any price.

A worked example: a small Grade A office floor

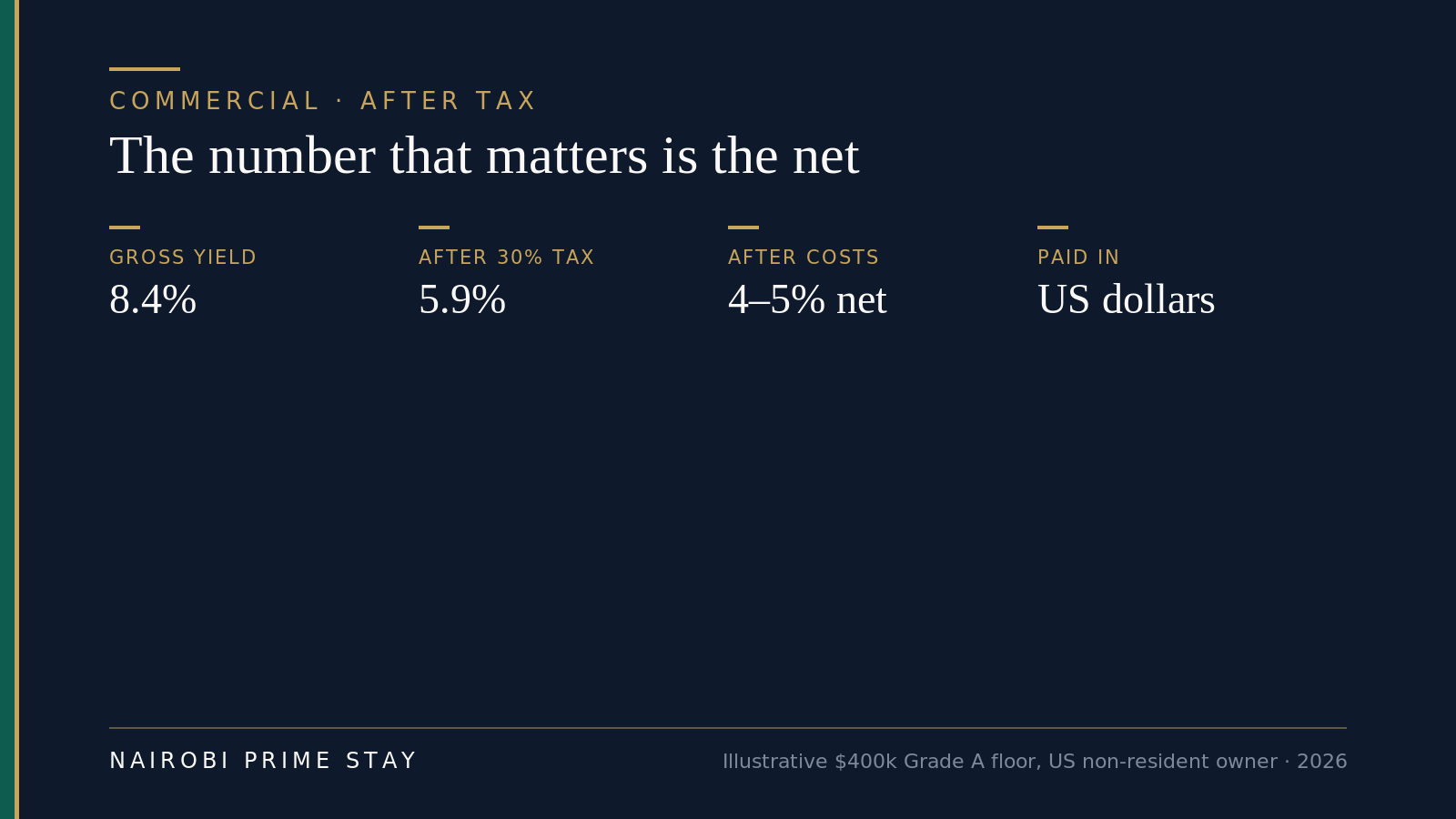

Numbers make this concrete. Say you buy a 200-square-metre Grade A office floor in Westlands for $400,000, let at $14 per square metre per month.

- Annual rent: 200 × $14 × 12 = $33,600.

- Gross yield: $33,600 ÷ $400,000 = 8.4 percent.

- Then the costs. Management at around 5 percent, plus a share of rates, insurance and the inevitable gap between tenants. Allow a realistic 6 to 12 percent of rent in costs and an occasional empty quarter, and your net yield lands nearer 6 to 7 percent in a good year.

- The tenant question. If that single tenant leaves, you could face several months with zero income while you find a replacement — which can pull a given year’s return down sharply. One tenant, one risk.

This is the honest shape of commercial: a higher headline yield than an apartment, in dollars, on a longer lease — but concentrated in one tenant and slower to exit. (These are illustrative figures, not a quote; verify live rents and prices with a valuer.)

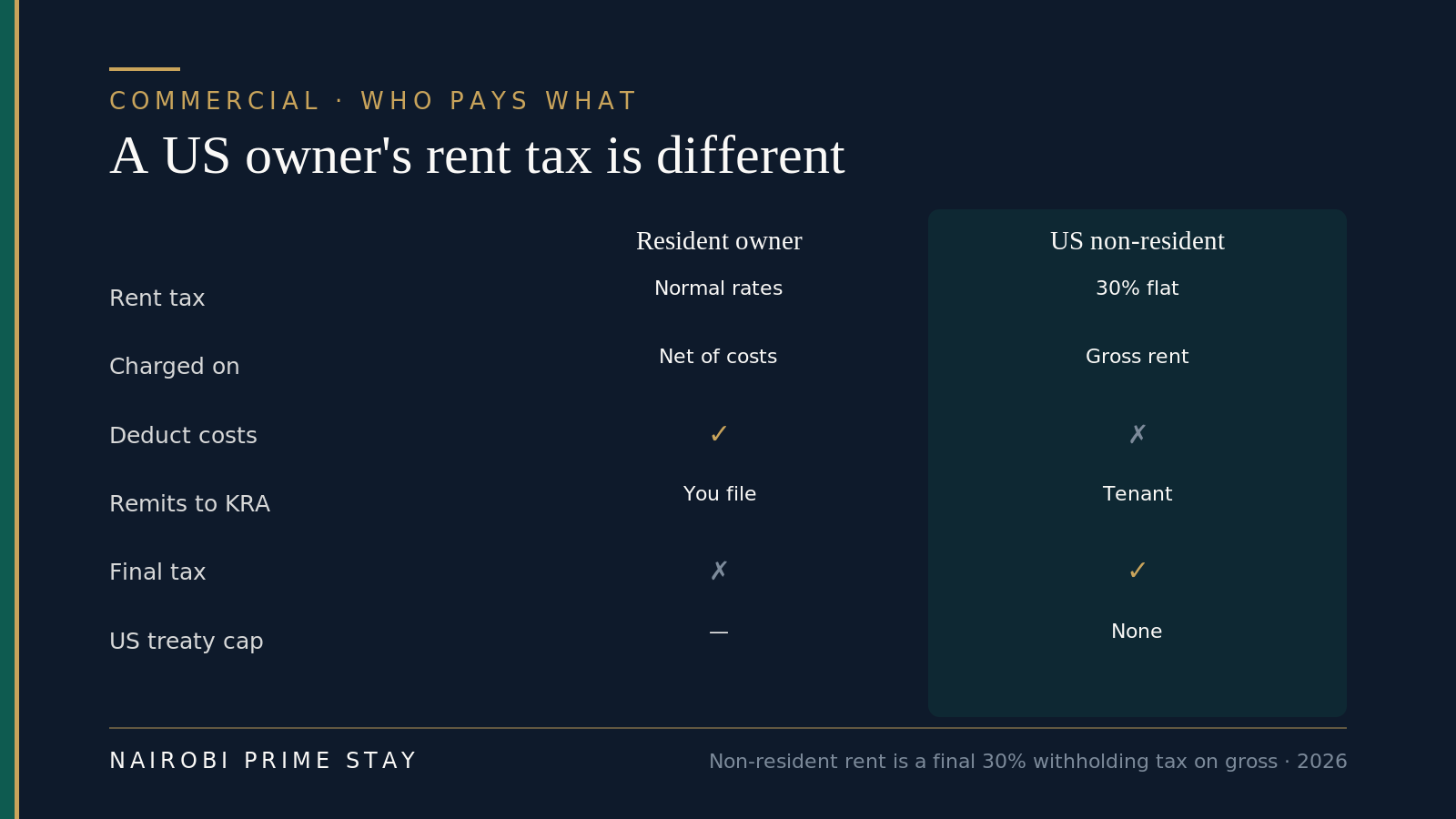

Buying from the US? Your yield comes before a 30 percent tax

Here’s the part the gross-yield headline hides for an American owner. The moment rent is paid to a non-resident landlord, Kenyan tax comes off the top — 30 percent of the gross, withheld by the tenant or the managing agent and paid straight to the Kenya Revenue Authority. It’s a final tax, so there’s no return to file on that income, but there’s no deducting your costs first either. The “taxed as business income, with deductions” route in the tax section above is the resident’s. If you live in the US, the flat 30 percent is yours.

Two things make it bite for Americans specifically. Kenya has double-tax treaties with the UK, Canada, Germany, France, the UAE, Mauritius and South Africa, and some cap the rate on rent below 30 percent. Kenya has no such treaty with the United States. So a US owner pays the full 30 percent while a British or Canadian owner next door might pay less. And because the US taxes its citizens on worldwide income, you also report the Kenyan rent on your US return — claiming a foreign tax credit (IRS Form 1116) for the Kenyan tax so the same dollar isn’t taxed twice. It generally works, but it’s paperwork, and you’ll want a cross-border accountant. Our expat tax guide goes deeper.

A US owner’s rent is taxed at a flat 30 percent of the gross — a very different number from the resident’s.

A US owner’s rent is taxed at a flat 30 percent of the gross — a very different number from the resident’s.

Then there’s VAT. Commercial rent carries 16 percent VAT that you charge the tenant and remit. The tenant bears it, not you, but you have to register once you’re over the threshold, file the returns, and accept that your space costs a tenant 16 percent more than a VAT-exempt home would.

Put numbers on it. Take the worked example above — the $400,000 Grade A floor at $33,600 a year, an 8.4 percent gross yield. Knock off the 30 percent non-resident rent tax and you keep about $23,520, or 5.9 percent on the price. Take out management, rates, insurance and the odd empty quarter, and a US owner’s net lands nearer 4 to 5 percent in a good year, before any US tax. The dollar lease is still a genuine advantage — your income doesn’t sink when the shilling slides — but the honest figure is the after-tax one, not the 8.4 percent on the brochure.

The walk from headline gross to honest net for a US non-resident owner. Illustrative, not a quote.

The walk from headline gross to honest net for a US non-resident owner. Illustrative, not a quote.

Paying in, getting paid, and taking your money home

Moving money is the easy part — Kenya has no exchange controls. You can wire the purchase price in, and later send rent and sale proceeds out, without asking anyone’s permission. That’s a real advantage over markets where getting your own money back out is the hard bit.

Do it by bank transfer, not cash. Declare any physical cash over $10,000 at the border — both countries require it — but there’s rarely a reason to carry it. The rate sits around 129 to 130 shillings to the dollar in mid-2026 (about 129.4 on the 1st of July); track it in our USD/KES currency guide and see sending money to Kenya for the cheapest ways to move a large sum. The nice twist for commercial: because prime leases are quoted and paid in dollars, a sliding shilling doesn’t erode your rent the way it erodes a shilling-denominated apartment.

Send the purchase money to your advocate’s client (trust) account — never a seller’s or an agent’s personal account — to be released on completion. That single rule prevents most horror stories; our conveyancing guide explains the escrow mechanics.

You don’t have to fly in to buy. You can complete through a power of attorney — but a US-signed PoA has to be notarized and then legalized at a Kenyan embassy or consulate, because Kenya isn’t in the Apostille Convention, so a plain apostille won’t do. Even buying remotely, run your own independent title search and send your own valuer or surveyor to the building; distance is no reason to skip diligence. Local financing is possible but pricey — commercial mortgage rates run well into double digits and are hard for non-residents — so most diaspora buyers pay cash or borrow against a US asset instead. Our property financing guide covers the options.

Buying and funding a commercial asset from abroad — no exchange controls, but a US power of attorney must be embassy-legalized, not just apostilled.

Buying and funding a commercial asset from abroad — no exchange controls, but a US power of attorney must be embassy-legalized, not just apostilled.

Running a building from 8,000 miles away

You can’t self-manage a commercial building from the US, and commercial management is a bigger job than collecting a flat’s rent. There’s the service charge and common-area upkeep, compliance and safety certificates, lease administration and rent reviews, and — the part that really matters — keeping the tenant happy enough to stay. Budget for a professional manager; commercial and facilities management typically runs about 5 to 10 percent of rent, sometimes structured differently for a single-tenant building. Our property management guide covers what good looks like.

The risk you’re really managing from afar is concentration. One or two tenants carry your entire return, and when a commercial tenant leaves the space can sit empty for many months, because there are far fewer replacement tenants than for a flat. You can’t drive past to check on it, so you lean harder on two things: the covenant you bought — a strong tenant on a long lease — and the manager you hired.

That distance is exactly why, for many US owners, the sensible commercial exposure takes one of two shapes. Either a single prime asset — a Grade A office floor or a well-let warehouse — with a strong tenant, a long dollar lease and a good manager. Or the fully hands-off route: a listed REIT. It’s worth repeating that the ALP Industrial REIT is dollar-denominated, which makes it an unusually clean fit for a dollar-earning investor who wants Nairobi logistics exposure without a title, a tenant or a 30 percent withholding form. Our diaspora property investment guide weighs the hands-on and hands-off routes side by side.

The honest pros and cons

| The case for | The case against |

|---|---|

| Higher gross yields than residential (~7.5–9.5% on the right asset) | Large entry ticket — usually well into the hundreds of thousands of dollars |

| Income often in US dollars — no shilling currency risk | Illiquid; selling a commercial building can take many months |

| Long leases (3–10 years) give predictable, plannable income | Concentrated risk — one or two tenants carry your whole return |

| Tenants often cover more running costs than residential | Heavier tax: 16% VAT, business-rate rental tax |

| Logistics demand is genuinely strong in 2026 | Offices still carry oversupply risk; more space due in 2027–2028 |

| Special economic zones offer tenant tax incentives | Needs real expertise and active management to do well |

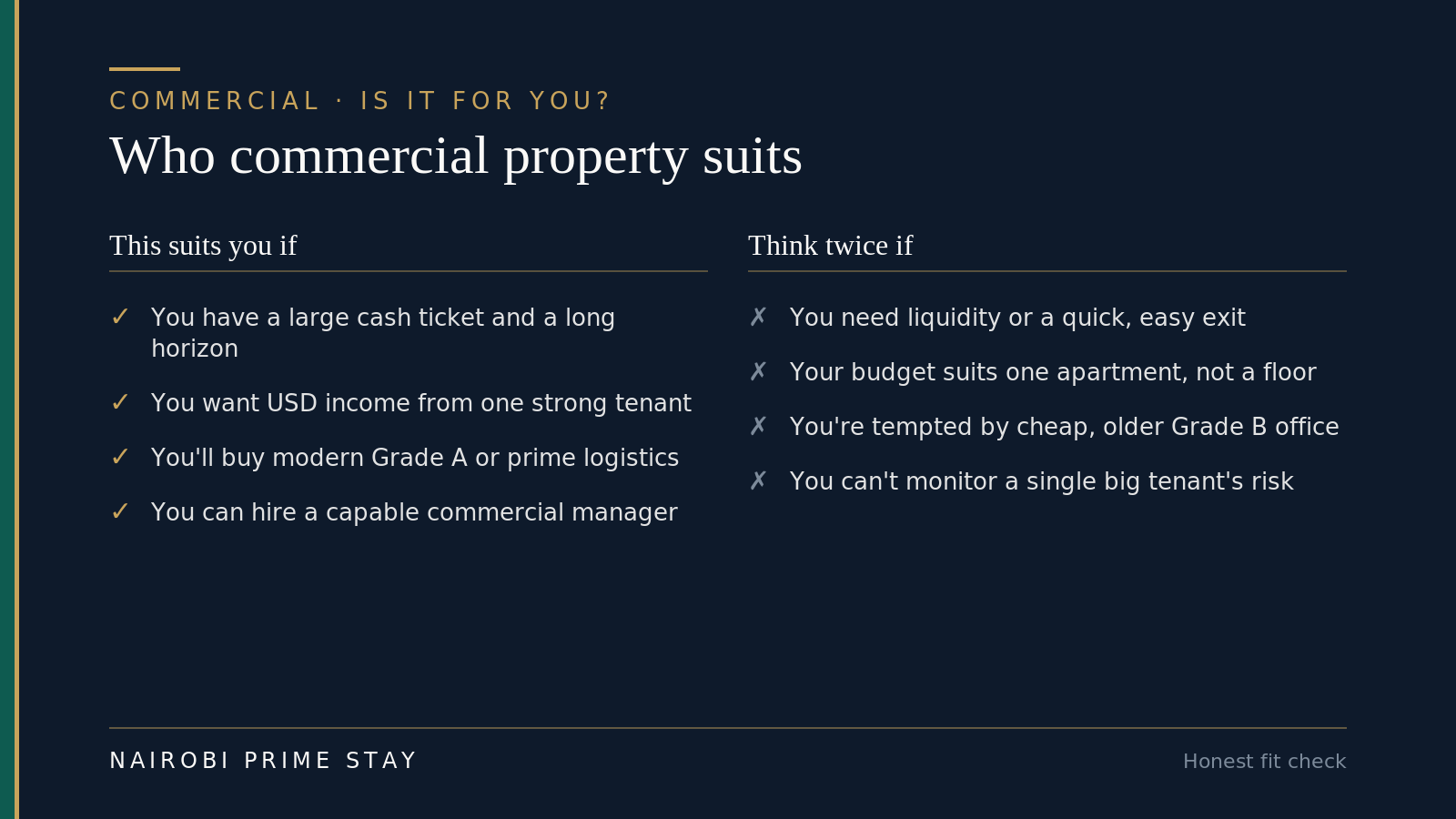

Who commercial property suits — and who it doesn’t

An honest fit check before you commit a large cheque.

An honest fit check before you commit a large cheque.

Commercial property in Nairobi suits an investor with a large cash ticket, a long time horizon, an appetite for dollar income from a strong tenant, and either the expertise to manage a building or the budget to hire someone who can. If that’s you, the right Grade A office or prime warehouse can be an excellent, dollar-paying, long-lease asset.

It doesn’t suit someone who might need their money back quickly, whose budget stretches to one apartment rather than a floor or a shed, or who’d be tempted by a cheap older Grade B office the market has already rejected. For most first-time investors in Nairobi, an apartment or a REIT is the wiser entry point — you can always graduate to commercial later.

A commercial-property checklist

Before you commit, work through this:

- Pick the segment first. Office, retail, industrial or mixed-use — each behaves differently. In 2026, logistics has the strongest fundamentals and offices reward quality only.

- Buy grade and location. A prime Grade A building in a strong node, or a well-specified warehouse on a good corridor. Never a cheap Grade B block bought on hope.

- Interrogate the tenant. Who they are, their covenant strength, the unexpired lease term, the rent-review clauses, and your exposure if they leave.

- Confirm the lease currency. Dollar leases remove your currency risk — a genuine advantage worth paying for.

- Model the net, not the gross. Deduct management, rates, insurance, service charge and a realistic void. The gross yield is the headline; the net is the truth.

- Price the tax. 16 percent VAT, stamp duty, CGT on exit — and, if you own as a US non-resident, a flat 30 percent withholding tax on your gross rent rather than the resident business rate. Get a cross-border accountant if you’re a US person.

- Use your own advocate and run full title and tenancy due diligence — see conveyancing in Kenya.

- Plan the exit. Commercial is illiquid. Know who your future buyer is before you become a seller.

- Consider a REIT instead if you want the exposure without the ticket size, the illiquidity or the management.

The hands-off alternative: REITs

If commercial property’s appeal is the income but the ticket size, illiquidity and management are off-putting, a real estate investment trust gives you most of the upside with none of the landlording. Kenya’s listed REITs let you own a slice of professionally managed commercial and residential property — including the logistics space that’s performing so well — from a small sum, with the ability to sell your units on the exchange. The ALP Industrial REIT’s heavily oversubscribed March 2026 listing — dollar-denominated, so a natural fit for a dollar investor — shows how much appetite there is for exactly this. Read our Kenya REITs guide for how they work, what’s listed, and the trade-offs versus owning a building outright.

Frequently asked questions

Is commercial property a good investment in Nairobi in 2026?

It can be, on the right asset, but it’s a large-ticket, illiquid, tenant-concentrated bet rather than a starter investment. Industrial and logistics is the strongest segment in 2026 (prime warehouse yields around 9.5 percent), offices are recovering but reward quality only (vacancy down to about 15.3 percent), and retail is steady at about 7.9 percent. Verify current figures and get professional advice before committing.

Which commercial segment has the best yields in Nairobi?

Industrial and logistics. Prime warehouse yields were around 9.5 percent in the first half of 2025, higher than offices (about 7.8 percent) or retail (about 7.9 percent), driven by e-commerce and distribution demand. The growth is concentrated in special economic zones and corridors such as Tatu City, Tilisi and the Ruiru and Mombasa Road belts.

Can foreigners buy commercial property in Kenya?

Yes, on a leasehold of up to 99 years, and most commercial land is leasehold anyway. Foreigners can’t hold freehold, and a company counts as Kenyan only if it’s 100 percent citizen-owned. Many foreign investors prefer to gain commercial exposure through a listed REIT instead, which is liquid and needs no direct ownership.

Are Nairobi commercial leases really paid in US dollars?

Often, yes — especially for prime Grade A office, retail and logistics space. Dollar-denominated leases remove the shilling currency risk for an investor who earns in dollars, and make the income more stable in real terms. Always confirm the lease currency before you buy, because it’s one of the most valuable features of a prime commercial asset.

Is Nairobi’s office oversupply over?

It’s easing, not over. Office vacancy fell to about 15.3 percent at the end of 2025 from roughly 19.3 percent a year earlier, and prime Grade A buildings are filling up (prime occupancy reached about 81.6 percent). But older Grade B space stays empty, and an estimated 2.5 million square feet is due in 2027 and 2028. Buy prime or skip offices.

How much tax do you pay on commercial property in Kenya?

More than on residential. Commercial sale and rent carry 16 percent VAT (residential is exempt), and rental income is taxed as business income rather than the simplified residential rate — which itself rose to a flat 10 percent of gross for 2026, up from 7.5 percent. You pay 4 percent stamp duty on purchase and 15 percent capital gains tax on sale. If you own as a US-based non-resident, your rent is instead hit by a flat 30 percent withholding tax on the gross. US citizens are taxed worldwide, so get cross-border tax advice. This is general information, not tax advice.

What’s the minimum to invest in Nairobi commercial property?

Direct ownership is a large-ticket game — typically hundreds of thousands of dollars for a quality office floor or warehouse. For a much smaller sum, a listed REIT gives you commercial property exposure, including logistics, that you can buy and sell on the Nairobi Securities Exchange. That’s why REITs are the common entry point for smaller and diaspora investors.

Office, retail or warehouse — which should I buy in Nairobi?

In 2026, industrial and logistics has the strongest demand and the best yields, offices reward only prime Grade A space in Westlands or Upper Hill, and retail is a steady bet if the mall has a strong anchor on a long lease. Match the segment to your risk appetite, then buy the best building you can in that segment.

How is my commercial rent taxed if I live in the US?

As a non-resident landlord, your Kenyan rent is taxed at a flat 30 percent of the gross, withheld by your tenant or managing agent and remitted to the KRA as a final tax, with no expense deductions. Kenya has no double-tax treaty with the US, so unlike a UK, Canadian or German owner you pay the full 30 percent. Because the US taxes worldwide income, you also report the rent to the IRS and claim a foreign tax credit for the Kenyan tax. Get a cross-border accountant.

Can I buy Nairobi commercial property from the US without flying in?

Yes. You can complete through a power of attorney, but a US-signed PoA must be notarized and then legalized at a Kenyan embassy or consulate — Kenya isn’t in the Apostille Convention, so an apostille alone won’t do. Wire the money to your advocate’s client (trust) account, never a personal account, and still run an independent title search and send your own valuer. Kenya has no exchange controls, so funds move in and rent and sale proceeds move out freely.

Can I get Nairobi commercial exposure in US dollars without being a landlord?

Yes, through a listed REIT. The ALP Industrial REIT, which listed on the Nairobi Securities Exchange in March 2026, is East Africa’s first industrial REIT and the exchange’s first US-dollar-denominated security, giving you logistics-property exposure in dollars from a small sum. You get professional management and can sell your units on the exchange, taking market and liquidity risk instead of the tenant, title and 30 percent-withholding grind of direct ownership.

Final thoughts

Commercial property in Nairobi is a real opportunity and a real commitment. The income is higher than residential, often in dollars, on leases you can plan around — and in 2026 the logistics segment in particular has the wind at its back. But it’s a large, slow, concentrated bet that rewards expertise and punishes the casual buyer. Pick the segment before the building, buy quality, interrogate the tenant, and model the net yield honestly.

If you’re still finding your feet in Kenya, there’s no rush. Many of our investor guests start with an apartment or a REIT, learn the market from the inside, and move into commercial once they know it well. This is general information, not legal, tax or investment advice — confirm the specifics with a Kenyan advocate and a cross-border accountant before you commit.

Related reading

- Property investment in Kenya: the complete guide — the cluster hub that ties every property topic together.

- Best areas to invest in Nairobi real estate — where the yields and growth are.

- Investing in Kenyan REITs — commercial exposure without the landlording.

- Property taxes in Kenya — VAT, stamp duty, CGT and rental tax in detail.

- New developments and satellite cities — where mixed-use and industrial schemes are clustering.

- Nairobi property prices and market trends — the wider market context.

- Buy-to-let in Nairobi — the residential comparison.

- Moving to Nairobi: the complete guide — if you’re relocating as well as investing.

Ready to know Nairobi before you invest?

The investors who do best here learn the city first. A serviced apartment for your first month gives you a secure, all-inclusive base — Wi-Fi, cleaning, generator and security included — while you meet agents, tour buildings and see which nodes are really filling up. Browse our serviced apartments, or tell our AI relocation assistant what you’re after and it’ll shortlist options in a couple of minutes. A $50 deposit reserves your place; you pay the balance on arrival.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.