Guides · Property investment

Best Areas to Invest in Nairobi Real Estate (2026)

Best Areas to Invest in Nairobi Real Estate (2026)

If you want rental income, the best bets in Nairobi right now are well-located two-bedroom apartments in Kilimani and Kileleshwa, and apartments in the satellite town of Ruaka — they earn the strongest yields in the city. If you want long-term capital growth and blue-chip tenants, the prime western suburbs — Lavington, Westlands, Riverside and the diplomatic belt around Gigiri — are steadier. There’s no single “best area.” The right one depends on whether you’re chasing yield, growth, or an easy life as a landlord.

This guide compares Nairobi’s investment areas through an investor’s lens: yield, capital growth, tenant demand and how easy each is to let and resell. We split the city into the prime apartment belt and the growth corridors, give honest 2026 numbers, and tell you who actually rents where. The figures come from HassConsult’s 2026 index, Cytonn’s reports and live listings — quoted as ranges, dated, and meant to be checked, not taken as gospel.

It’s written for Americans and diaspora buyers weighing a buy-to-let or a holiday-let, and for anyone who wants to know where their money works hardest in Nairobi. Short version: the trophy address rarely gives the best return, the highest yields sit in busy mid-market and satellite areas, and “best” is the area that matches your goal and your appetite for hassle.

TL;DR — where to invest in Nairobi (2026)

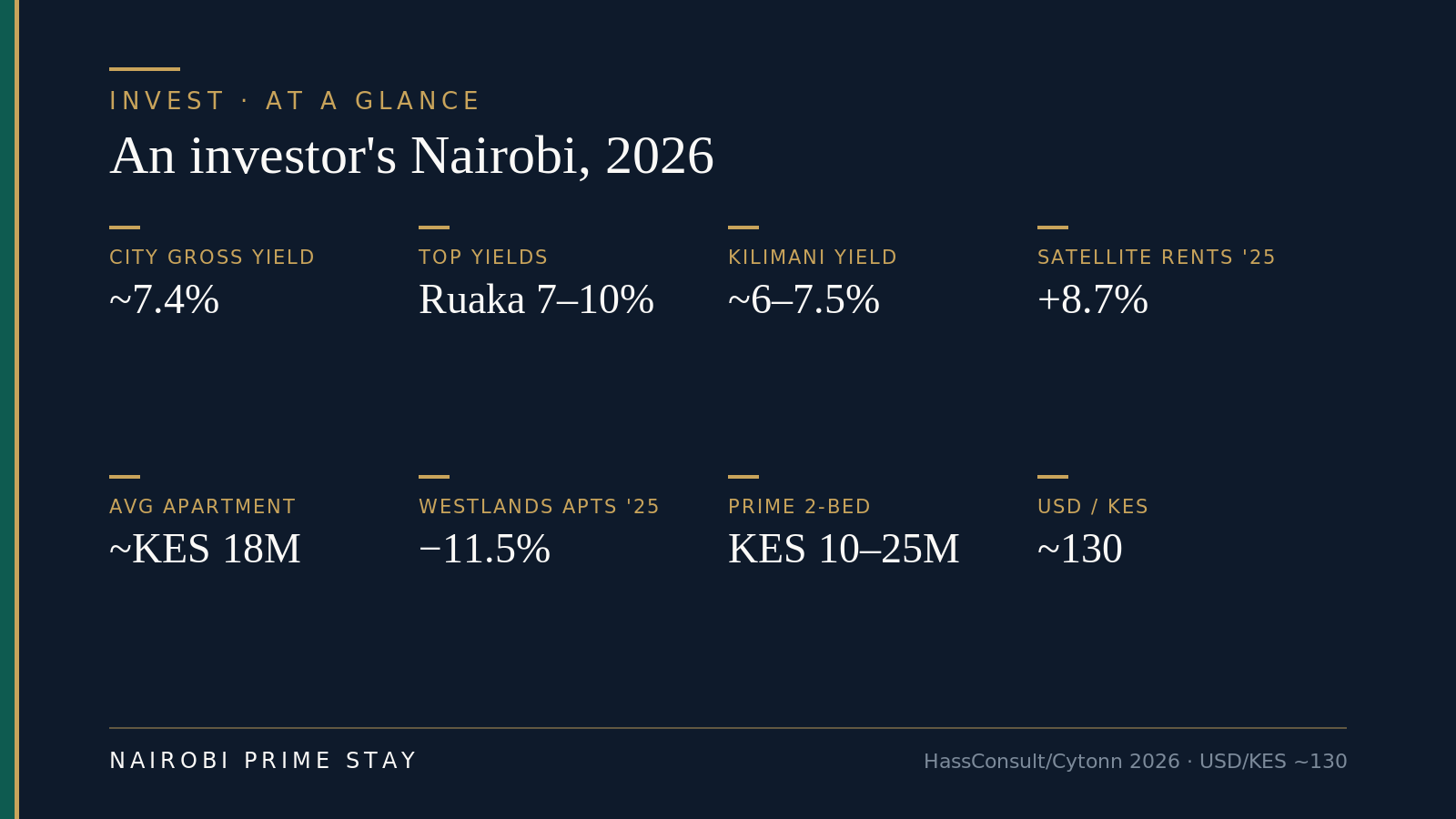

For yield, look at apartments in Kilimani (~6–7.5%), Kileleshwa and Ruaka (~7–10%) — the city-wide gross yield is about 7.4%, the best since 2007. For capital growth, prime houses in Lavington, Spring Valley, Karen and Loresho led 2026 price gains (about 3.8–4.2% a quarter). For blue-chip expat and diplomatic tenants, the Gigiri–Runda–Muthaiga belt plus Westlands, Riverside and Lavington give the most reliable rent. For lower entry prices and strong rent growth, the satellite corridors — Ruaka, Syokimau, Athi River, Ruiru/Thika Road — are rising on new roads, though some saw prices dip in early 2026. Watch oversupply: Westlands apartment prices fell about 11.5% across 2025. Quote any figure as “as of 2026” and confirm against HassConsult, Cytonn and live listings.

Why this matters

In Nairobi, the area you choose drives your return more than almost anything else — more than the building, the finish, or the price you negotiate. Two apartments bought for the same money in different suburbs can deliver wildly different rent, occupancy and resale. Get the area right and a mediocre unit still performs; get it wrong and a beautiful unit sits empty.

It matters more here than in the US because the market is less transparent. There’s no MLS, no public sold-price history, and parts of the city are oversupplied with new apartments while others are starved of good rentals. Picking the right area is how you avoid buying into a glut — and how you find the tenants who pay on time and stay. Before you commit serious money, it’s worth renting a serviced apartment for a few weeks to learn the neighbourhoods first-hand.

How to judge the “best” area for investment

“Best” depends on what you want the property to do. Weigh five things, and accept that no area wins on all five.

Rental yield. Annual rent divided by price, before costs. Smaller apartments in busy areas yield more; trophy houses yield less. If income is the goal, yield leads.

Capital growth. How fast prices rise. Prime houses and land have historically appreciated most; apartments in oversupplied pockets can stall or fall.

Tenant demand. Who rents there, how deep the pool is, and how reliably they pay. Diplomats, expats and corporate tenants pay premium rent in hard-ish currency; students and young professionals fill cheaper units fast but turn over more.

Liquidity. How easily you can re-let or resell. Established suburbs move faster than untested new estates.

Hassle and risk. Oversupply, off-plan completion risk, distance to manage, and title quality all add friction. A slightly lower yield in a safe, liquid area often beats a headline number in a risky one.

The honest rule: chase yield in the mid-market and satellite areas, chase growth and easy tenants in the prime belt, and never buy an area on the strength of one number. For the full investment picture, start with our property investing in Kenya pillar.

An investor’s Nairobi at a glance, 2026 — sources: HassConsult and Cytonn; USD/KES ~130.

An investor’s Nairobi at a glance, 2026 — sources: HassConsult and Cytonn; USD/KES ~130.

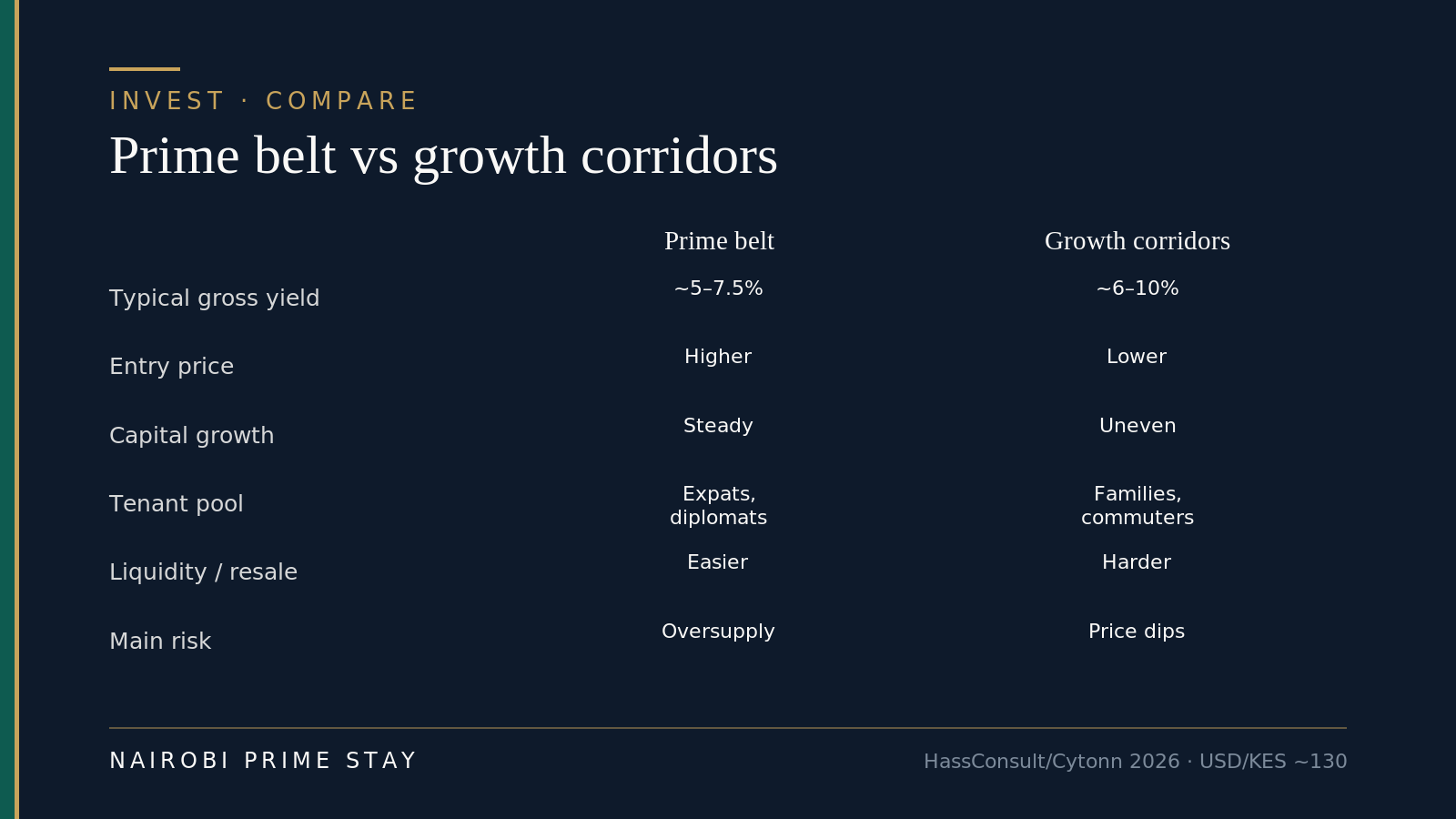

The prime apartment belt: steady tenants, moderate yields

Nairobi’s prime apartment belt is the cluster of established western suburbs where most expats, diplomats and well-paid professionals rent: Kilimani, Kileleshwa, Lavington, Westlands, Riverside and Upper Hill. These areas give you a deep, reliable tenant pool, easier resale, and steadier prices. The trade-off is moderate yields — roughly 5–7.5% gross — and, in a few pockets, real oversupply. Here’s how they stack up for an investor.

Kilimani — the yield workhorse

Kilimani is the most investable apartment area in the city for income. It’s central, modern and busy, with the deepest rental pool in Nairobi and the most affordable prime apartments. Gross yields run about 6–7.5% — among the best in the prime belt — because rents stay strong and entry prices are reasonable (a two-bed asks roughly KES 10–20M). The catch is supply: Kilimani has seen years of heavy apartment building, so you must buy a well-located, well-built block to stand out. For income with liquidity, it’s hard to beat.

Kileleshwa — quieter, leafy, in demand

Next door to Kilimani but calmer and greener, Kileleshwa attracts families and professionals who want central living without Kilimani’s bustle. Demand is deep and supply is more measured, so it’s one of the better risk-adjusted apartment areas in 2026. Yields sit a touch below Kilimani’s headline but occupancy is reliable. Two-beds ask around KES 11–22M. A solid choice if you want strong tenants without buying into a glut.

Westlands — urban hub, but mind the oversupply

Westlands is the city’s commercial and nightlife hub — offices, malls, restaurants — and a magnet for corporate tenants and singles. As a rental area, demand is genuine. As a place to buy in 2026, tread carefully: HassConsult data shows Westlands apartment sale prices fell about 11.5% across 2025, the steepest drop of any suburb, on years of oversupply. That’s painful for sellers but can hand a patient buyer a bargain with a strong long-term tenant base. Buy below the headline, and buy quality.

Lavington and Riverside — family and embassy money

Lavington is cosmopolitan and family-friendly — gardens, embassies, good schools — and it led suburb house-price growth in 2026 (about +4.2% in the first quarter). Riverside is its high-end neighbour, a strip of premium residences and embassies along the river near Westlands. Both attract diplomats, senior expats and established families who pay well and stay. Yields are moderate (these are pricier units), but tenant quality, growth and liquidity are excellent. Think capital preservation with steady rent rather than a yield play.

Upper Hill — executives and the short commute

Upper Hill is Nairobi’s business district — hospitals, corporate HQs, the Nairobi Hospital. It suits executives who want to live minutes from the office. The apartment segment here softened in early 2026 (prices off about 2.5% in the first quarter), again a supply story. For investors it’s a corporate-let play: reliable professional tenants, moderate yields, but watch the new-build pipeline.

The diplomatic belt — Gigiri, Runda, Muthaiga

If your aim is the most bankable tenants in the country, the diplomatic belt is it. Gigiri wraps around the UN headquarters and the US embassy; Runda and Muthaiga are the large-garden gated suburbs beside it. Tenants here are UN agencies, embassies, NGOs and corporates — often on housing allowances, frequently paying in or near dollars, on long, well-documented leases. Yields on big standalone houses are low (Karen-style, roughly 3–5%), but rent reliability is the highest in Nairobi and Gigiri led house-rent growth in 2026 (about +4.2%). This is a slow, safe, prestige play. Read our Gigiri neighbourhood guide for the on-the-ground detail, and see where these tenants look in our best neighborhoods in Nairobi guide.

The growth corridors: lower entry, higher yield, more risk

Beyond the prime belt, the action is on Nairobi’s edges — the satellite towns strung along the new highways. This is where prices are low enough for a first investment, yields are high, and rents are climbing fastest: satellite-town rents rose about 8.7% in 2025 while prices rose 4.5%, pushing yields up. The risk is real too. Some of these towns saw prices dip in early 2026, off-plan projects can stall, and an untested estate is harder to re-let or resell than a Kilimani block. The honest framing: more reward, more homework.

Prime belt vs growth corridors — the trade-off in one view. Sources: HassConsult and Cytonn, 2026.

Prime belt vs growth corridors — the trade-off in one view. Sources: HassConsult and Cytonn, 2026.

Ruaka — the standout for yield

Ruaka, just north-west of the city near Two Rivers and the Village Market, is the growth corridor that behaves like a prime area. It’s close in, well-served, and packed with new apartments aimed at young professionals and families priced out of Westlands. Yields are the highest in the city — roughly 7–10% gross. It’s the clearest “high yield, still convenient” play in Nairobi in 2026, and the link between the prime belt and the true satellite towns. As always, supply is heavy, so buy a strong block.

Syokimau and Athi River — the Mombasa Road corridor

South-east of the city along Mombasa Road, Syokimau and Athi River have boomed on the back of the Nairobi Expressway and the SGR train station. A commuter can reach the centre in under 30 minutes via the expressway. Entry prices are low, plots and townhouses are plentiful, and rents are rising with the population. Note the wrinkle: HassConsult recorded small price declines here in early 2026 (Athi River about −2.5%, Syokimau about −0.7%), a sign that supply is running ahead of prices even as rents climb. Good for yield and patient growth; not a quick flip.

Ruiru, Thika Road and Tatu City — the northern boom

Thika Superhighway turned the northern corridor into Nairobi’s fastest-growing residential belt. Ruiru anchors it, with apartments, gated communities and commercial space going up quickly, plus the student demand around nearby universities. The headline project is Tatu City, a large special-economic-zone “new city” with homes, schools, industry and logistics — the ALP Industrial REIT alone raised about KES 3.82 billion for logistics parks at Tatu City and Tilisi. For investors, the corridor offers low entry, real infrastructure and long-run upside, balanced against the usual new-city execution risk. See our guide to Nairobi’s new developments and satellite cities for the master-planned options.

Ngong Road, Kitengela and the rest

Ngong Road bridges the city and the south-western suburbs and has steadily densified with mid-market apartments — a decent rental area, though Ngong town itself saw prices ease in early 2026. Kitengela, further south past Athi River, is a high-yield, low-entry plot-and-build market that demands extra title care. The pattern across all the corridors is the same: cheaper money, stronger yields, faster rent growth — paired with thinner liquidity and the need for serious due diligence on title and developer.

The investment areas compared

Here’s the whole city in one table — indicative 2026 price bands, gross yields, who rents, and what each area is best for. Treat the numbers as starting ranges to verify, not quotes; actual sale prices often sit below asking in a slow market. Full price detail is in our Nairobi property prices in 2026 guide, and the return math is in buy-to-let in Nairobi.

Where to look and who rents there — Nairobi’s main investment areas, 2026.

Where to look and who rents there — Nairobi’s main investment areas, 2026.

| Area | Type | Indicative price (2-bed apt unless noted) | Gross yield | Who rents there | Best for |

|---|---|---|---|---|---|

| Kilimani | Prime apartments | KES 10–20M | ~6–7.5% | Young professionals, expats | Yield + liquidity |

| Kileleshwa | Prime apartments | KES 11–22M | ~6–7% | Families, professionals | Risk-adjusted income |

| Westlands | Prime apartments | KES 12–25M | ~5–6.5% | Corporate tenants, singles | Bargain hunting, long-term |

| Lavington | Prime apt / town houses | KES 10–22M | ~5–6% | Families, diplomats | Growth + steady rent |

| Riverside | Prime apartments | KES 13–26M | ~5–6% | Diplomats, senior expats | Prestige, capital safety |

| Gigiri / Runda / Muthaiga | Diplomatic houses | KES 40–150M+ (houses) | ~3–5% | UN, embassies, NGOs | Bankable tenants, prestige |

| Ruaka | Growth apartments | KES 6–14M | ~7–10% | Young families, professionals | Highest yield, still close in |

| Syokimau / Athi River | Growth apts / town houses | KES 5–12M | ~6–8% | Commuters, families | Low entry, rising rents |

| Ruiru / Thika Road | Growth apts / estates | KES 4–10M | ~6–9% | Families, students | Infrastructure-led growth |

Who rents where — and why it decides your return

The single best predictor of a good rental is a deep, reliable tenant pool. In Nairobi the pools are distinct, and matching your unit to one is half the job.

Diplomats, UN and embassy staff are the gold standard — long leases, housing allowances, often dollar-linked rent, low default. They cluster in Gigiri, Runda, Muthaiga, and spill into Westlands, Riverside and Lavington. Buy a quality house or large apartment near the UN and your tenant risk is about as low as it gets in Kenya.

Corporate expats and senior professionals want Westlands, Riverside, Lavington, Kileleshwa and Upper Hill — close to offices, malls and good schools. They pay well and value security and backup power above all.

Young Kenyan and expat professionals fill Kilimani, Kileleshwa, Westlands and Ruaka. This is the deepest, fastest-moving pool — smaller two-beds let quickly here, which is exactly why these areas yield well.

Students drive demand around the universities — Parklands, the Thika Road corridor near campuses, and Ruiru. Purpose-built student housing (the kind Acorn’s REITs fund) targets this pool specifically.

Mid-income families are the engine of the satellite towns — Ruaka, Syokimau, Athi River, Ruiru, Kitengela — where a family budget buys a townhouse instead of a city studio. This is where rent growth has been fastest.

Match your goal to your area — the quickest way to narrow the field.

Match your goal to your area — the quickest way to narrow the field.

If your goal is income with the least hassle, the answer might not be a building at all: listed REITs on the Nairobi Securities Exchange (accessible to foreigners through Acorn’s Vuka platform from a few hundred shillings) give you property exposure without tenants or title risk. We cover that route in the property investing in Kenya pillar.

A realistic example

Say you have about $130,000 (roughly KES 17M) and want rental income. You compare two options. Option A: a trophy three-bed in a prestige suburb at the top of your budget, asking high, likely yielding 3–4% with a small, picky tenant pool. Option B: a well-built two-bed in Kilimani with a generator, borehole, lift and fibre, bought at KES 16.5M after negotiating below asking. It rents for about KES 95,000–110,000 a month to a young professional — a gross yield near 7%. Add roughly 8–10% in transaction costs up front, and budget for service charge, management and the odd void.

Option B wins on income, lets faster, and resells more easily, even though Option A feels more impressive. That’s the pattern across Nairobi: the best return and the best address are rarely the same property. Run the numbers in our buy-to-let and financing guides before you choose.

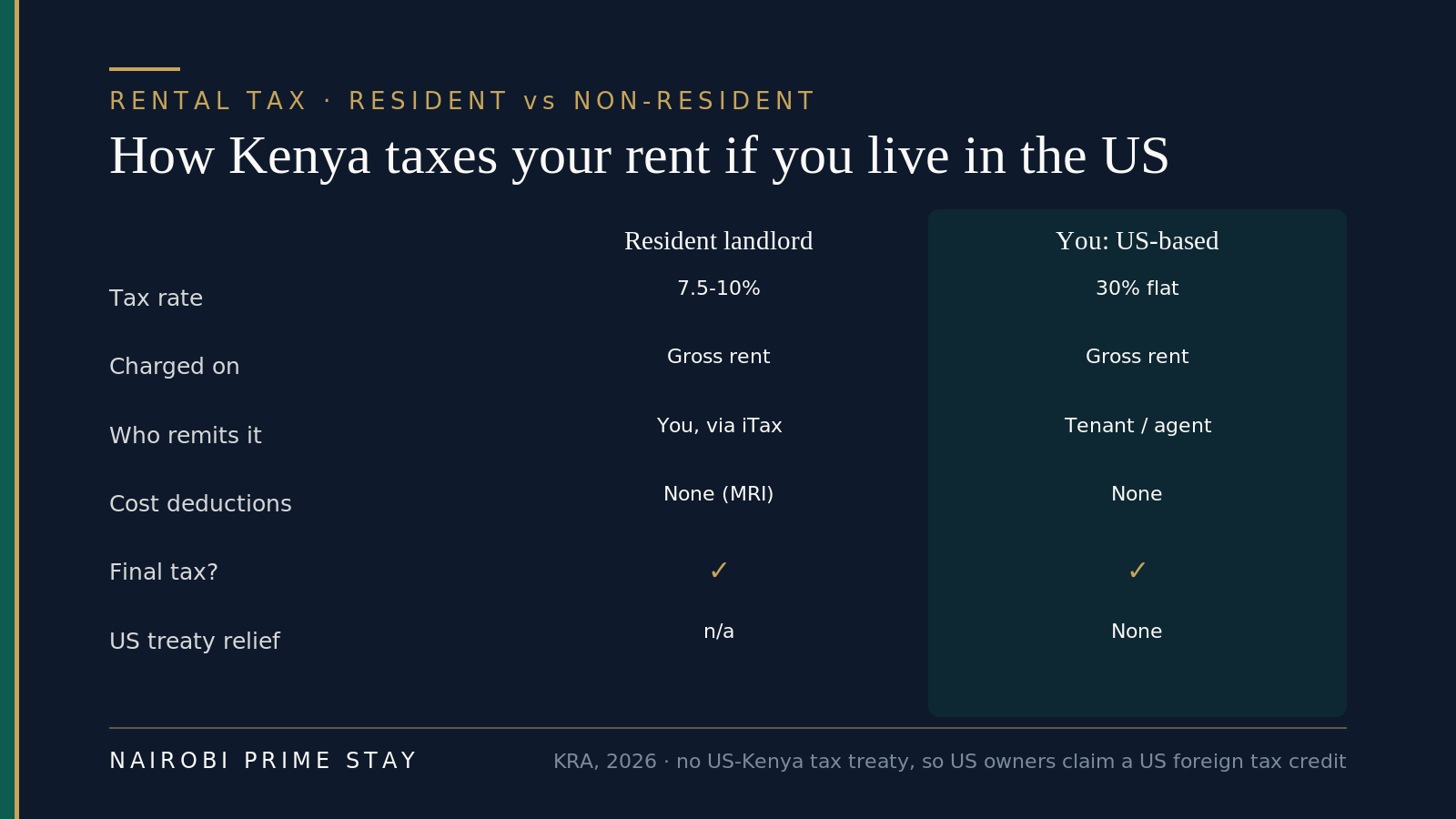

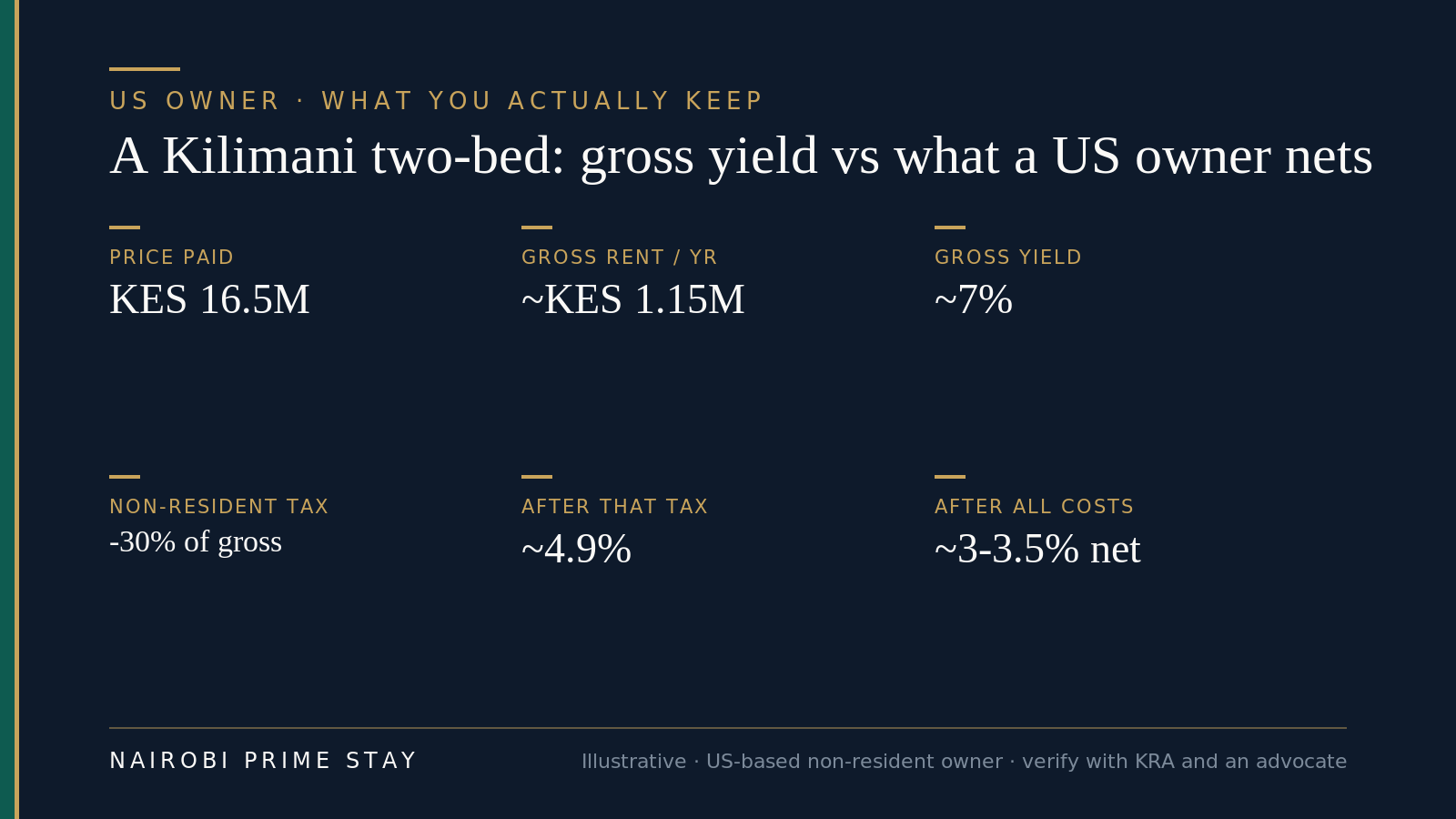

Buying from the US: your yield is before the 30% tax

Every yield in this guide is a gross number, and gross flatters a US owner more than most. Here’s the part that changes the math: if you live in the US and rent out a Kenyan property, you’re a non-resident landlord, and Kenya taxes your rent at a flat 30% of the gross — not the 7.5–10% a resident pays. Your tenant or letting agent is required to withhold that 30% and remit it to the Kenya Revenue Authority by the 20th of each month. It’s a final tax, so there’s nothing to deduct and little to reclaim on the Kenyan side.

Kenya has tax treaties with the UK, Canada, Germany and a handful of other countries that can cut that rate. It does not have one with the United States. So a US owner pays the full 30%, then claims a US foreign tax credit (IRS Form 1116) so the same rent isn’t taxed twice. You still file in both countries. Our taxes for expats in Kenya and property taxes in Kenya guides walk through the mechanics.

Resident vs non-resident landlord — the 30% is the number US owners plan around. Source: KRA, 2026.

Resident vs non-resident landlord — the 30% is the number US owners plan around. Source: KRA, 2026.

What does that do to a real return? Take the Kilimani two-bed from the example above. A ~7% gross yield on a KES 16.5M unit is about KES 1.15M in rent a year. Knock off the 30% non-resident tax and you’re at roughly 4.9% before you’ve paid anyone else. Add management, service charge and a realistic vacancy allowance and the number a US owner actually banks is closer to 3–3.5% net. That’s not a reason to walk away — it’s a reason to buy on net yield, not the headline.

The gap between gross and net for a US-based owner — plan around the net. Illustrative; verify with KRA and an advocate.

The gap between gross and net for a US-based owner — plan around the net. Illustrative; verify with KRA and an advocate.

The 30% haircut hits every area equally, so it doesn’t change which area wins — but it does raise the bar. A 5% gross prime unit can net under 3% for a US owner, while a well-let 8% gross unit still clears 4–5%. Run your shortlist through the buy-to-let math on a net, after-tax basis before you fall for a glossy gross figure.

Running it from abroad: management, money and which areas suit

You can’t self-manage a Nairobi rental from the US, so budget for someone who can. A full-service property manager or letting agent typically charges around 8–10% of the rent for a long let (more for a furnished short-let), and earns it — vetting tenants, chasing rent, handling repairs, and being the person who actually shows up. Factor that into your net yield from day one. Our property management in Nairobi guide covers what a good manager does and what to pay.

Managing at a distance also quietly argues for the liquid prime belt over the cheapest far-flung estate. A vacant two-bed in Kilimani you can re-let in a week is a very different risk from a half-finished townhouse in a satellite town you’ve never seen and can’t easily check on. When you’re 12,000 km away, liquidity and a deep tenant pool are worth paying for. If you’re buying sight-unseen, read diaspora property investment in Kenya first — it’s written for exactly this situation.

Moving the money is the easy part. Kenya has no exchange controls, so you can bring dollars in and take shillings back out freely — pay the deposit and balance by bank transfer or a service like Wise into your advocate’s account (never a personal one), and declare any cash over USD 10,000 both on the way in and out. Rent and, eventually, sale proceeds convert back to dollars and repatriate without special permission; you just wear the exchange-rate spread. See our USD to KES currency guide and sending money to Kenya for the cheapest, cleanest ways to do it.

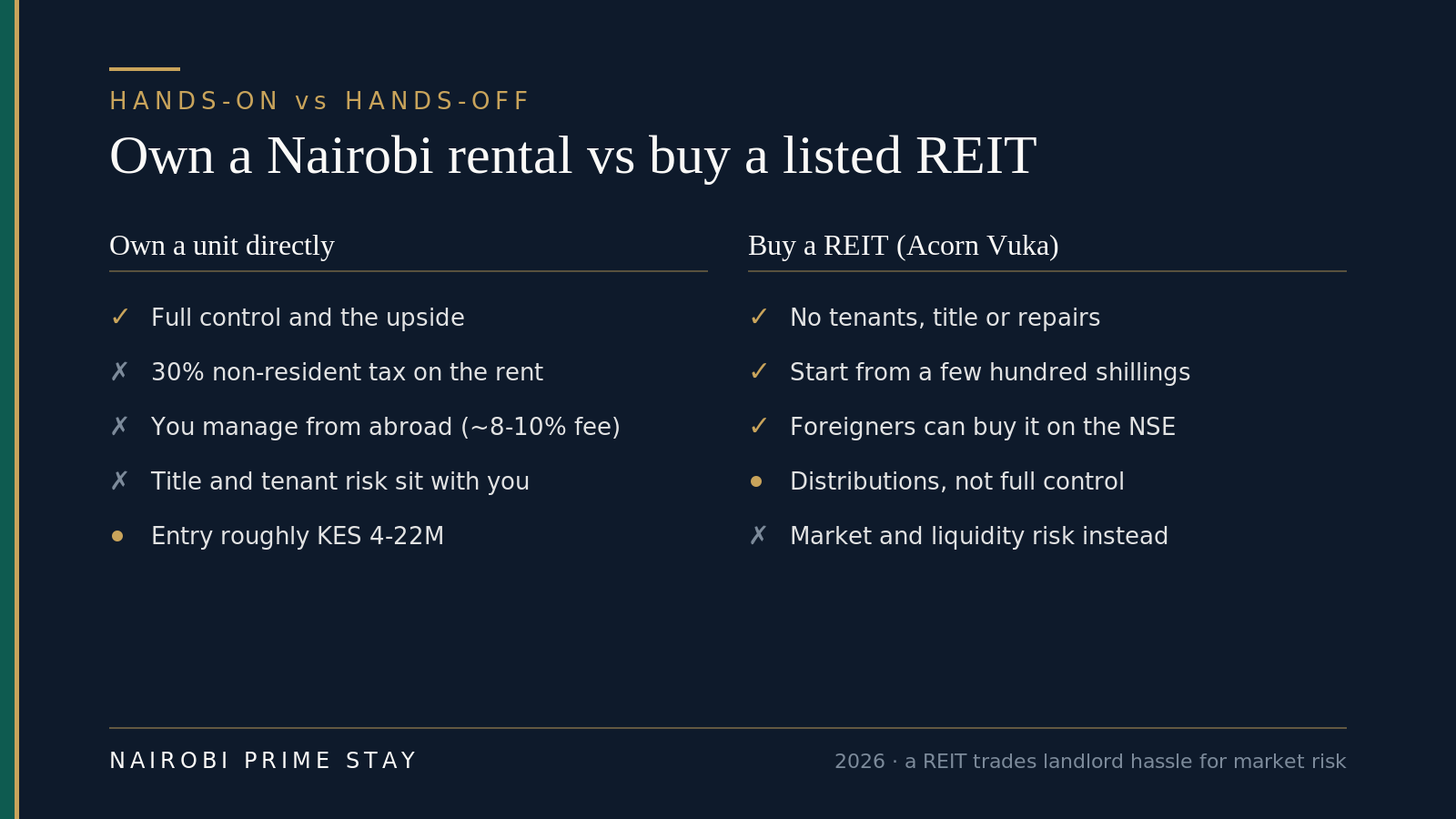

The hands-off route: REITs for exposure without the grind

If the 30% tax, remote management and title homework are starting to sound like a second job, there’s a lighter way to own Nairobi property: a REIT. A real estate investment trust pools investors’ money to own income property and lists on the Nairobi Securities Exchange, so you buy a slice the way you’d buy a share. Acorn’s Vuka platform opens its student-housing REITs to individuals — including foreigners — from a few hundred shillings, and ILAM Fahari trades on the main market. You get exposure to real Nairobi rental income without a single tenant, title search or midnight plumbing call.

The trade-off is honest: you swap a landlord’s control and gearing for market and liquidity risk, you take distributions rather than run the asset, and Kenya’s listed REIT market is still thin. But for a US investor who wants in on the ~7% yield story without becoming a non-resident landlord, it’s the simplest entry there is. We cover the options in the Kenya REITs guide and the wider property investing in Kenya pillar.

Direct ownership vs a REIT — control and upside on one side, simplicity on the other.

Direct ownership vs a REIT — control and upside on one side, simplicity on the other.

The risks worth pricing in

No area is a sure thing. Before you buy, price these in honestly:

Apartment oversupply. Years of building have flooded parts of Kilimani, Westlands and Upper Hill with new units. Oversupply caps rent growth and can push prices down (Westlands fell about 11.5% in 2025). It’s good for buyers and renters, tough for sellers. Buy quality in a strong micro-location, not just the cheapest unit in a crowded block.

Satellite-town price wobbles. High yields in the corridors come with thinner, more volatile prices — Athi River, Ngong and Syokimau all dipped in early 2026 even as rents rose. Expect a longer hold and harder resale than in the prime belt.

Off-plan completion risk. Developer payment plans fund much of the new supply, but projects stall and timelines slip. Only buy off-plan from developers with a real completion record, and structure payments against milestones.

Title and land risk. This is where the worst losses happen, especially on land and in satellite towns. Verify a clean title before anything else — read property taxes in Kenya for the holding costs and lean on a good advocate for the search and transfer.

Currency. If you earn dollars and the rent is in shillings, the exchange rate moves your real return. The shilling has held near KES 129.5 through mid-2026, but the rate moves your real return, so budget for swings.

Smart moves and costly mistakes

Picking an investment area — the moves that make money and the mistakes that lose it.

Picking an investment area — the moves that make money and the mistakes that lose it.

The thread running through every smart move is the same: buy the tenant, not the postcard. A reliable rental in a slightly dull, well-supplied area beats a glamorous unit you can’t keep occupied. And run the net yield — after service charge, management, tax and a realistic vacancy allowance — not the gross headline. A 9% gross in a far satellite town can net less than a 6.5% gross in Kilimani once costs and voids are real.

How to choose your area (checklist)

- Decide your priority first: yield, capital growth, or bankable tenants. You can’t max all three.

- Shortlist two or three areas that match that priority, not just the ones you’ve heard of.

- Pull 5–10 comparable rentals and 5–10 sale listings in each, on at least two portals.

- Calculate the gross yield (annual rent ÷ price) and compare to the ~7.4% city average.

- Then calculate the net yield after service charge, management, tax and a vacancy allowance.

- Check the tenant pool — who rents here, how fast units let, how reliably they pay.

- Test for oversupply: how many new blocks are going up within a few hundred metres?

- Verify the building essentials (generator, water, security, lift, fibre) and the service charge.

- Verify a clean title with an independent advocate before you fall for the price.

- If you’ll own from the US, run the net yield after the 30% non-resident tax and ~8–10% management — not the gross.

- Decide between owning a unit directly and a hands-off REIT before you commit serious money.

- Budget 8–10% transaction costs, and re-check every figure as “of 2026” against HassConsult and live listings.

Frequently asked questions

What is the best area to invest in real estate in Nairobi?

There’s no single best area — it depends on your goal. For rental income, well-located two-bed apartments in Kilimani and Kileleshwa, and apartments in Ruaka, offer the strongest yields (about 6–10% gross). For capital growth and blue-chip tenants, the prime western suburbs — Lavington, Westlands, Riverside and the diplomatic belt around Gigiri — are steadier. For low entry prices and fast-rising rents, the satellite corridors (Syokimau, Athi River, Ruiru) are growing on new highways. Match the area to whether you want yield, growth or the easiest tenants.

Which area in Nairobi has the highest rental yield?

Ruaka has the highest gross rental yields in 2026 — roughly 7–10% — while staying close to the city near Two Rivers. Kilimani follows at about 6–7.5%, helped by deep tenant demand and reasonable entry prices. The city-wide average gross yield is about 7.4%, the best since 2007. Smaller, well-located apartments yield more than big prestige houses, which often sit at just 3–5%.

What are the up-and-coming areas in Nairobi for property investment?

The growth corridors along Nairobi’s new highways are the up-and-coming areas: Ruaka to the north-west, Syokimau and Athi River along Mombasa Road and the SGR, and Ruiru and the Thika Road belt around Tatu City. They offer lower entry prices and rents that rose about 8.7% in 2025, faster than the prime suburbs. The trade-off is thinner liquidity and some price volatility — Athi River and Syokimau saw small price dips in early 2026 even as rents climbed — so expect a longer hold.

Are apartments in Nairobi a good investment in 2026?

They can be, if you buy the right one. Apartments in high-demand areas like Kilimani, Kileleshwa and Ruaka deliver solid gross yields of about 6–10% and let quickly. But parts of the city are oversupplied — Westlands apartment prices fell about 11.5% across 2025 — which caps rent growth and can push prices down. Buy a well-built block in a strong micro-location with a deep tenant pool, run the net yield after costs, and avoid the cheapest unit in a crowded new development.

Where do expats and diplomats rent in Nairobi?

UN, embassy and NGO staff cluster in the diplomatic belt — Gigiri, Runda and Muthaiga — near the UN headquarters and the US embassy, often on long, allowance-backed leases. Corporate expats and senior professionals also rent in Westlands, Riverside, Lavington, Kileleshwa and Upper Hill, close to offices and good schools. These tenants pay reliably and value security and backup power, which makes the prime belt a lower-risk landlord play even at moderate yields.

Should I invest in Nairobi’s prime suburbs or the satellite towns?

Prime suburbs (Kilimani, Kileleshwa, Westlands, Lavington, Riverside) give steadier prices, deeper tenant pools and easier resale, with moderate yields around 5–7.5%. Satellite towns (Ruaka, Syokimau, Athi River, Ruiru) give lower entry prices and higher yields of about 6–10%, but with more price volatility, thinner liquidity and more due-diligence risk. Choose prime if you want safety and growth, satellite if you want yield and can hold longer. Many investors do best with mid-market apartments that bridge the two, like Kilimani or Ruaka.

How much money do I need to start investing in Nairobi property?

A small one- or two-bed apartment in a growth corridor like Ruiru or Syokimau can start around KES 4–8 million (roughly $30,000–$60,000), while a prime two-bed in Kilimani or Kileleshwa runs about KES 10–22 million ($80,000–$170,000). Budget another 8–10% on top for stamp duty, legal and valuation costs. If that’s out of reach, listed REITs via Acorn’s Vuka platform give property exposure from a few hundred shillings, with no tenants or title risk.

What rental yield can I expect in Nairobi?

Gross rental yields average about 7.4% city-wide in 2026 — the highest in years. Apartments in high-demand areas yield more (Kilimani roughly 6–7.5%, Ruaka up to 7–10%), while large prestige houses in Karen or the diplomatic belt yield less, around 3–5%. Satellite towns average about 5.3%. Gross yield is annual rent divided by price before costs, so always work out the net yield after service charge, management, tax and vacancy.

How is my Nairobi rental income taxed if I live in the US?

As a US-based non-resident landlord, your Kenyan rent is taxed at a flat 30% of the gross — not the 7.5–10% a resident pays. Your tenant or agent withholds it and remits it to the KRA by the 20th of each month, and it’s a final tax with no deductions. There’s no US–Kenya tax treaty to reduce it, so you pay the 30% and then claim a US foreign tax credit (Form 1116) to avoid being taxed twice. Plan returns on a net, after-tax basis: a 7% gross yield can net closer to 3–3.5% once tax, management and vacancy are counted.

Can I manage a Nairobi rental property from the US?

Not directly — you’ll need a local property manager or letting agent, who typically charges about 8–10% of the rent for a long let. That cost, plus the distance, is a good reason to favor the liquid prime belt (Kilimani, Kileleshwa, Westlands) over a cheap, hard-to-check estate far out of town. Moving money is straightforward: Kenya has no exchange controls, so you pay in and repatriate rent and sale proceeds freely, minus the exchange-rate spread. Declare any cash over USD 10,000 in or out.

Can I invest in Nairobi real estate without buying a property?

Yes. Listed REITs on the Nairobi Securities Exchange give you property exposure without tenants, title risk or the 30% non-resident landlord tax. Acorn’s Vuka platform opens its student-housing REITs to individuals, including foreigners, from a few hundred shillings, and ILAM Fahari trades on the main market. You take distributions and market risk instead of running an asset — the simplest way for a US investor to back the ~7% yield story hands-off.

Final thoughts

Nairobi rewards investors who buy the tenant, not the trophy. The best returns sit in well-located mid-market apartments — Kilimani, Kileleshwa, Ruaka — and in the satellite corridors riding the new highways, not in the prestige houses that look best on paper. The prime belt and the diplomatic suburbs earn their keep through reliable, bankable tenants and steadier growth. Pick your priority first, match two or three areas to it, run the net yield, verify the title, and check the supply pipeline before you commit.

A quick disclaimer: this is general guidance for 2026, not investment, tax or legal advice. Yields and prices move and vary by the specific unit — verify current figures against HassConsult, Cytonn and live listings, and lean on a good local agent and advocate before you buy.

Related reading

- Start with the property investing in Kenya pillar for the full picture.

- Price the market with Nairobi property prices in 2026 and run returns in buy-to-let in Nairobi.

- Weigh the hands-on route in Airbnb and short-let investment in Nairobi.

- Explore master-planned options in Nairobi’s new developments and satellite cities.

- Budget the extras with property taxes in Kenya and financing and mortgages.

- Buying from abroad? Read diaspora property investment, taxes for expats in Kenya, property management, Kenya REITs, and the USD to KES currency guide.

- New to the city? See where expats live, the Gigiri guide, and the moving to Nairobi hub.

Ready to look — or want a soft landing first?

Scouting investment areas is far easier from the ground. A serviced apartment for your first weeks gives you a secure, all-inclusive base while you view neighbourhoods, meet agents and test the traffic — Wi-Fi, cleaning, generator and security included, with a $50 deposit to reserve and the balance on arrival. Want a shortlist of areas and apartments that fit your budget and goal? Our AI relocation assistant can pull options together in a couple of minutes, any time.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.