Guides · Healthcare

Health Insurance in Kenya for Expats: The 2026 Guide

Health Insurance in Kenya for Expats: The 2026 Guide

Health insurance is the one piece of your move you should sort before you book the flight. Kenya has excellent private hospitals, but you pay to use them, and a serious emergency can mean being flown to a bigger center. The right policy turns all of that into a phone call instead of a five-figure bill.

This guide is for Americans moving to Nairobi — retirees, remote workers, families, employees on a local contract. It explains the two systems you’ll deal with (the national scheme and private insurance), the real difference between an international plan and a local one, why medical evacuation cover matters more here than at home, what it all costs, and how to choose. We use 2026 figures, flag what changes, and point you to the official sources to confirm against.

If you only read one section, read the next one.

Quick answer

Most American expats in Kenya use the private healthcare system and pay for it with private insurance — either an international (global) plan or a regional/local plan. The one feature you must not skip is medical evacuation. Kenya’s new national scheme, SHA (the Social Health Authority, which replaced NHIF in late 2024), is a legal baseline you’ll likely pay into if you’re employed on a Kenyan contract — 2.75% of gross salary — but it is not designed to be an expat’s main cover.

For a healthy adult, a solid regional plan (Kenya and East Africa) with evacuation runs very roughly $1,500–$3,000 a year. A full international plan that also covers treatment abroad costs more — often $3,000–$8,000+ depending on age, scope and limits. Older movers and anyone with a chronic condition should expect to pay more and shop earlier. Premiums vary widely, so get real quotes; the bands here are a starting point, not a promise.

The honest version: pick the level of cover that matches how you’ll actually live — staying mostly in Nairobi, traveling the region, or wanting the option to fly home for major treatment — and make sure evacuation and the big private hospitals are both included.

Why this matters

In Kenya you use the private system, and private care is pay-as-you-go. Walk into a top hospital without insurance and you’ll be asked for a deposit before anything happens. Routine visits are cheap by US standards — a specialist consult is roughly $15–40 — but a major operation, an ICU stay, or a cancer course runs into thousands, and a medical flight can cost more than a year’s premium on its own.

Insurance does two jobs here. It caps your exposure on a big event, and it gives you direct billing (sometimes called cashless) so the hospital invoices your insurer instead of you. Without it, you’re the bank.

Evacuation is the part newcomers underestimate. Nairobi’s private hospitals are genuinely good, but if you’re on the coast, upcountry, or traveling in the region and something serious happens, you may need a flight to reach the right specialists. That flight is what evacuation cover buys. For a balanced picture of the hospitals and care quality behind all this, read our healthcare in Nairobi guide; this article is the deep-dive on the insurance itself.

The two systems you’ll deal with

The shape of health cover for an American moving to Kenya, 2026. Verify current figures with each insurer and at sha.go.ke.

There are two layers. The first is SHA, Kenya’s national health scheme — a legal requirement for people on a Kenyan payroll, but limited in what it does for an expat. The second is private insurance, which is what almost every expat actually relies on. Most people end up with private cover and treat SHA as a small mandatory contribution on the side.

Get the private layer right and the national one takes care of itself.

What SHA covers (and what it doesn’t) for foreigners

SHA is the Social Health Authority, which runs the Social Health Insurance Fund (SHIF). It replaced the old NHIF in October 2024 under the Social Health Insurance Act of 2023. If you’re employed on a Kenyan contract, you contribute 2.75% of your gross monthly salary, with a minimum of about KES 300 a month and — unlike the old NHIF — no upper cap. Your employer deducts it from payroll and remits it, currently by the 9th of the following month. Self-employed and non-salaried residents pay a means-assessed contribution instead, also from a KES 300 floor.

Here’s the honest part for expats. SHA is built around empaneled facilities — mostly public hospitals plus some private ones — and benefit limits that are modest next to private-hospital bills. Many of the private hospitals expats actually use either aren’t fully covered or only cover part of a bill. The scheme is also new and still bedding in, with rules and provider lists that have shifted since launch.

So treat SHA as what it is: a baseline and a legal obligation if you’re on a local payroll, not your real protection. Don’t cancel or skip private cover because you’re paying into SHA. Confirm the current contribution rules, benefits and empaneled hospitals at the official portal, sha.go.ke, because the details are still moving.

If you’re employed in Kenya, SHA contributions sit alongside your other payroll deductions — see how that fits the wider picture in our taxes for expats in Kenya and cost of living in Nairobi guides.

International vs local plans — the real decision

This is the choice that matters. Both kinds of plan are sold in Kenya, and the right answer depends on how you’ll live.

An international (global) plan is portable and broad. It covers private treatment in Kenya, usually includes treatment in other countries, and often lets you choose a region that includes or excludes the US. The big names you’ll see marketed to expats include Allianz Care, Bupa Global, AXA, April International and GeoBlue or William Russell for some nationalities. (A quirk worth knowing: Cigna Global, a name many Americans recognize, generally isn’t sold to people who are resident in Kenya, though it covers many other countries — so don’t be surprised if a broker steers you to Allianz instead.) International plans are the priciest option, but they travel with you and are strong on big, complex treatment and on flying you elsewhere.

A local or regional plan is bought from a Kenyan insurer and built around Kenyan hospitals. The established names include Jubilee Health, AAR, Britam, APA, Madison, CIC and Old Mutual/UAP. These cost less, have excellent direct-billing networks at the private hospitals you’ll use, and handle everyday care well. The trade-off is geography: cover is centered on Kenya and East Africa, with limited or no benefit for planned treatment overseas.

Many expats combine the two — a local plan for day-to-day and outpatient care, plus an international layer or a standalone evacuation membership for major events and flights. That hybrid is common and often the best value.

Three layers, three jobs. Most expats rely on a private plan and treat SHA as a small mandatory baseline.

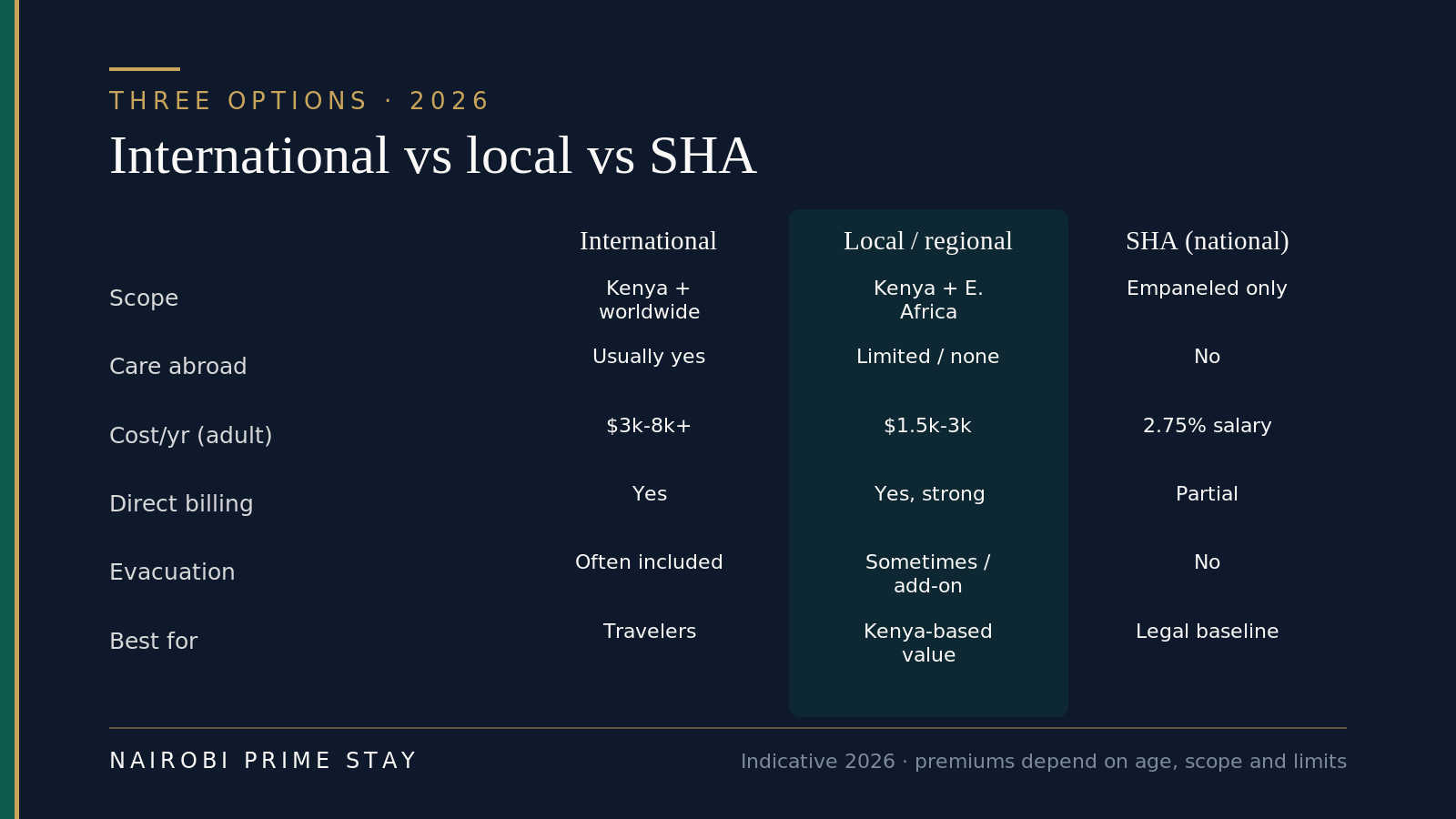

International vs local at a glance

| Feature | International (global) plan | Local / regional plan | SHA (national) |

|---|---|---|---|

| Sold by | Allianz, Bupa Global, AXA, April, etc. | Jubilee, AAR, Britam, APA, CIC, etc. | Social Health Authority |

| Geographic cover | Kenya + worldwide (you pick the region) | Kenya + East Africa | Kenya, empaneled facilities |

| Treatment abroad | Yes, usually included | Limited or none | No |

| Typical cost/yr (healthy adult) | ~$3,000–8,000+ | ~$1,500–3,000 | 2.75% of salary |

| Private-hospital direct billing | Yes | Yes, strong local networks | Partial / limited |

| Medical evacuation | Often included | Sometimes; often add-on | No |

| Best for | Frequent travelers, complex needs, “fly me home” | Staying mostly in Kenya, value, everyday care | Legal baseline only |

Figures are indicative for 2026 and depend heavily on age, the limits you choose and any pre-existing conditions. Get a written quote before you decide.

Why medical evacuation cover matters

Medical evacuation is the benefit that pays to move you — by air ambulance or arranged flight — to a hospital that can actually treat what’s wrong. In a country where the best specialists cluster in a few Nairobi hospitals, and where you may be traveling to the coast, upcountry or across the region, that’s not a luxury. It’s the difference between hours and a very long, very expensive scramble.

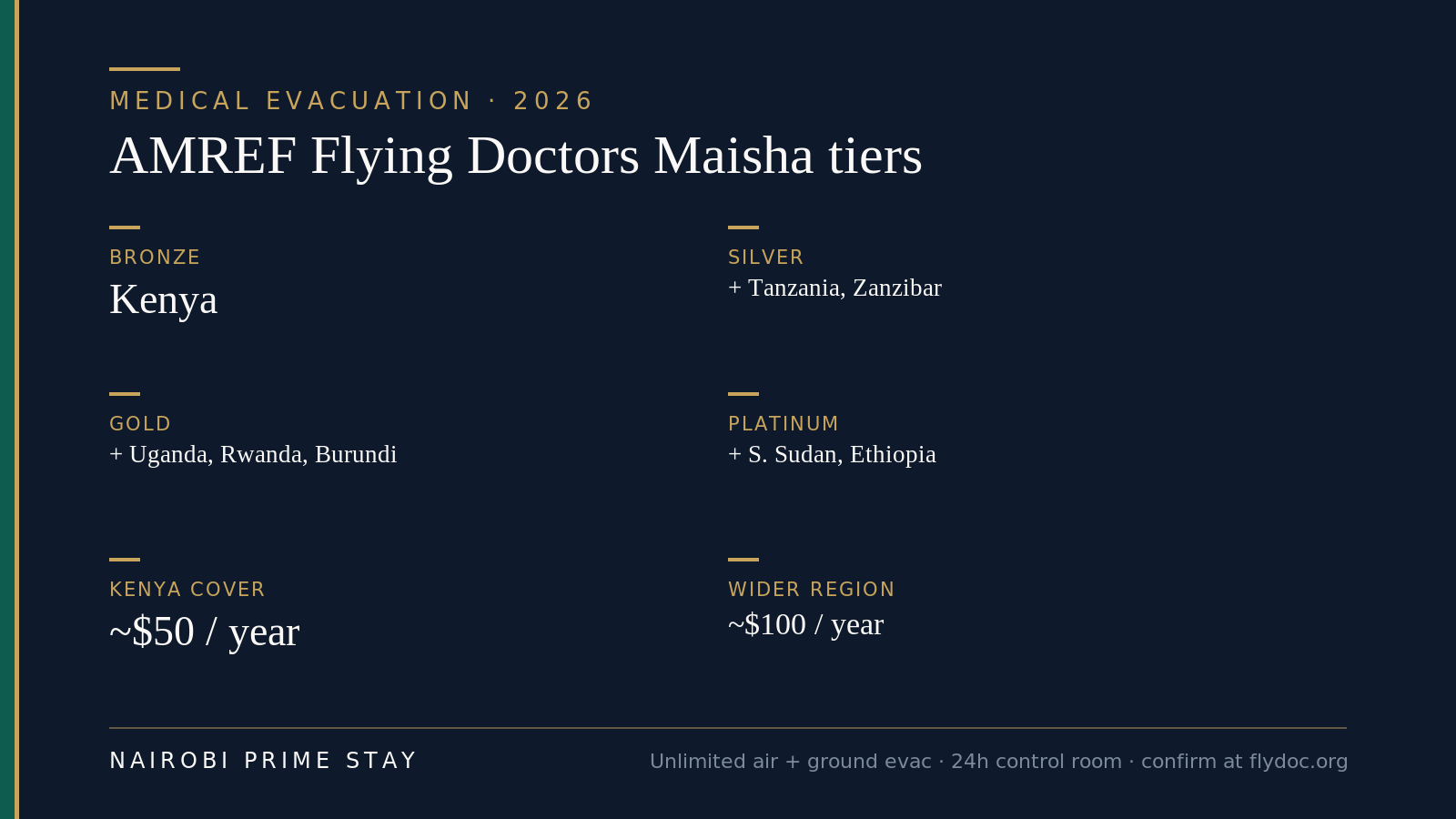

Evacuation cover is cheap relative to what it does. Confirm current Maisha tiers and prices at flydoc.org.

The best-known provider is AMREF Flying Doctors, whose Maisha membership covers unlimited emergency air and ground evacuation, backed by a 24-hour control room. It’s sold in tiers by how far the geographic cover stretches: Bronze (Kenya), Silver (Kenya, Tanzania and Zanzibar), Gold (adding Uganda, Rwanda and Burundi) and Platinum (adding South Sudan and Ethiopia). Annual membership is modest — roughly $50 a year for Kenya-level cover and around $100 for the wider region — which is tiny next to the cost of an unplanned medical flight. Confirm current tiers and prices at flydoc.org.

Two practical points. First, check whether your main health plan already includes evacuation or offers it as an add-on; many regional and international plans do, and you don’t want to pay twice. Second, evacuation cover gets you to the hospital — it doesn’t pay the hospital bill. You still need a health plan for the treatment itself. The two work together.

What it costs: premiums by age

Premiums rise with age, and they rise steeply later in life. The single biggest driver of your quote is your age, followed by the geographic scope (Kenya-only is cheapest, worldwide-with-US the most expensive), the annual limit, and whether you add outpatient, maternity, dental and optical. Two people the same age can pay very different premiums depending on those choices.

The bands below are indicative for 2026 and meant to set expectations, not to quote you. A broker will price your actual policy.

| Age band | Local / regional plan (per adult/yr) | International plan (per adult/yr) |

|---|---|---|

| 20s–30s | ~$1,000–2,200 | ~$2,500–5,000 |

| 40s | ~$1,800–3,200 | ~$3,500–6,500 |

| 50s | ~$2,800–4,800 | ~$5,000–9,000 |

| 60s+ | ~$4,500–8,000+ | ~$8,000–15,000+ |

A few things to know about how the money works:

- Inpatient vs outpatient. The core of any plan is the inpatient (hospital admission) limit. Outpatient — GP visits, tests, physio — is often a separate, capped add-on. Decide whether you want everyday cover or just protection against the big events.

- Deductibles and co-pays. Choosing a higher excess (the amount you pay first) lowers your premium. For a young, healthy person who mainly wants catastrophe cover, that can be a smart trade.

- Maternity has a waiting period. If a baby might be on the horizon, this matters a lot — see the costs and timing in our maternity care in Nairobi guide. Most plans make you wait 10–12 months before maternity benefits start, so buy early.

- Family plans. Insuring a family is cheaper per person than several singles, but children’s cover and school-age needs add up. Families should also read moving to Nairobi with kids.

- Currency. Local plans are priced in shillings, international plans usually in dollars, pounds or euros. With the dollar around KES 129–130 (129.4 on 1 July 2026), a shilling-priced plan can move with the exchange rate — see our cost of living guide for how that feeds the wider budget.

Pre-existing conditions

Be upfront about your medical history. Insurers handle pre-existing conditions in one of two ways, and which one you get shapes everything.

Full medical underwriting means you declare your history when you apply, and the insurer decides what to cover, what to exclude, and what to load (charge extra for). You get certainty: you know on day one what’s in and what’s out. Moratorium underwriting skips the questionnaire but won’t pay for any condition you had in a set look-back window (often five years) until you’ve gone a continuous stretch — typically two years — without symptoms, treatment or advice for it.

Whichever applies, the rule is the same: declare everything honestly. A non-disclosed condition is the fastest way to have a future claim denied, and that’s exactly when you can least afford it. If you take regular medication or manage a chronic condition — blood pressure, diabetes, thyroid, anything ongoing — ask specifically how the plan treats chronic-condition cover and whether your prescriptions are included. Older movers and retirees should weigh this most carefully; the right plan for you is the one that covers what you actually have. If a Kenya move is part of your retirement, our retire in Kenya guide walks through the wider planning.

How to choose the right plan

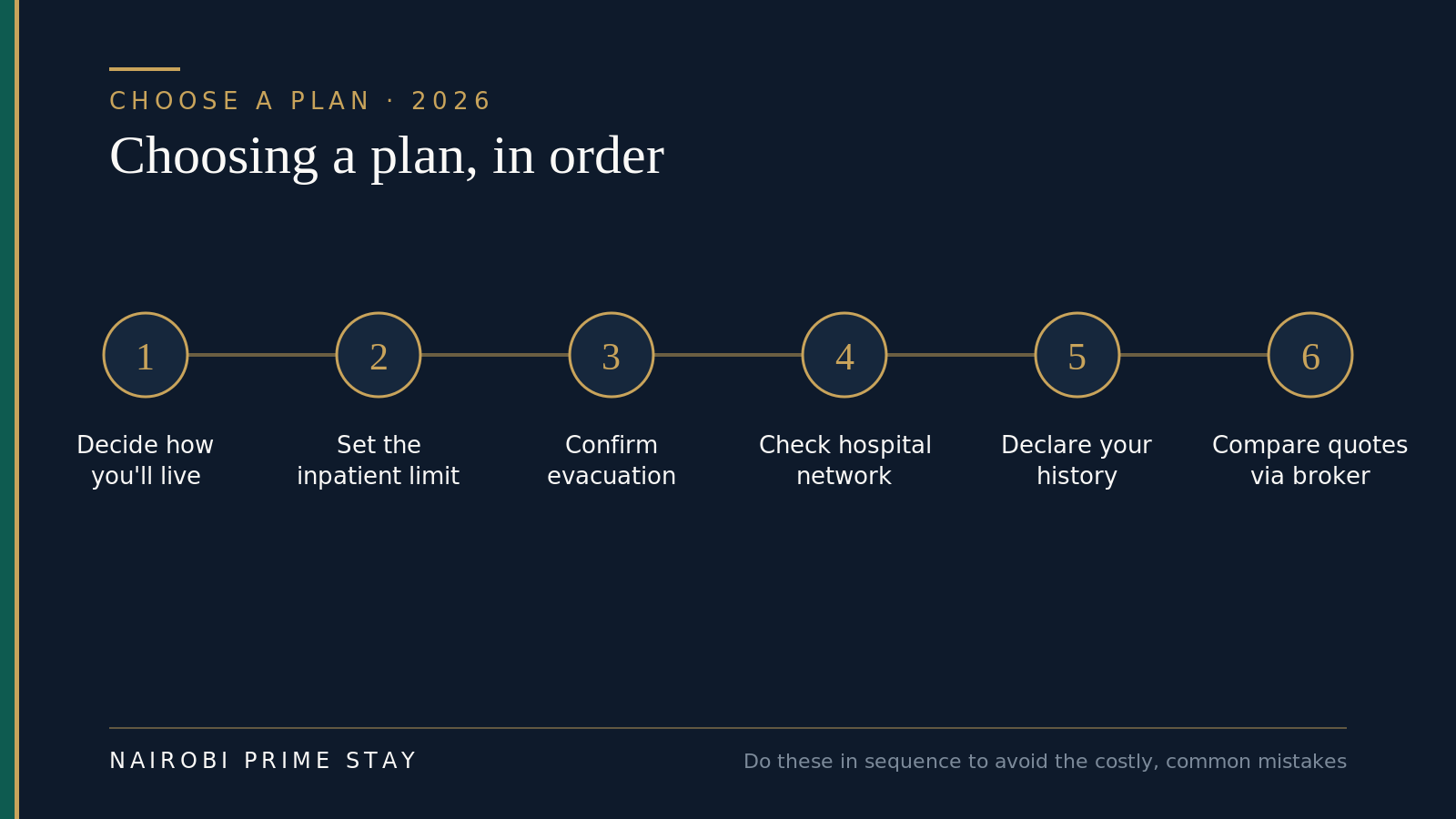

A simple order of operations. Do these in sequence and you’ll avoid the common, expensive mistakes.

Work through it in this order:

- Decide how you’ll actually live. Mostly in Nairobi? A strong local plan plus evacuation may be all you need. Traveling the region often, or want the option to fly home for major treatment? Lean international.

- Set the inpatient limit first. This is your protection against the big bill. Pick a limit you’d be comfortable with for a serious admission, then build outpatient and extras around it.

- Confirm medical evacuation is included or added. Don’t assume — check the wording, and check the geographic range matches where you’ll travel.

- Check the hospital network and direct billing. Make sure the plan bills directly at the private hospitals nearest your home — Aga Khan, Nairobi Hospital, MP Shah, Karen Hospital, Gertrude’s for kids. Our healthcare guide maps who’s where.

- Declare your full medical history and get the exclusions in writing before you pay.

- Compare written quotes through a broker. A good local broker who works with expats will line up several insurers, explain the fine print, and handle claims help later. Compare like-for-like limits, not just headline prices.

What to compare line by line: the annual inpatient limit, outpatient cover and its cap, maternity (and its waiting period), chronic and pre-existing terms, dental and optical, the evacuation provider and range, the direct-billing hospital list, the excess, and how much the premium jumps at each age band.

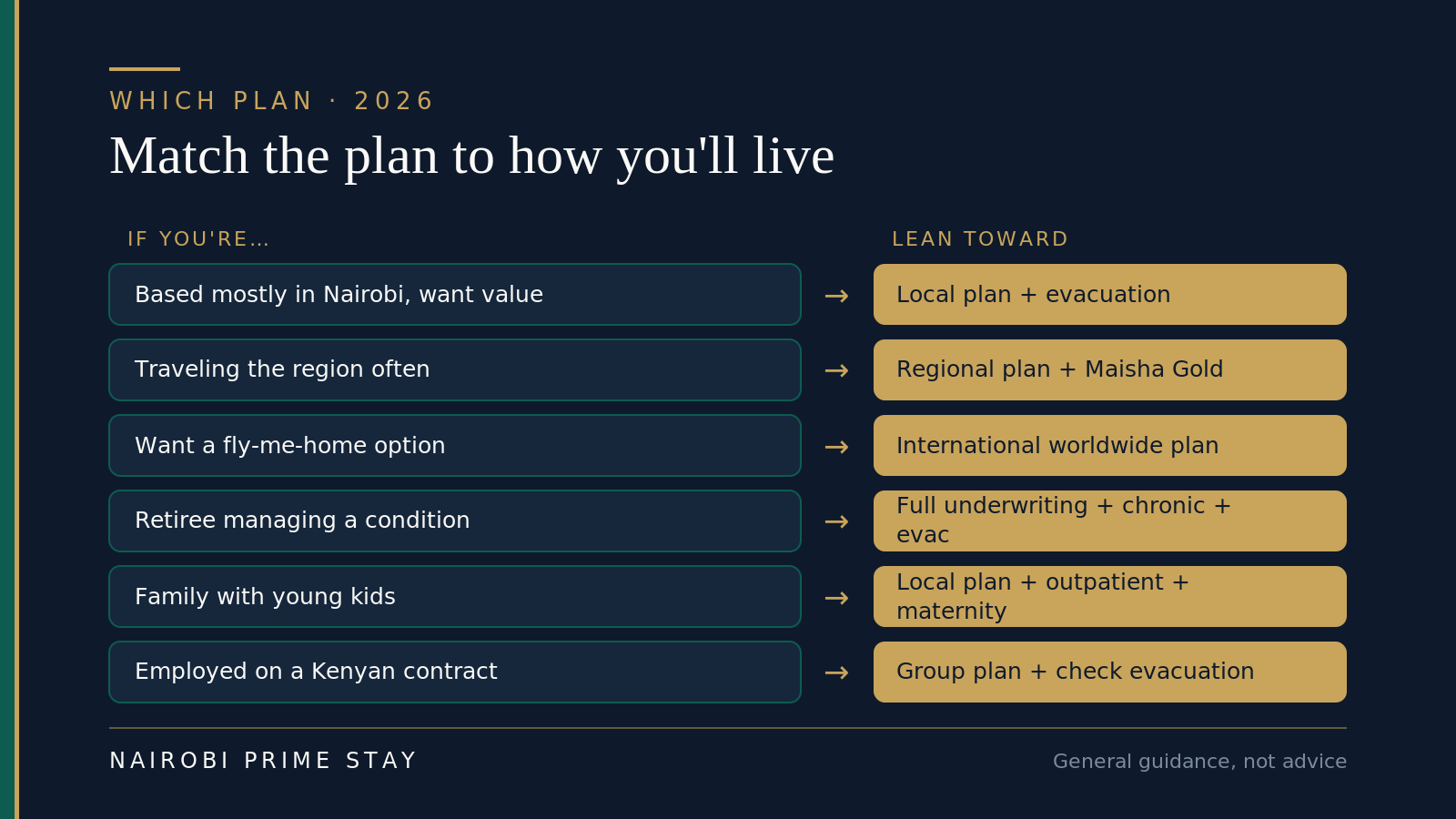

Match the plan to how you’ll live

General guidance, not advice. Your health, budget and travel patterns decide the right fit.

Three real-world examples

The retiree couple, both 64. They’ll be based in Karen, traveling within Kenya and occasionally home to the US. Their priorities are chronic-condition cover (he manages blood pressure), a generous inpatient limit, and rock-solid evacuation. They choose a regional plan with full medical underwriting so they know exactly what’s covered, add AMREF Maisha at the regional tier, and keep a separate travel policy for US trips. It isn’t cheap at their age, but it’s predictable.

The remote-working family of four. Two parents in their late 30s, two kids in school. They want everyday outpatient cover for the children, maternity benefit in case a third arrives, and direct billing at Gertrude’s and Aga Khan. A local family plan covers day-to-day care affordably; they add an evacuation membership and a modest international top-up for major events. They buy before arrival so the maternity waiting period is already running.

The employee on a Kenyan contract. Her company provides a group health plan — common for professional roles — and deducts SHA at 2.75% of her gross salary automatically. The group plan is decent, but she checks two things: whether it includes evacuation (it didn’t, so she added Maisha herself for about $50), and what happens to her cover if she leaves the job (it ends, so she lines up a personal plan as backup). If your move is tied to a work permit, see our Kenya visa guide for Americans for how employment and residence fit together.

International or local? An honest reckoning

Neither is “better.” They solve different problems. Here’s the trade-off laid out plainly.

| International (global) plan | Local / regional plan | |

|---|---|---|

| Strengths | Travels with you; covers treatment abroad; high limits; strong on complex, major treatment; portable if you move countries again | Much cheaper; excellent direct billing at Kenyan hospitals; built for local everyday care; claims handled locally |

| Weaknesses | Expensive, especially with age; can be more cover than a Nairobi-based life needs | Limited or no cover for planned treatment overseas; lower limits; evacuation often an add-on |

| Best if | You travel often, want a “fly me home” option, or have complex needs | You’ll be based mostly in Kenya and want value and good everyday care |

The pragmatic middle path most expats land on: a local plan plus evacuation, with an international top-up only if you genuinely need worldwide treatment. Don’t over-buy out of nerves, and don’t under-buy on evacuation.

Your health-insurance checklist

Work through this before you fly:

- Decided international, local, or a hybrid — based on how you’ll live, not fear.

- Inpatient limit set at a level you’d trust for a serious admission.

- Outpatient, maternity, dental and optical added or consciously declined.

- Medical evacuation confirmed in writing, with a geographic range that matches your travel.

- Direct billing checked at the private hospitals nearest your home.

- Full medical history declared; exclusions and any loadings in writing.

- Maternity waiting period started early if a baby is possible.

- Quotes compared like-for-like through an expat-savvy broker.

- If employed locally: checked whether the group plan includes evacuation and what happens if you leave.

- Cover active from your arrival date — not “starting next month.”

- SHA registration sorted if you’re on a Kenyan payroll (your employer usually handles it); current rules confirmed at sha.go.ke.

What changed with SHA in 2026?

Three things worth knowing if you arrived — or hired — this year. First, the registration duty moved to employers: as of 2026, companies are responsible for registering their staff with SHA, and that explicitly includes non-Kenyan employees on work permits, who contribute on the same terms as everyone else. Second, the mechanics are fixed and simple: 2.75% of gross salary, a minimum of KES 300 a month, no upper cap, deducted before tax and remitted by your employer by the 9th of the following month. On a $60,000 Nairobi salary that is roughly $1,650 a year — real money, so it belongs in your budget alongside the premium for your private plan; our cost of living guide shows where it sits in the bigger picture.

Third, the benefits side keeps moving. In 2026 the government made normal and caesarean delivery free at public Level 2 and 3 facilities under Legal Notice 78 — a genuine improvement to the public baseline, though most expats still deliver privately at Aga Khan or Nairobi Hospital, where the costs and the insurance waiting-period trap in our maternity guide apply. None of this changes the core advice: SHA is a legal baseline you comply with, not the cover you rely on. Rules shift — confirm the current position at sha.go.ke before you rely on any of it.

How do you buy a plan from the US before you fly?

Entirely doable, and better than waiting — cover that starts the day you land is the goal. Work backwards from your flight:

- Start 60–90 days out. Underwriting, questions about your medical history and back-and-forth on exclusions all take longer than you expect, and you want it settled before the movers arrive.

- Get two or three like-for-like quotes. Use an expat-savvy broker or go direct to insurers, but hold the inpatient limit, outpatient cap and evacuation terms constant so you are comparing plans, not headlines.

- Complete medical underwriting while you are still home. You have easy access to your doctors, records and prescription lists in the US; chasing paperwork across time zones after you move is miserable.

- Set the start date to your arrival date. Not “the first of next month.” The gap between landing and cover starting is exactly when an emergency is most expensive and most disorienting.

- Match the geographic scope to your real plans. If weekend trips to Zanzibar, Kigali or Kampala are on the list — see our East Africa regional travel guide — pick an evacuation tier and plan scope that follow you across borders.

- Load the proof into your phone. Digital member card, the insurer’s 24-hour pre-authorization number, your evacuation membership certificate and a photo of the policy schedule. That is what the admissions desk asks for.

One practical note on paying: international plans happily take a US card in dollars. Kenyan insurers usually want a local payment method at renewal — a Kenyan bank account or M-Pesa — which is one more reason to sort a bank account and M-Pesa in your first weeks.

How do claims and direct billing actually work?

Better than you might fear, if you set it up right. With a local or regional plan, you get a member card (increasingly an app) that the big private hospitals bill against directly: you show it at registration, the hospital invoices the insurer, and for outpatient visits you often pay nothing at the desk beyond any co-pay. Planned admissions need pre-authorization — the hospital and insurer agree the cover before you’re admitted — so call the member line as soon as an admission is discussed, not after.

With an international plan, everyday outpatient care is often pay-and-claim: you settle the bill, keep itemized invoices and receipts, and submit through the insurer’s app for reimbursement. For large inpatient events, international insurers can usually arrange direct settlement with the major Nairobi hospitals if you (or the hospital) call their assistance line before or at admission — that phone call is the difference between the insurer paying the hospital and you fronting a serious bill.

Two honest warnings. If you arrive at a private hospital with no card and no guarantee of payment, expect to be asked for a cash deposit on admission — private care here is pay-as-you-go, and the admissions desk means it. And keep every receipt for anything you pay out of pocket (M-Pesa and cards are accepted everywhere that matters); reimbursement lives and dies on paperwork. Our healthcare guide covers which hospitals to head for in the first place.

Final thoughts

Health insurance in Kenya looks complicated from a distance and turns out to be simple up close. Use the private system. Insure it properly. Make sure evacuation is in the package. Treat SHA as the small legal baseline it is, not your safety net. And buy before you land, so your first month is about settling in, not scrambling for cover after something goes wrong.

Get a couple of real quotes from a broker who works with expats, compare the limits rather than the headline price, and you’ll have this handled in a week. It’s the most important box you’ll tick on the whole move, and one of the easiest once you know what you’re looking at.

Related reading

- Start with the big picture in our complete guide to moving to Nairobi.

- See the hospitals and care quality behind the insurance in healthcare in Nairobi.

- Fit premiums into your monthly budget with the cost of living in Nairobi guide.

- Planning a family? Read maternity care in Nairobi and moving to Nairobi with kids.

- Looking after teeth, eyes and specialists? See dentists and specialists in Nairobi — honest 2026 costs and where to go.

- Retiring here? Our retire in Kenya guide covers the wider planning.

- Moving for work? See the Kenya visa guide for Americans.

When you arrive

A serviced apartment for your first weeks puts you somewhere secure and connected, close to the major private hospitals, while you finalize insurance, register with a doctor and find your feet. Browse our serviced apartments in Nairobi — honest monthly pricing with Wi-Fi, cleaning, a backup generator and security included; a $50 deposit reserves your dates and the balance is paid on arrival. Not sure which area keeps you closest to the right hospital and within budget? Our AI relocation assistant can shortlist options in a couple of minutes, day or night.

Frequently asked questions

Do expats need private health insurance in Kenya?

In practice, yes. Expats use Kenya’s private hospitals, and private care is pay-as-you-go, so without insurance you pay large bills up front and may be asked for a deposit before admission. A private plan — local, regional or international — with medical evacuation included is the standard setup for Americans living in Nairobi.

What does SHA (formerly NHIF) cover for foreigners in Kenya?

SHA, the Social Health Authority, runs the Social Health Insurance Fund that replaced NHIF in October 2024. If you are employed on a Kenyan contract you contribute 2.75% of gross salary, and the fund covers a defined benefits package aimed mainly at public and lower-tier facilities. It is a legal baseline, not a substitute for private cover at the hospitals expats actually use.

How much does expat health insurance in Kenya cost?

It depends mostly on your age, the geographic scope and the limits you choose. As a rough 2026 guide, a healthy adult might pay about $1,500 to $3,000 a year for a solid regional plan with evacuation, and about $3,000 to $8,000 or more for a full international plan; premiums rise steeply from your 50s onward. Get written quotes through a broker — the bands are a starting point, not a promise.

Should I get an international or a local health plan in Kenya?

Choose based on how you will live. A local or regional plan from a Kenyan insurer like Jubilee, AAR or Britam is much cheaper, has strong direct billing at local hospitals, and suits a mostly-Nairobi life; an international plan costs more but covers treatment abroad and travels with you. The pragmatic middle path many expats choose is a local plan plus a dedicated evacuation membership.

Why do I need medical evacuation cover in Kenya?

Because the best specialists cluster in a few Nairobi hospitals, and a serious emergency on the coast, upcountry or while traveling the region may require a flight to reach them. Evacuation cover pays for that air ambulance and the 24-hour coordination behind it; without it, an unplanned medical flight is a five-figure bill. Make sure it is included in your plan or added separately.

Does AMREF Flying Doctors Maisha replace health insurance?

No. AMREF Flying Doctors Maisha is evacuation cover, not health insurance. Its membership pays for unlimited emergency air and ground evacuation, backed by a 24-hour control room, but it does not pay the hospital bill once you arrive. Pair it with a health plan that covers the treatment itself.

How much does AMREF Maisha cost, and which tier do I need?

Maisha is sold in tiers by geography: Bronze covers Kenya, Silver adds Tanzania and Zanzibar, Gold adds Uganda, Rwanda and Burundi, and Platinum adds South Sudan and Ethiopia. Entry-level annual cover starts around KES 1,800, with the regional tiers roughly $50 to $100 a year as of July 2026, and every tier includes unlimited emergency evacuations. Match the tier to where you will actually travel and confirm current prices at flydoc.org.

Do foreigners on work permits have to pay SHA in 2026?

Yes. Non-Kenyan employees working in Kenya on a work permit must be registered with SHA, and as of 2026 that registration duty sits with the employer, who deducts 2.75% of gross salary — minimum KES 300 a month, with no upper cap — before tax and remits it by the 9th of the following month. Treat it as a payroll line, not your main cover; you still want a private plan for the hospitals you will actually use.

Can I arrange health insurance from the US before I arrive in Kenya?

Yes, and you should. Start 60 to 90 days before you fly: get two or three like-for-like quotes, complete the medical underwriting while you still have easy access to your records, and set the policy start date to your arrival date so you are covered from the moment you land. International plans can be bought in dollars with a US card; local insurers usually want a Kenyan bank account or M-Pesa once you are on the ground.

Will insurance cover pre-existing conditions in Kenya?

Sometimes, depending on the plan and how it is underwritten. With full medical underwriting you declare your history up front and the insurer tells you what is covered, excluded or loaded; with moratorium underwriting, recent conditions are excluded until you have gone a set period — often two years — without symptoms or treatment. Declare everything honestly, because non-disclosure is the fastest route to a denied claim.

Can I use my US health insurance in Kenya?

Usually not for ongoing care. Most US domestic plans, including Medicare, do not cover routine treatment overseas, so you generally need cover bought for expat life — an international plan or a Kenyan private plan. Some US travel policies cover emergencies on short visits, but they are not a substitute once you actually live here.

Ready to look?

Find your apartment in Nairobi

Browse verified serviced apartments, or ask the AI concierge which area fits your life.